Breathalyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

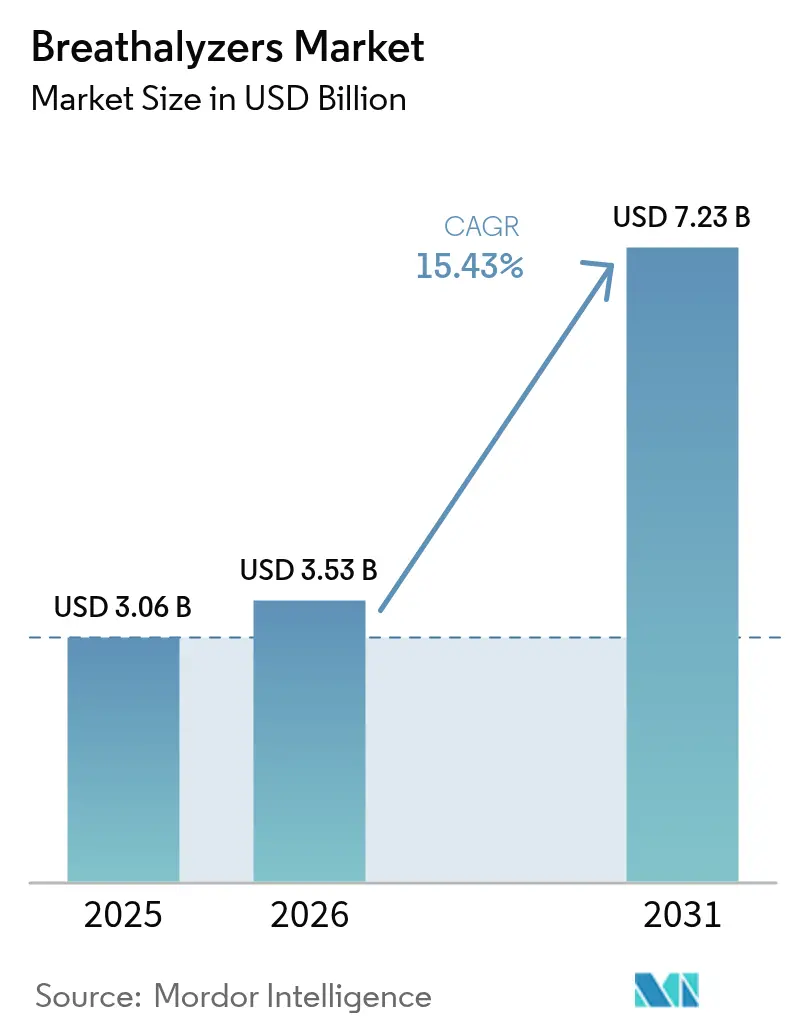

| Market Size (2026) | USD 3.53 Billion |

| Market Size (2031) | USD 7.23 Billion |

| Growth Rate (2026 - 2031) | 15.43% CAGR |

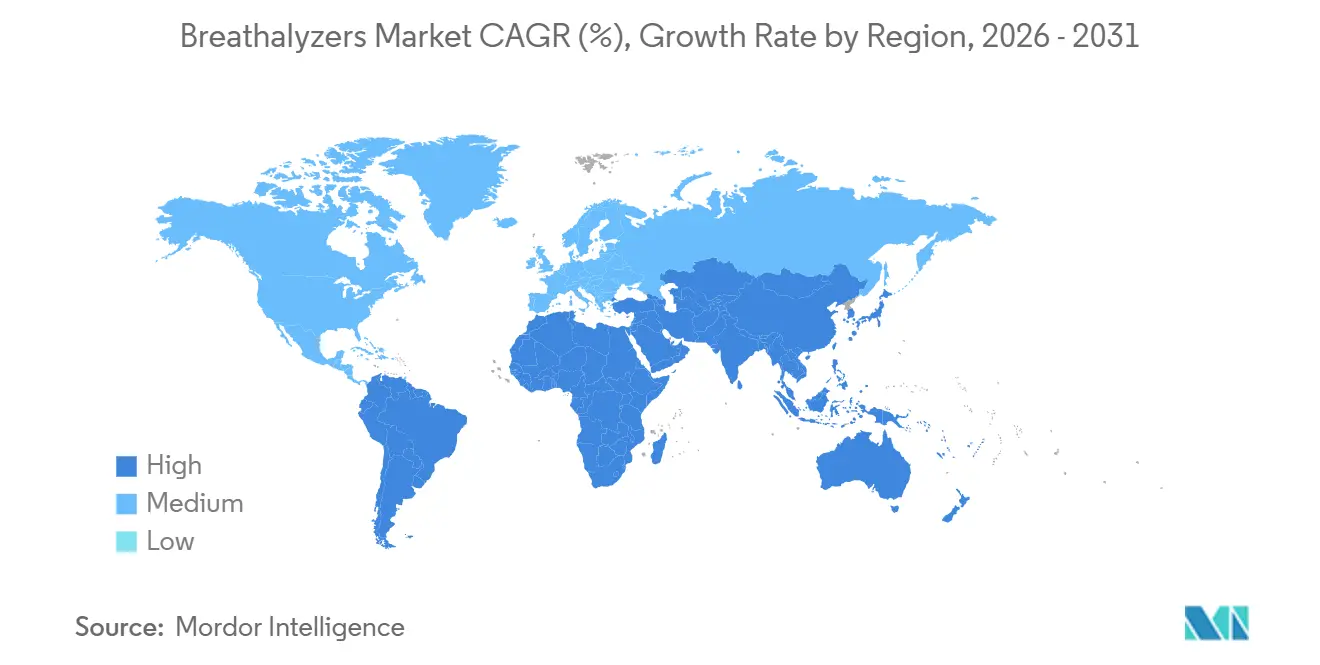

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breathalyzers Market Analysis by Mordor Intelligence

Breathalyzers market size in 2026 is estimated at USD 3.53 billion, growing from 2025 value of USD 3.06 billion with 2031 projections showing USD 7.23 billion, growing at 15.43% CAGR over 2026-2031. Expanding ignition-interlock mandates across major economies keep a steady flow of orders for professional-grade units and sustain long-term service contracts for recalibration. At the same time, miniaturized, smartphone-linked models are opening a consumer channel that moves the market beyond deterrence and into everyday self-monitoring. Manufacturers are also being pulled toward healthcare as breath-based disease diagnostics gain scientific backing, prompting new partnerships between traditional safety firms and medical-device specialists. These overlapping opportunities are encouraging strategic investments in sensor accuracy, connectivity, and cloud analytics, while also blurring the line between public-sector and retail demand. Competitive differentiation is therefore shifting from hardware alone to integrated ecosystems that promise continuous compliance and actionable data.

Key Report Takeaways

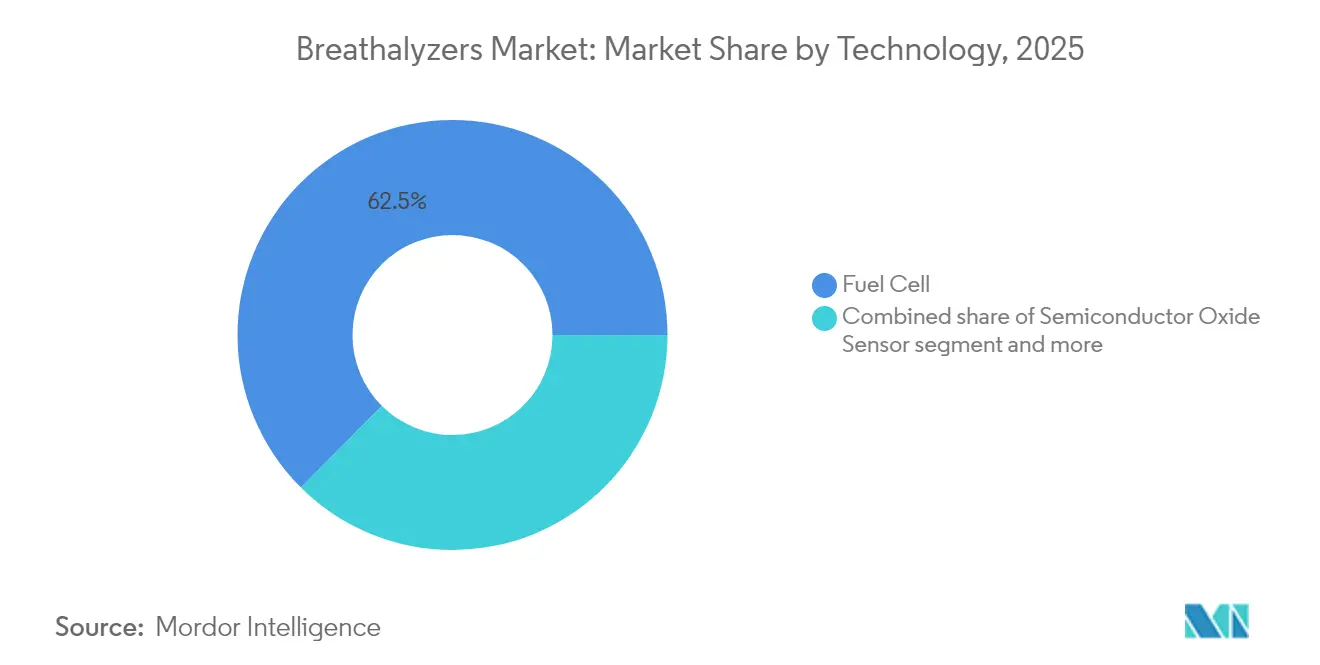

- By technology, fuel cell sensors held a 62.54% share of the breathalyzer market in 2025, while infrared spectroscopy is projected to grow at a 18.92% CAGR to 2031.

- By product type, hand-held/portable devices accounted for 53.76% of 2025 revenue, whereas smartphone plug-in breathalyzers are forecast to register a 21.02% CAGR through 2031.

- By distribution channel, direct tenders/contracts controlled 47.22% of sales in 2025, yet online stores are set for the fastest growth at a 23.18% CAGR during 2026-2031.

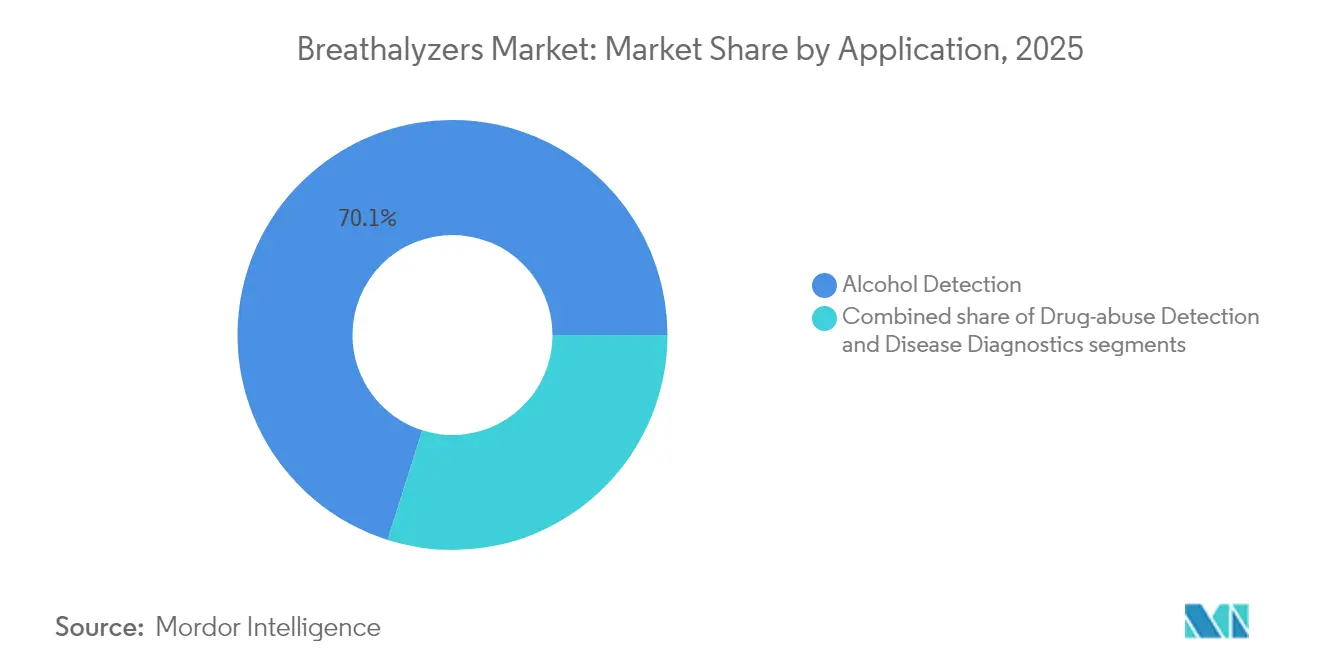

- By application, alcohol detection represented 70.12% of the breathalyzer market size in 2025, and disease diagnostics is advancing at a 21.44% CAGR to 2031.

- By end-user, law enforcement agencies captured 39.12% market share in 2025, while personal consumers are expected to expand at a 19.52% CAGR over the forecast period.

- By geography, North America led global revenue in 2025 with 41.25% of market share, while Asia-Pacific is anticipated to post the quickest gains with 17.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breathalyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening DUI legislation and Expansion of ignition-interlock mandates | +8.0% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Rising Technological Advancements and Increasing Funding | +5.3% | Global, with highest impact in high-income regions | Medium term (2-4 years) |

| Miniaturized smartphone-connected devices | +3.5% | Global, with highest impact in high-income regions | Short term (≤ 2 yrs) |

| Corporate zero-alcohol workplace policies | +2.5% | Global, with highest impact in industrial economies | Medium term (2-4 years) |

| Breath-based disease-diagnostics funding | +1.8% | North America, Europe, advanced Asian economies | Long term (≥ 4 years) |

| Usage-based-insurance sober-driving programs | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening DUI Legislation and Expansion of Ignition-Interlock Mandates

National and sub-national authorities continue to lower acceptable blood-alcohol content (BAC) thresholds, sustaining demand momentum for evidential Breathalyzer market equipment. Expansion of ignition-interlock mandates in 31 US states[1]National Conference of State Legislatures, “State Ignition Interlock Laws,” NCSL, ncsl.org ensures a recurring equipment replacement cycle, while similar legal tightening in South Korea and parts of Europe reinforces a dependable order pipeline. Utah’s 0.05% limit and South Korea’s revised Road Traffic Act illustrate a wider policy pivot. As legal frameworks converge on “all-offender” ignition-interlock schemes, device volume per offender rises, a dynamic that indirectly elevates service revenues from calibration programs. In practice, suppliers that offer mobile field-service vans cut downtime for probationers, which both courts and offenders find appealing. The trend implies that distributors with robust after-sales networks could capture disproportionate breathalyzers market share, especially where offenders must prove compliance before license reinstatement.

Rising Technological Advancements and Increasing Funding

Miniaturized fuel-cell sensors coupled with Bluetooth deliver laboratory-grade accuracy in palm-sized housings, encouraging repeat use by non-technical consumers. Concurrently, venture investment in breath-based oncology screening has surged, signalling a path for cross-subsidizing research costs with alcohol-testing cash flow. Manufacturers that license diagnostic IP therefore secure early optionality in adjacent health markets without diluting their breathalyzer industry identity. Investment analysts note that this diversification reduces revenue cyclicality tied to DUI enforcement budgets, making publicly traded suppliers more attractive to institutional investors.

Corporate Zero-Alcohol Workplace Policies

High-risk sectors such as construction and logistics are formalizing zero-tolerance rules, and insurers increasingly require proof of policy enforcement.[3]International Alliance for Responsible Drinking, “IARD Launches Resources to Support Workplace Alcohol Policies,” IARD, iard.org Employers cite liability exposure as the primary trigger, turning breathalyzer units into a cost-effective risk-mitigation tool. A fresh inference is that hybrid work schedules complicate random testing, prompting interest in connected devices that employees can operate at home. Providers integrating cloud dashboards now enjoy a competitive edge, as policy auditors favor verifiable digital logs. Several manufacturers have responded by launching subscription portals that provide anonymized usage analytics to human-resources teams, effectively transforming a one-time purchase into a recurring revenue stream.

Usage-Based-Insurance Sober-Driving Programs

Insurers piloting premium discounts for drivers who log regular zero-BAC readings reveal a new revenue corridor for device makers. Since each policy may require monthly verification, subscription data services become as lucrative as hardware sales. The market’s response shows that motorists accept mild privacy intrusions when economic incentives are clear. Telematics platforms that already collect speed and braking data find integration straightforward, because breath-test timestamps simply join existing metadata strings. Early actuarial studies indicate a noticeable drop in alcohol-related claims, reinforcing carrier enthusiasm.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy variability in low-cost sensors | -2.1% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) |

| High life-cycle calibration/consumable cost | -1.5% | Global, with highest impact in emerging economies | Medium term (2-4 years) |

| Data-privacy & liability concerns (GDPR, HIPAA) | -1.2% | Europe, North America | Medium term (2-4 years) |

| Competition from camera / wearable impairment tech | -0.7% | Global, with highest impact in advanced economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Life-Cycle Calibration and Consumable Costs

Annual calibration charges and replaceable mouthpieces still deter small fleets from upgrading to professional-grade units. However, recent state subsidies covering up to 50% of ignition-interlock fees in Louisiana demonstrate that public funding can neutralize this barrier. An observable outcome is rising interest in “as-a-service” models that bundle maintenance into a flat monthly rate, smoothing cash flow for price-sensitive buyers. Some vendors now employ predictive maintenance algorithms that flag sensors likely to drift out of tolerance, allowing proactive recalibration and reducing costly evidence disputes.

Competition from Camera / Wearable Impairment Tech

Computer-vision systems detecting facial cues of impairment reach 75% accuracy in early trials. Although promising, fleet managers still require confirmatory breath data before disciplining staff, preserving the breathalyzers market’s incumbency. The co-existence of passive and active screening tools points toward integrated dashboards that flag anomalies and prompt breath checks only when risk escalates. Over time, this layered approach may lift total safety-technology spend per vehicle, indirectly boosting breathalyzer unit sales rather than cannibalizing them.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Fuel Cell Dominance Faces Infrared Challenge

Fuel cell sensors held 62.54% of the breathalyzers market share in 2025, underscoring their status as the evidential benchmark for police and court systems. Agencies confirm that fuel-cell units show minimal cross-reactivity with acetone, a finding that directly underpins admissibility in legal proceedings. A notable consequence is that budget cuts rarely affect replacement cycles for this specific technology, safeguarding vendor revenue streams even during downturns. Meanwhile, semiconductor oxide sensors retain relevance because novice users value low sticker prices over ultimate precision, keeping this category profitable in consumer retail.

Infrared spectroscopy’s market size is forecast to expand by a 18.92% CAGR between 2026-2031, narrowing the historical gap with fuel-cell solutions. Recent uncooled micro-bolometer arrays reduce power draw, letting manufacturers design battery-operated infrared handhelds that were not commercially feasible five years ago. This shift enables multi-substance detection, suggesting future devices may scan for both alcohol and controlled drugs in a single breath. Start-ups exploring carbon-nanotube coatings could leapfrog both incumbent technologies by offering trace-level sensitivity without frequent calibration, and developmental prototypes already demonstrate promising baseline stability over 12-month test horizons.

By Product Type: Portability Drives Market Evolution

Hand-held breathalyzers market size accounted for 53.76% of revenue in 2025, thanks to ease of use in roadside scenarios. Police officers note that lightweight casings accelerate traffic-stop throughput, indirectly freeing patrol resources for other duties. For consumers, keychain models double as novelty items at social events, creating viral word-of-mouth that free-rides on social media platforms. Standardization around USB-C charging further lifts user satisfaction, suggesting that ancillary accessory sales (cables, power banks) will follow hardware adoption.

Smartphone plug-in devices are projected to secure a 21.02% CAGR, rewriting the breathalyzers industry revenue mix. Integration with wellness apps means a single reading feeds into broader health dashboards, weaving alcohol data into daily fitness routines. Desktop units remain indispensable in booking stations because they withstand heavy use and connect to secure databases, but their growth is inherently tied to public-sector budget cycles. Continuous-wear biosensors like transdermal wristbands introduce a passive alternative, yet early adopters still purchase traditional breath devices as a verification fallback given regulatory familiarity.

By Distribution Channel: E-Commerce Disrupts Traditional Channels

Direct tenders held 47.22% share in 2025, reflecting bulk orders from the government and large enterprises. Procurement officers prefer contract bundles that guarantee onsite calibration, generating predictable service revenue for vendors. The locked-in nature of tenders creates high switching costs, implying that incumbents who win framework agreements enjoy multiyear cash flows and can amortize R&D across stable demand.

Online stores represent the fastest-growing channel with a forecast 23.18% CAGR as consumers turn to comparison sites before purchase. Free shipping and easy returns mitigate perceived risk, which is crucial for a technical product aimed at non-experts. Marketplaces also allow small brands to compete on equal footing with legacy manufacturers, expanding the overall breathalyzer market size rather than simply cannibalizing retail shelves. Physical specialty outlets still attract professional buyers who want hands-on calibration demos, revealing a hybrid distribution landscape rather than a zero-sum shift to digital.

By Application: Disease Diagnostics Emerges as Growth Frontier

Alcohol detection commands roughly 70.12% of the breathalyzers market size in 2025 and continues to be the anchor revenue stream because regulatory demand is non-discretionary. Each time a jurisdiction lowers the legal BAC limit, the installed base refreshes to meet stricter accuracy tolerances. Employers in petrochemical plants reinforce this baseline by mandating random testing before shift handover, which internal audits show reduces lost-time injuries.

Disease diagnostics exhibits a forecast 21.44% CAGR, positioning itself as the fastest-growing breathalyzers industry segment. Pilot programs showing reliable liver-disease biomarker detection have attracted cross-industry collaboration between breath sensor firms and hospital networks. One emergent outcome is that clinical researchers now request modular firmware updates to comply with evolving medical-device regulations. As data privacy legislation tightens, vendors offering on-device encryption for health analytics could unlock premium pricing tiers, because hospitals prefer solutions that minimize patient-data transit outside institutional firewalls.

By End-User: Personal Consumers Drive Future Growth

Law-enforcement agencies accounted for 39.12% of the breathalyzers market share in 2025, anchored by federal conformity lists that drive brand selection. Fleet-wide hardware upgrades usually align with budget cycles, producing a predictable revenue cadence for established suppliers. Centralized evidence-management needs mean agencies prioritize devices with secure data-export functions, raising software-licensing income and boosting aftermarket contract value.

Personal consumers are expected to register a 19.52% CAGR, expanding their share of the overall breathalyzers market size through 2031. Increasing ride-share usage has heightened awareness of personal liability, prompting individuals to self-test before calling a driver. A subtle yet measurable effect is that social hosts now keep pocket testers alongside drink mixers, promoting responsible entertainment culture. Rehabilitation centers, universities, and military units form a smaller but steady “other end-users” category, generating demand for tamper-proof logging systems that blend alcohol and drug-abuse monitoring.

Geography Analysis

North America remained the most significant regional contributor to the breathalyzer market size with 41.25% share in 2025, catalyzed by federal infrastructure legislation that obliges automakers to integrate impaired-driving prevention technologies. That mandate, while vehicle-centric, indirectly stimulates aftermarket breathalyzer sales as public discourse spotlights alcohol safety. Canada’s emergence as an R&D hub creates spill-over effects: domestic suppliers secure early-adopter trials that later translate to export orders, tightening the regional feedback loop between innovation and commercialization. Evidence suggests that insurers in both countries are experimenting with telematics-linked sober-driving discounts, a move likely to sustain consumer segment growth and elevate data-analytics demand.

Europe ranks second in breathalyzer industry revenue, with France’s requirement for motorists to carry disposable testers illustrating how policy nuances influence unit volumes. GDPR compliance pushes vendors to embed advanced anonymization protocols into connected devices, inadvertently upgrading global product standards. A new observation is that cross-border truck fleets adopt pan-European testing guidelines to avoid logistical confusion, creating multi-country bulk orders that favor manufacturers with multilingual software interfaces. The region’s aging demographic also elevates medical breath-diagnostics demand, as early detection aligns with preventive-health policy goals that curb long-term healthcare costs.

Asia-Pacific records the fastest forecast CAGR with 17.12% to 2031, as rising disposable incomes intersect with stricter traffic enforcement. China’s high-profile anti-drunk-driving campaigns have moved roadside testing from sporadic to routine, swelling public-sector orders. Japan’s zero-tolerance stance stimulates technological experimentation; local firms are piloting cabin-embedded sensors that auto-lock ignition if alcohol is detected. India shows latent demand in workplace safety, where multinational corporations apply uniform global policies that exceed local legal minimums. The region is also witnessing government encouragement for low-cost sensor innovation, suggesting that home-grown suppliers may soon challenge Western incumbents on price without sacrificing core accuracy, thereby reshaping competitive equations.

Competitive Landscape

The breathalyzers market is moderately concentrated, yet competitive intensity is climbing as medical-device specialists enter with diagnostic solutions. Drägerwerk AG & Co. KGaA leverages a century-plus heritage in safety engineering, positioning its products as the evidential gold standard. Recent financial disclosures show growing earnings resilience, implying operational efficiencies that could support forthcoming R&D into multi-analyte breath screening. An immediate implication is that smaller rivals may need alliances to match Dräger’s global calibration infrastructure or risk declining visibility in high-value tender lists.

BACtrack differentiates via consumer-oriented design and FDA 510(k) clearance on select models, reinforcing brand trust among non-professional buyers. Its proprietary Xtend Fuel Cell Sensor underpinning both portable and wearable offerings affords a scalable platform, enabling rapid iteration without full re-certification. Market observation suggests that BACtrack’s app ecosystem acts as a customer-retention moat, as historical readings encourage repeat engagement and mouthpiece re-orders.

Emerging players such as Owlstone Medical target high-margin diagnostic niches, applying Breath Biopsy technology to oncology and liver-disease detection. Their entry signals a strategic fork in the competitive landscape: while traditional vendors refine accuracy for alcohol policing, newcomers prioritize biomarker libraries and clinical partnerships. The intersection of these priorities could birth collaborative models where forensic devices double as health-screening platforms, creating a multi-tier product hierarchy that satisfies both safety regulators and healthcare providers.

Breathalyzers Industry Leaders

Alcohol Countermeasure Systems Corp.

Alcolizer Technology Pty Ltd

BACtrack (KHN Solutions)

Drägerwerk AG & Co. KGaA

Intoximeters Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Owlstone Medical reported further validation of Breath Biopsy for early disease detection and is engaging clinical partners to accelerate regulatory submissions. Two discrete biomarker panels advanced to late-stage trials, underscoring breath diagnostics’ commercial viability.

- January 2025: Intelligent Bio Solutions teamed with IVY Diagnostics to penetrate Europe’s USD 3.6 billion drug-screening sector, structuring the agreement to include Middle-East distribution rights for breath-and-saliva test kits.

- January 2025: Cannabix Technologies unveiled a lighter Breath Collection Unit featuring a rechargeable battery, improving ergonomics for marijuana breathalyzer field trials.

- November 2024: Alivion began collaborative studies with University Hospital Zurich on SmartSelect breath analysis and opened a CHF 1 million financing round to fund miniaturization efforts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the breathalyzers market as every handheld, desktop, and in-vehicle instrument that measures breath-alcohol concentration through fuel-cell, semiconductor, or infrared sensors and converts the result into an equivalent blood-alcohol value. According to Mordor Intelligence, this universe generated USD 3.06 billion in revenue in 2025 (mordorintelligence.com).

Scope exclusion: Devices that analyze exhaled breath for gases unrelated to ethanol (for example, hydrogen sulfide or acetone) and full laboratory gas-chromatography systems are excluded.

Segmentation Overview

- By Technology

- Fuel Cell

- Semiconductor Oxide Sensor

- Infrared Spectroscopy

- Others

- By Product Type

- Hand-held / Portable

- Desktop / Stationary

- Others

- By Distribution Channel

- Direct Tender / Contracts

- Retail & Specialty Stores

- Online Stores & E-commerce

- By Application

- Alcohol Detection

- Drug-abuse Detection

- Disease Diagnostics

- By End-User

- Law-Enforcement Agencies

- Hospitals & Clinics

- Workplace / Industrial

- Personal Consumers

- Other End-Users

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed traffic-safety officers, workplace-safety managers, hospital biomedical engineers, distributors, and sensor suppliers spread across North America, Europe, and Asia-Pacific. These conversations verified price dispersion, fleet replacement cycles, and the uptake of smartphone-linked units, closing data gaps left by desk research.

Desk Research

We began with trade flows under HS 902710 and 902720, drunk-driving statistics from the National Highway Traffic Safety Administration, EU road-safety scoreboards, and WHO Global Health Observatory accident data. Supplementary evidence came from the International Association of Chiefs of Police, peer-reviewed journals on sensor accuracy, and company filings accessed through D&B Hoovers and Dow Jones Factiva. These sources established shipment volumes, average selling-price corridors, and regulatory pacing. The sources named illustrate our mix; many additional open and subscription references helped round out facts and context.

Market-Sizing & Forecasting

We rely on a top-down model that starts with each country's roadside-test penetration and enforcement intensity, multiplies them by average unit life, and then values demand using current price bands. Selective bottom-up checks, aggregated vendor shipments and channel ASP samples, validate and adjust totals. Key model drivers include annual roadside test volumes, ignition-interlock mandates, accident trends, sensor cost curves, exchange-rate movements, and personal-use adoption rates. A multivariate-regression forecast, stress-tested through scenario analysis, projects figures to 2030. Where supplier data were sparse, regional enforcement benchmarks from primary research filled the gap before reconciling with trade statistics.

Data Validation & Update Cycle

Outputs pass dual-layer analyst reviews, anomaly checks against independent accident and import datasets, and re-contact with experts when disparities surface. Models refresh annually, with interim updates after material regulatory or technology events, ensuring clients always receive our latest view.

Why Mordor's Breathalyzers Market Baseline Offers Unmatched Decision Support

Published estimates often diverge; one open study pegs the 2023 market at USD 2.6 billion, another claims USD 14.91 billion for 2025, while a third puts 2025 at USD 4.36 billion. We acknowledge such spread so readers see why numbers differ.

Key gap drivers include broader product scopes that bundle drug-testing analyzers, older base-year anchoring, reliance on shipment press releases without price validation, and static currency conversions. Our scope remains focused on ethanol breath testing devices; we refresh every twelve months, and we ground prices in interview-backed samples.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 3.06 B (2025) | Mordor Intelligence | - |

| 2.60 B (2023) | Regional Consultancy A | Narrow scope, older base year, limited primary validation |

| 14.91 B (2025) | Global Consultancy B | Bundles drug-testing and in-vehicle sensors, GDP-based scaling |

| 4.36 B (2025) | Trade Journal C | Constant 2022 exchange rates, vendor press-release volumes |

This comparison shows that our disciplined scope selection, currency alignment, and interview-anchored pricing deliver a transparent, balanced baseline that decision-makers can replicate with confidence.

Key Questions Answered in the Report

What is the current value of the Breathalyzers Market?

The Breathalyzers Market is valued at USD 3.53 billion in 2026.

How are ignition-interlock mandates shaping supplier strategies?

Vendors increasingly bundle long-term calibration and data-reporting services with each device to meet court monitoring requirements and secure recurring revenue.

Why are employers in high-risk industries adopting workplace breath-testing programs?

Companies view on-site or remote alcohol screening as a simple way to reduce liability exposure and satisfy insurer expectations for demonstrable safety controls.

What technological shift is expanding the role of breathalyzers in healthcare?

Advances in breath-based biomarker detection allow the same core sensor platforms to screen for metabolic or liver conditions, attracting medical-device partnerships.

How are online sales channels influencing competition among breathalyzer brands?

E-commerce lowers barriers for niche entrants, so established manufacturers differentiate with cloud analytics, extended warranties, and easier at-home calibration options.

In what way could vehicle integration affect future demand for stand-alone breathalyzers?

Factory-installed impairment-detection systems may become standard, but portable units remain essential for probation monitoring, fleet audits, and personal verification outside the car.

What is driving the growing use of smartphone-linked breathalyzers among consumers?

Compact fuel-cell sensors now pair seamlessly with mobile apps, letting individuals track sobriety and receive real-time feedback, which makes self-testing both convenient and engaging.

Page last updated on: