Large Format Printers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.92 Billion |

| Market Size (2031) | USD 13.49 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

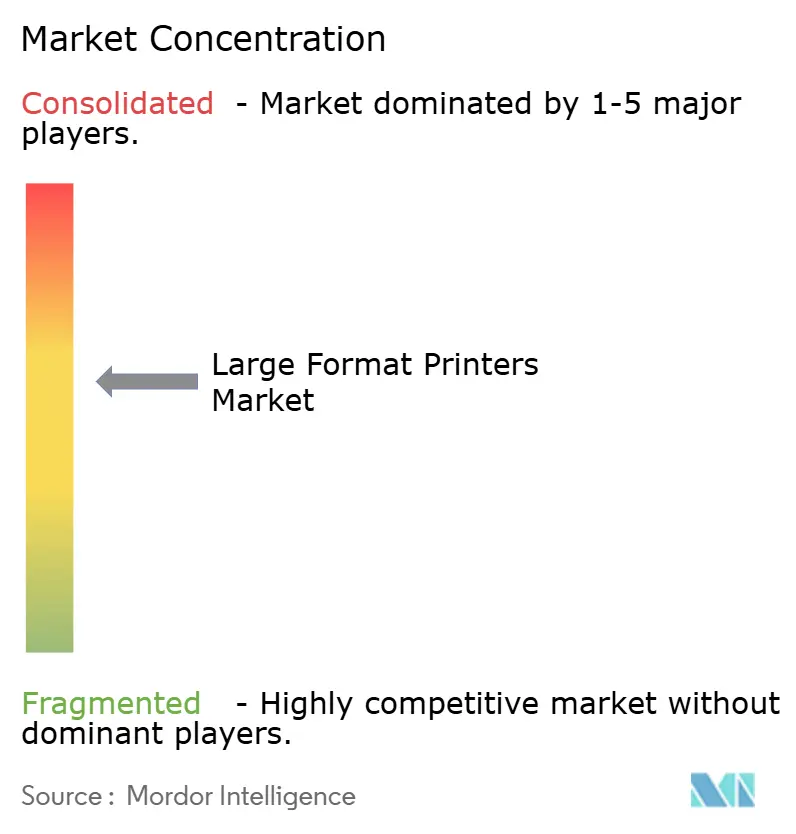

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Large Format Printers Market Analysis by Mordor Intelligence

The large format printers market size is projected to increase from USD 10.47 billion in 2025 to USD 10.92 billion in 2026 and reach USD 13.49 billion by 2031, growing at a CAGR of 4.32% during 2026-2031. The measured headline growth masks a deeper pivot toward service-centric procurement models, in which integrated contracts bundle hardware, consumables, and AI-driven workflow software into predictable operating expenses. Industrial buyers are compressing refresh cycles and shifting obsolescence risk to vendors, a move that is broadening adoption among small- and medium-sized print shops that could not previously justify capital expenditures. Sustainability mandates are simultaneously reshaping ink demand, with water-based latex formulations gaining traction in indoor graphics while UV-curable chemistries retain an edge in high-throughput, mixed-substrate environments. Regional demand is diverging: Asia-Pacific leads in volume, the Middle East posts the fastest growth as infrastructure projects proliferate, and North America navigates cost pressure from import duties that inflate the prices of consumables.

Key Report Takeaways

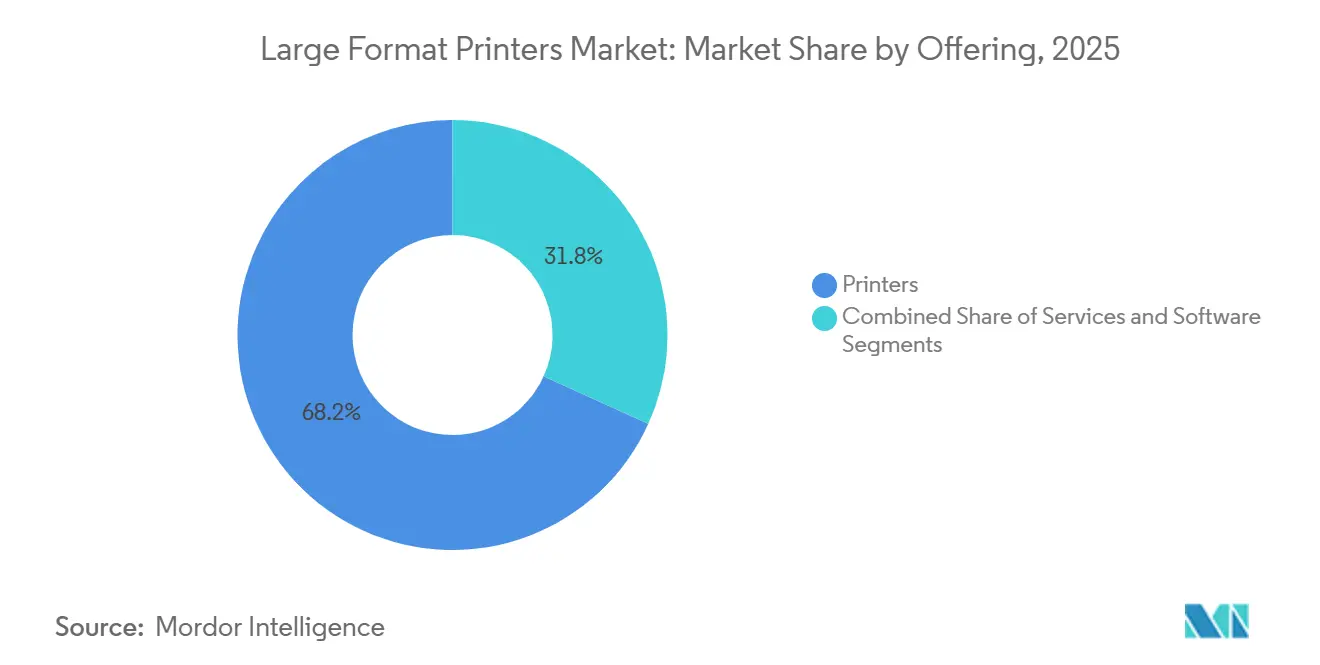

- By offering, printers led with 68.23% revenue share in 2025, while services are projected to grow fastest at a 4.91% CAGR through 2031.

- By printing technology, inkjet captured 79.41% of the large format printers market share in 2025, and is expected to post the highest 4.74% CAGR over 2026-2031.

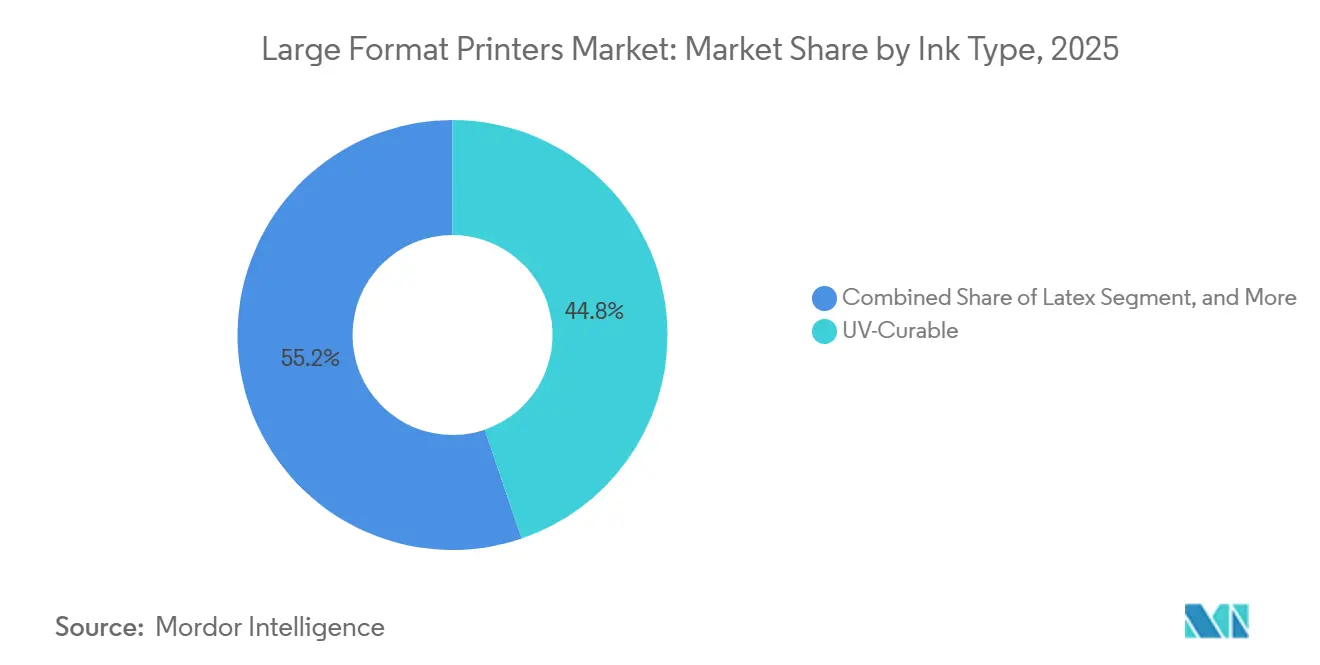

- By ink type, UV-curable inks accounted for 44.78% of the market in 2025, whereas latex formulations are forecast to expand at a 5.37% CAGR during the same period.

- By end-user industry, signage and outdoor advertising dominated with a 36.92% of the large format printers market share in 2025, while apparel and textiles are set to advance at a 5.56% CAGR to 2031.

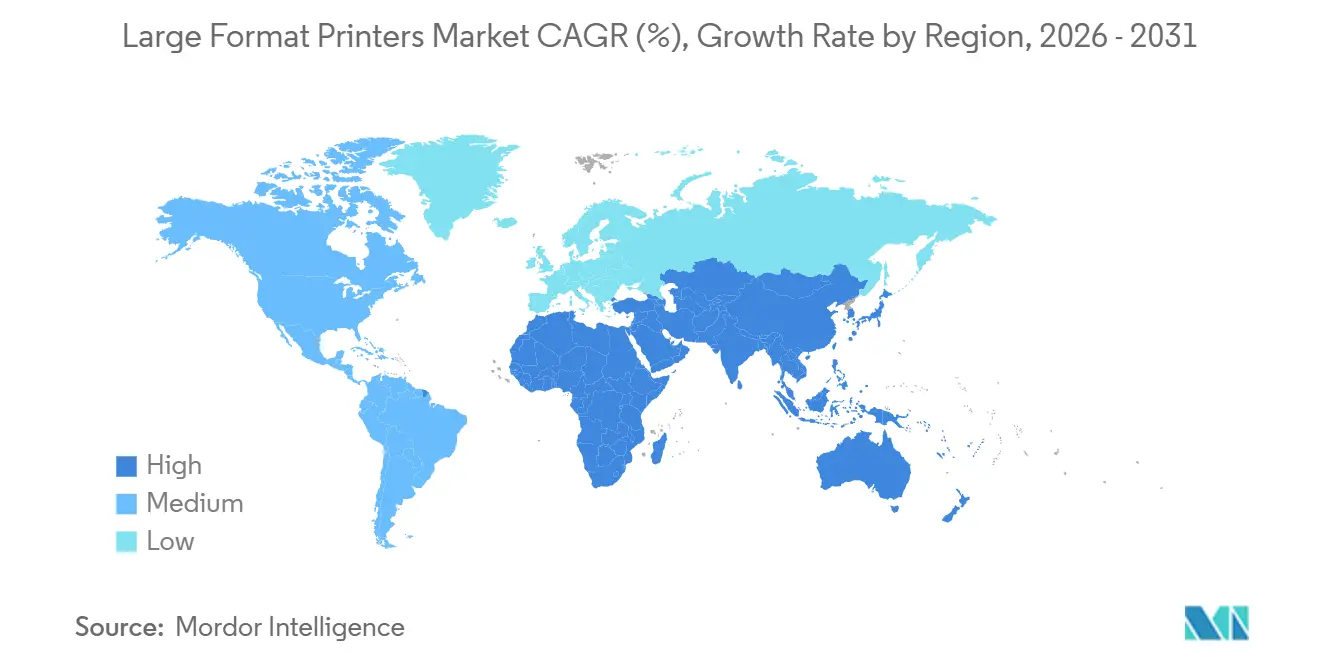

- By geography, Asia-Pacific accounted for 39.83% of global revenue in 2025, and the Middle East is anticipated to be the fastest-growing region, with a 5.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Large Format Printers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaging, Advertising and Textile Boom | +1.8% | Global focus on Asia-Pacific and Middle East | Medium term (2-4 years) |

| UV-Curable and High-Speed Inkjet Adoption | +1.2% | North America and Europe for industrial, Asia-Pacific for volume | Short term (≤ 2 years) |

| ESG-Driven Shift to Water-Based Inks | +0.9% | Europe, North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| AI-Automated Workflow for SMB Print Shops | +0.7% | Global, early uptake in North America and Western Europe | Medium term (2-4 years) |

| Rise of Localised Micro-Factory Print Hubs | +0.5% | Asia-Pacific secondary cities, Middle East, Latin America | Long term (≥ 4 years) |

| On-Demand Décor Customisation for Short Runs | +0.4% | North America and Europe homes, Asia-Pacific hospitality | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Packaging, Advertising, and Textile Boom

E-commerce penetration, which crossed 19.7% of global retail in 2024, is driving demand for corrugated boxes that require variable-data codes for traceability under EU packaging rules.[1]European Chemicals Agency, “PFAS Restriction Proposal,” echa.europa.eu Large-format digital presses make SKU-level customization economical at run lengths previously served only by offset, bringing 68% of new fast-moving consumer goods launches within profitable thresholds. In textiles, on-demand micro-factories harness direct-to-fabric platforms to cut sample-to-production lead times from weeks to hours, reducing inventory risk for fashion brands. Outdoor advertising spending in the United States climbed 4.5% in 2024, yet static billboard inventory shrank as operators upgraded premium sites to LED. Print volume is migrating toward event wraps and building graphics, where flexible substrates outperform rigid displays. Emerging print hubs in Indonesia, Vietnam, and India are adding capacity to serve both export apparel and regional décor, compressing investment payback for UV-LED and latex systems to less than 24 months.

UV-Curable and High-Speed Inkjet Adoption

UV-LED curing lowers energy consumption by 70% compared with mercury lamps, enabling printing on heat-sensitive plastics for point-of-purchase displays.[2]Canon, “Colorado 1650 UVgel Printer Data Sheet,” canon.com Systems such as Canon’s Colorado 1650 achieve 1,200 dpi at production speeds, expanding the use of technical documentation and CAD applications that demand fine-line accuracy. In centralized reprographic departments, HP’s PageWide XL 8200 outputs 30 D-size prints per minute, delivering cost-per-page advantages once daily volumes exceed 500 m². Hybrid platforms that switch between roll-to-roll and flatbed modes in a single chassis free up floor space and broaden the substrate mix, a decisive factor for commercial shops facing real-estate constraints. Although UV inks cost more than latex, their instant curing eliminates drying bottlenecks, sustaining throughput in deadline-driven print-for-pay environments. Inline spectrophotometers, now required under ISO 12647-2, add capital cost but reduce reprints by 18%, preserving margins under tight delivery windows.

ESG-Driven Shift to Water-Based Inks

California’s AB 1200 ban on intentionally added PFAS in textiles, effective January 2025, is pushing producers to reformulate coatings and inks. Maine’s reporting requirements follow a similar trajectory, signaling wider U.S. adoption. HP’s Latex 2700 series, certified GREENGUARD Gold, avoids hazardous air pollutants, saving print shops the ventilation upgrades needed for solvent or UV systems.[3]HP Inc., “HP Site Flow Workflow Suite,” hp.com The EU’s draft PFAS restriction under REACH is set to cover more than 10,000 substances, creating compliance uncertainty that favors suppliers with dedicated regulatory teams. While latex inks cure more slowly, steady improvements in oven design have narrowed throughput gaps, and their zero-VOC profile aligns with tightening indoor-air standards for schools and hospitals. Environmental liability under EPA’s PFAS Strategic Roadmap is further motivating closed-loop solvent recovery investments for shops that remain on legacy chemistries.

AI-Automated Workflow for SMB Print Shops

A Ricoh 2024 survey revealed that 52% of commercial printers implemented automation, yet most still rely on manual job ticketing, which adds 18 hours to the average turnaround. HP Site Flow integrates order intake, pre-flight, and scheduling, reducing operator touchpoints from 12 to three and trimming setup time by 35% on mixed-substrate runs. Predictive maintenance algorithms embedded in cloud dashboards reduce unplanned downtime by 22%, making it viable for shops with fewer than 20 employees for a single operator to be responsible for multiple devices. Machine-learning-driven RIP software automatically corrects PDF errors, eliminating two-thirds of pre-press rejections and sustaining the large format printers market’s pivot toward service revenue. Leasing contracts increasingly embed workflow licenses, transforming capital expenditures into operating expenses and aligning costs with revenue generation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Signage Substitution | -1.1% | North America, Europe tier-1 cities, Asia-Pacific metros | Short term (≤ 2 years) |

| High Cap-Ex and Op-Ex of Industrial LFPs | -0.8% | Global, pronounced in South America, Africa, Southeast Asia | Medium term (2-4 years) |

| Looming PFAS-Free Ink Compliance Gap | -0.6% | North America, Europe export markets, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Lightweight Glass Tech Eroding Weight Edge | -0.3% | Europe and North America architectural sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Signage Substitution

Programmatic digital out-of-home revenue in the United States jumped 18.2% in 2024, with LED networks commanding premium locations such as airports and transit hubs. Cost-per-thousand impressions for LED in New York’s Times Square averages USD 2.80, compared with USD 4.50 for static vinyl, prompting operators to retire aging print billboards. Print remains indispensable for building wraps, vehicle graphics, and event installations where LED’s rigid form factor cannot conform to complex surfaces. Municipal rules in European cities increasingly restrict new static billboard permits while exempting digital displays capable of public-service messaging, a regulatory divergence that squeezes print volume in urban cores. Nevertheless, the economics of low-traffic roads continue to favor vinyl, costing USD 1,200-2,500 per installation, compared with USD 150,000-300,000 for an equivalent LED installation.

High Cap-Ex and Op-Ex of Industrial LFPs

Entry-level UV flatbeds start at USD 50,000, and hybrid 3.2 m platforms climb to USD 500,000, a hurdle that sidelines many small businesses. Consumables add pressure: UV inks average USD 85 per liter, and printheads, priced up to USD 4,000, require replacement every two years. An industry survey found 74% of shops absorbed higher costs in 2024, but only half passed them through, compressing margins. Import tariffs magnify the squeeze, with 68.8% of North American printers expecting 10.8% higher consumable costs in 2025. Leasing reduces upfront cash outlay but transfers the risk of obsolescence to lessees, who face penalties if they migrate to next-generation devices early. In emerging markets, double-digit interest rates stretch payback beyond five years, narrowing adoption to established commercial houses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum as Risk Shifts to Vendors

The large format printers market size tilted toward services, as the segment logged a 4.91% CAGR through 2031, while printers, though still 68.23% of revenue in 2025, grew more slowly. Contracts that wrap equipment, maintenance, and consumables into monthly fees let buyers preserve cash and sidestep technological obsolescence. Managed print agreements now bundle AI-enabled predictive maintenance that flags printhead wear 72 hours before failure, sparing emergency call-outs. Subscription-based workflow software lowers entry barriers for micro-shops: a cloud RIP priced at USD 995 per month replaces a USD 15,000 perpetual license, smoothing cost over time. The services model is most entrenched in North America and Western Europe, where 63% of commercial printers already run cloud workflows, compared with 31% in Asia-Pacific, where data-sovereignty concerns persist. Vendors benefit from locked-in consumable streams that stabilize revenue even as hardware margins tighten, reinforcing a virtuous cycle that propels the segment’s expansion in the large format printers market.

At the same time, printer ownership remains essential for integrated producers that juggle packaging, textiles, and signage orders that require rapid substrate changeovers. These operators optimize uptime across their fleets, extracting utilization rates above 80%. Software, the smallest revenue slice, nevertheless posts a 4.68% CAGR as AI-rich modules unlock savings through lights-out production and predictive quality control. Overall, the offering landscape illustrates a gradual migration from capital outlay to pay-as-you-go models without eroding the central role of hardware in throughput-driven businesses.

By Printing Technology: Inkjet Dominates while Latex Accelerates

Inkjet technology accounted for 79.41% of the large format printers market share in 2025, owing to its versatility across substrates ranging from glass to polyester. High-performance dye-sublimation units such as Epson’s SureColor F10070H deliver 108 m² per hour, enabling profitable apparel runs of more than 500 pieces. Toner platforms, although marginal, persist in technical documentation where ISO-compliant archival accuracy is mandatory. Looking ahead, inkjet’s 4.74% CAGR lags that of latex because environmental regulations favor water-based chemistries for indoor graphics. California’s VOC cap of 150 g/L effectively sidelines solvent devices in the Los Angeles basin, propelling the adoption of latex among print-for-pay shops serving retail interiors and healthcare facilities.

Toner’s future remains niche: temperatures above 180 °C preclude the use of thin plastics in half of retail display applications, constraining its role to architecture and engineering drawing, where longevity outweighs material flexibility. Overall, competitive dynamics show mature inkjet segments offset by expansion into packaging and textiles, ensuring the technology remains central to the large format printers market even as latex captures incremental indoor volume.

By Ink Type: UV-Curable Leads, Latex Takes the Sustainability Baton

UV-curable inks led revenue growth with 44.78% in 2025, thanks to instant curing that enables immediate lamination and finishing. Their ability to adhere to metal, wood, and plastics without primers underpins demand in industrial signage and décor. However, water-based latex formulations are growing at the fastest 5.37% CAGR as buyers align with low-VOC mandates; GREENGUARD Gold certification has become a prerequisite for many public-space tenders. The share of solvents and eco-solvents is shrinking in regulated markets, yet they remain relevant in regions with looser environmental rules.

Meanwhile, dye-sublimation inks benefit from the growing demand for polyester textiles in sportswear, aided by direct-to-fabric systems that deliver wash-fastness beyond 40 laundering cycles. The looming phase-out of PFAS surfactants threatens certain UV chemistries, forcing costly reformulations and opening a compliance gap that latex suppliers exploit. This regulatory headwind explains the ink-type shift visible in the outlook for the large format printers market.

By End-User Industry: Apparel Emerges as Fastest-Growing Vertical

Signage and outdoor advertising retained the largest share at 36.92% in 2025; nonetheless, apparel and textiles outpaced all other verticals with a 5.56% CAGR to 2031. Direct-to-garment and roll-to-roll dye-sublimation printers let fashion brands trial micro-runs of 500 units, avoiding overstock and responding swiftly to viral trends. Packaging and labels grow at 4.82% as retailers demand scan-ready codes for omnichannel logistics, requiring large format overprinting on corrugated sheets. Décor applications, including custom wallpaper and interior murals, track a 4.95% CAGR in tandem with robust home-renovation spending in North America.

CAD and technical output remain stable, buoyed by infrastructure investment across Asia-Pacific and the Middle East that mandates printed plan sets for regulatory approvals. Niche segments such as fine-art reproduction advance on the back of archival pigment sets that guarantee 100-year longevity. On-demand models are reshaping volume distribution in the large format printers market, as evidenced by the acceleration in apparel. The growing demand for customization and quick turnaround times in the apparel industry has driven the adoption of these models. This shift highlights the increasing importance of flexible production processes to meet evolving consumer preferences.

Geography Analysis

Asia-Pacific accounted for 39.83% of global revenue in 2025, bolstered by Chinese exports of 284,000 printing units, a 52% increase from the prior year. Indonesia, Vietnam, and India collectively post above-regional-average growth as textile and décor exports expand, while Japan’s replacement of solvent fleets with UV-LED drives upgrade demand. India’s 6.1% CAGR outstrips its neighbors, fueled by booming e-commerce packaging. South Korea exhibits the region’s highest AI workflow penetration, though demographic contraction caps overall growth.

The Middle East has the fastest regional CAGR of 5.33%, driven by Saudi Arabia’s Vision 2030 megaprojects, which are multiplying demand for site graphics and indoor décor. The United Arab Emirates leverages legacy capacity from Expo 2020 to serve broader Gulf needs, while solvent devices remain in use due to lighter environmental regulations. Africa’s adoption is slower, hampered by financing costs, yet South Africa and Egypt serve as continental beachheads for packaging tied to multinational consumer-goods producers.

North America accounted for 28.14% of the global value in 2025, but tariffs and stringent VOC rules temper future expansion to a 3.87% CAGR. Diversified shops earn EBITDA margins of 19.7% against 8.2% for single-service peers, underscoring the advantage of wide-format integration. Canada grows moderately on the back of government infrastructure spending, and Mexico posts a 5.2% CAGR as nearshoring boosts packaging demand. Europe’s 3.92% CAGR is driven by solvent-fleet replacement under the EU Green Deal; Eastern Europe records the fastest sub-regional growth as brands set up localized print capacity. South America remains a small but steady 6.89% share, with Brazil dominating through agricultural export packaging linked to coffee and soy shipments.

Competitive Landscape

The large format printers market is moderately fragmented. The top five HP, Canon, Epson, Roland DG, and Mimaki collectively hold roughly a 55% share, while regional challengers in China and India offer 30-40% cheaper alternatives that appeal in price-sensitive segments. Competition intensifies around UV-LED, where Agfa, Durst, and SwissQprint race to raise productivity and substrate flexibility. Vertical integration is a common hedge: HP’s acquisition of a latex-ink chemistry unit in 2023 secured proprietary formulations that rivals cannot match, reinforcing supply-chain control.

Service revenue is the new battleground. IT service firms now bundle large format devices with managed print contracts that guarantee uptime via predictive analytics, eroding the hardware-only value proposition. Start-ups targeting micro-factory apparel printing use direct-to-fabric engines to bypass traditional textile workflows, compressing lead times from weeks to days and courting fashion brands experimenting with regional production.

Technology alignment differs by application: HP and Canon lead signage and technical graphics with PageWide and Colorado platforms, Epson and Mimaki dominate textiles with dye-sublimation, and Agfa and Durst excel in rigid-substrate printing for décor. Consolidation may accelerate as compliance costs rise; manufacturers with in-house ink research hold an advantage over assemblers reliant on external chemists because PFAS-free regulations demand rapid formulation pivots.

Large Format Printers Industry Leaders

HP Inc.

Canon Inc.

Seiko Epson Corporation

Ricoh Company, Ltd.

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: HP Inc. began commercial shipments of the HP Latex 2800 series, featuring nozzle-level recirculation to extend printhead life and cut consumable waste (ongoing).

- September 2025: ISO 12647-2 color management standards now require spectrophotometric verification for 95% of commercial print jobs, driving adoption of inline sensors that add USD 15,000 to USD 25,000 to system costs but reduce waste from color drift by 18% ISO.

- April 2025: Gelato’s 2025 report on AI adoption in print production documented that 80% of surveyed print service providers implemented at least one AI-driven tool, with predictive maintenance algorithms reducing unplanned downtime by 22% and ink consumption optimization lowering per-job costs by 8% Gelato.

- January 2025: California Assembly Bill 1200, effective January 2025, prohibits the manufacture or sale of textiles containing intentionally added PFAS, forcing reformulation of water-repellent and stain-resistant finishes that rely on fluorinated chemistries California Legislative Information.

Global Large Format Printers Market Report Scope

The Large Format Printers Market Report is Segmented by Offering (Printers, Software, Services), Printing Technology (Inkjet, and Toner / Laser), Ink Type (Aqueous, Solvent and Eco-Solvent, UV-Curable, Latex, Dye-Sublimation), End-User Industry (Signage and Outdoor Advertising, Apparel and Textiles, Décor and Interior Graphics, CAD and Technical, Packaging and Labels, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Printers |

| Software |

| Services |

| Inkjet |

| Toner / Laser |

| Aqueous |

| Solvent and Eco-Solvent |

| UV-Curable |

| Latex |

| Dye-Sublimation |

| Signage and Outdoor Advertising |

| Apparel and Textiles |

| Décor and Interior Graphics |

| CAD and Technical |

| Packaging and Labels |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Offering | Printers | ||

| Software | |||

| Services | |||

| By Printing Technology | Inkjet | ||

| Toner / Laser | |||

| By Ink Type | Aqueous | ||

| Solvent and Eco-Solvent | |||

| UV-Curable | |||

| Latex | |||

| Dye-Sublimation | |||

| By End-User Industry | Signage and Outdoor Advertising | ||

| Apparel and Textiles | |||

| Décor and Interior Graphics | |||

| CAD and Technical | |||

| Packaging and Labels | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is apparel printing expanding within the large format printers market?

Apparel and textiles is the fastest-growing vertical, forecast to rise at a 5.56% CAGR through 2031 as on-demand micro-factories enable profitable short runs.

Which ink type is gaining traction due to environmental mandates?

Water-based latex inks are expanding at 5.37% CAGR because their zero-VOC profile helps buyers comply with emerging PFAS and indoor-air regulations.

What is the main advantage of UV-curable platforms?

Instant curing lets operators laminate or finish graphics immediately, boosting throughput in deadline-driven signage and décor jobs.

Why are services outpacing hardware sales?

Integrated contracts bundle equipment, consumables and AI workflow tools into operating fees, shifting obsolescence risk away from buyers and stabilizing vendor revenue.

Which region is currently the fastest-growing?

The Middle East is advancing at 5.33% CAGR, led by Saudi Arabia’s Vision 2030 projects that require extensive site graphics and interior décor.

What hinders adoption in emerging economies?

High capital costs, double-digit financing rates and elevated import duties extend payback periods beyond five years, limiting investments to larger commercial printers.

Page last updated on: