Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.35 Billion |

| Market Size (2031) | USD 52.34 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Esoteric Testing Market Analysis by Mordor Intelligence

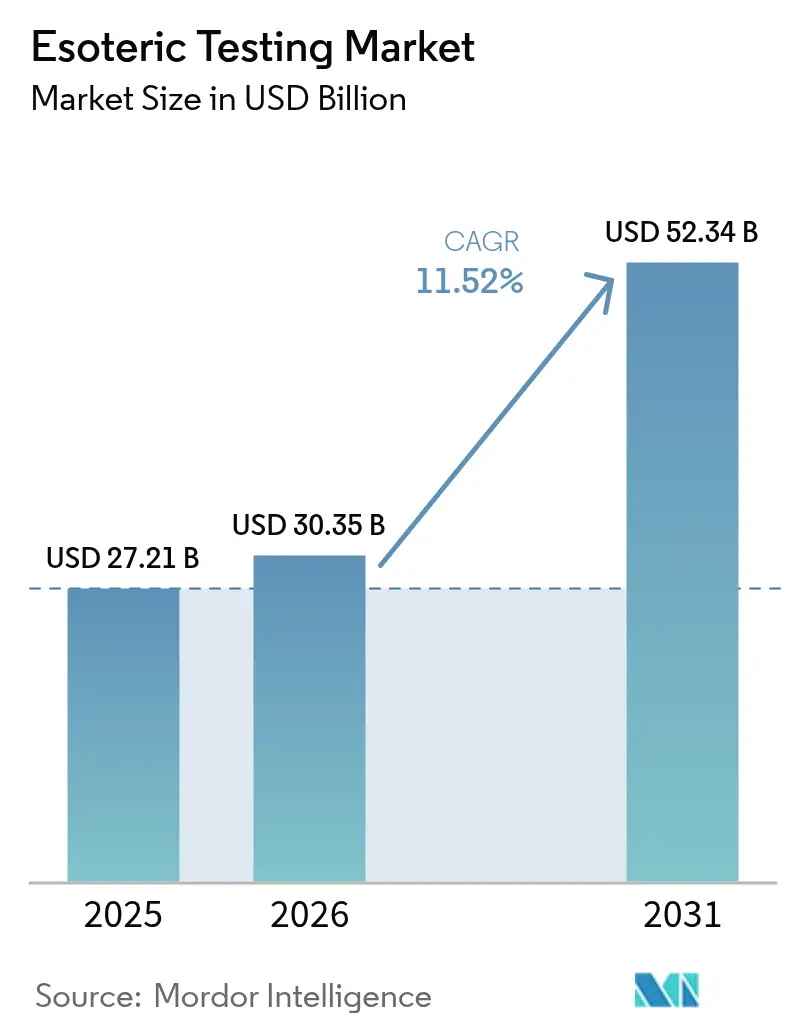

The Esoteric Testing Market size was valued at USD 27.21 billion in 2025 and estimated to grow from USD 30.35 billion in 2026 to reach USD 52.34 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

Demand accelerates as chronic disease prevalence rises, next-generation sequencing (NGS) becomes routine, and hospitals outsource complex assays to reference laboratories. New FDA rules classifying laboratory-developed tests as medical devices introduce cost but ultimately set clear quality standards that can boost global credibility [1]U.S. Food and Drug Administration, “Final Rule: Medical Devices; Laboratory Developed Tests,” fda.gov . Automation investments, declining sequencing costs, and payer support for high-impact panels further reinforce growth momentum.

Key Report Takeaways

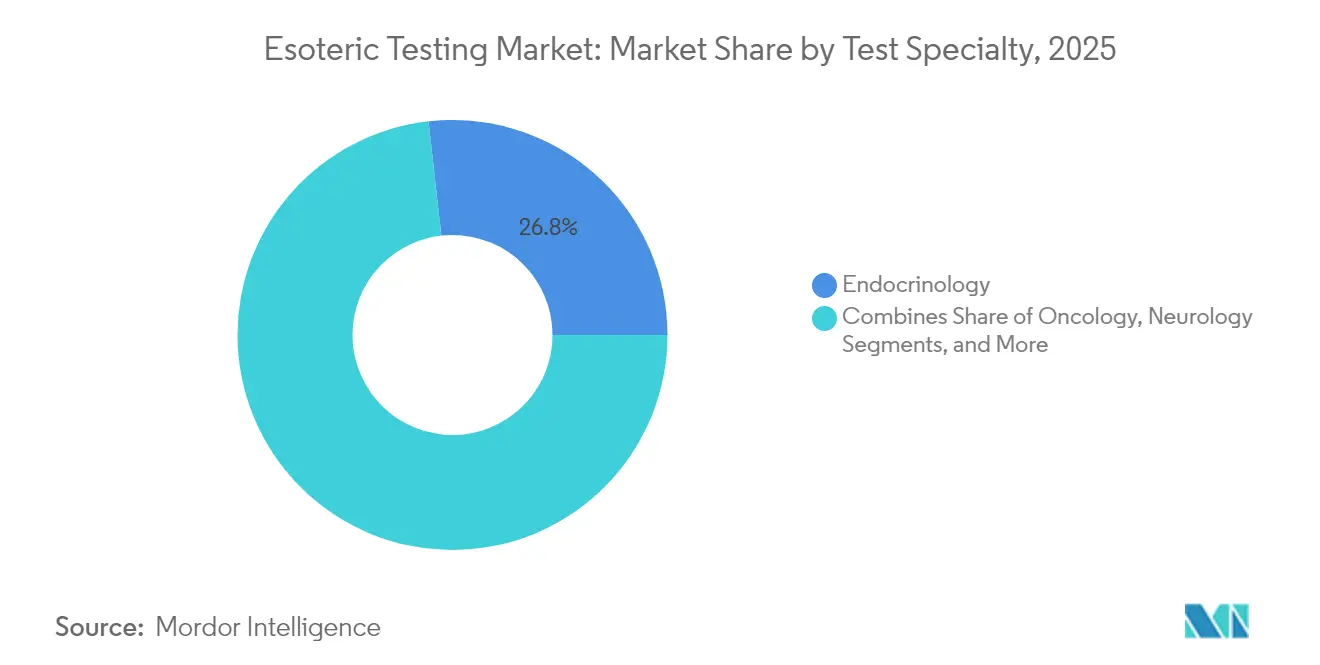

- By test specialty, endocrinology led with 26.78% of the esoteric testing market share in 2025; oncology tests are projected to grow at a 12.18% CAGR through 2031.

- By technology, chemiluminescence immunoassay held 26.45% of the esoteric testing market size in 2025, while NGS platforms are advancing at a 12.05% CAGR to 2031.

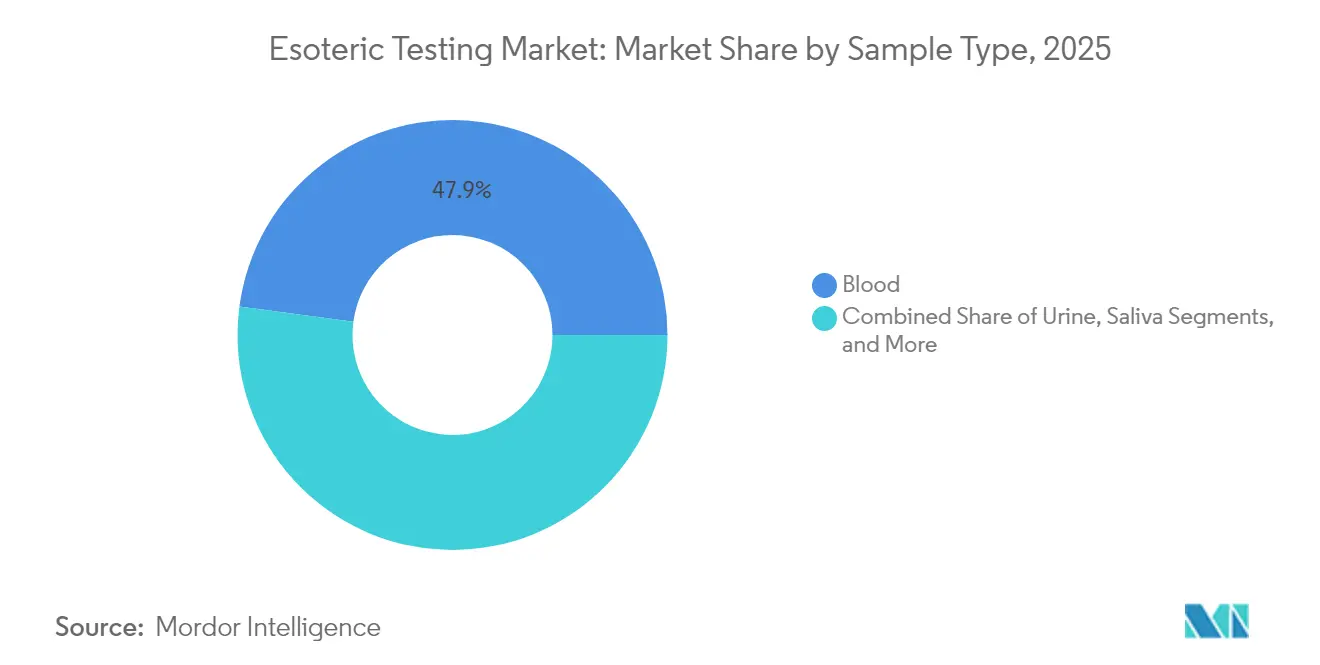

- By sample type, blood accounted for 47.88% of the esoteric testing market size in 2025; saliva specimens record the fastest 12.21% CAGR to 2031.

- By end user, hospitals and clinics controlled 51.35% of the esoteric testing market size in 2025, whereas diagnostics laboratories expand at a 12.29% CAGR to 2031.

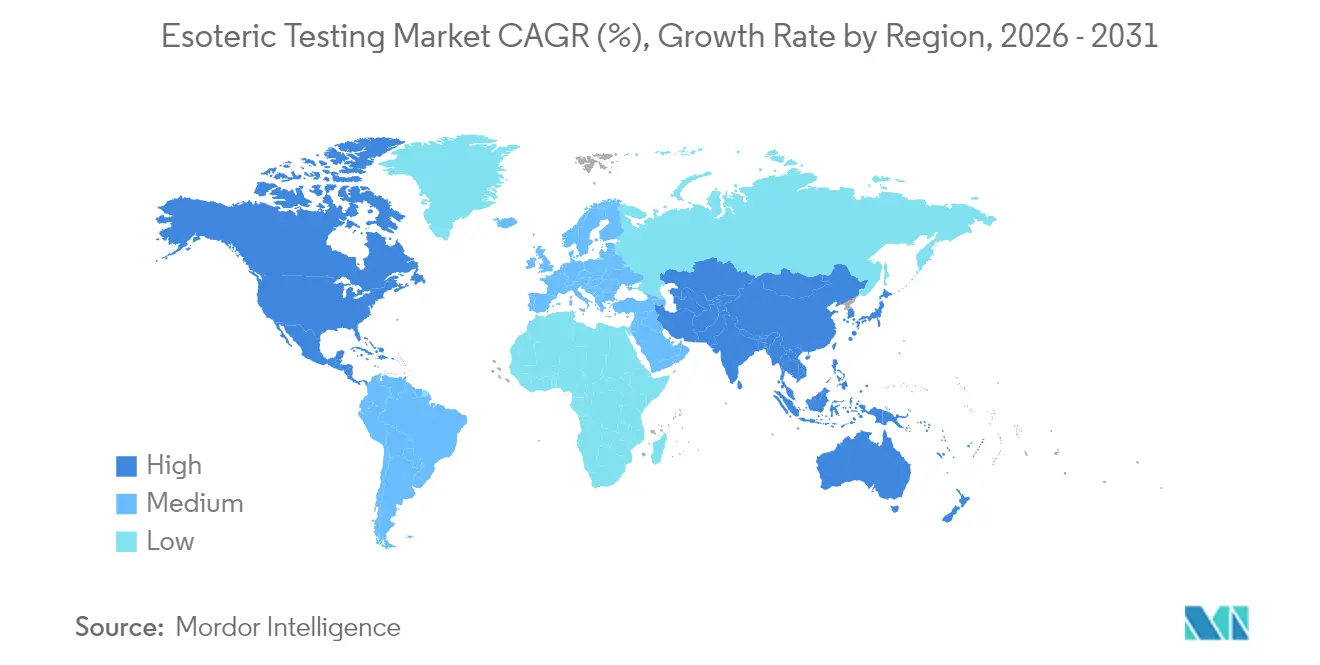

- By geography, North America controlled 41.35% of the esoteric testing market size in 2025, whereas Asia-Pacific expand at a 12.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Esoteric Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic & complex diseases | +2.8% | North America, Europe | Long term (≥ 4 years) |

| Growing demand for rare-disease diagnostics | +2.1% | North America expanding to APAC | Medium term (2-4 years) |

| Advances in molecular & multi-omics platforms | +3.2% | North America, EU, APAC | Medium term (2-4 years) |

| Increased R&D funding and lab automation | +1.9% | Developed markets worldwide | Long term (≥ 4 years) |

| Value-based reimbursement for high-impact panels | +1.6% | North America, EU | Medium term (2-4 years) |

| Digital e-ordering portals | +1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic & Complex Diseases

Long-term growth is tied to diabetes, autoimmune disorders, and cancer, all of which require multi-analyte panels that routine labs cannot handle. Medicare’s MolDX program links payment to clinical utility, encouraging physicians to order advanced assays [2]Centers for Medicare & Medicaid Services, “Molecular Diagnostic Services (MolDX) Program,” cms.gov . As populations age, clinicians face overlapping comorbidities; definitive esoteric testing offers clarity, reduces misdiagnosis costs, and supports value-based care.

Growing Demand for Rare-Disease Diagnostics

Improved physician awareness and over 54,000 available genetic tests have boosted orders for ultra-low-volume assays. The FDA breakthrough device pathway accelerates approval timelines, while orphan-drug sponsors fund companion diagnostics that identify niche patient cohorts, enabling laboratories with deep genomic capability to command premium pricing.

Advances in Molecular & Multi-Omics Platforms

NGS panels that profile hundreds of genes, such as Illumina’s TruSight Oncology Comprehensive, signal regulatory acceptance of broad molecular insights [3]U.S. Food and Drug Administration, "Premarket Approval (PMA)," accessdata.fda.gov. Integration with mass-spectrometry-based proteomics gives clinicians holistic disease signatures. AI tools aggregate data layers and flag actionable variants faster than manual review, justifying higher test reimbursement.

Increased R&D Funding and Lab Automation

Robotics and “dark labs” reduce manual error and mitigate a workforce deficit estimated at 20,000–25,000 professionals in the United States. Venture capital flowed into workflow-automation start-ups during 2024, and connected laboratory information systems now deliver predictive maintenance and real-time quality metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory & compliance requirements | -1.8% | North America, EU | Short term (≤ 2 years) |

| High per-test cost in price-sensitive economies | -1.4% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Shortage of highly skilled laboratory personnel | -1.1% | North America, Europe | Long term (≥ 4 years) |

| Data-integration hurdles for multi-omics reports | -0.9% | Advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory & Compliance Requirements

The FDA now demands that laboratory-developed tests meet medical-device rules, adding up to USD 3.56 billion in cumulative costs across U.S. labs and causing smaller facilities to reconsider new-test launches. Ongoing legal appeals create uncertainty that may defer capital spending.

High Per-Test Cost in Price-Sensitive Economies

Specialized assays often exceed USD 500, dwarfing routine-test fees. Limited insurance coverage in emerging markets forces self-pay, curbing uptake despite clinical need. Currency volatility and shipping costs for reagents further elevate final patient charges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Specialty: Oncology Drives Precision Medicine Growth

Oncology’s 12.18% CAGR makes it the fastest-moving specialty because liquid biopsy and comprehensive genomic profiling guide targeted treatments. FoundationOne CDx and Guardant Shield approvals show regulators view broad tumor panels as clinically essential. Endocrinology remains the revenue anchor, capturing 26.78% of the esoteric testing market size in 2025 through insulin, HbA1c, and thyroid assays.

Clinical focus continues to shift from high-volume thyroid testing to sophisticated biomarker suites that stratify cancer risk. Infectious-disease, neurology, and immunology segments benefit from AI-driven interpretation, but oncology captures the spotlight as payers reimburse for tests that match therapy to mutation, shortening hospital stays and improving outcomes.

By Technology: NGS Platforms Reshape Molecular Diagnostics

Sequencing costs have fallen below USD 200 per genome, and regulatory green lights for multi-gene panels propel NGS to a 12.05% CAGR. Illumina’s kit-based oncology panel gained FDA clearance, giving smaller labs plug-and-play capability. Chemiluminescence immunoassay remains dominant with a 26.45% esoteric testing market share due to its scalable menu across endocrinology and infectious disease.

Flow cytometry broadens from hematology into immune profiling, while mass spectrometry moves from research to routine through automated sample prep. Although real-time PCR sustains infectious-disease demand, ELISA and radio-immunoassay fade as labs consolidate around faster, multiplexed options.

By Sample Type: Saliva Testing Gains Non-Invasive Advantage

Blood retained 47.88% of the esoteric testing market size in 2025 thanks to clinician familiarity and robust reference ranges. Yet saliva registers the strongest 12.21% CAGR as patients prefer painless self-collection and telehealth expands kit distribution.

COVID-19 catalyzed saliva acceptance; now hormone, pharmacogenomic, and viral-load assays routinely run on spit specimens. Urine and cerebrospinal fluid serve niche metabolic and neurological needs, but logistics, not clinical value, restrict wider adoption.

By End User: Diagnostics Laboratories Lead Specialization Trend

Hospitals delivered 51.35% of revenue in 2025, yet reference labs grow faster at 12.29% CAGR as health systems outsource complexity. Staffing gaps—80% of microbiology labs report vacancies—push work to high-throughput centers with robotics.

Academic institutes pilot novel assays, then license them to commercial labs. Consolidators such as LabCorp snapped up BioReference oncology assets to broaden menus nationally, signaling that size plus specialization beats geography alone.

Geography Analysis

North America commanded 41.35% revenue in 2025. Medicare’s MolDX pathway speeds coverage for molecular tests, and the region’s payer mix supports premium pricing. Ongoing mergers—including Quest Diagnostics’ takeover of LifeLabs—bundle logistics networks with AI-enabled result portals, reinforcing regional dominance.

Asia-Pacific is the fastest-growing region at a 12.07% CAGR. China’s regulator cleared 228 new drugs in 2024, 92 with companion diagnostics, sparking hospital demand for multi-gene tests. Indian chains such as Dr. Lal PathLabs push into tier-3 cities while Molbio Diagnostics readies a USD 265 million IPO to fund molecular expansion. Mobile health platforms link rural clinics to reference labs, shortening sample-to-result cycles.

Europe posts stable single-digit gains. Cross-border lab alliances streamline sample routing, and sustainability mandates spur demand for environmental toxicology panels. Eurofins reported EUR 6.951 billion revenue in 2024 after 31 acquisitions, highlighting a buy-and-build model that keeps menu breadth ahead of regional peers. Latin America and Middle East & Africa advance steadily as private insurers widen coverage, though infrastructure gaps and import duties temper immediate scale.

Competitive Landscape

Market concentration is moderate. LabCorp, Quest Diagnostics, and Eurofins together control roughly one-third of global revenue, aided by nationwide logistics, regulatory muscle, and multi-omics menus. Each firm inked multiple acquisitions in 2024; LabCorp’s purchase of BioReference assets broadened oncology reach, while Eurofins picked up 18 start-ups to boost regional depth.

Specialist players carve niches. ARUP Laboratories secured the first FDA-authorized AAV5 DetectCDx for gene-therapy monitoring, underscoring academic labs’ role in pioneering new categories. Caris Life Sciences combined whole-exome and transcriptome sequencing in its MI Cancer Seek test, winning approval for pan-tumor profiling.

Technology partnerships proliferate. AI vendors integrate with LIMS software to flag contamination, while robotics firms supply modular aliquoting lines that raise throughput without adding staff. Workforce shortages create barriers to entry, yet cloud-hosted analysis pipelines let smaller labs run sophisticated panels without building local bioinformatics teams.

Esoteric Testing Industry Leaders

-

bioMontr Labs

-

Quest Diagnostics

-

Kindstar Globalgene Technology, Inc.

-

H.U. Group Holdings, Inc.

-

Laboratory Corporation of America Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ARUP Laboratories extended its AI parasitology system to wet-mount slides, recording five-fold sensitivity gains.

- March 2025: LabCorp bought BioReference Health’s oncology testing assets, deepening nationwide cancer-genomics coverage.

- January 2025: bioMérieux closed its EUR 111 million acquisition of SpinChip Diagnostics, adding 10-minute whole-blood immunoassay capability.

- November 2024: Caris Life Sciences obtained FDA approval for MI Cancer Seek, the first assay to combine whole-exome and whole-transcriptome sequencing for solid tumors.

Global Esoteric Testing Market Report Scope

As per the scope of the report, esoteric testing is used for analyzing and detecting rare substances and molecules.

The esoteric testing market is segmented by test type, technology, and geography. By test type, the market is segmented into endocrinology, infectious disease, oncology, neurology, toxicology, and others. By technology, the market is segmented into flow cytometry, chemiluminescence immunoassay, mass spectrometry, radio immunoassay, and others. By geography, the market is segmented into North America, Europe, Asia Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

By Test Specialty

| Endocrinology |

| Infectious Disease |

| Oncology |

| Neurology |

| Immunology |

| Genetics |

| Others |

By Technology

| Flow Cytometry |

| Chemiluminescence Immunoassay |

| Mass Spectrometry |

| Real-time PCR |

| Next-Generation Sequencing (NGS) |

| ELISA |

| Radio Immunoassay |

| Others |

By Sample Type

| Blood |

| Urine |

| Saliva |

| Cerebrospinal Fluid (CSF) |

| Others |

By End User

| Hospitals and Clinics |

| Diagnostics Laboratories |

| Academic and Research Institutes |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Specialty | Endocrinology | |

| Infectious Disease | ||

| Oncology | ||

| Neurology | ||

| Immunology | ||

| Genetics | ||

| Others | ||

| By Technology | Flow Cytometry | |

| Chemiluminescence Immunoassay | ||

| Mass Spectrometry | ||

| Real-time PCR | ||

| Next-Generation Sequencing (NGS) | ||

| ELISA | ||

| Radio Immunoassay | ||

| Others | ||

| By Sample Type | Blood | |

| Urine | ||

| Saliva | ||

| Cerebrospinal Fluid (CSF) | ||

| Others | ||

| By End User | Hospitals and Clinics | |

| Diagnostics Laboratories | ||

| Academic and Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the esoteric testing market by 2031?

The esoteric testing market is expected to reach USD 52.34 billion by 2031.

Which test specialty is growing the fastest?

Oncology testing leads growth with a 12.18% CAGR through 2031, driven by liquid biopsy and comprehensive genomic profiling approvals.

Why are saliva-based assays gaining popularity?

Saliva sampling is non-invasive and supports at-home collection, fueling a 12.21% CAGR for saliva tests within the esoteric testing market.

How will the new FDA LDT rule affect laboratories?

Labs must meet medical-device standards, adding compliance costs of up to USD 3.56 billion industry-wide but ultimately ensuring higher quality and global credibility.

Which region offers the highest growth potential?

Asia-Pacific records the fastest 12.07% CAGR, buoyed by China’s companion-diagnostic approvals and expanding molecular-testing infrastructure.

What technology holds the largest esoteric testing market share today?

Chemiluminescence immunoassay leads with 26.45% of 2025 revenue, though NGS platforms are growing the quickest.

Page last updated on: