Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 20.4 Billion |

| Market Size (2026) | USD 22.25 Billion |

| Market Size (2031) | USD 34.37 Billion |

| Growth Rate (2026 - 2031) | 9.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait ICT Market Analysis by Mordor Intelligence

The Kuwait ICT market size was valued at USD 20.4 billion in 2025 and estimated to grow from USD 22.25 billion in 2026 to reach USD 34.37 billion by 2031, at a CAGR of 9.08% during the forecast period (2026-2031). Robust growth in the Kuwait ICT market is underpinned by the New Kuwait 2035 vision, rapid 5G deployment, and a cloud-first policy that accelerates public-sector digitalization. Early adoption of advanced mobile networks encourages investment in edge computing, while data-center free-zone incentives create a favorable environment for hyperscale providers. Government ministries mandate cloud migration, prompting enterprises to modernize legacy systems, and rising cybersecurity concerns drive a parallel surge in IT security spending. Strategic partnerships between telecom operators and global technology firms shorten time-to-market for AI-powered Arabic language solutions, positioning Kuwait as a regional development hub.

Key Report Takeaways

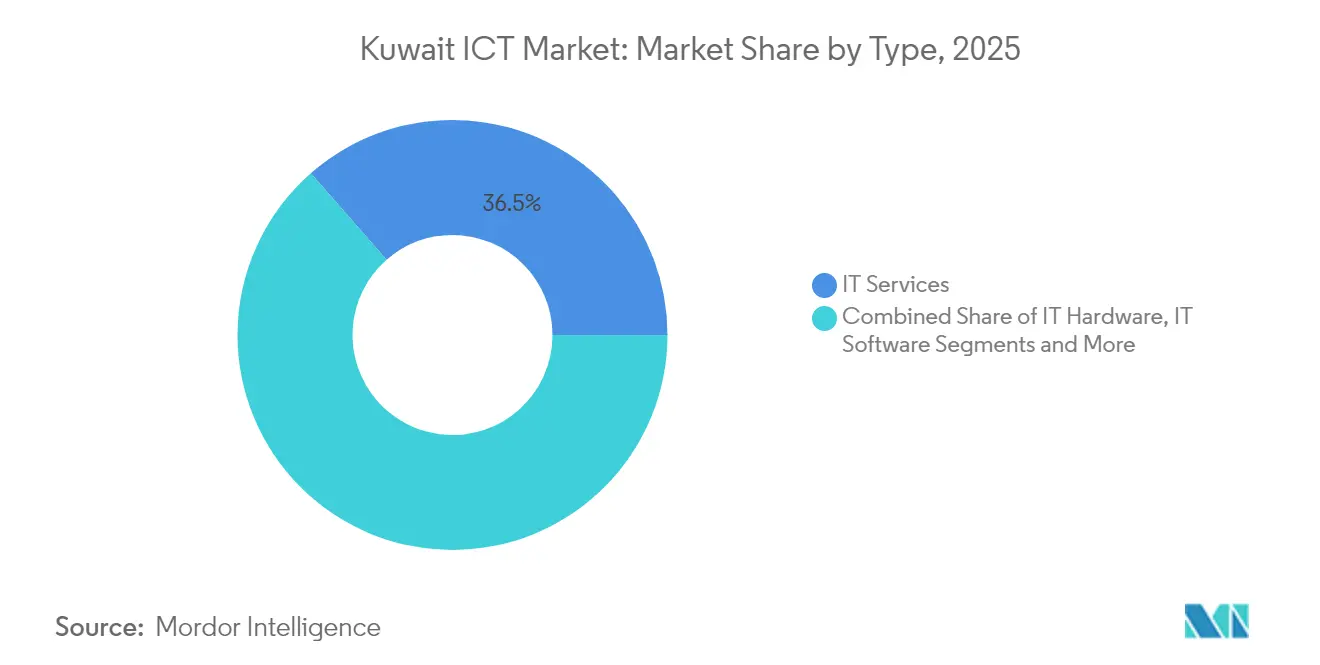

- By type, IT services led with 36.45% revenue share in 2025; IT security is advancing at a 10.02% CAGR through 2031.

- By enterprise size, large enterprises held 63.05% of the Kuwait ICT market share in 2025, while SMEs are projected to expand at a 9.55% CAGR to 2031.

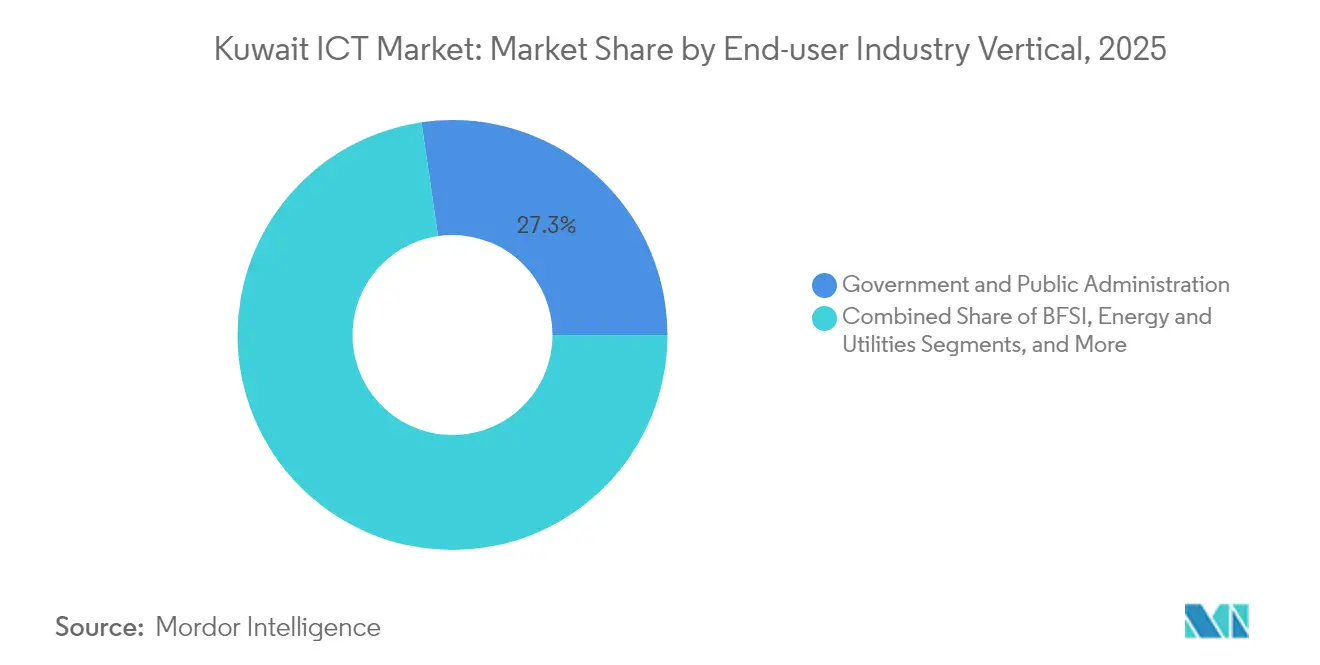

- By end-user vertical, government and public administration captured 27.31% revenue share in 2025; gaming and esports is expected to record a 10.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New Kuwait 2035 digital-first agenda | +2.8% | Nationwide, strongest in Kuwait City | Medium term (2-4 years) |

| Early 5G rollout and fiber densification | +2.1% | Urban and suburban areas | Short term (≤ 2 years) |

| Cloud-first policy for ministries and SOEs | +1.9% | All government entities | Medium term (2-4 years) |

| Data-center free-zone incentives | +1.4% | Designated economic zones | Long term (≥ 4 years) |

| AI-powered Arabic LLM localization | +1.0% | Regional, Kuwait as hub | Medium term (2-4 years) |

| Regional gaming-esports ambitions | +0.8% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

New Kuwait 2035 Digital-First Agenda Drives Comprehensive ICT Transformation

Mandatory migration of ministries to cloud services, rollout of the Meta central appointment platform, and upcoming AI-ready Azure region collectively stimulate large-scale contracts across infrastructure, software, and services. The unified citizen portal improves service quality and elevates demand for identity management, integration, and analytics tools.[1]Microsoft, “Microsoft to Establish AI-Powered Azure Region in Kuwait,” microsoft.com Budget allocations earmarked for e-government accelerate vendor onboarding, and standardized broadband pricing guarantees last-mile connectivity. [2]Kuwait Government Online, “Broadband Internet Pricing,” e.gov.kw Continuous flagship events such as Digital Transformation Kuwait maintain policy momentum and foster public-private collaboration.[3]Digital Transformation Kuwait, “Conference Summary,” digitaltransformationkuwait.com

Early 5G Rollout Creates Advanced Mobile Infrastructure Foundation

Nationwide 5G coverage enables telcos to monetize home broadband, fixed-wireless access, and network slicing solutions, stimulating incremental revenue in the Kuwait ICT market. Consolidation of nearly 1,675 tower sites by Zain optimizes radio planning and speeds up 5G layer densification. Partnerships like stc Kuwait and IPification showcase identity-as-a-service models, emphasizing security and user experience in fintech and media streaming

Cloud-First Policy Accelerates Enterprise Digital Migration

Cloud adoption gains traction across oil, banking, and retail domains. Kuwait Oil Company’s embrace of DecisionSpace 365 exemplifies production-scale data ingestion and analytics in upstream operations. National Bank of Kuwait extends its digital platform to AI-enabled transaction banking, signaling regulatory comfort with SaaS for critical workloads. Local ISVs collaborate with hyperscalers to offer Arabic NLP, low-code platforms, and sectoral clouds aligned to sovereignty norms, broadening Kuwait ICT market opportunities.

Data-Center Free-Zone Incentives Attract Hyperscale Investment

Tax holidays, customs exemptions, and streamlined licensing issued by KDIPA lure global colocation and cloud operators. Edge facilities near smart-meter clusters reduce latency for utilities, while free-zone sub-tenancies encourage managed-service ecosystems. Developers integrate renewable energy and waste-heat reuse to meet green-building codes, preparing the Kuwait ICT market for ESG-compliant workloads

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic ICT talent gap and visa caps | −1.8% | Concentrated in Kuwait City | Short term (≤ 2 years) |

| High oil-price correlation of public ICT budgets | −1.2% | Nationwide | Medium term (2-4 years) |

| Legacy on-premise dependency in critical sectors | −1.0% | Oil and gas, defense, banking hubs | Medium term (2-4 years) |

| Delayed e-payment regulation updates | −0.7% | Retail and fintech clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic ICT Talent Gap Constrains Market Growth

Localization targets of 66% at leading operators reveal continued reliance on expatriates for deep-tech roles, especially in cybersecurity and AI engineering. Stringent work-permit quotas lengthen hiring cycles, inflating wage bills and delaying project timelines. Upskilling programs and accelerator cohorts such as Zain Great Idea facilitate exposure to Silicon Valley practices but require several intake cycles to close systemic gaps.

High Oil-Price Correlation Creates Budget Volatility

Capital expenditure on national datacenters and smart-city pilots ebbs and flows with hydrocarbon receipts, forcing vendors to structure multiyear contracts with milestone-based payments. While peak oil prices unlock budget surpluses for transformational projects, downturns trigger spending freezes, affecting revenue visibility across the Kuwait ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: IT Services Remain Core as Security Accelerates

IT services contributed the largest share, buoyed by managed operations centers, help-desk outsourcing, and public-sector consulting engagements. The Kuwait ICT market size for IT services is projected to reach USD 12.58 billion by 2031. Escalating threat vectors plus enforcement of the Data Privacy Protection Regulation elevate cybersecurity outlays, propelling IT security toward double-digit CAGR. Hardware refresh cycles focus on 5G CPE, Wi-Fi 7 access points, and edge gateways, while software revenues stem from ERP modernization and analytics licenses. Incumbent integrators partner with international vendors to deliver turnkey upgrades that converge IT-OT for utilities.

The Kuwait ICT industry increasingly favors OPEX-based contracts bundled with SLA-driven performance incentives. Service providers differentiate on vertical expertise in oil, banking, and healthcare. Vendor-agnostic platforms reduce lock-in, and multicloud orchestration gains favor among enterprises balancing compliance and innovation needs.

By Enterprise Size: SME Digital Adoption Accelerates

Large organizations continue to anchor demand, purchasing advanced AI-enabled workloads and private 5G campus networks. However, governmental procurement reforms reserve up to 10% of ICT tenders for SMEs, catalyzing broader ecosystem growth. The Kuwait ICT market size captured by SMEs is expected to climb at 9.55% CAGR through 2031 as subscription-based SaaS and pay-as-you-go cloud lower entry barriers.

Entrepreneurial activity expands in e-commerce logistics, fintech gateways, and on-demand services. Incubators provide seed funding and cloud credits, while banks roll out digital lending tailored to tech startups. Cross-border venture syndicates open additional capital pools, diversifying the ownership structure of the Kuwait ICT industry.

By End-User Vertical: Gaming Emerges as Growth Leader

Public-sector entities spearhead digital ID, e-payment, and citizen-service rollouts that anchor steady ICT spend. In contrast, gaming and esports register the steepest ascent, fueled by youth demographics, high smartphone penetration, and policies promoting Kuwait as an events venue. The Kuwait ICT market share tied to gaming is small today yet forecast to expand rapidly as telcos bundle zero-rating and low-latency circuits.

Banks upgrade core systems with AI-driven fraud analytics and open-banking APIs, while oil and gas majors deploy digital twins and predictive maintenance. Healthcare providers implement telemedicine and e-pharmacy platforms, benefiting from 5G low-latency video consultations.

Geography Analysis

The capital governorate commands the bulk of datacenters, fiber interconnects, and systems-integration headquarters. Adjacent Hawalli and Farwaniya display strong consumer broadband uptake, whereas Al-Ahmadi hosts large industrial complexes that prioritize OT cybersecurity and private LTE. Northern Jahra integrates smart-grid pilots aligned with desert solar farms.

Per-capita ICT spend in Kuwait City surpasses GCC peers, reflecting high disposable income and government subsidies. Submarine cable landings enhance Kuwait’s role as a transit hub linking Saudi Arabia and Iraq to Europe and Asia. Free-zone parcels near Shuwaikh port facilitate just-in-time hardware logistics, reducing lead times for cloud-scale builds.

CITRA’s nationwide spectrum roadmap provides clear visibility for operators, and ISO-aligned data-protection rules attract foreign SaaS players comfortable with global compliance baselines. Combined, these factors strengthen the competitiveness of the Kuwait ICT market against the UAE and Saudi Arabia in selected verticals.

Competitive Landscape

The Kuwait ICT market features moderate concentration. Zain, Ooredoo, and stc Kuwait own most mobile spectrum and fiber backhaul, anchoring connectivity revenues. Zain booked KD 2 billion (USD 2.26 billion) in 2024 revenue, a 15% YoY jump that finances 5G densification and cloud partnerships. Ooredoo reported KWD 711 million (USD 803 million) in 2024 revenue, leveraging bundled 5G and fixed offers to defend share.

Global tech leaders secure long-term framework deals: Microsoft with government, IBM on core banking modernization, and Oracle on cloud ERP for diversified conglomerates. Systems integrators collaborate rather than compete head-on; for instance, stc and Microsoft co-deliver secure cloud connectivity, while Zain and Oracle promote joint SaaS bundles.

Emerging challengers include fintechs exploiting open-banking APIs, SaaS cybersecurity specialists delivering MDR, and gaming studios that monetize Arabic IP. M&A targets comprise Tier-3 datacenters and niche ISVs, reflecting a pivot toward platform capabilities over pure infrastructure.

Kuwait ICT Industry Leaders

International Business Machines Corp.

Microsoft Gulf FZ-LLC

SAP SE

Cisco Systems Inc.

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Gulf Business Machines secured a three-year managed-services contract with Landmark Hospitality Group across the GCC, including Kuwait.

- January 2025: KKR and Gulf Data Hub announced a USD 5 billion hyperscale data-center partnership with Kuwaiti sites.

- January 2025: eand and IBM launched an AI governance platform based on watsonx.governance, spotlighted at the World Economic Forum.

- December 2024: Zain Group acquired full ownership of IHS Kuwait, strengthening vertical integration.

Kuwait ICT Market Report Scope

Information and communication technologies, or ICT, are a broader term for information technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services that enable users to store, access, transmit, retrieve, and manipulate information in a digital form.

Kuwait's ICT market is segmented by type (IT hardware (computer hardware, networking equipment, peripherals), IT software, IT services (managed services, business process services, business consulting services, cloud services), IT infrastructure/data centers (colocation data centers, data center storage, data center servers, data center compute), IT security/ cybersecurity (application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, endpoint security), communication services), by enterprise size (small and medium enterprises, large enterprises), by industry vertical (BFSI, IT & Telecom, government, retail & e-commerce, manufacturing, energy & utilities, others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Kuwait ICT market tracks revenue accrued through the sale of ICT offerings including IT hardware, IT software, IT services, IT infrastructure and communication services that are being used in various end-user industry across the Country.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Verticals | ||

Key Questions Answered in the Report

How large is the Kuwait ICT market in 2026?

The Kuwait ICT market is valued at USD 22.25 billion in 2026.

What annual growth rate is forecast for Kuwait’s ICT sector to 2031?

Market revenue is expected to rise at a 9.08% CAGR to reach USD 34.37 billion by 2031.

Which segment holds the largest share of ICT spending?

IT Services led with 36.45% of 2025 revenue.

Which deployment model is expanding the fastest?

Cloud solutions are forecast to grow at a 14.05% CAGR through 2031, fueled by government cloud-first mandates.

How is 5G influencing Kuwait’s technology adoption?

97% population coverage and 10 Gbps pilot speeds enable low-latency applications and edge-computing services.

What is the main risk to ICT investment levels?

Volatile oil prices can restrict public-sector IT budgets, although cloud pay-as-you-go models help mitigate capex pressure.

Page last updated on: