Kuwait Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

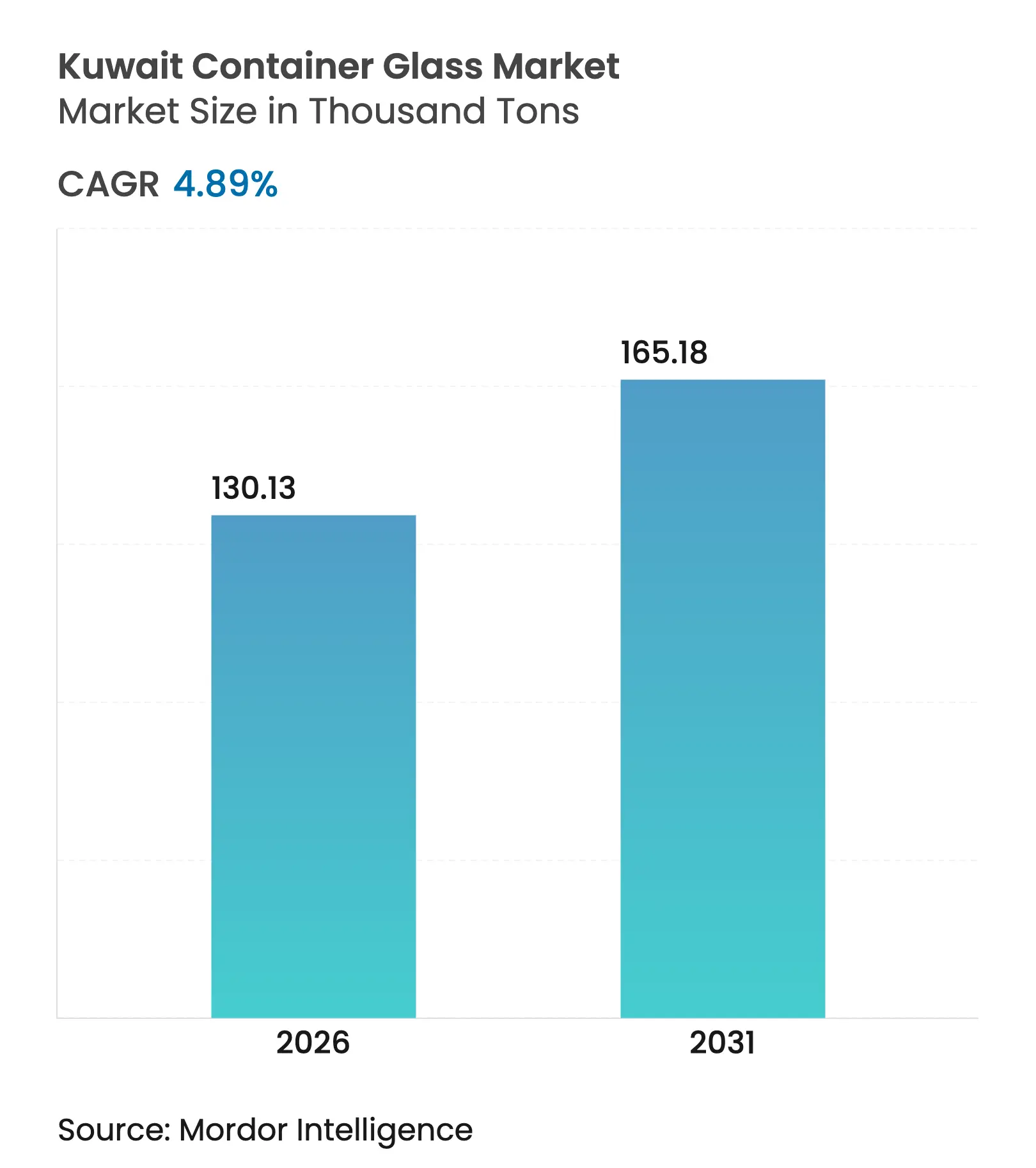

| Market Volume (2026) | 130.13 Thousand tons |

| Market Volume (2031) | 165.18 Thousand tons |

| CAGR | 4.89 % |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Kuwait Container Glass Market Analysis by Mordor Intelligence

The Kuwait Container Glass Market size was valued at 124.06 Thousand tons in 2025 and estimated to grow from 130.13 Thousand tons in 2026 to reach 165.18 Thousand tons by 2031, at a CAGR of 4.89% during the forecast period (2026-2031). Robust demand emerges from beverage fillers, personal care formulators, and pharmaceutical repackers that regard glass as an infinitely recyclable, chemically inert, and brand-enhancing medium. Vision 2035 industrial policies, combined with the National Waste Management Strategy 2040, incorporate economic incentives that reward high-recovery packaging streams and penalize less recyclable alternatives.[1]Public Authority for Industry, “Industry Strategies,” pai.gov.kw Regional capacity additions in Qatar and Saudi Arabia intensify competitive pressure yet simultaneously validate the growth potential of the broader Gulf glass ecosystem, encouraging Kuwait-based suppliers to climb the value curve through quality certifications, energy-saving furnace retrofits, and premiumized product mixes. Finally, subsidy reforms that lifted historically low gas and electricity tariffs, while challenging cost structures, are catalyzing process-efficiency investments that should temper margin compression and sustain medium-term profitability.

Key Report Takeaways

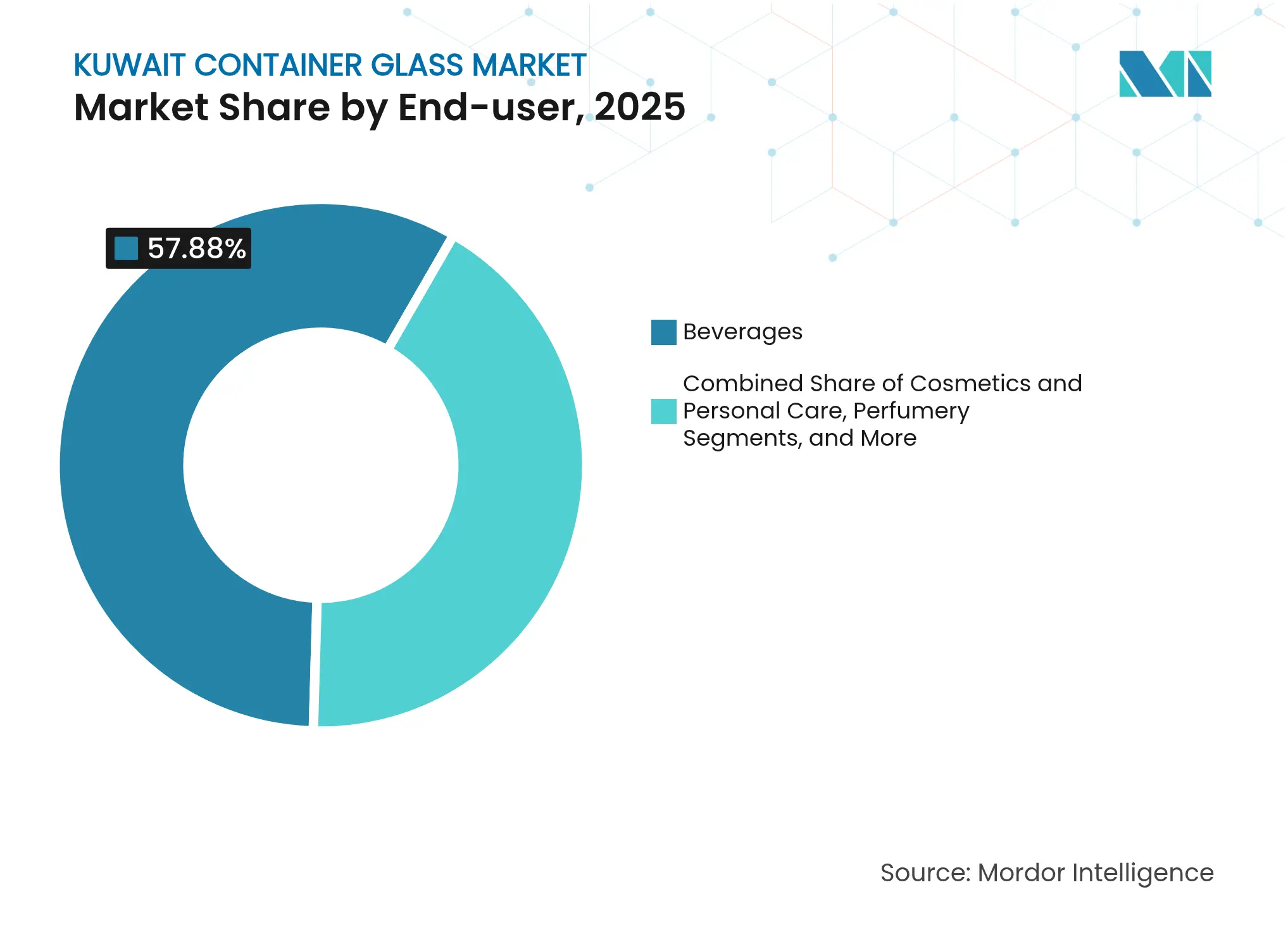

- By end-user, beverages captured 57.88% of the Kuwait container glass market share in 2025.

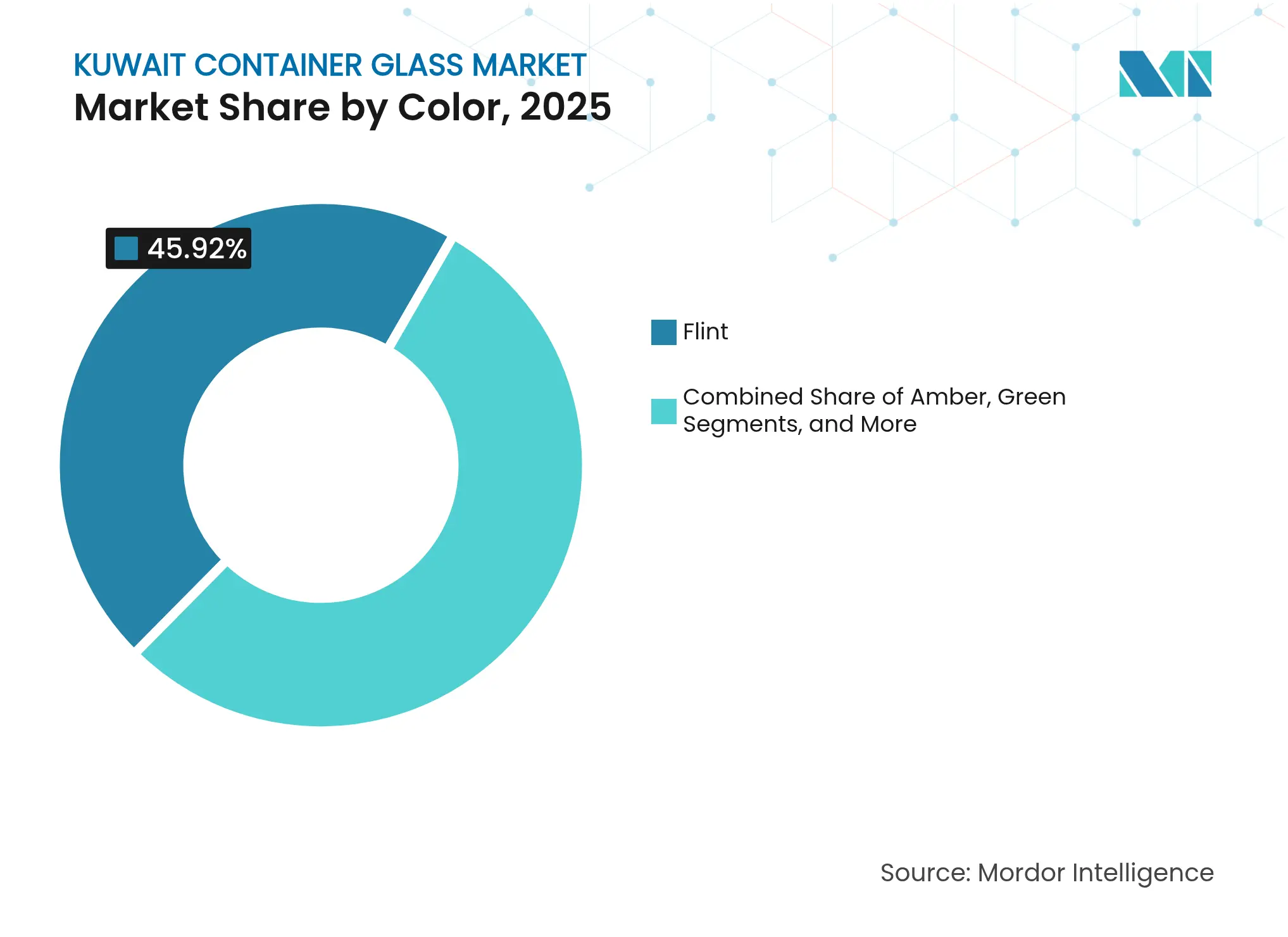

- By color, the Kuwait container glass market for amber glass is projected to grow at a 6.31% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Container Glass Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Urbanisation and shift to sustainable packaging Urbanisation and shift to sustainable packaging | +0.8% | Kuwait national, spillover to GCC | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:Kuwait national, spillover to GCC | Impact Timeline:Medium term (2-4 years) |

Premium-pack product boom across sectors Premium-pack product boom across sectors | +0.7% | Kuwait core, regional luxury markets | Short term (≤ 2 years) | |||

Beverage industry capacity expansions Beverage industry capacity expansions | +0.6% | Kuwait and neighboring GCC states | Medium term (2-4 years) | |||

Vision-2035 recycling incentives Vision-2035 recycling incentives | +0.5% | Kuwait national policy scope | Long term (≥ 4 years) | |||

Niche GCC perfumery export demand Niche GCC perfumery export demand | +0.4% | GCC regional, Kuwait as production hub | Medium term (2-4 years) | |||

Pharma track-and-trace localisation Pharma track-and-trace localisation | +0.3% | Kuwait national, GCC regulatory alignment | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Urbanization and shift to sustainable packaging

Kuwait’s population clusters continue widening around Kuwait City, driving higher per-capita consumption of packaged food and beverage items. Urban shoppers increasingly favor recyclable substrates and are influenced by municipal green-labeling programs that highlight glass’s closed-loop recyclability. Supermarket chains have responded by trialing glass-only aisles for premium water and juice SKUs, thereby reinforcing brand visibility and nudging suppliers toward thicker, embossed bottles that can withstand multiple reuse cycles. The Public Authority for Industry has further accelerated the adoption of eco-score labeling, which assigns penalty points to multilayer plastics. These combined measures elevate the Kuwait container glass market as a visible beneficiary of sustainability-linked consumer preferences.

Premium-pack product boom across sectors

Luxury positioning permeates beverages, fragrances, and gourmet condiments, each leaning on glass to project authenticity and shelf appeal. Regional fragrance houses demand intricate flacons with UV-blocking pigments and ornate closures, orders that command unit prices multiple times higher than commodity soft-drink bottles. High-end water brands have shifted their flagship SKUs from PET to flint glass with cobalt accents, marketing the switch as a guarantee of zero microplastics. Food processors have adopted squat, wide-mouth jars with decorative embossing that reinforces artisanal cues, further lifting glass tonnage despite modest fill volumes. Gulf Glass Manufacturing Company has capitalized by dedicating one furnace line to small-volume, high-color-precision runs, bolstering margins and export potential.

Beverage industry capacity expansions

Soft-drink bottlers, dairy processors, and specialty coffee brewers have added new fillers that collectively raise container demand. The United Beverage Company’s historical experience highlights how fill-line investments quickly translate into packaging orders; modern fillers now request heavier-gauge returnable bottles that can withstand 35-40 trips before being recovered as cullet. Neighboring Qatar’s new 1 million-unit-per-day facility signals a regional bid to internalize packaging supply, which may divert some Kuwaiti exports, but simultaneously opens toll-manufacturing opportunities for niche SKUs. Kuwaiti water brands eye premium export channels into Bahrain and Oman, preferring domestically sourced glass that satisfies country-of-origin marketing claims.

Vision-2035 recycling incentives

The National Waste Management Strategy 2040 sets landfill diversion targets that closely track EU benchmarks and earmarks funding for separate glass collection streams.[2]Fraunhofer UMSICHT, “Waste Management Plan for Kuwait,” fraunhofer.de Pilot curbside schemes in Hawalli have already increased recovered glass by 280% year-over-year, delivering cullet feedstock that reduces furnace energy consumption by 4% for every 10 percentage points of cullet ratio. Planned reverse vending machines at retail outlets will further boost return rates, anchoring a circular model that solidifies long-term glass competitiveness. Subsidized grants for optical sorters and cullet wash plants aim to stabilize cullet quality, a crucial variable for color control during furnace charging.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Substitution by plastics and aluminium Substitution by plastics and aluminium | -1.2% | Kuwait national, regional competitive pressure | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.2% | Geographic Relevance:Kuwait national, regional competitive pressure | Impact Timeline:Short term (≤ 2 years) |

Rising energy costs after fuel-subsidy reforms Rising energy costs after fuel-subsidy reforms | -0.8% | Kuwait national manufacturing sector | Medium term (2-4 years) | |||

Shortage of domestic cullet Shortage of domestic cullet | -0.6% | Kuwait national, regional supply chain | Medium term (2-4 years) | |||

Gulf-route raw-material supply risk Gulf-route raw-material supply risk | -0.4% | Kuwait import-dependent supply chains | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Substitution by plastics and aluminium

PET and lightweight cans remain formidable challengers where unit economics trump brand aesthetics. Petrochemical complexes that came online after 2024 are offering bottle-grade resin at aggressive transfer prices to integrated beverage groups, widening the cost delta per liter between plastic and glass. Aluminum smelters have sharpened recycling loops, enabling near-closed-loop can recovery that rivals glass’s sustainability narrative. The success of can conversions in local carbonated soft drinks during the 1980s serves as a reference point for how swiftly end-markets can pivot when promotional pricing aligns with consumer convenience. Unless glass producers maintain differentiated value through shape innovation and refill-centric business models, volume leakage to substitute materials could intensify.

Rising energy costs after fuel-subsidy reforms

The 2024-2025 phased withdrawal of industrial energy subsidies resulted in a more than 100% increase in gas tariffs, directly inflating glass melting costs, which rely on continuous 1,600 °C furnaces. Comparative benchmarking reveals that energy accounts for roughly 22% of the total cost of goods sold in similar emerging markets. Kuwait’s jump places local producers at a temporary disadvantage against newer furnaces in Saudi Arabia that combine oxy-fuel combustion with waste-heat recovery. Gulf Glass Manufacturing Company has responded by contracting an audit with the International Finance Corporation to model electrode boost retrofits that could slash specific energy by up to 15%. The payback horizon, however, remains sensitive to volatile LNG import prices that track global indices rather than historical domestic subsidies.

Segment Analysis

By End-user: Beverages sustain dominance while personal care accelerates

The beverages segment accounted for 57.88% of the Kuwait container glass market size in 2025, driven by high-throughput carbonated soft drink and juice lines that favor returnable glass for reuse economics. Non-alcoholic malt variants, kombucha, and craft coffee concentrate are expanding shelf presence, adding format variety, and driving bespoke mold orders. Returnable bottle pools managed by leading fillers typically average 18-20 rotation cycles annually, maintaining a stable baseline tonnage. Meanwhile, public health campaigns promoting reduced plastic usage in ready-to-drink water have catalyzed a premium glass tier that commands double-digit price premiums and enhances segment resilience against can encroachment.

Cosmetics and personal care volumes are forecast to rise at a 6.74% CAGR through 2031, outpacing all other applications. Regional fragrance houses require small-format flacons that utilize Kuwait’s color-flexible batch furnaces, enabling rapid changeovers. GCC travelers purchasing high-value oud and bukhoor variants at duty-free outlets reinforce export opportunities, particularly as brand owners prioritize Made-in-GCC provenance. This demand is less price-sensitive, enabling Gulf Glass Manufacturing Company to offset higher energy tariffs through value-added decoration such as acid etching and screen printing. Pharmaceutical vials and food condiment jars provide steady base-load demand, benefiting from the inertness of glass and adherence to ISO 22000:2005 food-safety and PAS 223:2011 prerequisite standards.

Note: Segment shares of all individual segments available upon report purchase

By Color: Flint leads, amber rises on regulated uses

Flint captured 45.92% of the Kuwait container glass market share in 2025, reflecting consumer preference for product visibility and label vibrancy in soft drinks, juices, and premium water. Fillers exploit flint’s clarity to showcase color cues while leveraging UV-absorbing coatings when required. Higher cullet ratios in flint batches promote energy savings but demand strict contaminant control to avoid color-cast deviations.

Amber glass is projected to expand at a 6.31% CAGR through 2031, as pharmaceutical and specialty beverage applications increasingly mandate UV protection. Regulatory guidance for light-sensitive antibiotics and nutraceutical beverages repeatedly cites amber as the preferred barrier, prompting capacity allocation toward darker melts. Batch formulations rely on iron, sulfur, and carbon chromophores; securing the sourcing of these additives becomes an operational imperative, given Kuwait’s import-dependent raw-material matrix. Green and specialty tints occupy niche roles, often commissioned for limited-edition perfumery or seasonal beverage launches that reward distinct shelf differentiation over economies of scale.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Kuwait remains the sole domestic source of container glass within its borders, operating a 280-ton-per-day plant that supplies both local fillers and export channels. The Kuwait container glass market benefits from seamless road connectivity to key seaports that handled 863,618 TEU in 2024, enabling cost-effective palletized shipments across the Gulf. Export consignments typically move under regional free-trade provisions that zero-rate customs duties, preserving Kuwait’s competitiveness despite distance penalties relative to emergent Qatari and Saudi furnaces.

New capacity in Doha and Dammam is reshaping trade flows. Qatari buyers, who historically imported entire bottle lots from Kuwait, now enjoy a domestic supply for mainstream beverages, prompting Kuwaiti producers to redeploy tonnage toward higher-margin personal care and pharmaceutical clients in Bahrain, Oman, and Iraq. Such pivoting is facilitated by ISO-accredited quality systems that exceed the minimum regional pharmacopeia standards, creating a defensible moat against newer plants that have yet to complete qualification audits.

Kuwait’s National Waste Management Strategy 2040 introduces a circular economy dimension into geographic dynamics. Investments in cullet-processing hubs adjacent to Shuaiba Port would concentrate reclaimed glass, reducing inland haulage and reclaiming cost advantages for Kuwait's exports. However, current cullet recovery rates fall well below the planned 50% target, leaving furnaces dependent on virgin silica sand and soda ash, which are imported mainly through the Gulf-route supply chain. This supply chain itself is vulnerable to disruptions in shipping lanes and price volatility.

Competitive Landscape

Market Concentration

Gulf Glass Manufacturing Company operates two regenerative furnaces and five production lines, and maintains ISO 9001, ISO 14001, and ISO 22000 certifications, solidifying its role as the backbone of the Kuwait container glass market. The company’s 280 tons-per-day capacity is modest in global terms but adequate for the 124.06 kilotons domestic market, especially given its 50% export mix targeting nearby GCC states. Monopolistic status delivers scale economies in procurement and logistics, yet also concentrates systemic risk; an unplanned furnace outage could trigger immediate supply gaps for national beverage fillers.

Regional challengers are scaling aggressively. Qatar Industrial Manufacturing Company’s 200 tons-per-day greenfield plant started commercial production in July 2024 and aims to double capacity, while Saudi Arabia’s Zoujaj Glass revamped a line to 150,000 metric tons annually. Both compete on freight proximity to high-volume beverage fillers and on newer energy-efficient furnace technology. Kuwait’s incumbent, therefore, invests in oxy-fuel retrofit studies, automated hot-end inspection cameras, and lightweight bottle designs that cut glass per unit by up to 12%, narrowing freight costs without compromising strength.

Strategic focus is shifting toward premium niches. Perfume bottles, pharma vials, and returnable beverage bottles with enhanced color consistency represent product arenas less susceptible to commoditized price wars. The company has signed multi-year supply agreements with leading fragrance houses and commenced trial batches with borosilicate blends for injectable drug formats, underscoring a pivot from volume to value. Simultaneously, it explores joint ventures with local waste management firms to secure cullet streams, thereby tying raw material security to municipal recycling performance.

Kuwait Container Glass Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Qatar Industrial Manufacturing Company began commercial production at its 200 tons-per-day glass container facility, marking Qatar’s first domestic source of beverage and food bottles.

- July 2024: Middle East Glass ownership shifted when Gulf Capital exited, and MENA Glass Holdings took majority control after doubling capacity to more than 385,000 metric tons annually.

- April 2024: Şişecam commissioned a USD 145 million furnace at Eskişehir, adding 198,000 tons annual capacity and creating the world’s largest integrated glass hub.

- March 2024: Kuwait’s Public Authority for Industry released its National Industrial Strategy 2035, calling for KWD 11 billion in industrial capital and emphasizing sustainable packaging.

Table of Contents for Kuwait Container Glass Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Urbanisation and shift to sustainable packaging

- 4.2.2Premium-pack product boom across sectors

- 4.2.3Beverage industry capacity expansions

- 4.2.4Vision-2035 recycling incentives

- 4.2.5Niche GCC perfumery export demand

- 4.2.6Pharma track-and-trace localisation

- 4.3Market Restraints

- 4.3.1Substitution by plastics and aluminium

- 4.3.2Rising energy costs after fuel-subsidy reforms

- 4.3.3Shortage of domestic cullet

- 4.3.4Gulf-route raw-material supply risk

- 4.4PESTEL Analysis

- 4.5Industry Supply-Chain Analysis

- 4.6Container Glass Furnace Capacity and Locations in Kuwait

- 4.6.1Plant Locations and Year of Commencement

- 4.6.2Production Capacities

- 4.6.3Types of Furnaces

- 4.6.4Color of Glass Produced

- 4.7Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.7.1Import Volume and Value, 2021-2024

- 4.7.2Export Volume and Value, 2021-2024

- 4.8Porter’s Five Forces Analysis

- 4.8.1Threat of New Entrants

- 4.8.2Bargaining Power of Suppliers

- 4.8.3Bargaining Power of Buyers

- 4.8.4Threat of Substitutes

- 4.8.5Competitive Rivalry

- 4.9Raw Material Analysis

- 4.10Recycling Trends for Glass Packaging

- 4.11Demand vs Supply Analysis for Glass Packaging

5. MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1By End-user

- 5.1.1Beverages

- 5.1.1.1Alcoholic

- 5.1.1.1.1Beer

- 5.1.1.1.2Wine

- 5.1.1.1.3Spirits

- 5.1.1.1.4Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2Non-Alcoholic

- 5.1.1.2.1Juices

- 5.1.1.2.2Carbonated Drinks (CSDs)

- 5.1.1.2.3Dairy Product Based Drinks

- 5.1.1.2.4Other Non-Alcoholic Beverages

- 5.1.2Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3Cosmetics and Personal Care

- 5.1.4Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5Perfumery

- 5.2By Color

- 5.2.1Green

- 5.2.2Amber

- 5.2.3Flint

- 5.2.4Other Colors

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves and Developments

- 6.3Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Gulf Glass Manufacturing Co.

- 6.4.2Feemio Group Co., Ltd.

- 6.4.3Mexim Company W.L.L

- 6.4.4Qingdao Qitengyongxin Glass Products Co., Ltd

- 6.4.5Coming Century Company WLL

- 6.4.6Pragati Glass Pvt. Ltd.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Kuwait Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Kuwait container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.