Cameroon Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

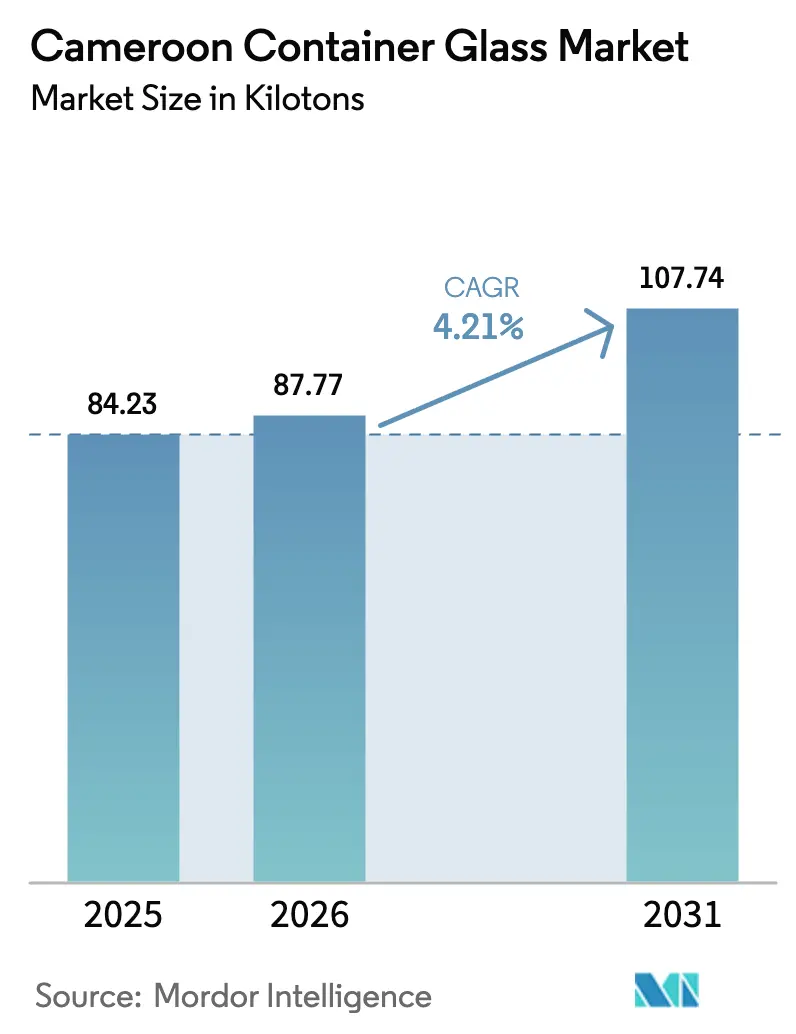

| Base Year Market Size (2025) | 84.23 kilotons |

| Market Volume (2026) | 87.77 kilotons |

| Market Volume (2031) | 107.74 kilotons |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

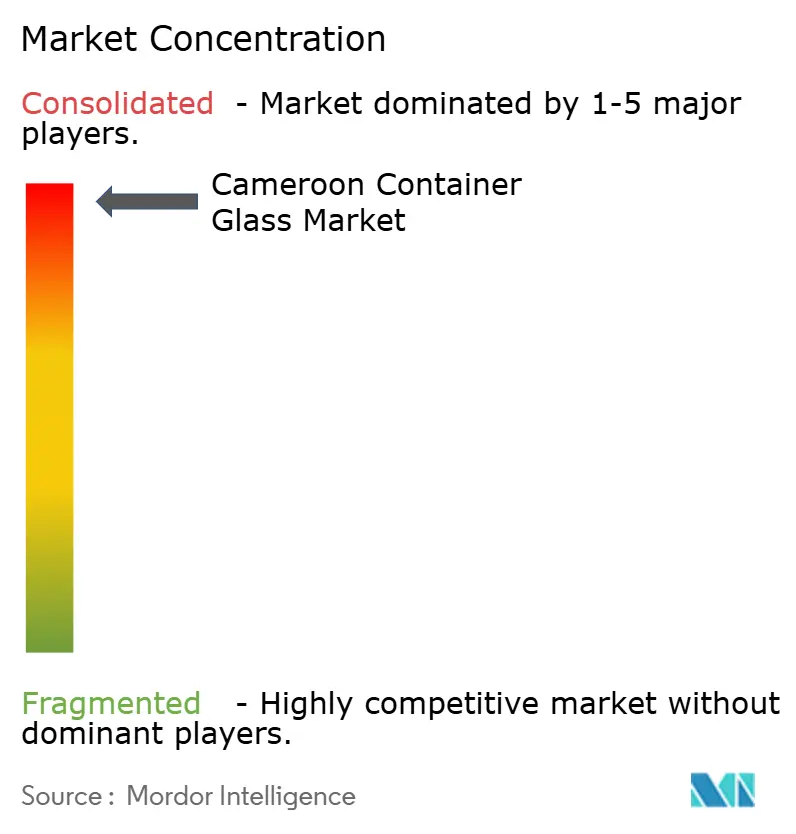

| Market Concentration | High |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cameroon Container Glass Market Analysis by Mordor Intelligence

Cameroon container glass market size in 2026 is estimated at 87.77 kilotons, growing from 2025 value of 84.23 kilotons with 2031 projections showing 107.74 kilotons, growing at 4.21% CAGR over 2026-2031. Robust beverage-sector spending, deeper CEMAC trade integration, and widening premium-packaging adoption across pharmaceuticals and alcoholic drinks combine to propel the Cameroon container glass market. Imports of industrial equipment rose to USD 944.4 million in 2024, modernizing bottling lines in Douala and Yaoundé and signaling greater domestic capacity to convert cullet and virgin raw materials into finished containers.[1]Ecofin Agency, “Cameroon’s Industrial Equipment Imports Reach Six-Year High at USD 944.4 Million,” ecofinagency.com Vertical integration remains a defining feature, as SOCAVER, embedded within Brasseries du Cameroun, supplies in-house beer and soft drink demand while defending margins against fluctuations in power and fuel costs. Even so, furnace operations face persistent volatility; retail fuel prices climbed 40% between 2022 and 2024, and the removal of subsidies slated for 2026 could elevate energy’s share of production costs. Competitive pressure is intensifying as Beta Glass of Nigeria has completed a USD 15.3 million furnace rebuild and increased exports to Francophone Africa, sharpening price discipline within the Cameroon container glass market.

Key Report Takeaways

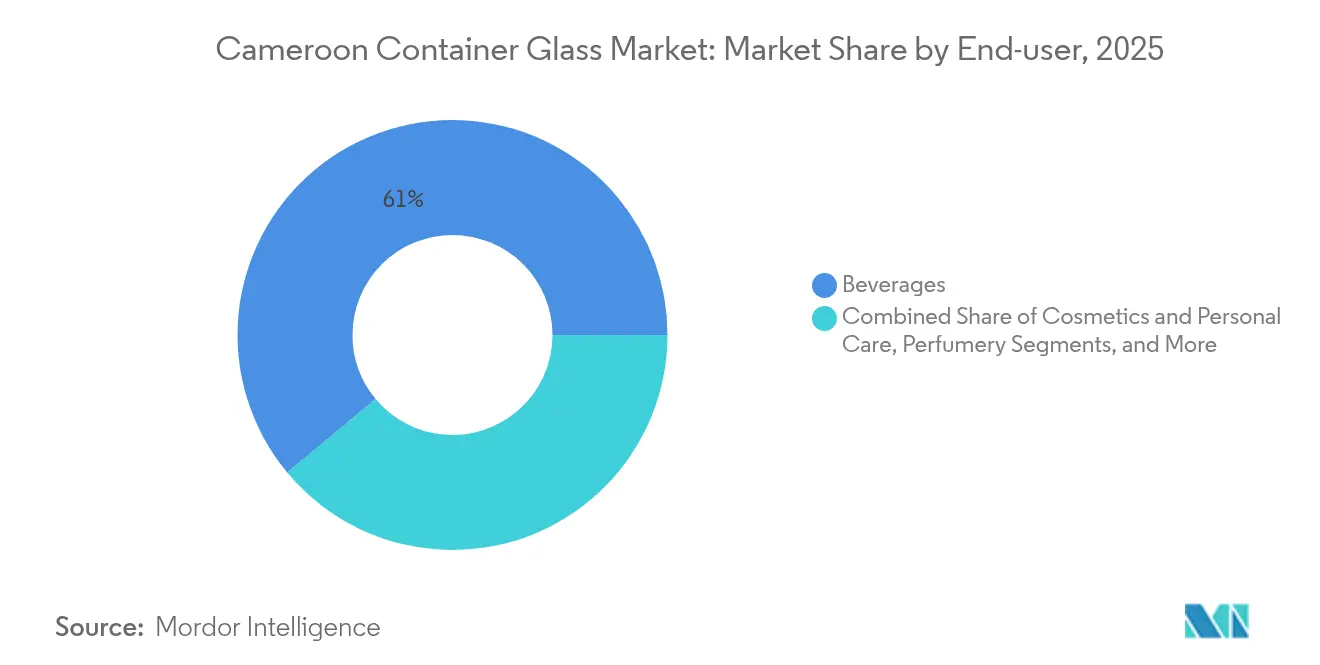

- By end-user, beverages captured 61.05% of the Cameroon container glass market share in 2025.

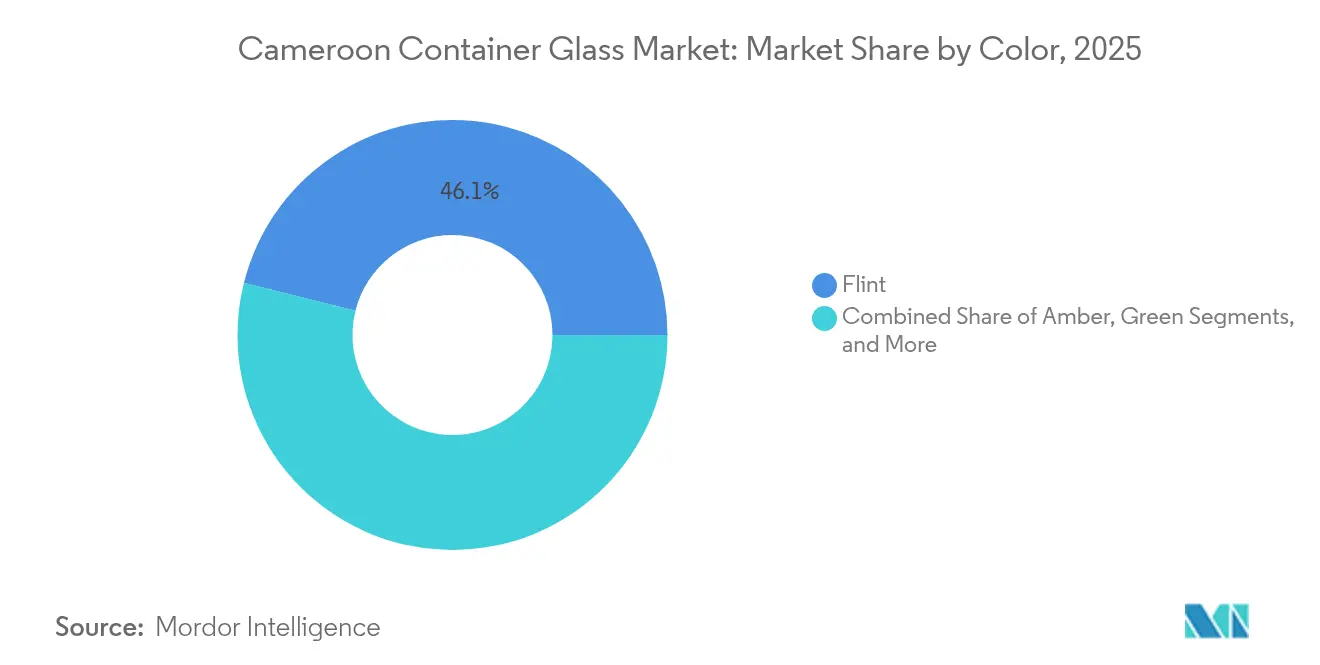

- By color, the Cameroon container glass market for amber glass is projected to grow at a 5.63% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Cameroon Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eco-conscious consumer preference surge | +0.8% | Douala and Yaoundé | Medium term (2-4 years) |

| Food and beverage sector capacity expansion by bottlers | +1.2% | Douala, Yaoundé, Bafoussam, Garoua | Short term (≤ 2 years) |

| Government tax incentives on recycled glass inputs | +0.4% | National | Long term (≥ 4 years) |

| Rising premiumisation in alcoholic beverages | +0.6% | Urban centers nationwide | Medium term (2-4 years) |

| Growth of pharmaceutical glass primary packaging | +0.7% | National and CEMAC export | Medium term (2-4 years) |

| Niche export demand from neighboring CEMAC countries | +0.5% | Regional trade via Douala and Kribi ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food and Beverage Sector Capacity Expansion by Local Bottlers

Local beverage producers continue to invest record amounts in brewhouses and soft-drink lines, driving growth in the Cameroon container glass market. Following its 2022 acquisition of Guinness Cameroon, Société Anonyme des Brasseries du Cameroun launched a CFA 200 billion (USD 323 million) five-year modernization program across Douala, Yaoundé, Bafoussam, and Garoua, incorporating high-speed fillers and automated cullet-handling systems that promote the use of returnable glass bottles. Returnable systems extend each bottle’s life cycle yet demand frequent replenishment because breakage and abrasion retire up to 10% of the circulating pool annually. Union Camerounaise de Brasseries achieved a 50% increase in throughput and a 40% reduction in CO₂ consumption after installing next-generation lines, illustrating the operating-cost benefits that reinforce the adoption of glass packaging. Boissons du Cameroun’s CFA 21 billion (USD 34 million) upgrade added new fillers in Yaoundé and Bafoussam, and incorporated glassmaking modules into its training curricula, thereby deepening the technical labor pool.[2]Boissons du Cameroun, “Les Boissons du Cameroun | Plus d’un demi-siècle de qualité !,” boissonsducameroun.com Concentration of these upgrades in Cameroon’s four largest cities lowers logistics costs and streamlines cullet flows, anchoring growth momentum for the Cameroon container glass market.

Rising Premiumisation in Alcoholic Beverages

Urban consumers increasingly favor premium lagers, specialty spirits, and imported wines, all of which require high-clarity or amber glass to convey brand value. Heineken and Castel enhance brand equity by retaining glass, even in single-serve formats, while maintaining higher unit margins than PET or can alternatives, and reinforcing their share of the Cameroon container glass market. On-trade outlets account for more than half of alcoholic drink sales, and reusable bottles circulate through bars and small retail outlets, thereby embedding glass in consumption patterns. Niche opportunities emerge in traditional corn beer (sha); the beverage employs an estimated 30,000 workers but requires pressure-rated glass to support controlled secondary fermentation, presenting an opportunity for specialized containers. Premium spirits tend to lean strongly toward amber glass for ultraviolet protection, which explains the 5.89% CAGR expected for this color segment. Decorative techniques such as screen printing and embossing are gaining ground, suggesting added-value niches inside the Cameroon container glass market.

Growth of Pharmaceutical Glass Primary Packaging

Cameroon’s health-care expansion is translating into higher demand for molded and tubular vials, syrup bottles, and ophthalmic droppers. The global sodium-calcium molded vial segment is projected to rise from USD 2.5 billion in 2025 to USD 3.6 billion in 2033, and local buyers are aligning with this direction. While China supplies over 70% of the world's vials, pandemic-era disruptions have exposed supply-chain risks and strengthened arguments for regional manufacturing. Hospitals in Yaoundé and Douala now specify USP Type I and Type II amber containers for light-sensitive injectables, opening a premium niche within the Cameroon container glass market. Pharma distributors also ship to Chad, the Central African Republic, and Gabon duty-free under CEMAC rules, amplifying export potential. Quality compliance adds price-inflexibility, enabling container producers to offset rising soda-ash input costs and stabilize margins.

Government Tax Incentives on Recycled Glass Inputs

A national circular-economy roadmap adopted in October 2024 targets 25% renewable energy integration and 35% greenhouse-gas reduction by 2030. Draft fiscal guidelines propose a reduced value-added tax on cullet purchases and accelerated depreciation for cullet-processing equipment, designed to narrow raw material import exposure and drive up domestic recycling. At present, only 4% of municipal waste enters formal recycling streams, yet informal networks pay around CFA 100 per kilogram for recovered glass, suggesting a latent supply if collection logistics improve. Official waste-management registries maintained by MINEPDED offer potential public-private partnerships that could channel glass back into furnaces. Adoption lags, but when enacted, tax incentives would trim batch costs, lower furnace energy demand (cullet melts at 200 °C less than virgin mix), and enhance the competitiveness of the Cameroon container glass market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET substitution in carbonated soft drinks | -0.9% | Urban retail channels nationwide | Short term (≤ 2 years) |

| High energy cost volatility for furnace operations | -1.1% | All manufacturing facilities | Short term (≤ 2 years) |

| Currency-linked soda-ash import dependence | -0.7% | National exchange-rate exposure | Medium term (2-4 years) |

| Inefficient national waste-glass collection | -0.5% | Rural areas most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Energy Cost Volatility for Furnace Operations

Fuel-price escalation raises operational uncertainty across the Cameroon container glass market. Gasoline prices rose from USD 1.19 to USD 1.39 per liter and diesel from USD 1.17 to USD 1.37 per liter in February 2024, as the government subsidy reduction took effect. Container glass furnaces require a temperature of around 1,450 °C for continuous melting; a 10 °C drop in flame temperature can lower the pull rate by 1%. Since the 2019 Limbe refinery fire, Cameroon has imported all refined petroleum, exposing producers to global price surges until the Kribi refinery opens in 2027. Natural-gas output quadrupled to 2.5 billion m³ in 2023, yet industrial tariff structures remain unresolved, limiting switching potential. A rising electricity demand forecast of 15-17 TWh by 2035 could further strain the supply, risking periodic outages that interrupt glass production cycles and curtail growth in the Cameroon container glass market.

PET Substitution in Carbonated Soft Drinks

PET bottles weigh about one-fifth as much as equivalent glass containers and seldom break in distribution, giving them an immediate logistics advantage in single-use beverage channels. The mineral-water segment, led by Stricam, with a capacity of 291,000 hectoliters, already relies almost exclusively on PET, while its juice line produces 17 million liters annually using a mix of PET and glass. Plastic’s cost superiority pressures the Cameroon container glass market, especially in urban supermarkets where convenience packaging dominates. Recycling infrastructure remains embryonic; Stricam’s own plastic-recycling plant processes 17,280 t annually, but Cameroon lacks bottle-to-bottle loops that would mitigate PET’s environmental footprint. Regulatory discussions on single-use plastics are ongoing, which could temper PET growth; however, in the near term, substitution erodes the share of glass in soft drinks and bottled water.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Demand Amid Diversification

Beverages accounted for 61.05% of the Cameroon container glass market size in 2025, driven by beer returnable cycles and growing premium spirit volumes. Beer bottles circulate in deposit loops of eight to ten trip cycles, sustaining replacement demand despite reuse, while premium spirit brands favor heavier flint or amber bottles that convey upmarket cues. Carbonated soft drinks show mixed dynamics: local players maintain glass for legacy one-liter formats but shift single-serve SKUs to PET, trimming incremental glass volume. Juice producers like Stricam are increasingly applying glass to their organic lines, targeting affluent urban buyers and balancing the substitution trend. Food applications such as jams, condiments, and edible oils maintain steady throughput because glass ensures barrier performance and shelf-life stability. The cosmetics and personal-care category, growing at a 5.47% CAGR, is driven by rising disposable incomes and brand positioning strategies that associate glass with cleanliness and a premium feel, carving out additional space for the Cameroon container glass market. Pharmaceutical demand outside vials aligns with hospital construction and pharmacy retail expansion, while perfumery and luxury candles form a small but margin-rich niche that maximizes decorative finishes.

Ongoing diversification helps buffer the Cameroon container glass market against potential substitution by PET in the soda industry. Breweries continue to purchase multi-trip bottles, while cosmetic and pharma clients integrate amber and flint formats with tamper-evident finishes. Producers differentiate themselves through lightweighting programs that trim bottle mass by 5-7 g without compromising strength, thereby reducing freight costs and emissions. Such optimizations become increasingly attractive as fuel prices rise. Fresh investment in end-of-line inspection and automatic labeling also enhances quality consistency, reinforcing customer loyalty across non-beverage segments that are now scaling volume in the Cameroon container glass market.

By Color: Flint Dominance with Amber Acceleration

Flint bottles captured 46.10% of the Cameroon container glass market share in 2025, reflecting wide acceptance in beer, edible oils, and non-alcoholic beverages, where product visibility drives consumer trust. High furnace utilization on clear glass maximizes pull rate and reduces color-change downtime, underscoring its cost leadership. Breweries request Flint for export labels destined for regional markets that prefer transparent bottles to verify fill level and color integrity. Green glass serves a narrower range of wine and specialty beer but remains structurally limited by Cameroon’s modest grape-wine bottling base. Specialized custom shades are primarily featured in perfume and cosmetics, leveraging small-batch production for branding impact; however, overall tonnage remains marginal within the Cameroon container glass market.

Amber containers are forecast to grow at 5.63% CAGR through 2031, reflecting both pharmaceutical-quality specifications and premium spirit adoption. Pharmacists increasingly insist on amber for photosensitive formulations, while craft brewers emulate European lager traditions that rely on brown glass to block ultraviolet rays, extending shelf life. Amber’s rising share stimulates batch-house modifications and colorant-handling upgrades, prompting producers to invest in automatic color feeders and oxygen-optimized furnaces to preserve amber consistency. Although amber pigment raises batch cost, higher selling prices in pharma and spirit channels offset expense, protecting contribution margins and supporting broader revenue growth inside the Cameroon container glass market.

Geography Analysis

Douala and Yaoundé generate the lion’s share of demand and supply; together, they contain most of Cameroon’s brewery, soda, and pharmaceutical fill lines, along with SOCAVER’s central furnace, reinforcing a clustered supply model within the Cameroon container glass market. Douala’s port handles over 70% of containerized imports. A new 25-hectare empty-container logistics platform, announced in May 2025, will streamline inbound soda-ash and outbound filled bottles, creating 1,200 jobs. Yaoundé complements Douala with pharmaceutical storage and national-level distribution, benefiting from road freight corridors that link to rural clinics.

Secondary hubs Bafoussam and Garoua draw new filling lines under SABC’s five-year capex plan, narrowing freight distances to northern and western consumers and adding redundancy that shelters the Cameroon container glass market from localized outages. Kribi’s deep-sea port, whose second container berth opened in May 2025, increased capacity to over 1 million TEUs per year. The port features a draft suitable for 15,000-TEU vessels, reducing ocean-freight transit times and expanding direct links to Asia for furnace refractory and mold imports. Faster maritime routes help mitigate the landed cost of soda ash, cullet additives, and decorative sleeves, slightly offsetting currency volatility risk.

CEMAC integration magnifies export prospects. Seventy-seven Cameroonian firms now hold duty-free status for regional sales, and glassware exports to Gabon reached USD 3.4 million in 2021, indicating a solid foothold. Yet inland freight costs remain steep; shipping a 20-foot container from Douala to Bangui can reach USD 4,000, hindering price competitiveness until road and rail upgrades close the gap. Despite this friction, coordinated customs clearance, common product standards, and the franc-zone currency regime lower administrative barriers and reinforce the Cameroon container glass market’s positioning as a regional supply base.

Competitive Landscape

A moderate concentration prevails, with vertical integration influencing bargaining power. SOCAVER secures raw-glass output for its parent, Brasseries du Cameroun, maintaining furnace throughput above 90% even during periods of demand dips, and supplies external food and pharmaceutical clients on a spot or short-term contract basis. Beta Glass’s June 2024 furnace rebuild increased Nigerian capacity by 30 t/day and introduced advanced combustion control, reducing fuel use by 12%, thereby sharpening cross-border competition. Boissons du Cameroun acts as a captive buyer while also influencing technical standards through glassmaking training programs open to third parties.

Energy efficiency surfaces as a differential advantage: plants installing electric forehearth boosting and oxy-fuel burners report up to 18% energy savings. Producers also explore lightweighting; SOCAVER shaved 6 g off its flagship 60 cl beer bottle, saving 11% glass per unit without affecting fracture resistance. Raw-material strategies diverge: SOCAVER imports soda ash mainly from Europe and Turkey; Beta Glass trials East African soda ash via Kenyan suppliers to hedge currency risk and shorten shipping distance. Investment pipelines favor amber-colored capabilities to serve the pharma and spirits sectors; a greenfield project under evaluation near Kribi would tap nearby LNG supplies to power an all-oxy furnace, potentially adding 50 kt of annual capacity to the Cameroon container glass market by 2028.

Customer service innovation is expanding beyond packaging supply into logistics and bottle collection solutions. Breweries negotiate bundled contracts that cover bottle purchase, freight, and reverse logistics services, prompting glassmakers to either integrate their own trucking fleets or partner with third-party logistics providers. Margin pressure from currency swings and fuel costs is partly mitigated by index-linked surcharges that adjust monthly.

Cameroon Container Glass Industry Leaders

Pragati Glass Pvt. Ltd.

Shandong Province Medicinal Glass Co., Ltd.

Société Camerounaise de Verrerie

Feemio Group Co., Ltd.

Beta Glass Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kioo Ltd secured USD 60 million financing to scale East and Central African bottle output and raise recycled-glass input to 40%.

- May 2025: Kribi port inaugurated a second container terminal, expanding throughput to over 1 million TEUs annually and enabling direct Asia services.

- May 2025: Port Autonome de Douala agreed a CFA 50.4 billion public-private partnership for a 25-hectare empty-container logistics platform.

- October 2025: Cameroon approved a national circular-economy roadmap aimed at 35% GHG reduction by 2030.

Cameroon Container Glass Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

The Cameroon container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current size of the Cameroon container glass market?

The market stood at 87.77 kilotons in 2026 and is forecast to reach 107.74 kilotons by 2031 at a 4.21% CAGR.

Which end-user segment accounts for the most container glass demand in Cameroon?

Beverages lead, holding 61.05% of national demand, underpinned by returnable beer bottles and premium spirits.

What color segment is growing fastest?

Amber bottles, driven by pharmaceutical requirements and premium alcoholic beverages, are projected to register a 5.63% CAGR through 2031.

How are energy costs affecting glass production?

A 40% fuel-price surge between 2022 and 2024, combined with pending subsidy removal, is elevating furnace operating expenses and pressuring margins.

Are recycled materials gaining traction in Cameroonian glass furnaces?

Government draft tax incentives on cullet and a circular-economy roadmap are spurring interest, though current formal recycling captures only 4% of municipal waste.

Which regional trade agreements support export potential?

CEMAC duty-free rules now cover 77 Cameroonian firms, enabling container glass shipments to Gabon, Central African Republic, and other neighbors.

Page last updated on: