Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

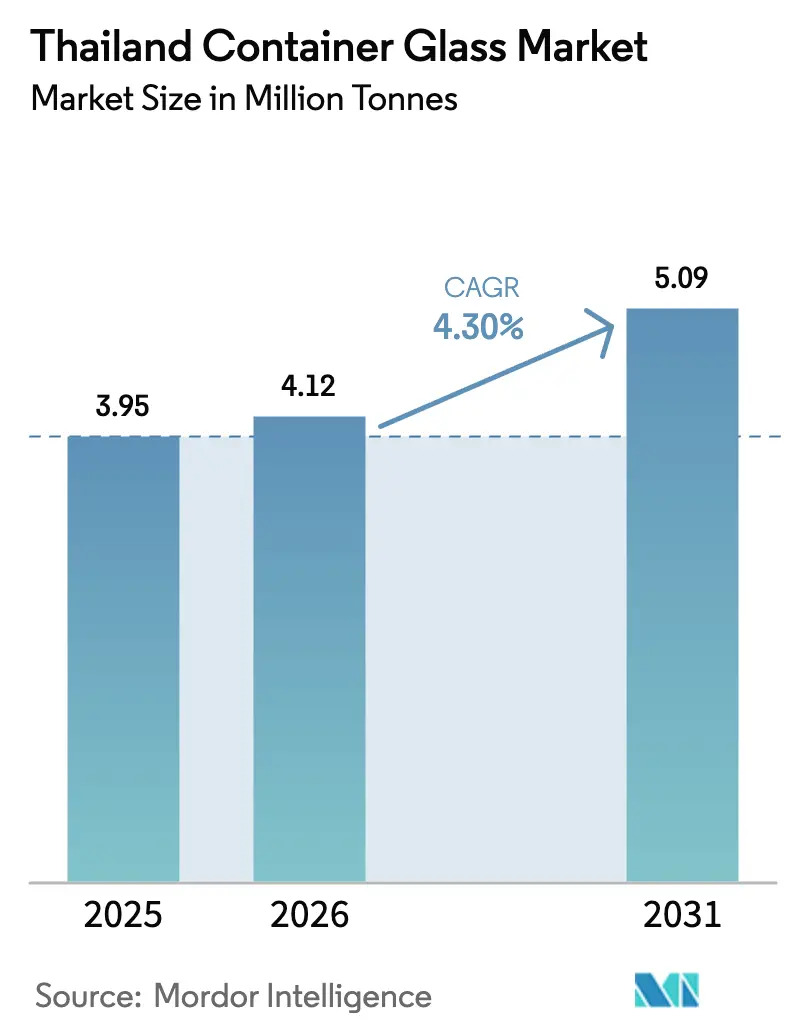

| Base Year Market Size (2025) | 3.95 Million tonnes |

| Market Volume (2026) | 4.12 Million tonnes |

| Market Volume (2031) | 5.09 Million tonnes |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Container Glass Market Analysis by Mordor Intelligence

The Thailand Container Glass Market size was valued at 3.95 million tonnes in 2025 and estimated to grow from 4.12 million tonnes in 2026 to reach 5.09 million tonnes by 2031, at a CAGR of 4.30% during the forecast period (2026-2031). Robust tourism-driven beverage consumption, the government’s plastic-waste reduction roadmap, and brand premiumization in both beverage and cosmetics categories underpin this steady expansion. Demand resilience also draws momentum from the voluntary elimination of plastic cap-seals in bottled water, which achieved a 98% reduction among small bottlers by 2019, signaling broad-based acceptance of glass as a sustainable alternative.[1]Pollution Control Department, “Draft Action Plan for Plastic Waste Management Phase 1,” PCD.go.th Thailand’s carbon tax of THB 200 (USD 5.67) per tonne of CO₂ equivalent reinforces the shift, favoring infinitely recyclable glass over single-use plastics. Meanwhile, cost-mitigation incentives tied to cullet usage above 60% partially offset energy-intensive furnace operations, tempering the inflationary impact of rising electricity tariffs.

Key Report Takeaways

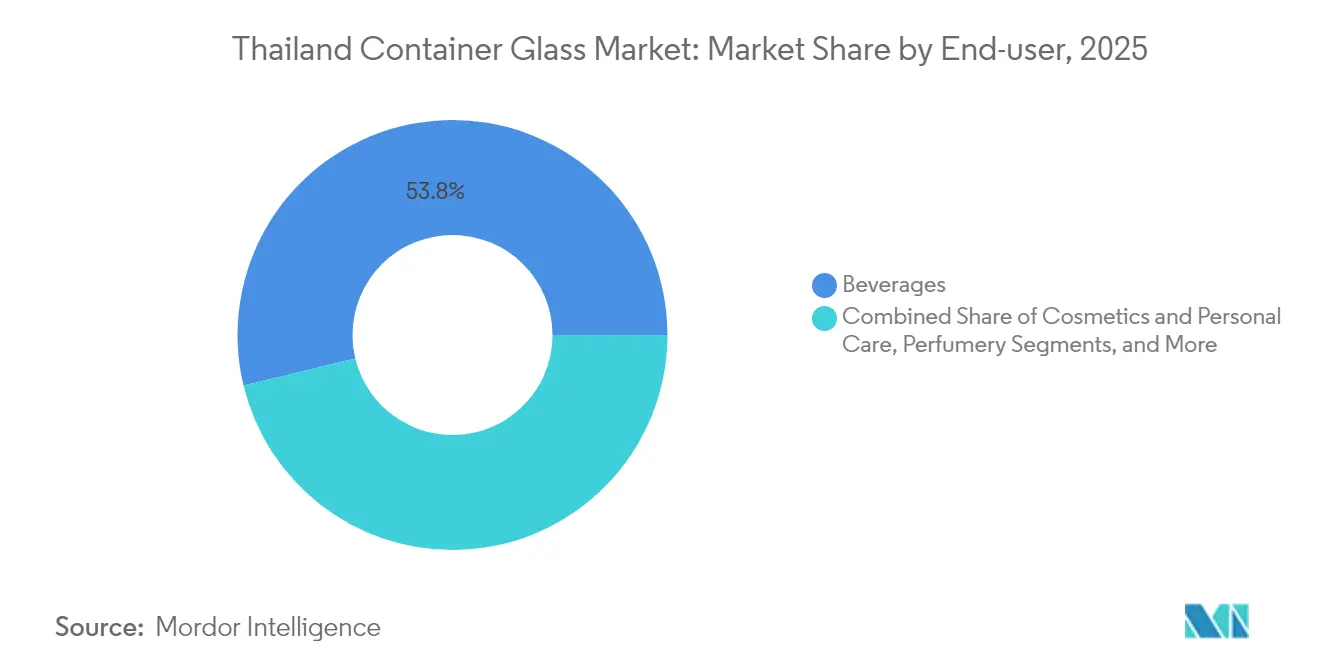

- By end-user, beverages captured 53.78% of the Thailand container glass market share in 2025.

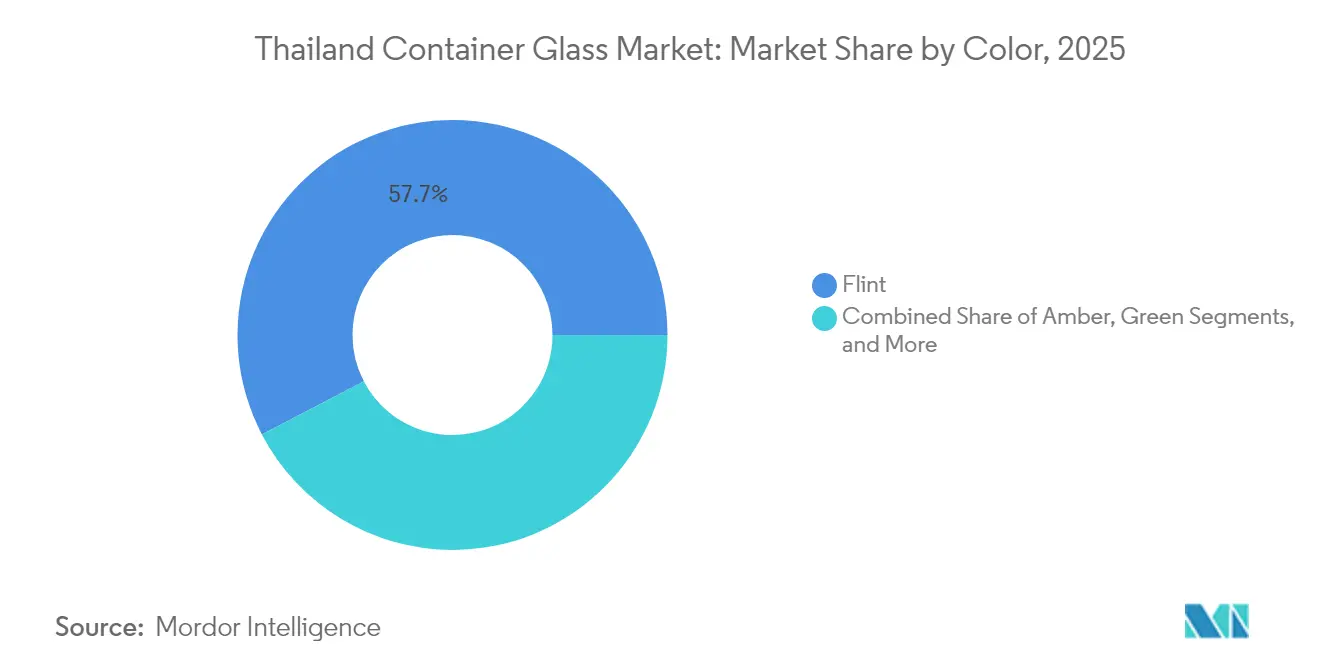

- By color, the Thailand container glass market size for the amber glass segment is projected to grow at 4.92% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for sustainable and recyclable packaging | +1.2% | National - industrial provinces and Bangkok | Medium term (2-4 years) |

| Premiumization in beverage and cosmetics packaging | +0.8% | National - urban centers | Long term (≥ 4 years) |

| Domestic craft-beer and alcoholic consumption uptrend | +0.6% | Tourism zones | Short term (≤ 2 years) |

| Mandatory recycled-content targets in government procurement | +0.4% | National | Medium term (2-4 years) |

| Cannabis beverages driving demand for UV-protective glass | +0.3% | Bangkok metro | Short term (≤ 2 years) |

| Scrap-surcharge rebates for ≥ 60% cullet usage | +0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Sustainable and Recyclable Packaging

Thailand’s plastic-waste roadmap eliminates single-use foam food boxes and thin plastic cups by 2025, creating structural substitution toward glass containers. Enforcement extends to microbead bans in cosmetics since 2020 and retailer-led plastic-bag phase-downs, anchoring consumer perception of glass as the low-carbon default. The carbon tax amplifies cost differentials between plastics and glass when lifecycle footprints are considered, encouraging brand owners to specify recycled-content glass. Leading energy conglomerate PTT has already committed to circular waste management targets, reinforcing supply-chain alignment around recyclable packaging. As policy milestones approach, demand visibility rises for producers able to guarantee high-cullet, low-emission output. The combined regulatory environment therefore adds 1.2 percentage points to the forecast CAGR of the Thailand container glass market.

Premiumization in Beverage and Cosmetics Packaging

Brands leverage glass aesthetics to justify higher price points in craft beer, functional drinks, and prestige beauty lines, where packaging communicates authenticity and sustainability. Early success stories in ready-to-drink green tea, whose value expanded from USD 10 million in 2001 to USD 150 million by 2004, underscore consumers’ willingness to trade up when packaging aligns with perceived quality.[2]USDA Foreign Agricultural Service, “Non-Alcoholic Beverage Report Bangkok Thailand,” FAS.usda.gov Social-media imagery further rewards clear, glossy glass surfaces, elevating shelf appeal and driving repeat purchases among eco-conscious millennials. Domestic cosmetic companies translate these cues into product launches that feature thick-wall flint jars and droppers, sustaining a premiumization flywheel that adds 0.8 percentage points to market growth.

Domestic Craft-Beer and Alcoholic Consumption Uptrend

Local breweries experiment with bespoke amber bottles that protect hop volatiles from UV damage, while spirits distillers prefer flint shapes that showcase coloration and purity. The hospitality rebound, fueled by a return of foreign visitors to Bangkok, Phuket, and Chiang Mai, lifts on-premise glass bottle consumption. Sugar-tax reformulations toward premium, lower-sugar beverages further support glass uptake as brands position themselves away from mass-market PET. Aggregate demand from craft beer and premium spirits therefore adds 0.6 percentage points to the Thailand container glass market CAGR.

Cannabis Beverages Driving Demand for UV-Protective Glass

Thailand’s progressive cannabis legislation creates a nascent drink category requiring amber bottles that block UV wavelengths detrimental to cannabinoid stability. Early entrants target niche consumers in Bangkok, but distribution is widening into mainstream retail as product awareness grows. Regulatory discussions on child-resistant closures and accurate THC labeling also favor established glass suppliers, who can integrate compliant features at scale. Though volumes remain low, margins are high, supporting incremental growth of 0.3 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid penetration of PET and aluminum cans | -1.1% | National - mass-market beverage segments | Long term (≥ 4 years) |

| High furnace energy costs and fuel-switching CAPEX | -0.9% | Major production hubs | Medium term (2-4 years) |

| Stricter 2023 NOx caps delaying furnace rebuilds | -0.5% | All facilities | Short term (≤ 2 years) |

| Fragmented rural cullet-collection logistics | -0.3% | Rural provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Penetration of PET and Aluminum Cans

Lightweight PET and aluminum offer cost and logistics advantages in low-margin beverage segments, squeezing glass volumes in convenience channels. Indorama Ventures’ downstream PET integration improves supply economics, enabling aggressive pricing into mass-market soft drinks.[3]Indorama Ventures Public Company Limited, “Indorama Ventures Evolves its Business Strategy,” Indoramaventures.com C-store operators favor lighter packs to optimize shelf replenishment, dulling glass demand in price-sensitive categories and shaving 1.1 percentage points off market CAGR.

High Furnace Energy Costs and Fuel-Switching CAPEX

Electricity tariffs could rise up to 44%, while natural gas volatility drives furnace operating costs that comprise up to one-fourth of total production spend. Generating efficiency gains demands expensive oxy-fuel modifications or alternative-fuel retrofits that many smaller players cannot finance quickly. These energy headwinds therefore trim 0.9 percentage points from the Thailand container glass market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Extend Leadership Amid Tourism Recovery

Beverages accounted for 53.78% of Thailand container glass market share in 2025, outpacing all other uses by leveraging the tourism rebound and a shift toward premium craft formulations. Within this base, beer maintains volume leadership, but premium spirits and functional drinks now contribute the highest value growth, supported by differentiated bottle shapes, embossing, and tamper-evident closures. The Thailand container glass market size attached to beverages is projected to expand steadily as hospitality footfall returns to pre-pandemic norms.

Growing brand focus on sustainability integrates 30-65% recycled cullet into bottles, reinforcing circular economy positioning while reducing furnace energy intensity. In parallel, non-alcoholic segments such as kombucha and cold-brew coffee migrate to glass to emphasize authenticity and clean-label credentials. The cosmetics and personal care category though smaller today will post a 5.01% CAGR to 2031, reflecting consumer preference for premium glass jars, droppers, and rollers that convey efficacy and eco-consciousness. High-end skincare brands already advertise their bottles as 100% recyclable, reinforcing adoption momentum among domestic shoppers seeking responsible luxury.

By Color: Flint Retains Versatility While Amber Climbs

Flint glass captured 57.65% share of the Thailand container glass market size in 2025 thanks to its clarity and broad compatibility across food, pharmaceutical, and beauty applications. The segment’s dominance stems from visibility advantages that allow consumers to inspect product integrity, particularly in nutritionals and fragrance. Producers achieve flint cullet ratios of roughly 60%, balancing transparency with recycled content requirements.

Amber glass, however, registers a 4.92% CAGR and is set to claim additional share as craft beer, cannabis beverages, and essential-oil formulations favor UV protection. Leading furnaces have optimized colorants to accept up to 70% amber cullet, closing the cost gap with flint offerings while advancing sustainability goals. Although green and specialty hues remain niche, demand persists in imported wine and premium spirit lines where brand equity hinges on distinctive color cues.

Geography Analysis

Thailand container glass market demand clusters around Bangkok, Chonburi, and Rayong, where beverage bottlers, pharmaceutical plants, and distribution hubs concentrate. The Eastern Economic Corridor’s upgraded road and port networks compress lead times between Map Ta Phut furnaces and high-volume customers, lifting supply reliability during peak tourist seasons. Bangkok’s affluent districts and duty-free outlets absorb the lion’s share of premium spirits and prestige cosmetics packaged in flint glass, while beach destinations such as Phuket fuel cyclical spikes in beer bottle orders.

In northern hubs like Chiang Mai, craft breweries and farm-to-table restaurants anchor boutique demand for custom amber bottles. Rural provinces remain underserved by organized cullet collection, prompting government-backed buyback schemes and color-sorted drop-off points to boost recycling rates. Import flows of specialty bottles rarely exceed niche perfume or pharmaceutical formats, given freight-weight penalties and sufficient local capacity.

The baht’s depreciation in 2024 eased export selling prices, enabling select producers to ship small volumes of beverage bottles to neighboring CLMV (Cambodia, Laos, Myanmar, Vietnam) markets; nonetheless, Thailand container glass market activity remains overwhelmingly domestic. As the carbon tax structure harmonizes with ASEAN partners, regional export competitiveness could improve, but near-term growth still rests on Thailand’s own tourism and premiumization drivers.

Competitive Landscape

Moderate concentration typifies the Thailand container glass market, where furnace investments run into tens of USD millions, deterring greenfield entrants. Siam Glass Industry and Thai Malaya Glass operate multicombustion furnaces near Bangkok and Eastern Seaboard petrochemical clusters, supplying more than half of national volumes. Berli Jucker leverages its consumer goods and retail arms to lock in downstream demand, while its joint venture with O-I Glass injects global design know-how and high-speed forming technologies.

Multinationals prefer partnering over standalone facilities; O-I’s acquisition of Berli Jucker’s Malaya Glass assets created scale synergies across Southeast Asia and raised cullet utilization benchmarks to 80% in select colors. Technology differentiation now centers on furnace oxy-fuel retrofits and predictive maintenance to temper refractory wear, extending campaign life beyond the 12-year norm. Smaller regional plants grapple with CAPEX hurdles, accelerating consolidation as larger players acquire permits and cullet networks in pursuit of efficiency gains.

White-space opportunities emerge in cannabis beverage packaging, where producers require certified child-resistant closures and UV-protective amber bottles at lower minimum order quantities than mainstream beer lines. Thai Glass Industries and select specialty converters are moving into molded glass droppers and roll-on applicators for high-growth serum and essential oil categories, capturing value where precision dosing and aesthetic appeal command price premiums. Collective strategic moves indicate a market trending toward high-margin niches rather than sheer volume plays.

Thailand Container Glass Industry Leaders

Thai Glass Industries Public Company Limited

Wellgrow Glass Industry Co., Ltd.

Berli Jucker Public Company Limited (BJC Packaging)

Ocean Glass Public Company Limited

O-I Glass, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sirio Pharma confirmed a USD 40 million nutraceutical facility in Chonburi, signaling incremental demand for pharmaceutical-grade glass.

- July 2024: SCG posted first-half 2024 growth and reiterated investments in packaging verticals to capture sustainability tailwinds.

- June 2024: Thailand Board of Investment cleared a THB 19.3 billion (USD 0.54 billion) bio-ethylene project by Braskem Siam, foreshadowing competition from bio-PET in premium beverage applications.

- May 2024: O-I Glass launched a USD 650 million global cost-reduction roadmap through 2027, including Southeast Asian footprint optimization.

Thailand Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

The Thailand Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments..

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Thailand container glass market in 2026?

It totals 4.12 million tonnes in 2026 and is forecast to reach 5.09 million tonnes by 2031 at a 4.30% CAGR.

Which end-user category leads demand?

Beverages command 53.78% of national volume, buoyed by tourism recovery and craft beer growth.

Why is amber glass growing faster than other colors?

Cannabis beverages and craft beers require UV protection, pushing amber glass to a 4.92% CAGR through 2031.

What policy actions favor glass over plastic?

Thailand’s plastic-waste phase-out by 2027, carbon tax of THB 200 per tonne CO₂, and cullet incentives above 60% collectively strengthen glass competitiveness.

How does rising energy cost affect producers?

Electricity and gas volatility raises furnace expenses, pressuring margins for smaller plants and encouraging consolidation among larger, more efficient players.

Page last updated on: