Global Actinic Keratosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

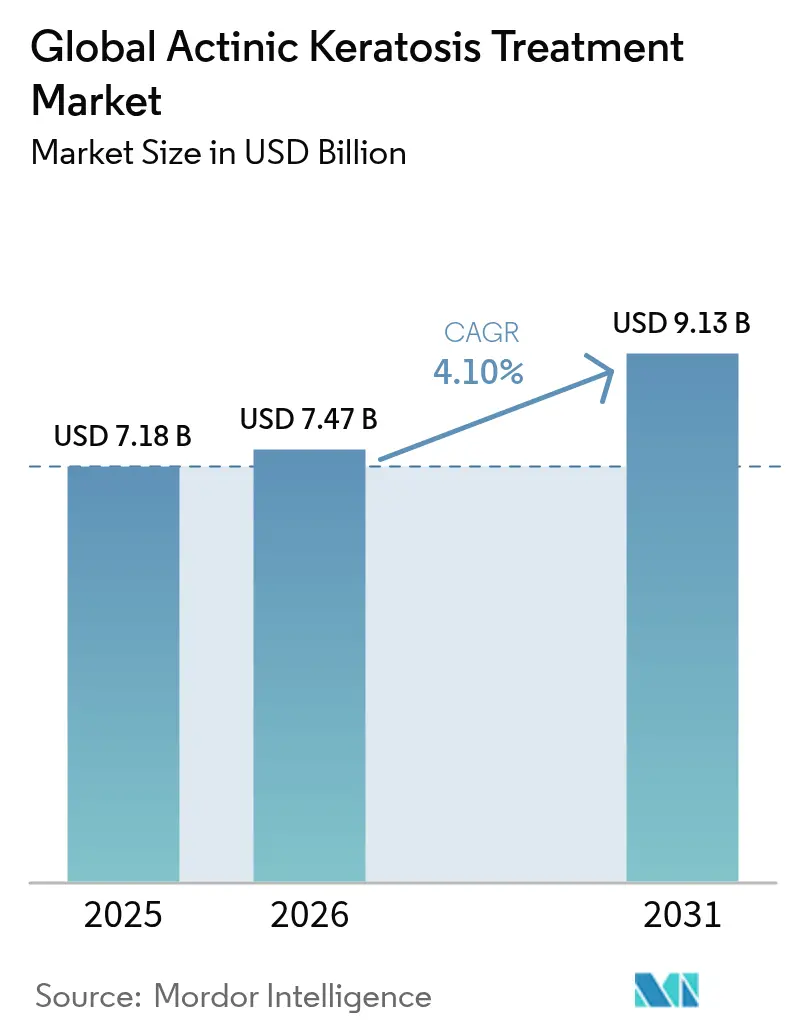

| Market Size (2026) | USD 7.47 Billion |

| Market Size (2031) | USD 9.13 Billion |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Actinic Keratosis Treatment Market Analysis by Mordor Intelligence

The actinic keratosis treatment market size is expected to grow from USD 7.18 billion in 2025 to USD 7.47 billion in 2026 and is forecast to reach USD 9.13 billion by 2031 at 4.10% CAGR over 2026-2031. This growth reflects rising lesion prevalence among aging, fair-skinned populations, rapid procedural innovation, and improving reimbursement clarity in major economies. North America retains leadership thanks to comprehensive insurance coverage and strong clinical research ecosystems, while Asia-Pacific, led by Japan and Australia, is expanding fastest on the back of demographic aging and wider dermatology access. Competitive rivalry remains moderate as established companies acquire pipeline assets and refine drug-device combinations, whereas smaller entrants emphasize daylight photodynamic therapy and AI-guided diagnosis. Procedural advances such as fractional laser systems and daylight-mediated PDT are accelerating physician adoption, even as topical therapies continue to dominate first-line care. Digital pharmacies, buoyed by pandemic-driven telehealth use, are reshaping distribution dynamics, while younger patient cohorts seek earlier, preventive intervention—signaling a gradual shift in treatment paradigms.

Key Report Takeaways

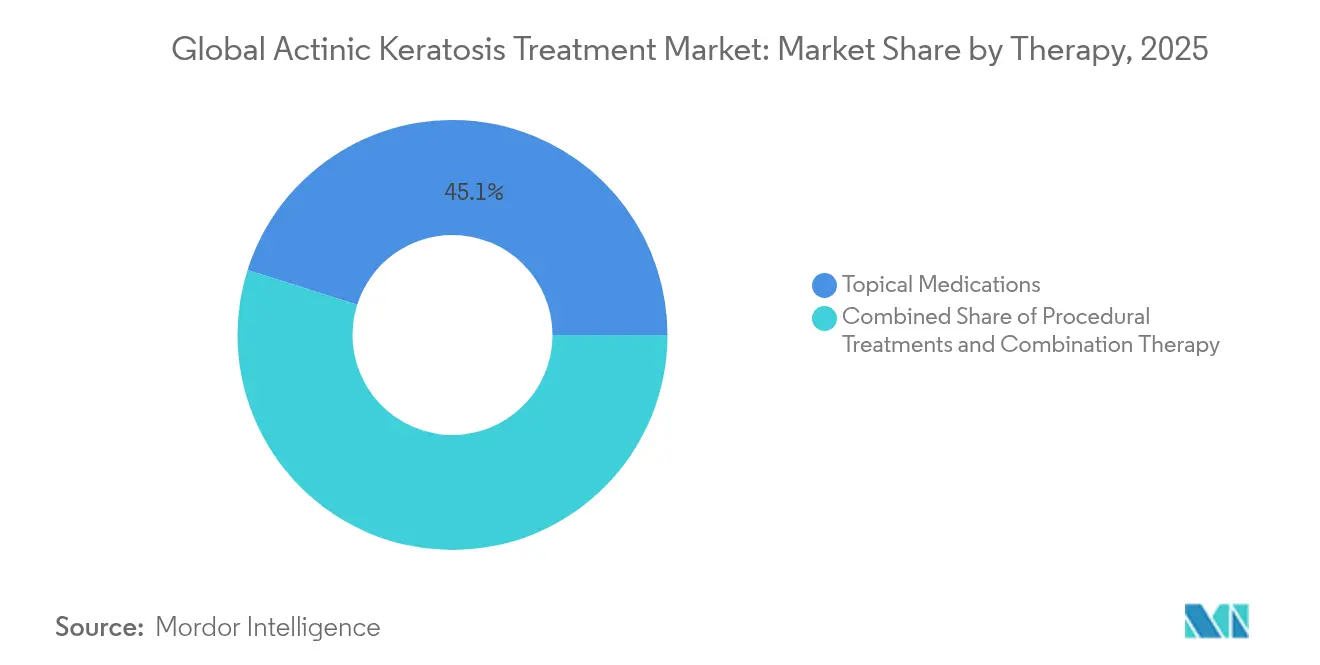

- By therapy, topical medications led with 45.12% of actinic keratosis treatment market share in 2025, while procedural treatments are projected to expand at a 5.12% CAGR through 2031.

- By end user, hospitals and oncology centers held 53.55% share of the actinic keratosis treatment market size in 2025, whereas home-care settings register the highest 4.73% CAGR to 2031.

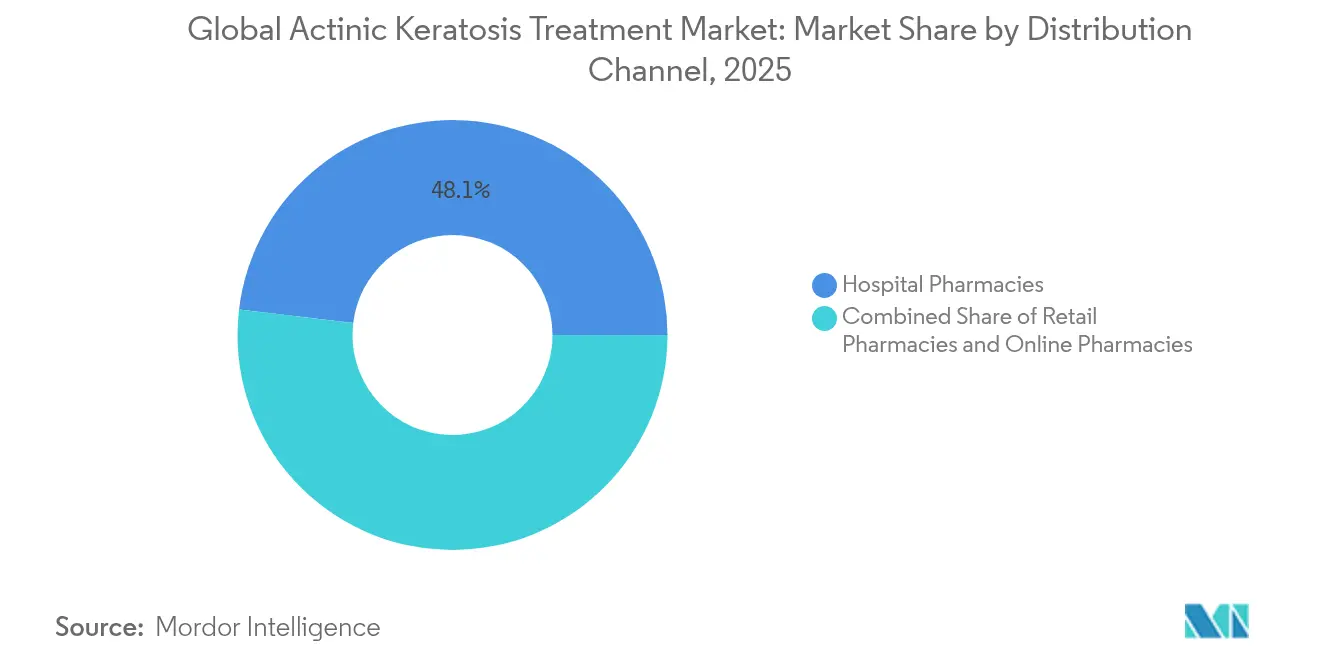

- By distribution channel, hospital pharmacies commanded 48.10% of the actinic keratosis treatment market in 2025; online pharmacies lead growth at a 5.06% CAGR through 2031.

- By patient age group, individuals older than 60 years captured 67.20% of the actinic keratosis treatment market in 2025, while the under-40 demographic is advancing at a 5.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Actinic Keratosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence among aging, fair-skinned populations | +1.2% | Global, high in North America & Australia | Long term (≥ 4 years) |

| Growing demand for minimally-invasive dermatologic procedures | +0.8% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Expansion of reimbursement coverage for AK therapies in OECD markets | +0.6% | US & Germany lead | Short term (≤ 2 years) |

| Adoption of daylight-PDT protocols reducing chair-time & cost | +0.5% | Europe & North America | Medium term (2-4 years) |

| Regulatory approvals of novel agents boosting physician uptake | +0.3% | US & EU frameworks | Short term (≤ 2 years) |

| AI-enabled dermoscopy driving earlier diagnosis | +0.2% | North America & APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Actinic Keratosis Among Aging, Fair-Skinned Populations

Prevalence rates range from 11% to 25% in northern latitudes and reach 60% among Australian adults, underscoring a large and rising patient pool. Spain’s clinic data show 28.6% overall prevalence, with men disproportionately affected, which shapes therapy demand. Improved public screening and longer life expectancy push more lesions into clinical settings, while each lesion signals elevated squamous cell carcinoma risk—with malignant transformation estimated at 8% in immunocompetent patients. Payers view early treatment as cost-avoiding, supporting broader coverage for both topical and procedural care. Collectively these dynamics create durable demand across every major geography.

Growing Demand for Minimally-Invasive Dermatologic Procedures

Patient preference is shifting toward approaches that offer high clearance and minimal downtime. Photodynamic therapy achieves 85%–90% clearance after one or two sessions and outperforms cryotherapy on cosmetic outcome. Daylight protocols lower pain scores and cut clinic occupancy, making the modality more acceptable to pain-averse patients. Fractional laser platforms such as the dual-wavelength Fraxel FTX deliver targeted ablation with faster recovery, driving procedural uptake. AI screening tools that hit 87% sensitivity accelerate early diagnosis, enabling doctors to select minimally invasive options sooner. Together these advances propel the procedural segment’s rapid growth.

Expansion of Reimbursement Coverage for AK Therapies in OECD Markets

Payers increasingly cover photodynamic therapy and established topicals, seeing them as preventive strategies that curb downstream oncology costs. Major U.S. insurers now reimburse ALA-PDT on multiple body sites, widening patient eligibility [1]Medica Policy Team, “Light Treatment and Laser Therapies for Benign Dermatologic Conditions,” medica.com. The FDA recently allowed use of up to three tubes of Ameluz per session, reflecting regulatory flexibility and paving the way for shorter, more effective regimens. Europe’s guideline bodies echo this stance, recommending PDT as first-line therapy. Sustained reimbursement support reduces patient out-of-pocket exposure and improves adherence across high-income markets.

Adoption of Daylight-PDT Protocols Reducing Chair-Time & Cost

Daylight-mediated photodynamic therapy delivers ≥70% lesion response and limits the intense pain reported with LED-based systems. Patients complete light activation outdoors, freeing clinic rooms and boosting provider throughput. Practices report shorter waitlists and improved resource utilization. Cost advantages span reduced capital equipment, lower staffing needs, and higher daily patient volumes. Broader availability of field-directed daylight kits is poised to make PDT feasible even in smaller urban and rural clinics, widening access.

Regulatory Approvals of Novel Agents Boosting Physician Uptake

The FDA and EMA continue to fast-track topicals and device-drug combinations that demonstrate strong safety benefits. Expanded-area approval for tirbanibulin up to 100 cm² quadruples eligible surface area per treatment cycle and simplifies field therapy for multifocal lesions. Similar label extensions for Ameluz and emerging 5-FU plus calcipotriene regimens illustrate a regulatory tilt toward convenience. Positive verdicts encourage prescribers to transition patients away from legacy cryotherapy toward evidence-backed pharmacologic or PDT options.

AI-Enabled Dermoscopy Driving Earlier Diagnosis & Treatment Volumes

Deep-learning models now outperform general dermatologists on several lesion-classification tasks, with 77% specificity recorded in meta-analysis. Earlier identification of thin or subclinical lesions increases the total addressable treatment volume. Commercial tele-dermoscopy platforms integrate AI triage to flag suspicious keratoses before in-person visits, streamlining referrals and reducing specialty bottlenecks. Providers benefit through higher procedural throughput, while patients access treatment sooner under less invasive protocols.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event profile of existing topicals limits patient compliance | –0.7% | Global, more severe in emerging markets | Short term (≤ 2 years) |

| High out-of-pocket costs in emerging economies | –0.4% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Withdrawal of ingenol mebutate eroding clinician confidence | –0.3% | Europe & North America | Medium term (2-4 years) |

| Margin pressure from European bundled-payment pilots | –0.2% | Europe, possible OECD spread | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Profile of Existing Topicals Limits Patient Compliance

Local reactions such as erythema, pain, and crusting cause many patients to discontinue 5-fluorouracil prematurely, hampering clearance outcomes. Ingenol mebutate’s 2020 market exit after safety alarms magnified prescriber caution about newer molecules. Field-directed regimens often require covering large facial or scalp regions, creating visible inflammation that deters cosmetically sensitive patients. Ongoing studies exploring 5-FU–calcipotriene combinations aim to shorten treatment to four days while preserving high efficacy. Until tolerability improves, some patients will defer or refuse needed therapy.

High Out-of-Pocket Costs in Emerging Economies

Procedural sessions and biologics can exceed USD 100,000 annually, placing therapy beyond reach for self-pay patients in low-insurance markets [2]Craig G. Burkhart, “Financial Toxicity of Biologics and JAK Inhibitors in the United States,” opendermatologyjournal.com. Scarcity of specialists compounds cost hurdles: Ghana counts only 25 dermatologists for 25 million residents, pushing untreated lesions into advanced stages. While digital pharmacies promise cheaper generics, logistical limitations and payment barriers slow adoption. Price sensitivity will therefore cap penetration of premium therapies in many emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy: Procedural Treatments Gain Ground Despite Topical Dominance

Topical medications held 45.12% of actinic keratosis treatment market share in 2025 as 5-fluorouracil, imiquimod, and newer tirbanibulin remain first-line for field therapy . Tirbanibulin’s label expansion to 100 cm² positions it for wider facial and scalp application, reinforcing topical leadership. Nonetheless, the procedural category is on a 5.12% CAGR trajectory, and its share of the actinic keratosis treatment market size is forecast to rise steadily toward 2031. Daylight-mediated PDT, fractional CO₂ lasers, and laser-assisted drug delivery are broadening the armamentarium, offering cosmetic advantages and shorter healing windows.

Procedural uptake varies by geography and reimbursement, yet clinical evidence continues to favor PDT over repeat topical courses for multi-lesion fields. Hospitals, dermatology clinics, and even ambulatory centers are investing in RhodoLED XL and similar platforms following recent FDA clearance. Cryotherapy, still widely used for isolated lesions, now competes with laser resurfacing that can remove diffuse ultraviolet damage in a single visit. As protocols mature, procedural treatments are expected to further dilute topical dominance, especially in markets where payers reward long-term clearance.

By End User: Hospitals Sustain Volume While Home-Care Models Expand

Hospitals and oncology centers accounted for 53.55% of actinic keratosis treatment market revenue in 2025, reflecting concentrated expertise and equipment-intensive procedures. Comprehensive reimbursement support and academic trial activity solidify their role in managing advanced or high-risk lesions. These facilities deploy integrated EHR, imaging, and AI triage that streamline field treatment mapping and follow-up. Nevertheless, capacity constraints and high overhead spur providers to triage stable cases into outpatient and home settings.

Home-care settings, aided by nurse-led phototherapy programs and self-applied topicals, are the fastest-growing channel at a 4.73% CAGR. Pilot programs demonstrate safe self-administration of narrow-band phototherapy and daylight-based PDT under virtual supervision, trimming transport and waiting costs. Teledermatology follow-up and app-based adherence reminders are critical enablers. As payers reimburse remote monitoring codes, home-care uptake is expected to accelerate, especially for maintenance and field therapies that do not require specialized devices.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies remained primary dispensers with 48.10% of actinic keratosis treatment market sales in 2025, driven by integrated specialty care and biologic handling requirements. Close coordination with oncology and dermatology teams ensures timely procurement of photosensitizers and investigational agents. However, online pharmacies are expanding at 5.06% CAGR as consumers embrace e-prescriptions and doorstep delivery. The global digital pharmacy market is on course for USD 35.33 billion by 2026, underpinned by AI order routing, blockchain verification, and adherence analytics.

Retail chains deploy in-store clinics and telehealth pods to remain relevant, but regulatory shifts such as FDA’s DSCSA interoperability rules favor digitally native players. As topical demand rises in younger cohorts, convenient refill mechanisms sway share toward online channels. Hospitals will defend their position by embedding e-dispensing portals and specialty medication counseling, yet expect continued share leakage to virtual providers through 2031.

By Patient Age Group: Prevention Moves Attention to Younger Cohorts

Individuals older than 60 years control 67.20% of actinic keratosis treatment market spending, reflecting accumulated ultraviolet damage and multi-lesion burden. Management complexity increases with comorbidities, often requiring gentler regimens such as daylight-PDT or low-dose 5-FU. Payers and clinicians therefore prioritize tolerability and adherence tools for this segment.

The under-40 group advances at 5.29% CAGR, signaling earlier lifestyle-driven prevention. AI-dermoscopy kiosks in primary-care offices detect precancerous lesions sooner, funneling patients to quick-recovery procedures like laser resurfacing. Brand-driven social media campaigns by manufacturers of field sunscreens and cosmetic-oriented topicals further heighten risk awareness. Over time, proactive treatment in younger adults is projected to flatten future invasive skin cancer incidence, altering long-term demand distribution.

Geography Analysis

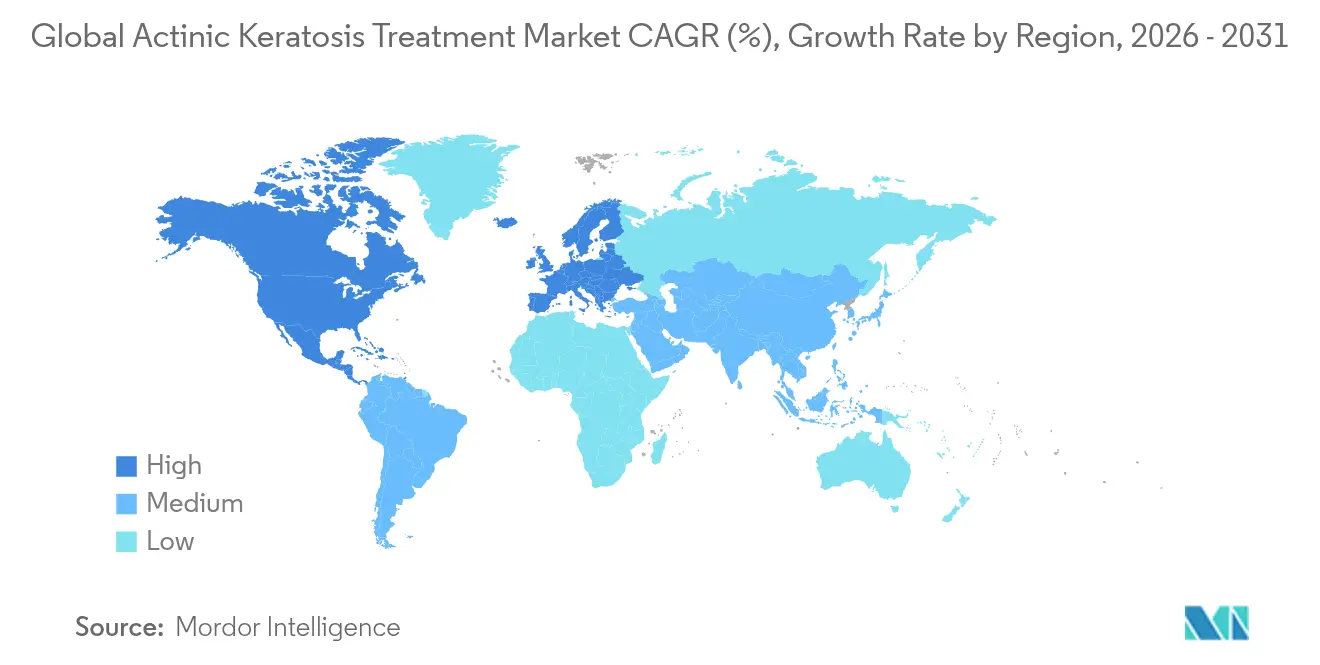

North America held 41.70% of the actinic keratosis treatment market in 2025, supported by insurance coverage that reimburses multiple AK therapies, advanced research infrastructure, and rapid uptake of AI diagnostic platforms. Academic centers in the United States spearhead trials for laser-assisted drug delivery and combination topicals, reinforcing regional technology leadership. Canada mirrors these trends through universal healthcare and robust dermatologist density. Ongoing consolidation may enhance purchasing power and accelerate technology roll-outs.

Asia-Pacific, expanding at 6.08% CAGR, benefits from demographic aging and growing middle-class health spending, yet faces specialist shortages in emerging economies. Japan illustrates the aging burden, with 74% of skin cancer patients now over 70 years. Australia sets procedural adoption benchmarks, especially for daylight-PDT. China and India witness double-digit growth in teledermatology startups, though uneven reimbursement and limited dermatologist distribution restrain full-market potential. Regional AI algorithm developers work to recalibrate models for darker skin phototypes, which differ from Western training datasets.

Europe remains a mature yet innovative arena. National health services endorse daylight-PDT, and bundled-payment pilots in Germany and the Nordics test cost-containment for dermatology episodes. The EMA’s decisive removal of ingenol mebutate underscores stringent safety oversight. Providers adjust formularies toward safer, evidence-heavy agents and invest in multi-wavelength laser workstations. Southern European countries, with higher UV indexes, allocate public funding to seasonal skin-cancer screening campaigns that feed procedure volumes during peak summer months.

Competitive Landscape

Market fragmentation is moderate; the top five companies collectively control an estimated 48% of worldwide actinic keratosis treatment market revenue. LEO Pharma intensified acquisition activity, purchasing Timber Pharmaceuticals for USD 36 million and licensing a Boehringer compound for EUR 90 million, strengthening its early-stage dermatology pipeline. Sun Pharma’s USD 347 million buyout of Taro and USD 355 million deal for Checkpoint Therapeutics adds UNLOXCYT to its onco-dermatology portfolio, signaling appetite for differentiated topical and systemic assets.

Technology acts as a key differentiator. Biofrontera’s RhodoLED XL lamp with five panels offers optimized light distribution and positioning sensors, underpinning 2024 revenue of USD 37.3 million and FDA-approved expanded Ameluz use. Bausch Health’s launch of Fraxel FTX with dual wavelengths enhances precision resurfacing, appealing to both therapeutic and cosmetic segments. Galderma recorded record quarterly net sales of USD 1.129 billion as its prescription and consumer units leveraged cross-channel marketing.

Strategic partnerships extend reach. Biofrontera allied with LEO Pharma to co-promote Advantan and Skinoren in Germany, exploiting Biofrontera’s dermatology sales force. Organon’s planned acquisition of Dermavant and its VTAMA cream diversifies its women’s-health portfolio into high-growth dermatology segments. Pipeline intensity remains high, with multiple Phase III trials assessing next-generation photosensitizers, laser-activated drug particles, and topical-systemic combination regimens poised to expand therapeutic choice.

Global Actinic Keratosis Treatment Industry Leaders

-

Sun Pharmaceutical Industries Limited

-

Biofrontera AG

-

Bausch Health Companies Inc.

-

LEO Pharma A/S

-

Almirall, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Tirbanibulin ointment 1% demonstrated efficacy in 100 cm² treatment fields; FDA approved sNDA expanding label coverage.

- August 2024: Biofrontera partnered with LEO Pharma to co-promote Advantan and Skinoren across Germany, leveraging Biofrontera’s specialty sales capabilities.

- June 2024: Almirall launched Klisyri in Europe, offering 5-day tirbanibulin therapy for multiple facial and scalp lesions.

Global Actinic Keratosis Treatment Market Report Scope

As per the scope of the report, actinic keratosis is a rough, scaly patch on skin that develops from years of exposure to solar radiation. It is commonly found on the face, lips, ears, back of hands, forearms, scalp, or neck.

The Actinic Keratosis Treatment Market is Segmented By Therapy Type (Topical Medications (Fluorouracil, Imiquimod, Ingenol Mebutate, and Other Medications), and Procedures (Photodynamic Therapy, Laser, and Other Procedures)), End User (Hospitals and Oncology Centers, Dermatology Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the market size and forecasts in value (USD million) for the above segments.

| Topical Medications | 5-Fluorouracil |

| Imiquimod | |

| Tirbanibulin | |

| Diclofenac | |

| Ingenol Mebutate | |

| Other Topicals | |

| Procedural Treatments | Cryotherapy |

| Photodynamic Therapy | |

| Laser Resurfacing | |

| Chemical Peels | |

| Curettage & Electrodessication | |

| Other Procedures | |

| Combination / Sequential Therapy |

| Hospitals & Oncology Centers |

| Dermatology Clinics |

| Ambulatory Surgical Centers |

| Home-care Settings |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| < 40 Years |

| 40 – 60 Years |

| > 60 Years |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy | Topical Medications | 5-Fluorouracil |

| Imiquimod | ||

| Tirbanibulin | ||

| Diclofenac | ||

| Ingenol Mebutate | ||

| Other Topicals | ||

| Procedural Treatments | Cryotherapy | |

| Photodynamic Therapy | ||

| Laser Resurfacing | ||

| Chemical Peels | ||

| Curettage & Electrodessication | ||

| Other Procedures | ||

| Combination / Sequential Therapy | ||

| By End User | Hospitals & Oncology Centers | |

| Dermatology Clinics | ||

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Patient Age Group | < 40 Years | |

| 40 – 60 Years | ||

| > 60 Years | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the actinic keratosis treatment market by 2031?

Forecasts place the sector at USD 9.13 billion by 2031, reflecting a 4.10% CAGR from 2026.

Who are the key players in Global Actinic Keratosis Treatment Market?

Sun Pharmaceutical Industries Limited, Biofrontera AG, Bausch Health Companies Inc., LEO Pharma A/S and Almirall, S.A. are the major companies operating in the Global Actinic Keratosis Treatment Market.

Which therapy category is growing fastest?

Procedural treatments such as daylight-mediated photodynamic therapy and fractional lasers are projected to grow at 5.12% CAGR through 2031.

Which region has the biggest share in Global Actinic Keratosis Treatment Market?

In 2025, the North America accounts for the largest market share in Global Actinic Keratosis Treatment Market.

Why are online pharmacies gaining traction?

Convenience, telehealth integration, and lower transaction costs are pushing online pharmacy sales forward at 5.06% CAGR.

Page last updated on: