Amino Acid Assay Kit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.30 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

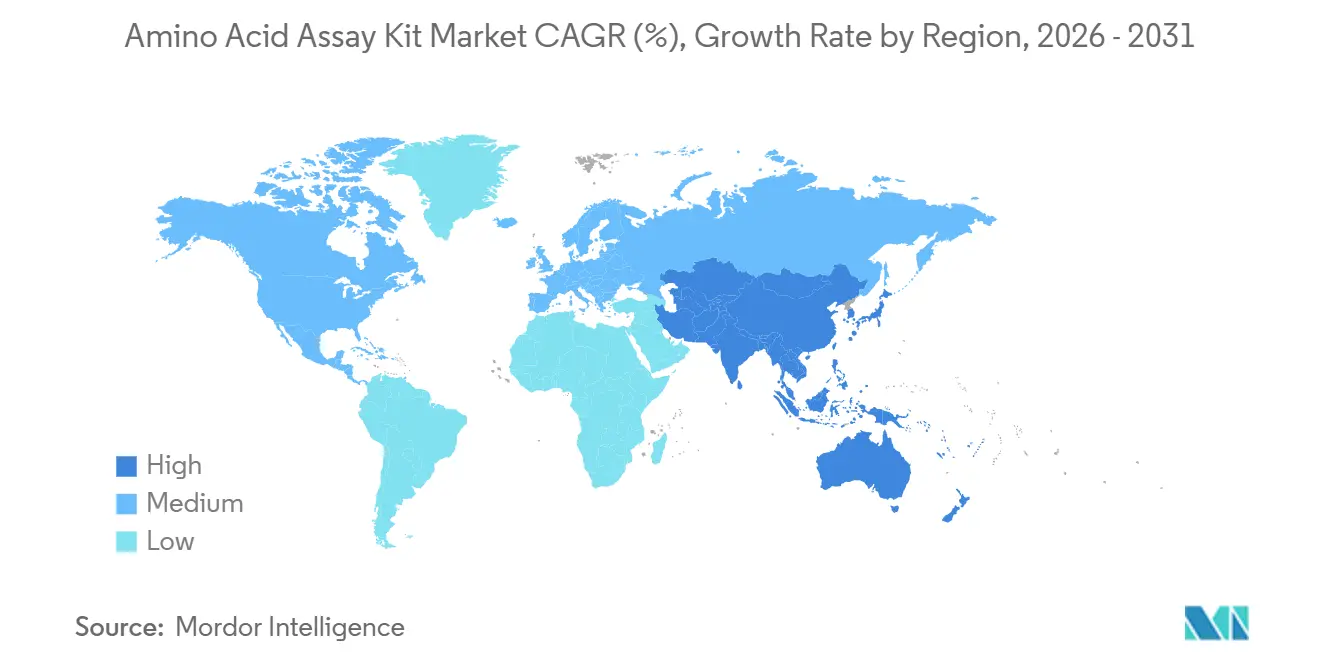

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

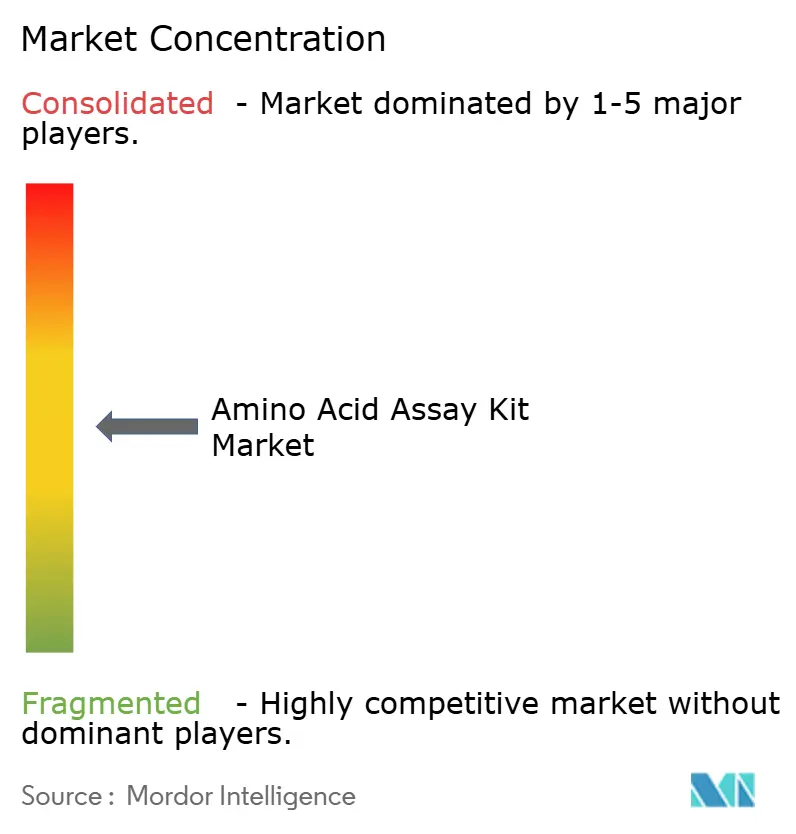

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Amino Acid Assay Kit Market Analysis by Mordor Intelligence

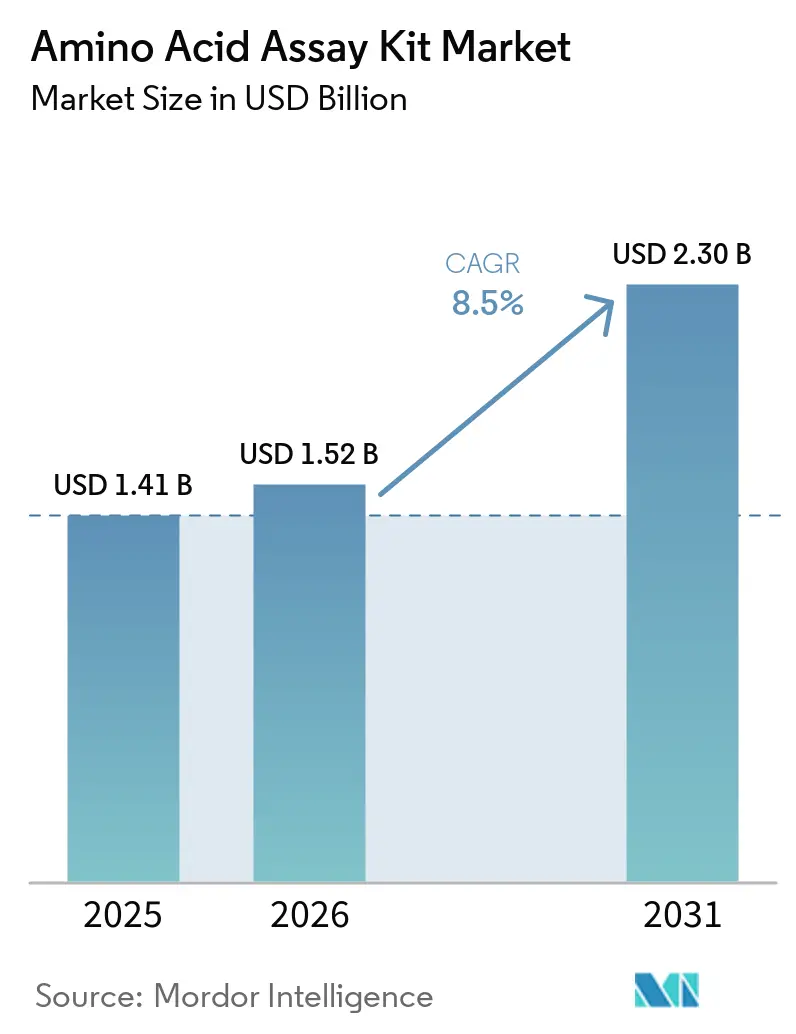

The Amino Acid Assay Kit Market size is projected to be USD 1.41 billion in 2025, USD 1.52 billion in 2026, and reach USD 2.30 billion by 2031, growing at a CAGR of 8.5% from 2026 to 2031.

Demand in the amino acid assay kit market is driven by three key factors: the growing use of proteomics in drug discovery, stricter amino acid-based protein quality standards in food and beverage production, and increased clinical applications in metabolic disorder diagnostics, particularly in newborn screenings. These kits are evolving into core analytical tools, closely integrated with automated, high-throughput LC-MS workflows in pharmaceutical, biotechnology, and clinical settings. Major suppliers dominate by bundling kits with proprietary instruments, increasing switching costs for institutional buyers and providing a competitive edge to integrated platforms. Simultaneously, the market is creating opportunities for cost-effective suppliers, especially in colorimetric and enzymatic formats, as price sensitivity rises in developing laboratory systems.

Key Report Takeaways

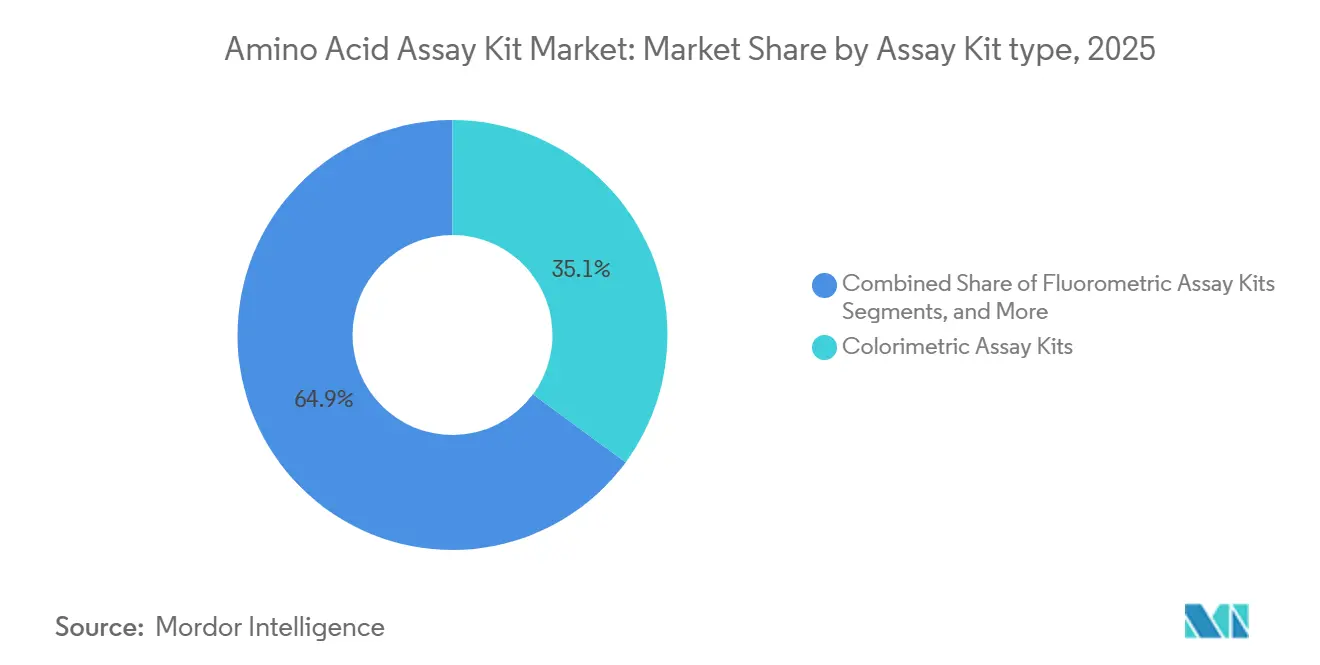

- By assay kit type, colorimetric assay kits held 35.13% of the amino acid assay kit market share in 2025, while fluorometric assay kits are projected to expand at a 10.25% CAGR through 2031.

- By application, protein quantification accounted for 28.45% of the amino acid assay kit market size in 2025, while amino acid profiling is forecast to grow at a 9.55% CAGR through 2031.

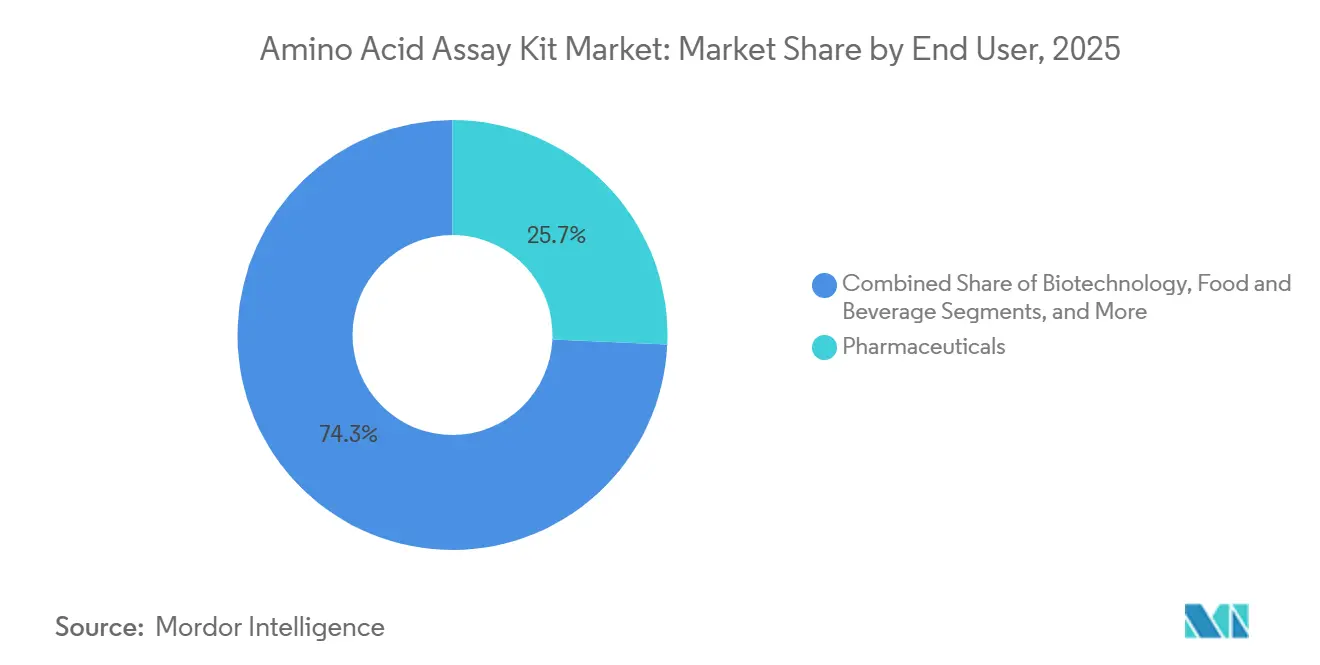

- By end user, pharmaceuticals accounted for 25.66% share in 2025, while diagnostic centers are expected to record the highest CAGR at 11.88% through 2031.

- By geography, North America held 39.56% of the amino acid assay kit market share in 2025, while Asia-Pacific is projected to expand at a 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Amino Acid Assay Kit Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising need for quantitative amino acid research in metabolomics and clinical studies | +2.1% | Global | Medium term (2-4 years) |

| Expanding proteomics and biomarker discovery programmes | +1.6% | North America & EU | Medium term (2-4 years) |

| Food authentication and protein label verification requirements | +1.2% | North America, EU & Asia-Pacific | Short term (≤ 2 years) |

| Point-of-care and low-volume workflow protocols in decentralized settings | +0.9% | Global, with early gains in Asia-Pacific & MEA | Long term (≥ 4 years) |

| Higher adoption of multiplex and high-throughput screening platforms | +0.8% | North America & EU, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Regulatory and quality-control push for standardization in amino acid testing | +0.6% | North America, EU & China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Quantitative Amino Acid Research Across Life Sciences

Metabolomics has transitioned from an exploratory tool to a critical component in pharmaceutical research, translational medicine, and disease screening, driving the amino acid assay kit market toward routine applications. Validated amino acid panels are now integral to workflows requiring repeatable and scalable testing. A 2025 study demonstrated that plasma amino acid concentration signatures detected four major cancer types with 78% sensitivity and a 0% false positive rate, achieving an AUROC of 0.95 in a validation cohort of 97 samples. The study's elimination of common sample pre-treatment steps enhances the feasibility of amino acid testing in frontline screening, creating opportunities in oncology testing programs and emphasizing the need for clinical-grade consistency in research and diagnostics.[1]Amado Torres, Marco, et al., “Immunodiagnostic Plasma Amino Acid Residue Biomarkers Detect Cancer Early and Predict Treatment Response,” Nature Communications, nature.com

Expanding Proteomics and Biomarker Discovery Programmes

Proteomics programs are increasingly incorporating amino acid quantification into drug discovery workflows, boosting demand in the amino acid assay kit market. Thermo Fisher Scientific’s acquisition of Olink in 2024 linked amino acid profiling to the UK Biobank Pharma Proteomics Project, which analyzes over 5,400 proteins from 600,000 samples for biomarker discovery. This expansion drives the need for calibration-grade quantification kits and supports growth in enzymatic and chromatographic formats, as consistent protein quantification remains essential before advanced analyses. The market benefits from both upstream standardization and downstream validation, supporting volume growth across workflows.

Food Authentication and Protein Label Verification Requirements

Protein label verification has become a key driver for the amino acid assay kit market as food manufacturers face stricter requirements for amino acid composition and digestibility claims. DIAAS reference values now cover over 400 foods, gaining recognition as a more accurate alternative to PDCAAS in regulatory settings.[2]Paul J. Moughan and Wen Xin Janice Lim, “Digestible Indispensable Amino Acid Score (DIAAS): 10 Years On,” Frontiers in Nutrition, frontiersin.org This is particularly relevant for plant-based protein suppliers, whose products often require repeated testing to meet label claims. Reformulation processes also contribute to recurring demand, establishing a consistent volume base for compliance-driven testing and ensuring the relevance of colorimetric and enzymatic kits alongside advanced methods.

Higher Adoption of Multiplex and High-Throughput Screening Platforms

Miniaturized workflows are addressing throughput challenges in the amino acid assay kit market, particularly in pharmaceutical and clinical settings. In 2026, Waters Advanced Diagnostics reported that its Kairos Amino Acid Kit quantified 42 amino acids in dried blood spot samples in under 10 minutes using UHPLC-MS/MS, with accuracy above 94.4% and imprecision below 2.6%. The kit’s availability in a high-throughput format for 500 samples highlights the growing importance of automation readiness, validated protocols, and seamless integration into pharmaceutical quality systems. Workflow efficiency has become a key purchasing factor, with formats compatible with 96-well and 384-well settings expected to capture significant demand.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Instrument-dependent performance and integration challenges with laboratory equipment | -1.3% | Global | Medium term (2-4 years) |

| Limited differentiation in commodity-tier colorimetric and enzymatic assay kits | -0.9% | Global, concentrated in Asia-Pacific & MEA | Short term (≤ 2 years) |

| Fragmented validation standards across end-user verticals and geographies | -0.7% | North America, EU & Asia-Pacific | Medium term (2-4 years) |

| Short shelf life and cold-chain dependence of sensitive reagents | -0.5% | MEA, South America & Asia-Pacific periphery | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Instrument-Dependent Performance and Integration Challenges

Instrument compatibility remains a significant limitation in the amino acid assay kit market, as many kits are optimized for specific fluorometric readers, ion-exchange analyzers, or LC-MS configurations. Laboratories with diverse instrument fleets face challenges in validating new kits on existing hardware, delaying adoption despite strong technical performance. The process requires substantial time and resources for method transfer, documentation, and staff training. Mid-tier institutions, with limited resources, are particularly affected, often favoring familiar, validated kits over superior alternatives. Suppliers offering integrated workflows across instruments and reagents hold a competitive edge by reducing implementation uncertainties.

Short Shelf Life and Cold-Chain Dependence

The amino acid assay kit market faces challenges with cold-chain handling, as sensitive components often require storage at -20°C and have limited usability after reconstitution. While mature laboratory networks manage these constraints effectively, emerging regions struggle with inconsistent transport conditions and storage stability. Decentralizing healthcare systems with growing testing demand but uneven infrastructure further complicate adoption. Vendors aiming to expand into MEA, South America, and Asia-Pacific markets face logistical hurdles, while resource-constrained settings increasingly favor cost-effective, stable alternatives. These factors limit adoption despite rising demand and expanding clinical applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Assay Kit Type: Colorimetric Formats Dominate and Fluorometric Formats Gain Ground

In 2025, colorimetric assay kits accounted for 35.13% of the amino acid assay kit market, maintaining their leading position among kit types. Their popularity stems from compatibility with standard microplate readers, simple workflows, and ease of use in quality control labs across food, beverage, and pharmaceutical industries. These kits utilize enzyme-catalyzed oxidation methods, offering linear detection ranges from 3.3 µM to 500 µM for samples like serum, urine, and tissue homogenates. Enzymatic assay kits cater to substrate-specific selectivity needs, while chromatographic kits, though costlier, are gaining traction in regulated environments requiring robust analytical validation.

The market is increasingly segmented between routine volume formats and high-performance specialty formats. Fluorometric assay kits, projected to grow at a 10.25% CAGR through 2031, are the fastest-growing segment. Their superior detection limits, 10 to 25 times better than many colorimetric alternatives, make them ideal for low-abundance samples like dried blood spots and microbioreactor media. These kits also align well with multiplexing and automated workflows, strengthening their role in pharmaceutical automation cycles.

By Application: Protein Quantification Anchors Demand and Amino Acid Profiling Accelerates

Protein quantification represented 28.45% of the amino acid assay kit market in 2025, making it the largest application. This demand is driven by its necessity in downstream analytical steps like SDS-PAGE and ELISA normalization. Nutritional analysis remains a stable segment, supporting infant formula standards and protein quality claims in alternative products. Research applications, including metabolomics, biomarker discovery, and preclinical drug development, further expand the market with demand for both simple and targeted analytical kits.

Amino acid profiling is expected to grow at a 9.55% CAGR from 2026 to 2031, driven by oncology research, personalized nutrition, and metabolic disorder screenings. Plasma amino acid profiling is increasingly used for assessing metabolic, cardiovascular, and liver-related risks, creating a middle tier of products that balance diagnostic sensitivity with multi-sample throughput.

By End User: Pharmaceuticals Lead and Diagnostic Centers Show the Fastest Growth

Pharmaceutical companies held a 25.66% share of the amino acid assay kit market in 2025, leading among end-user groups. Their demand spans drug development stages, including peptide composition analysis, toxicology biomarker studies, and therapeutic manufacturing support. The rise of GLP-1 receptor agonist development has amplified the need for high-throughput amino acid analysis in peptide synthesis workflows. Biotechnology firms closely follow, with consistent demand for amino acid monitoring in bioreactor optimization and process control.

Diagnostic centers are projected to grow at an 11.88% CAGR through 2031, driven by the expansion of newborn metabolic screenings and the adoption of amino acid panels for clinical risk assessments. Food and beverage sectors exhibit high testing volumes but lower per-kit prices. Academic and government research labs face spending constraints, impacting their purchasing patterns in the near term.

Geography Analysis

In 2025, North America led the amino acid assay kit market with a 39.56% share, driven by strong pharmaceutical R&D, a large biopharmaceutical manufacturing base, and stringent protein labeling regulations in the U.S. The U.S. dominated regional demand, while Canada contributed through academic and government research, and Mexico gained prominence with near-shoring in pharmaceutical manufacturing. Europe ranked as the second-largest market, supported by Germany, France, and the U.K., where university-linked proteomics centers and established food safety testing systems sustained demand. Merck KGaA emphasized Europe’s importance with its Irish expansion, including a EUR 150 million (USD 165 million) facility at Blarney Business Park and a EUR 440 million (USD 484 million) investment.

Asia-Pacific is projected to grow at a 10.12% CAGR through 2031, making it the fastest-growing region. Growth is driven by rising healthcare spending, expanding pharmaceutical manufacturing, and government-backed newborn screening initiatives. China plays a central role due to biotechnology policy support and cost-effective MS/MS-based newborn screening. Japan and South Korea, as advanced sub-markets, utilize established analyzers and automated systems, while India’s contract research base and Australia’s active university research network further boost demand.

MEA and South America are emerging markets for amino acid assay kits, progressing toward formal testing infrastructure. In MEA, Saudi Arabia and the UAE are investing in hospital-based newborn screening, while South Africa maintains demand through academic medical centers. In South America, Brazil and Argentina anchor demand, with Brazil’s pharmaceutical and food testing sectors leading purchases. Price sensitivity and inconsistent cold-chain systems in these regions favor colorimetric and enzymatic kits, resulting in a distinct product mix compared to North America, Europe, and advanced parts of Asia-Pacific.

Competitive Landscape

Leading the charge in the amino acid assay kit market are industry giants like Thermo Fisher Scientific, Danaher, Merck KGaA, Agilent Technologies, and Revvity. These companies leverage expansive product portfolios and a global commercial infrastructure, often bundling reagents with instruments, software, and workflow support. Such bundling is crucial as institutional buyers typically favor validated end-to-end setups, which mitigate implementation risks and streamline procurement. In a strategic move, Thermo Fisher bolstered its market position in 2024 by acquiring Olink, enhancing its footprint in proteomics and amplifying cross-selling avenues in biomarker discovery and analytical workflows. This platform expansion in the amino acid assay kit market fortifies top-tier suppliers, granting them an edge over standalone reagent vendors who primarily compete on price.

Agilent Technologies exemplified this strategy in May 2026 by launching its Multi-Attribute Method solution for biopharmaceutical quality control, tailored for LC-HRMS-based amino acid quantification in regulated environments. Revvity is also leveraging ecosystem positioning by integrating NeoBase 2 reagents with SCIEX mass spectrometers for newborn screenings. These strategies highlight how competitive strength in the amino acid assay kit market now hinges on workflow integration as much as assay chemistry. Suppliers capable of connecting reagents to hardware, automation scripts, and regulatory documentation are better positioned for long-term account retention.

While the top tier dominates, Chinese firms like Elabscience Biotechnology, CUSABIO Technology, and Abbkine are intensifying price competition in routine kit categories. Their ISO-certified products, priced 30% to 50% lower than many Western counterparts, are gaining traction in developing lab systems and among budget-conscious clients. As their publication visibility grows, they are narrowing the credibility gap that once shielded established players in research environments. Another notable development is Proteotype Diagnostics Ltd’s European patent EP4196797A1, covering amino acid concentration signature methods for cancer diagnostics, which could create a protected niche if commercialized into a regulated kit.

Amino Acid Assay Kit Industry Leaders

Abcam plc

Bio-Rad Laboratories, Inc.

Merck KGaA

Agilent Technologies, Inc.

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Agilent Technologies introduced its Multi-Attribute Method (MAM) solution for biopharmaceutical quality control. This globally available solution supports LC-HRMS-based amino acid quantification, meeting the increasing demand for regulatory-compliant analysis in biopharmaceutical QC laboratories.

- April 2026: Abcam, a Danaher company, launched the SimpleStep Ignite ELISA, a next-generation chemiluminescent immunoassay platform. Offering 50× the sensitivity and 35× the dynamic range of traditional colorimetric ELISAs, it delivers results in 55 minutes and competes directly with fluorometric amino acid assay formats for low-abundance detection, enhancing Danaher’s assay portfolio.

- April 2026: Waters Advanced Diagnostics released a UHPLC-MS/MS protocol for quantifying 42 amino acids in under 10 minutes, simplifying LC-MS-based newborn screening workflows.

- February 2026: Revvity showcased high-throughput platforms, including the EnVision Nexus One and Opera Phenix OptIQ, streamlining amino acid assay workflows in drug discovery automation.

- September 2025: Merck KGaA opened a EUR 150 million (USD 165 million) facility in Ireland, expanding filter manufacturing and reagent supply for global life science operations.

Global Amino Acid Assay Kit Market Report Scope

As per the scope of the report, an Amino Acid Assay Kit is a laboratory testing tool used to measure the exact amount of amino acids in a sample. Amino acids are the microscopic building blocks of proteins. These kits help scientists easily test food, blood, or plant tissue without needing expensive machinery.

The amino acid assay kit market is segmented by assay kit type, application, end-user, and geography. By assay kit type, the market includes colorimetric assay kits, fluorometric assay kits, chromatographic assay kits, and enzymatic assay kits. By application, the market is segmented into protein quantification, amino acid profiling, nutritional analysis, medical diagnostics, and research purposes. By end-user, the market is categorized into pharmaceuticals, biotechnology, food and beverage, diagnostic centers, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Colorimetric Assay Kits |

| Fluorometric Assay Kits |

| Chromatographic Assay Kits |

| Enzymatic Assay Kits |

| Protein Quantification |

| Amino Acid Profiling |

| Nutritional Analysis |

| Medical Diagnostics |

| Research Purposes |

| Pharmaceuticals |

| Biotechnology |

| Food and Beverage |

| Diagnostic Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Assay Kit Type | Colorimetric Assay Kits | |

| Fluorometric Assay Kits | ||

| Chromatographic Assay Kits | ||

| Enzymatic Assay Kits | ||

| By Application | Protein Quantification | |

| Amino Acid Profiling | ||

| Nutritional Analysis | ||

| Medical Diagnostics | ||

| Research Purposes | ||

| By End User | Pharmaceuticals | |

| Biotechnology | ||

| Food and Beverage | ||

| Diagnostic Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the amino acid assay kit space and where is it headed by 2031?

The amino acid assay kit market size stands at USD 1.52 billion in 2026 and is projected to reach USD 2.30 billion by 2031 at a CAGR of 8.50%.

Which assay kit type is growing the fastest through 2031?

Fluorometric assay kits are the fastest-growing type, with a projected CAGR of 10.25% because they offer stronger sensitivity in low-abundance and automated workflows.

Which application contributes the largest share of demand?

Protein quantification leads applications with 28.45% share in 2025 because it remains a routine and necessary step across pharma, biotech, and food testing workflows.

Which end-user group is expanding most quickly?

Diagnostic centers are expected to grow the fastest at 11.88% CAGR through 2031, supported by wider newborn screening and broader use of amino acid panels in clinical settings.

Which region leads global demand for amino acid assay kits?

North America led with 39.56% share in 2025 due to strong pharmaceutical R&D, mature laboratory systems, and a large biopharmaceutical manufacturing base.

What is shaping competition among leading suppliers?

Competition is being shaped by instrument-plus-reagent bundling, automation-ready workflows, and regulated QC solutions, with Thermo Fisher, Danaher, Merck KGaA, Agilent, and Revvity holding the broadest reach.

Page last updated on: