Luxembourg Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

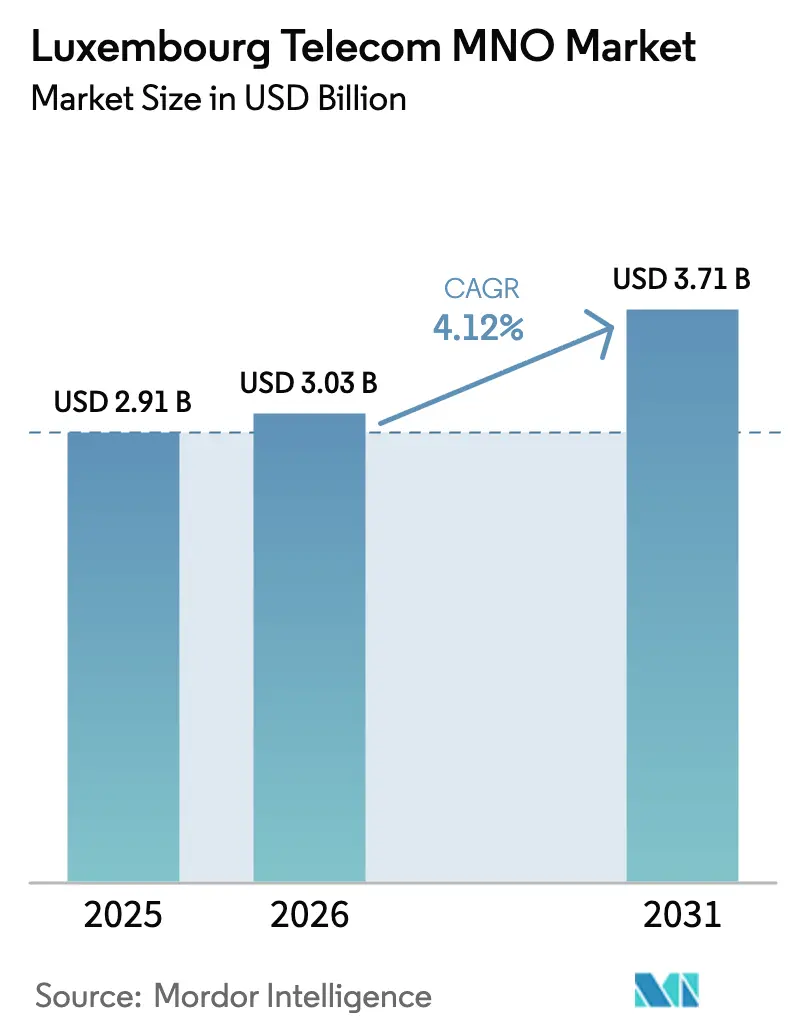

| Base Year Market Size (2025) | USD 2.91 Billion |

| Market Size (2026) | USD 3.03 Billion |

| Market Size (2031) | USD 3.71 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxembourg Telecom MNO Market Analysis by Mordor Intelligence

Luxembourg Telecom MNO Market size in 2026 is estimated at USD 3.03 billion, growing from 2025 value of USD 2.91 billion with 2031 projections showing USD 3.71 billion, growing at 4.12% CAGR over 2026-2031.

Sustained momentum comes from enterprise digitalization, sovereign-cloud investments, and growing cross-border data traffic that offset demographic saturation. Luxembourg’s 212,000 daily commuters, 46% of its workforce, create atypical weekday peaks that raise the value of surcharge-free EU roaming and drive premium data bundles. [1]European Commission, “Luxembourg 2024 Digital Decade Country Report,” digital-strategy.ec.europa.eu The government’s Digital Luxembourg program has earmarked EUR 302 million (USD 329 million) for 5G standalone and IoT campus networks, accelerating ubiquitous gigabit access and reinforcing the country’s reputation as one of Europe’s most connected economies. [2]Government of Luxembourg, “Luxembourg’s 5G Strategy,” innovative-initiatives.public.lu Concurrently, the completion of nationwide FTTH backhaul enables operators to sell genuinely unlimited mobile data while keeping congestion under control. [3]POST, “Discover the Speed of Fibre in Luxembourg,” post.lu SES’s growing multi-orbit satellite fleet further underpins coverage in rural pockets and introduces direct-to-device (D2D) use-cases that can be bundled with terrestrial plans. [4]SES & Lynk Global, “Strategic Partnership for D2D Services,” ses.com

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Luxembourg Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G standalone roll-out accelerates premium consumer and B2B use-cases | +1.2% | Luxembourg City and Esch-sur-Alzette | Medium term (2-4 years) |

| Nationwide FTTH backhaul enabling unlimited mobile data bundles | +0.8% | National corridors for cross-border commuters | Short term (≤ 2 years) |

| Government “Digital Luxembourg” subsidies for campus networks and IoT | +0.6% | Financial district and industrial zones | Medium term (2-4 years) |

| EU surcharge-free roaming boosts commuter usage | +0.5% | Borders with Belgium, France and Germany | Short term (≤ 2 years) |

| SES satellite–terrestrial convergence for seamless coverage | +0.4% | Rural and underserved communes | Long term (≥ 4 years) |

| Corporate demand for secure SD-WAN and private 5G slices | +0.7% | Enterprise zones in Luxembourg City | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G standalone roll-out accelerates premium consumer and B2B use-cases

POST Luxembourg activated Europe’s first autonomous AI-ready fiber core in March 2025 and paired it with 5G standalone, unlocking sub-10 ms latency services that meet algorithmic-trading thresholds and enable city-wide V2X pilots. Nokia’s selection by all three national networks reflects Luxembourg’s security-first procurement stance. Early proof-of-concept sites report 40% higher traffic per user versus NSA 5G, validating the upsell potential to both gamers and fintech clients. Demand is especially strong in Esch-Belval’s research campus, where edge nodes host AI inference for robotics trials. As spectrum refarming reaches the 700 MHz layer, operators can extend indoor 5G SA coverage without costly densification, further reinforcing premium tiers of the Luxembourg telecom MNO market.

Nationwide FTTH backhaul enabling unlimited mobile data bundles

More than 80% of households already connect to gigabit fiber, allowing mobile operators to shift from bandwidth rationing to abundance. Bundle offers now integrate 10 Gbit/s fixed and unlimited 5G mobile for a single price, raising subscriber stickiness and flattening peak-hour congestion through Wi-Fi offload. Cross-border workers exploit these plans during business hours, generating 30% higher uplink traffic than resident subscribers. The policy removes legacy constraints on video streaming and cloud-gaming, supporting double-digit growth in average data per SIM despite population saturation. All-IP migration also cuts opex by 18% in core networks, creating headroom to maintain EBITDA margins while scaling usage.

Government “Digital Luxembourg” subsidies for campus networks and IoT

Luxembourg invested EUR 155 million (USD 169 million) into the IRIS² sovereign constellation and channels EUR 302 million of recovery funds toward domestic digital projects. Subsidy schemes reimburse up to 35% of CAPEX for private 5G or Wi-Fi 6 campus networks that meet productivity KPIs, enticing manufacturers and banks to deploy latency-critical IoT. POST manages nearly 3 million active IoT lines spanning automotive telematics and remote-patient monitoring. The subsidy lowers risk for first movers, and the resultant data volumes reinforce the Luxembourg telecom MNO market’s transition toward analytics-led revenue models.

Corporate demand for secure SD-WAN and private 5G slices

Financial institutions account for one-third of corporate telecom spend and demand deterministic performance for digital trading desks, spurring uptake of network slicing layered on SD-WAN backbones. SES clinched a USD 200 million NATO secure-connectivity contract that showcases appetite for sovereign links with end-to-end encryption. Enterprises prefer bundled solutions that merge site-to-site SD-WAN, local 5G, and multi-orbit satellite redundancy. This integrated model commands ARPU premiums of 25% over legacy MPLS and accelerates the enterprise share of Luxembourg telecom MNO industry revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Population saturation limits organic SIM growth | -0.9% | Entire country | Short term (≤ 2 years) |

| High spectrum prices raise CAPEX burden | -0.6% | National | Medium term (2-4 years) |

| Stringent multilingual content rights inflate OTT costs | -0.4% | National | Medium term (2-4 years) |

| Intensifying price wars compress ARPU | -0.8% | Consumer segment nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Population saturation limits organic SIM growth

Luxembourg’s population hovers near 650,000, and mobile penetration exceeds 100%. Operators thus rely on churn capture rather than market expansion. With MVNO Join Experience having exited in 2020, competition now revolves around value-added bundles rather than subscriber additions. Cross-border commuters help soften the ceiling, yet EU “Roam-Like-at-Home” rules cap incremental revenue, forcing carriers to push service innovation instead of volume.

Intensifying price wars compress ARPU

Despite an oligopolistic structure, entry-level voice-plus-data plans can cost as little as EUR 10 (USD 11), as brands jockey for share in a zero-sum arena. The absence of roaming fees eliminates a historic cushion, while over-the-top messaging eats into paid SMS. Revenue growth slowed to 5.3% in 2023 compared with 7.3% a year earlier, indicating margin pressure. Operators, therefore, shift focus to upselling cloud storage, cybersecurity, and insurance add-ons to defend ARPU.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Drives IoT Innovation

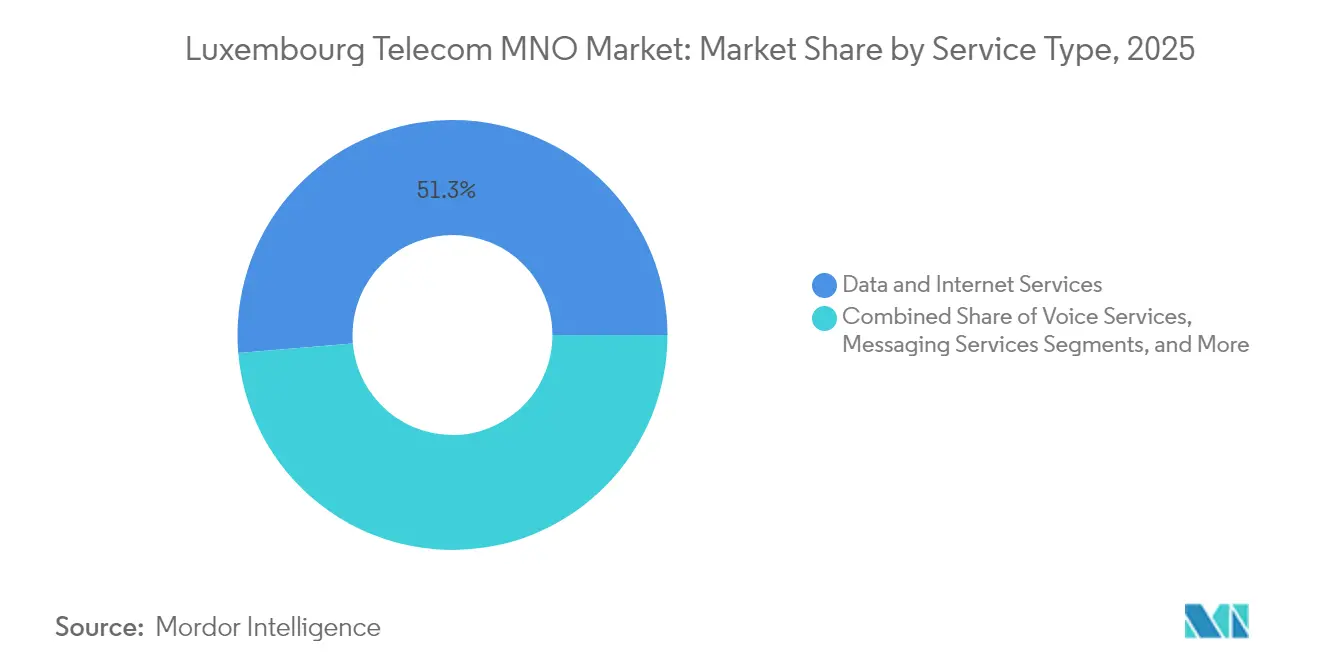

Data and internet services accounted for 51.34% of the Luxembourg telecom MNO market size in 2025, nearly double voice revenues, as commuters and residents alike consumed daily averages above 19 GB per SIM. Unlimited 5G bundles ride on FTTH backhaul, enabling HD-video, cloud-gaming, and hybrid-work traffic spikes. IoT and M2M hold a modest base today but post the fastest 4.42% CAGR through 2031, buoyed by government campus-network rebates and the influx of connected-vehicle mandates. Voice and legacy SMS revenues trend downward as RCS and OTT players gain mainstream adoption, while OTT & Pay-TV services find niche growth in Luxembourg’s multilingual households.

Operators leverage satellite integration to extend IoT beyond terrestrial footprints, positioning Luxembourg as a testbed for low-power massive IoT that can roam seamlessly onto non-terrestrial networks. Fixed-mobile convergence further blurs service lines, with cloud-gaming passes bundled into fiber and 5G offerings. The Luxembourg telecom MNO industry consequently pivots its revenue mix toward data analytics, subscription video, and IoT management platforms rather than classic usage-based tariffs.

By End User: Enterprise Acceleration Outpaces Consumer Growth

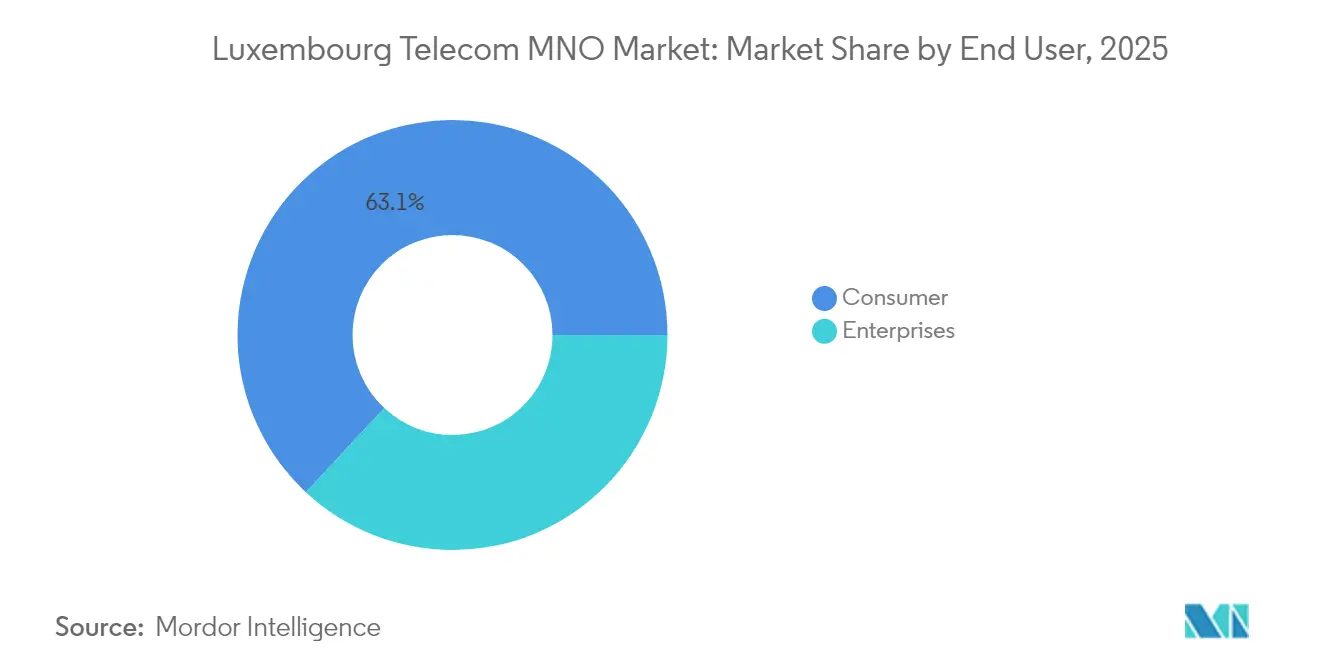

The consumer segment retained 63.05% of 2025 revenue, yet a 4.55% pace is projected for enterprises through 2031. Financial institutions, logistics hubs, and EU agencies seek private 5G slices paired with SD-WAN to secure workloads and slash latency. These premium contracts lift the enterprise share to an anticipated 41% of Luxembourg telecom MNO market revenue by decade-end.

Commuter behavior blurs the consumer-enterprise line, as cross-border workers generate weekday business traffic on personal plans. Operators, therefore, craft “dual-persona” bundles that fund enterprise-grade security while retaining consumer pricing. Sovereign-cloud requirements amplify enterprise spending on connectivity that stays within Luxembourg’s legal jurisdiction, offering incumbents a defensible niche. Meanwhile, value-sensitive consumers gravitate toward aggressive entry plans, necessitating ongoing cost discipline.

Geography Analysis

Luxembourg’s compact territory and landlocked position underpin a telecom fabric that must simultaneously cater to resident users and 212,000 daily commuters. German commuters alone number 52,619, and collectively cross-border households spend EUR 925 million (USD 1.01 billion) annually inside the Grand Duchy, a sum equivalent to 17% of gross income. Weekday data peaks therefore align with incoming rail and road corridors, requiring macro-cell densification near borders and highways.

EU roaming rules eliminate surcharge revenue but also encourage commuters to keep home SIMs active while in Luxembourg. Operators offset the foregone income by upselling unlimited plans that exploit FTTH backhaul capacity. Free nationwide public transport introduced in 2020 further redistributes network load, shifting part of rush-hour usage onto Wi-Fi on trains and buses.

Luxembourg boasts 99.6% household 5G coverage, surpassing the EU average and making capacity, not coverage, the primary engineering focus. The IRIS² sovereign constellation strengthens borderless connectivity for critical infrastructure, while SES’s acquisition of Intelsat raises the country’s geopolitical weight in multi-orbit policy discussions. These geographic and regulatory factors collectively ensure that the Luxembourg telecom MNO market remains export-oriented and interconnected with neighboring economies.

Competitive Landscape

Luxembourg’s telecom arena features three full MNOs plus a handful of niche MVNOs. State-owned POST heads the field by virtue of nationwide fiber ownership, a 10-Gbit/s retail benchmark, and early adoption of autonomous core networking. POST’s telecom division employs 800 specialists who manage fixed, mobile, and wholesale assets. The operator’s sovereign-cloud project with OVHcloud will commercialize in 2025, locking in enterprise workloads that comply with domestic data-residency rules.

Proximus-owned Tango focuses on efficiency after divesting 267 towers to InfraRed Capital Partners for EUR 108 million (USD 118 million), freeing capital for fiber co-builds and 5G densification. Orange Luxembourg leverages group-wide wholesale agreements to deliver competitively priced roaming and content bundles. All three picked Nokia as a 5G equipment vendor, underscoring alignment on supply-chain security.

Competitive strategies pivot away from legacy minute-based tariffs toward platform plays in IoT, cybersecurity and satellite extension. SES’s multi-orbit roadmap invites partnerships for hybrid connectivity, while start-ups such as OQ Technology target narrowband-IoT over satellite for asset-tracking niches. Vendor interest in Luxembourg as a European test lab is rising, evidenced by Adtran joining LU-CIX to showcase open-optics platforms.

Luxembourg Telecom MNO Industry Leaders

POST Luxembourg

Orange Luxembourg

Tango S.A.(Proximus Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SES completed its USD 3.1 billion purchase of Intelsat, creating the globe’s largest multi-orbit fleet.

- March 2025: SES and Lynk Global formed a D2D alliance covering MNO and automotive sectors.

- December 2024: SES signed the IRIS² concession with the European Commission for Europe’s sovereign constellation.

- November 2024: Proximus sold 267 Luxembourg towers to InfraRed Capital Partners for EUR 108 million (USD 118 million).

- November 2024: POST Group joined forces with OVHcloud to launch Luxembourg’s first sovereign cloud in 2025.

Luxembourg Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The Luxembourg telecom MNO market report includes an in-depth trend analysis based on connectivity, including fixed networks, mobile networks, and telecom towers. Several factors, including an increasing demand for 5G, are likely to drive the adoption of telecom services.

The Luxembourgish telecom MNO market is segmented by services (voice services (wired and wireless), data and messaging services, OTT and PayTV services). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Luxembourg telecom MNO market in 2026?

The market is valued at USD 3.03 billion in 2026 and is forecast to grow to USD 3.71 billion by 2031.

What is the projected CAGR for Luxembourg’s mobile operators?

Revenue is forecast to expand at a 4.12% CAGR over 2026-2031.

Which service category generates the most revenue?

Data and internet services lead with 51.34% of total telecom mobile revenue in 2025.

Why is enterprise growth outpacing consumer growth?

Financial institutions and multinational corporations are adopting private 5G slices, SD-WAN and secure IoT at faster rates, driving a 4.55% enterprise CAGR over 2026-2031.

How does Luxembourg’s commuter population affect network planning?

212,000 cross-border workers create weekday traffic peaks along border corridors, necessitating dense 5G deployments and generous roaming allowances.

What role does satellite play in the market?

Luxembourg-based SES complements terrestrial networks with multi-orbit coverage, enabling direct-to-device services and rural IoT backhaul.

Page last updated on: