Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

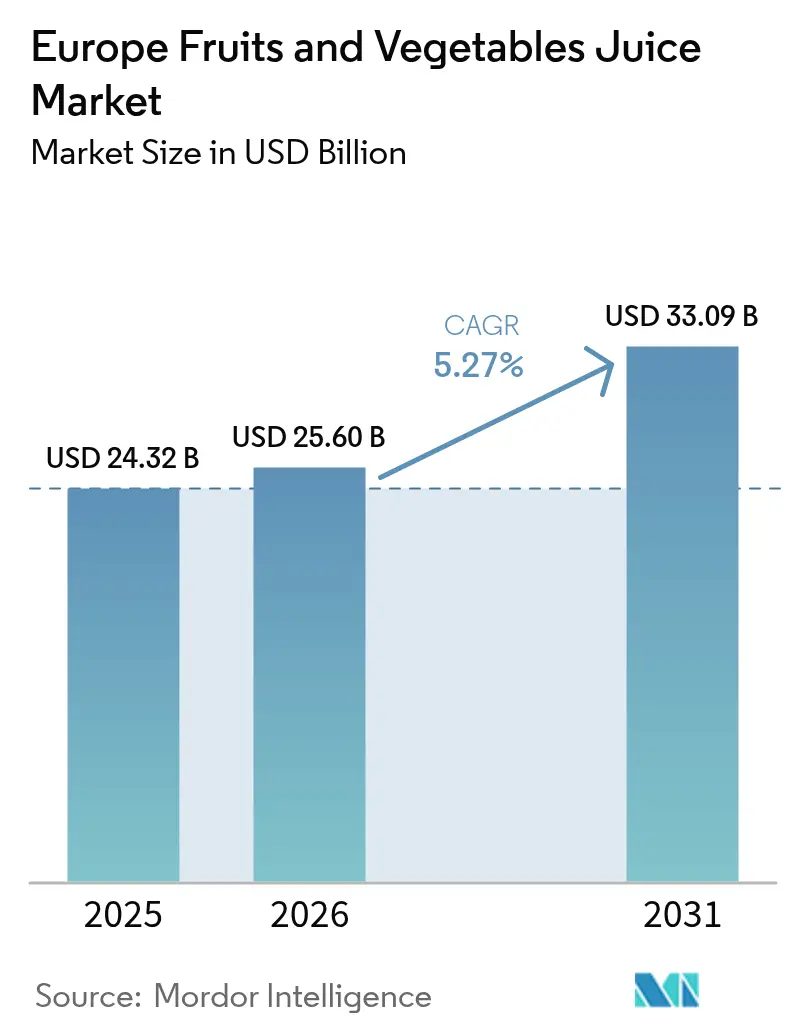

| Base Year Market Size (2025) | USD 24.32 Billion |

| Market Size (2026) | USD 25.6 Billion |

| Market Size (2031) | USD 33.09 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

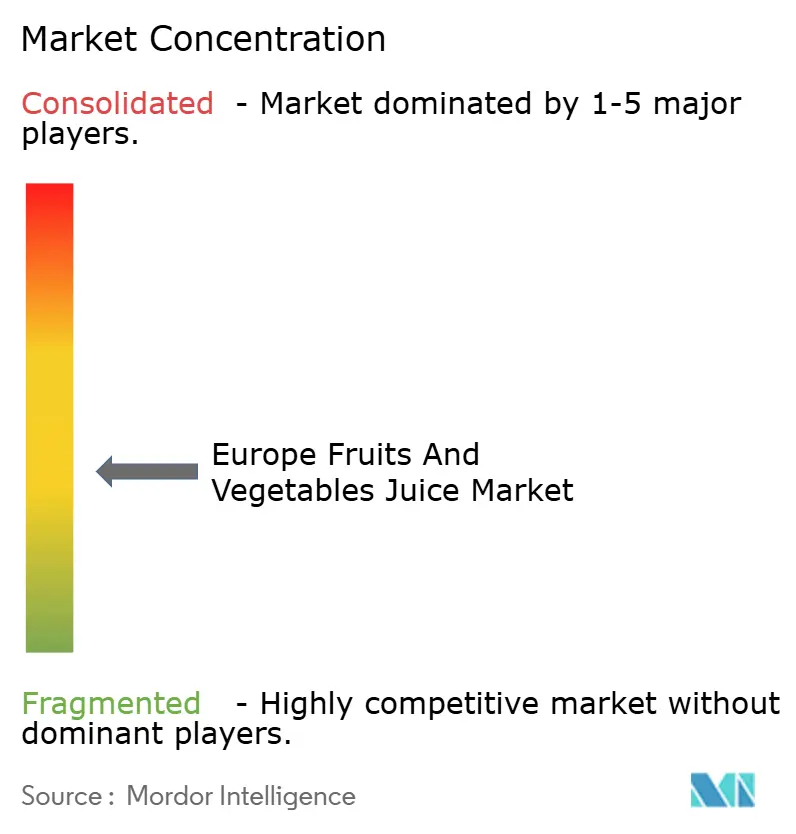

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Fruits And Vegetables Juice Market Analysis by Mordor Intelligence

The European fruit and vegetable juice market size was valued at USD 24.32 billion in 2025 and estimated to grow from USD 25.6 billion in 2026 to reach USD 33.09 billion by 2031, at a CAGR of 5.27% during the forecast period (2026-2031). The market growth is driven by increasing consumer preference for nutrient-rich beverages, as health-conscious consumers seek alternatives to sugary drinks. Government regulations promoting sugar reduction and strict labeling requirements have prompted manufacturers to reformulate their products. Continuous advancements in packaging technology, including sustainable materials and extended shelf-life solutions, further support market expansion. Manufacturers are investing heavily in cold-press and not-from-concentrate production methods to preserve essential vitamins, minerals, and antioxidants, while retailers are expanding their offerings of functional beverages targeting specific health benefits such as digestive health, immune system support, and enhanced cognitive performance. The 2024 Breakfast Directive enables companies to label juices as containing "only naturally occurring sugars," which is expected to increase premium 100% juice product launches and improve consumer perception of these products.[1]Source: European Parliament, “Directive 2024/1438 on fruit juices,” europarl.europa.euAdditionally, growing consumer demand for clean-label products is pushing manufacturers to simplify ingredient lists, establish transparent and traceable supply chains from farm to shelf, and obtain organic certifications to meet evolving consumer preferences.

Key Report Takeaways

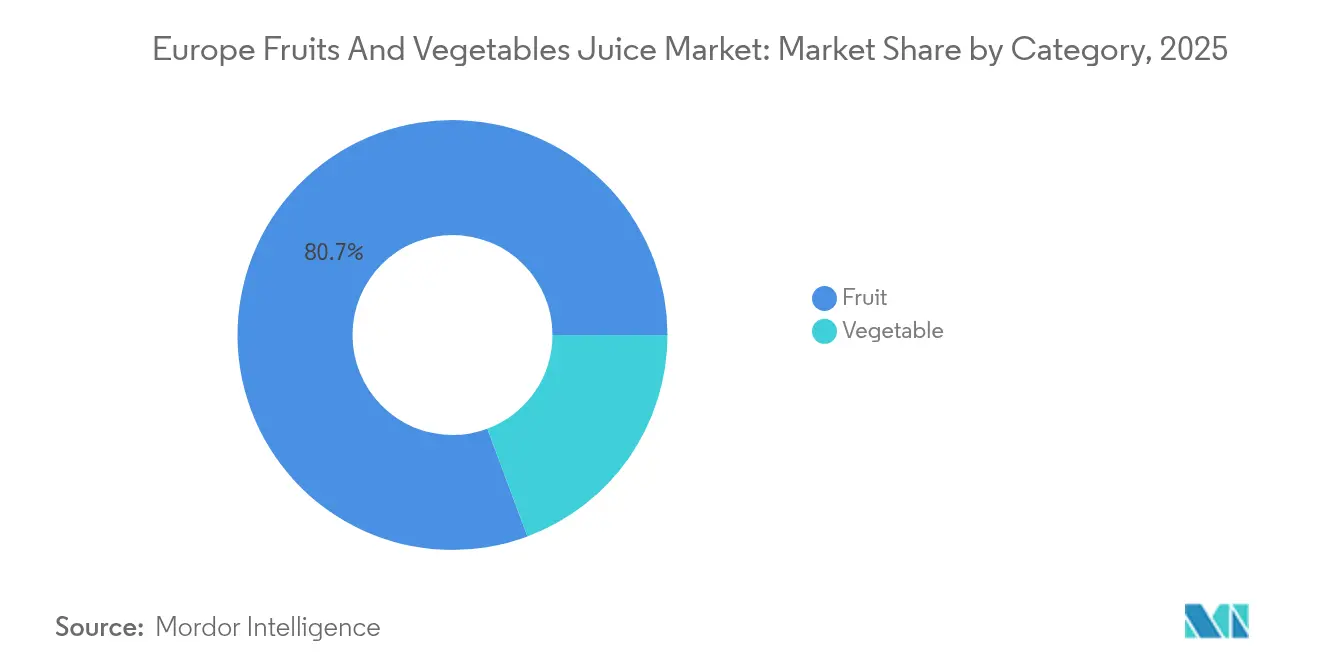

- By category, fruit juices led with 80.67% revenue share in 2025, while vegetable juices are projected to expand at a 5.44% CAGR through 2031.

- By type, 100% juice accounted for 48.82% of the European fruit and vegetable juice market size in 2025, and nectar products are projected to grow at a 4.79% CAGR through 2031.

- By nature, the conventional segment accounted for 86.75% share in 2025, and the organic segment is pacing ahead at a 6.92% CAGR through 2031.

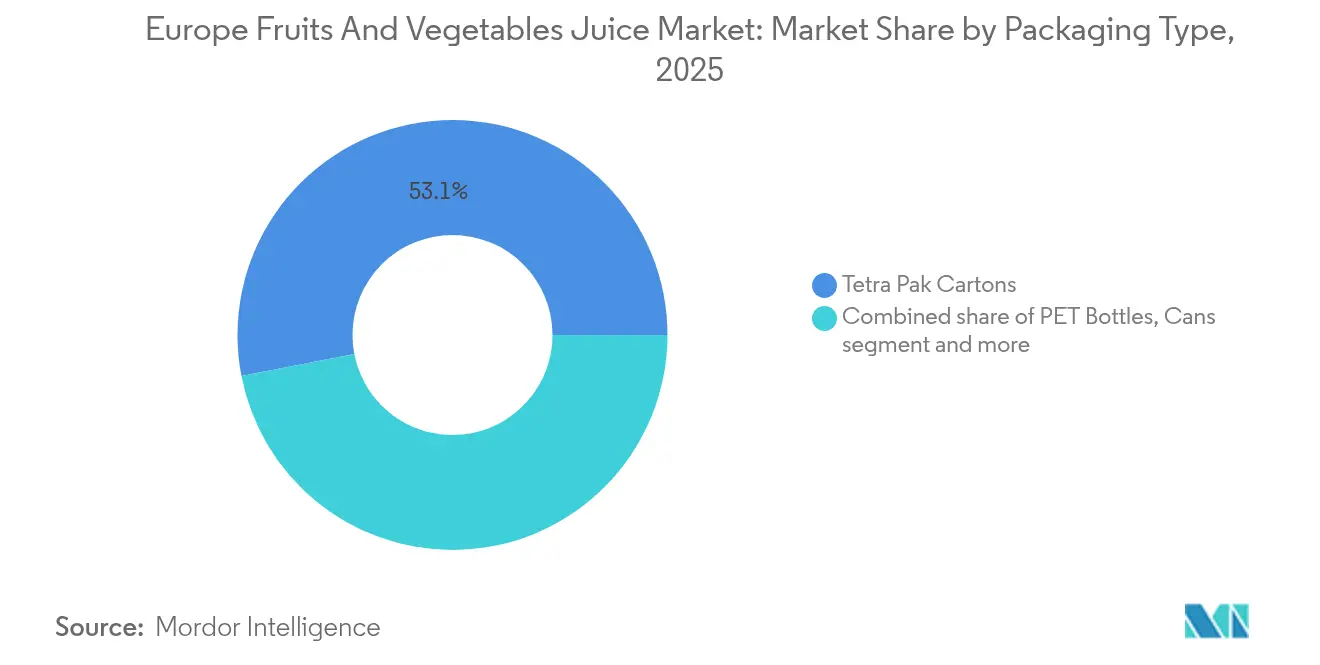

- By packaging, Tetra Pak cartons captured 53.05% of the European fruit and vegetable juice market share in 2025, whereas PET bottles deliver the quickest growth at 6.02% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets commanded 59.68% of sales in 2025, with online platforms forecast to post an 11.60% CAGR through 2031.

- By geography, Germany held a 20.12% market share in 2025, while the United Kingdom recorded a 6.52% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Fruits And Vegetables Juice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product innovation and flavor diversification | +1.2% | Germany, France, Netherlands | Medium term (2-4 years) |

| Growing demand for functional beverages | +1.5% | United Kingdom, Germany, Scandinavia | Long term (≥ 4 years) |

| Demand for sustainable juices | +0.8% | Germany, Netherlands, Austria | Long term (≥ 4 years) |

| Growing urbanization and on-the-go consumption | +0.7% | United Kingdom, France, Spain, Italy | Short term (≤ 2 years) |

| Growing demand for natural juices and clean label trends | +1.0% | Germany, United Kingdom, Netherlands | Medium term (2-4 years) |

| Expansion of retail and e-commerce channels | +0.9% | All European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Product Innovation and Flavor Diversification

European juice manufacturers are using advanced processing technologies, including high-pressure processing, ultrafiltration, cold-press extraction, and aseptic packaging systems, to develop products that address specific consumer health needs beyond traditional vitamin content. They are incorporating functional ingredients such as probiotics for digestive health and immune support, adaptogens like ashwagandha and rhodiola for stress management and mental clarity, and plant-based proteins derived from pea, hemp, and rice for muscle recovery and satiety to transform juice from a refreshment into a wellness product. Moreover, 100% fruit and vegetable juices are proven to benefit cardiometabolic health by reducing blood pressure, managing cholesterol levels, and improving circulation, enhance cognitive function through flavonoid compounds and omega-3 fatty acids, and optimize exercise performance by providing natural electrolytes, antioxidants, and essential minerals, providing scientific support for functional juice development. This research-based approach allows manufacturers to make validated health claims while distinguishing their products in the market. The growing focus on personalized nutrition is increasing demand for specialized formulations for different consumer groups, including immunity-boosting blends with elderberry, echinacea, zinc, and vitamin C for children and antioxidant-rich combinations with pomegranate, blueberry, acai, and green tea extracts for older consumers.

Growing Demand for Functional Beverages

The functional beverage market in Europe is growing as consumers seek drinks that offer specific health benefits beyond hydration. The United Kingdom and EU markets show increasing demand for beverages that combine health functionality with enjoyable taste. This shift reflects a broader consumer movement toward products that support overall wellness while maintaining convenience and palatability. The trend aligns with increasing health consciousness and preventive healthcare approaches among European consumers, particularly in urban areas where lifestyle-related health concerns are prevalent. Millennials and Gen Z consumers are driving this trend, showing a preference for premium-priced drinks that support mental wellness, digestive health, and immunity. These demographic groups prioritize products with scientifically backed ingredients and transparent labeling, often researching product benefits before purchase and sharing recommendations through social media platforms. European beverage manufacturers have adapted by integrating functional ingredients such as CBD, turmeric, and probiotics into their juice products, developing beverages that combine nutritional and therapeutic properties. The incorporation of these ingredients represents a strategic response to consumer demand for products that bridge the gap between conventional beverages and health supplements. This evolution in the beverage industry demonstrates the growing intersection between daily consumption habits and proactive health management, reflecting a fundamental shift in how Europeans approach their daily drink choices and overall wellness routines.

Demand for Sustainable Juices

Environmental concerns are fundamentally transforming the European juice industry as consumers increasingly prioritize both ecological impact and health benefits in their purchasing decisions. The EU's Farm to Fork strategy and its ambitious goal of achieving climate neutrality by 2050 are driving comprehensive changes throughout the supply chain, from sustainable agricultural methods to eco-friendly packaging alternatives.[2]Source: CBI Ministry of Foreign Affairs, “EU Farm to Fork strategy,” cbi.eu These changes include implementing regenerative farming practices, reducing water consumption, optimizing transportation networks, and developing biodegradable packaging solutions. German consumers are at the forefront of this environmental transition, consistently supporting organic market growth and maintaining strong demand despite ongoing economic challenges. The emphasis on sustainability has expanded beyond traditional environmental certifications to encompass broader initiatives, including systematic carbon footprint reduction, transparent ethical sourcing practices, and widespread circular economy adoption. This expansion involves detailed supply chain traceability, waste reduction programs, renewable energy integration, and community engagement initiatives. Companies that successfully demonstrate quantifiable environmental improvements across their operations are gaining significant market advantages, as sustainability metrics become increasingly integral to consumer purchasing decisions and brand loyalty. These metrics now include specific measurements of greenhouse gas emissions, water usage efficiency, waste reduction achievements, and social impact indicators.

Growing Urbanization and On-the-Go Consumption

European urbanization patterns are fundamentally transforming juice consumption habits, as increasingly busy lifestyles drive substantial demand for convenient, portable nutrition solutions. According to the World Bank, in 2023, approximately 85% of the United Kingdom's population resided in urban areas, reflecting a broader continental shift toward city living.[3]Source: World Bank, "Urban population (% of total population) - United Kingdom", data.worldbank.org The growing trend toward smaller households and extended commuting times has significantly increased demand for single-serve packaging formats and shelf-stable products that maintain nutritional value without refrigeration requirements. European grocery retailers are strategically responding to these changes by expanding convenience store formats and comprehensively adapting product selections for urban consumers. This urbanization impact is particularly significant in major metropolitan areas such as London, Paris, and Berlin, where time-conscious consumers consistently prioritize convenience and readily accept premium pricing for products that seamlessly align with their mobile lifestyles. These demographic and behavioral changes present substantial opportunities for packaging innovations, including advanced resealable pouches and sophisticated portion-controlled formats that effectively support on-the-go consumption while maintaining stringent product quality and safety standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content in juice products | -1.8% | United Kingdom, Germany, Netherlands | Short term (≤ 2 years) |

| Increasing popularity of low/no sugar RTD beverages | -1.2% | All European markets | Medium term (2-4 years) |

| Rising preference for whole fruits and vegetables | -0.9% | Germany, Austria, Switzerland | Long term (≥ 4 years) |

| High sugar content in commercial juices | -0.7% | France, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Sugar Content in Juice Products

High sugar content in commercial juice products is limiting market growth as European consumers increasingly examine nutritional labels and seek lower-sugar alternatives. The trend is particularly evident in markets like Germany, France, and the UK, where health awareness is driving purchasing decisions. The European Union's revised Breakfast Directive (May 2024) allows manufacturers to produce "reduced-sugar fruit juice" products with 30% less natural sugar while preserving fruit content. This directive specifically addresses consumer demands for healthier options while maintaining product authenticity. Major manufacturers like Innocent Drinks and Tropicana have invested significantly in research and development to develop sugar-reduction technologies. However, manufacturers face technical difficulties in reducing sugar levels without affecting taste and nutritional value, including challenges in enzyme processing and maintaining shelf stability. The cost of sugar-reduction processes has increased production expenses by 15-20% on average. While consumer education initiatives emphasize the difference between natural and added sugars through retail partnerships and digital campaigns, public health campaigns' broad categorization of all sugar types creates market uncertainty. New regulations enable manufacturers to label products with "only naturally occurring sugars," though consumer skepticism remains prevalent across European markets, particularly among millennials and health-focused demographic segments, with consumers aged 25-34 expressing concerns about sugar content in fruit juices.

Increasing Popularity of Low/No Sugar RTD Beverages

The growth of low-calorie and zero-calorie ready-to-drink beverages directly competes with traditional juice products in the global beverage market. This significant trend reflects changing consumer preferences driven by increased diabetes awareness, personal weight management goals, and broader wellness priorities that emphasize functional health benefits over conventional taste experiences. Recent advances in artificial sweeteners and natural zero-calorie alternatives enable beverage manufacturers to develop products that closely match traditional juice flavors while offering substantially lower caloric content. This intensifying competition particularly affects the premium juice segment, where consumers have traditionally accepted higher sugar content in exchange for superior quality ingredients and natural formulations. The shift has prompted traditional juice manufacturers to adapt their product portfolios and reformulate existing offerings to maintain market relevance. Manufacturers are investing in research and development to create innovative blends that balance health considerations with taste expectations, while retailers are adjusting shelf space allocation to accommodate the expanding range of alternative beverages. This market evolution has also led to strategic partnerships between juice companies and ingredient suppliers to develop proprietary sweetening solutions that meet evolving consumer demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Vegetable Juices Capture Wellness Momentum

Fruit juices led the European Fruits and Vegetable Juice Market with an 80.67% share in 2025, whereas vegetable juices demonstrated robust growth potential with a projected CAGR of 5.44% through 2031. Juices based on carrots, beets, and tomatoes gain market traction due to research from Cambridge Core establishing connections between nitrates and carotenoids with improved endurance and blood pressure regulation. Companies position these products as savory alternatives to traditional sweet beverages, addressing sugar concerns while targeting meal-replacement opportunities. In German e-commerce platforms, premium glass-packaged cold-pressed beetroot mint varieties command a price premium compared to conventional orange juice. Manufacturers combine beet with berry and carrot with mango to create balanced flavor profiles that appeal to younger demographics. The higher fiber content in these beverages supports satiety and aligns with consumer weight management goals.

The market expansion includes vegetable-based recipes in smoothie kits and High-Pressure Processing (HPP) chilled products available through the United Kingdom's click-and-collect services. Health-focused cafés incorporate ready-to-drink beet and kale bases in immunity-boosting beverages. Manufacturers enhance their production capabilities with advanced extraction systems that reduce oxidation and improve color retention, creating distinct product differentiation. In Spain, agricultural cooperatives establish fixed-price contracts for beet supply, adapting to shifts from sugar beet to table beet cultivation following European Union quota modifications. These operational improvements help maintain profit margins despite increasing market competition.

By Type: Nectar Products Bridge Health and Affordability

The market for 100% juice accounted for a 48.82% share in 2025, maintaining market leadership due to consumer perception of purity and natural ingredients. The nectar segment is growing at a 4.79% CAGR, as manufacturers adjust fruit concentration between 25% and 99% to optimize sugar content, pricing, and nutritional value. Apple-mango nectars with vitamin C fortification appeal to parents seeking school-compliant beverage options for their children's daily nutrition requirements. The controlled dilution process enables manufacturers to incorporate calcium and botanical extracts while maintaining balanced flavors and ensuring optimal taste profiles.

Not-from-concentrate (NFC) products continue to expand in the premium segment, driven by increasing consumer demand for minimally processed beverages. Consumer education initiatives emphasize NFC's reduced thermal processing time, which preserves essential aromatic compounds and delivers superior fresh taste characteristics. This positioning supports price premiums up to 30% higher than reconstituted 100% juice products, aligning with European consumer preferences for authentic, artisanal products and traditional production methods.

By Nature: Organic Segment Accelerates on European Union Farm to Fork Targets

Conventional segment maintains market dominance with an 86.75% share in 2025, while the organic segment demonstrates a 6.92% CAGR (2026-2031). Germany exhibits particularly strong expansion in its organic category, driven by increasing consumer health consciousness and environmental awareness. Retailers facilitate market penetration through dedicated refrigeration units, prominent shelf placement, and comprehensive loyalty program incentives to encourage consumer trials. Manufacturers focus on cloudy juice varieties and reduced filtration processes to retain natural fiber and pulp content, addressing consumer preferences for minimally processed products and authentic taste profiles.

Tropical organic fruit procurement faces persistent constraints due to limited certified farming operations and complex logistics networks. Manufacturers establish partnerships with Central American cooperatives to ensure a consistent mango and pineapple supply through long-term fair-trade agreements, which include technical support and sustainable farming practices. The combination of certification labels and carbon footprint information enhances product transparency, validates sustainability claims, and helps justify premium pricing in competitive retail environments.

By Packaging Type: PET Evolves Toward Closed-Loop Systems

Tetra Pak cartons capture 53.05% of the market share in 2025, whereas PET bottle packaging demonstrates significant growth with a 6.02% CAGR (2026-2031). German and Dutch recycling facilities have achieved 98% bottle-to-bottle recovery rates through advanced sorting technologies and efficient collection systems, enhancing PET's circular economy credentials. The TERRIFIC project, a collaborative European research initiative, aims to develop bottles with a minimum of 95% bio-based content and 40% reduced CO₂ emissions throughout the lifecycle through innovative material formulations and processing techniques. The transparent nature of PET packaging highlights juice colors and product authenticity, improving product visibility and consumer appeal on retail shelves.

Carton manufacturers continue to innovate through sustainable packaging solutions. Tetra Pak plans to introduce tethered caps in 2025, ensuring cap retention during recycling and compliance with EU Single-Use Plastics Directive requirements through integrated design features. The company currently incorporates plant-based plastic layers derived from sugarcane in more than 3.5 billion European packages annually, reducing fossil fuel dependency. Glass packaging maintains its premium position, particularly for not-from-concentrate products in specialty retail channels and high-end beverage segments, though higher transportation emissions and energy-intensive production processes limit its broader market adoption.

By Distribution Channel: Digital Platforms Reshape Consumer Access

Supermarkets and hypermarkets dominate with 59.68% of sales in 2025, with online platforms demonstrating significant growth with an 11.60% CAGR through 2031. Major retailers now offer nationwide next-day delivery services, complemented by subscription-based discounts for recurring juice purchases. Brand owners' direct-to-consumer platforms enhance customer experience through personalized product bundles and functional beverage recommendations based on customer preferences, resulting in increased average basket values. These platforms implement real-time temperature monitoring systems to ensure cold-chain integrity, particularly for high-pressure processed (HPP) products.

Convenience stores capitalize on impulse purchases near transportation hubs by offering 200 ml PET bottles at higher margins. The market accessibility extends through vending machines equipped with QR payment systems, providing 24-hour availability in universities and hospitals. In rural Germany, farm-shop collection points create direct links between small organic orchards and urban consumers seeking authentic sourcing. This diversified channel strategy ensures comprehensive market coverage and strengthens supply chain resilience against potential disruptions.

Geography Analysis

Germany dominates with a 20.12% share of the European fruit and vegetable juice market, driven by increasing consumer preference for organic products. The country's comprehensive certification infrastructure, rigorous quality standards, and consumers' willingness to pay premium prices of 15-20% above conventional products support this trend. Major retailers like Edeka prominently display cold-pressed juices in dedicated end-cap positions and refrigerated sections, highlighting Germany's established position in sustainable and functional beverages. Berlin's Fruit Logistica trade fair, attracting over 70,000 visitors annually, provides essential market access for international suppliers who meet Germany's strict residue limits, quality parameters, and detailed labeling standards.

The United Kingdom projects a robust 6.52% CAGR through 2031. Post-Brexit tariff reductions on citrus products and expanded bilateral agreements create substantial opportunities for Mediterranean suppliers. UK consumers demonstrate a marked preference for not-from-concentrate (NFC) orange juice and apple variants in convenient 330 ml PET containers with resealable caps, reflecting evolving consumption patterns. High urban population density increases demand for portable packaging formats, while expanding click-and-collect grocery services help new brands gain market presence through digital channels. Ongoing government discussions about sugar taxation influence product formulation strategies but position reduced-sugar juices as beneficial alternatives in the beverage category.

France, Italy, and Spain represent significant market volume, with established processing capabilities and distribution networks. France maintains premium pricing for NFC juices and leads innovative bottle-return programs supporting circular economy initiatives across major retail chains. Italy's extensive domestic citrus production enables competitive pricing for seasonal blood-orange products, particularly during winter months. Spain, processing substantial volumes of peach and apricot concentrates, benefits from increasing re-export trade with Asian markets as post-pandemic demand recovers. The Netherlands serves as a strategic distribution center, utilizing Rotterdam's advanced cold-chain facilities and extensive European transport connections. Austria and Switzerland, though smaller markets, demonstrate high per-capita consumption rates and strong consumer loyalty to organic cloudy apple juices, creating profitable opportunities for specialized producers in premium segments.

Competitive Landscape

The European fruit and vegetable juice market is moderately fragmented, with several established companies controlling significant portions of the market share. Major players, including PepsiCo Inc., The Coca-Cola Company, Capri Sun Group Holding AG, and Eckes-Granini Group GmbH, hold significant market shares. The 2024 acquisition of Britvic by Carlsberg introduces a major brewing company into the juice market, combining Britvic's extensive raw material procurement capabilities with Carlsberg's comprehensive European distribution network.

Market leaders differentiate themselves through comprehensive technological advancement strategies. PepsiCo implements sophisticated AI systems to predict fruit yield variations and maintain consistent blend quality across multiple European manufacturing facilities. Eckes-Granini utilizes advanced ultraviolet flash pasteurization technology, which substantially reduces thermal impact on the product and increases shelf life from 30 to 70 days. Private-label products, manufactured by contract packers with sophisticated multi-fruit filling capabilities, create intense price competition and significantly impact branded product margins. Brand manufacturers maintain market position through focused messaging on ingredient sourcing transparency and scientifically-backed product benefits.

New market entrants utilize innovative direct-to-consumer distribution models, delivering specialized not-from-concentrate beet-ginger shots in temperature-controlled packaging systems. These companies emphasize comprehensive regenerative agriculture partnerships and provide detailed transparency through satellite imagery of their orchards to demonstrate sustainable farming practices. They typically establish strategic partnerships with ISO-certified co-packers for production, maintaining flexible variable cost structures until achieving operational scale. Investment activity increasingly focuses on probiotic juice companies, identifying dairy-free gut health products as a significant underdeveloped segment in the European fruit and vegetable juice market, presenting substantial growth opportunities.

Europe Fruits And Vegetables Juice Industry Leaders

-

PepsiCo Inc.

-

The Coca-Cola Company

-

Eckes-Granini Group GmbH

-

Capri Sun Group Holding AG

-

Refresco Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Marks and Spencer (M&S) launched a new seven-vegetable, cold-pressed drink called Punishment Juice. The beverage, which combines fresh vegetables in a unique blend, is available in more than 400 M&S stores across the United Kingdom.

- May 2025: Vianature launched a natural refrigerated pineapple juice made from Golden Sweet pineapples. The product contains no added sugars or preservatives, addressing consumer demand for natural, high-quality beverages.

- March 2025: Tropicana introduced its Fresh & Light juice range in the United Kingdom, which is offered across major British retailers in Pure-Pak cartons. The Fresh & Light range offers Tropicana's juice with reduced sugar content, providing consumers with an alternative to traditional fruit juice products.

- February 2024: James White Drinks launched Veg It, a new vegetable juice blend containing eight vegetables, following the withdrawal of V8 juice from UK supermarket shelves. The product aims to help consumers increase their daily vegetable consumption.

Europe Fruits And Vegetables Juice Market Report Scope

Fruit and vegetable juices are healthy drinks made from the extraction or pressing of natural fruits and vegetables.

The European Fruits and Vegetables Juice Market is segmented by category, type, nature, packaging type, distribution channels, and geography. The market is categorized into fruit and vegetables based on category type. According to juice type, the market is divided into 100% juice, nectar containing 25-99% juice content, and juice drinks with less than 25% juice content. Based on nature, the market is classified into conventional and organic segments. The packaging types in the market include Tetra Pak cartons, PET bottles, glass bottles, cans, pouches, and others. The distribution channels comprise supermarkets/hypermarkets, convenience/grocery stores, online retail, and other channels. Geographically, the market covers the United Kingdom, Germany, France, Italy, Spain, Netherlands, and the Rest of Europe.

For each segment, the market sizing and forecasting have been done in value terms (USD million).

By Category

| Fruit Juice |

| Vegetable Juice |

By Type

| 100 % Juice |

| Nectar (25-99 % Juice) |

| Juice Drinks (<25 % Juice) |

By Nature

| Conventional |

| Organic |

By Packaging Type

| Tetra Pak Cartons |

| PET Bottles |

| Glass Bottles |

| Cans |

| Pouches and Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail |

| Other Distribution Channels |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Category | Fruit Juice |

| Vegetable Juice | |

| By Type | 100 % Juice |

| Nectar (25-99 % Juice) | |

| Juice Drinks (<25 % Juice) | |

| By Nature | Conventional |

| Organic | |

| By Packaging Type | Tetra Pak Cartons |

| PET Bottles | |

| Glass Bottles | |

| Cans | |

| Pouches and Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail | |

| Other Distribution Channels | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe fruit and vegetable juice market?

The Europe fruit and vegetable juice market is valued at USD 25.6 billion in 2026.

How fast is the Europe fruit and vegetable juice market expected to grow?

The market is projected to expand at a 5.27% CAGR, reaching USD 33.09 billion by 2031.

Which country is the largest consumer of fruit and vegetable juice in Europe?

Germany leads with a 20.12% share, supported by advanced processing infrastructure and strong demand for organic products.

What packaging format is growing quickest in the region?

PET bottles post the fastest growth at a 6.02% CAGR due to recycling progress and resealable convenience.

Page last updated on: