Georgia Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 537.58 Million |

| Market Size (2030) | USD 657.63 Million |

| Growth Rate (2025 - 2030) | 4.11% CAGR |

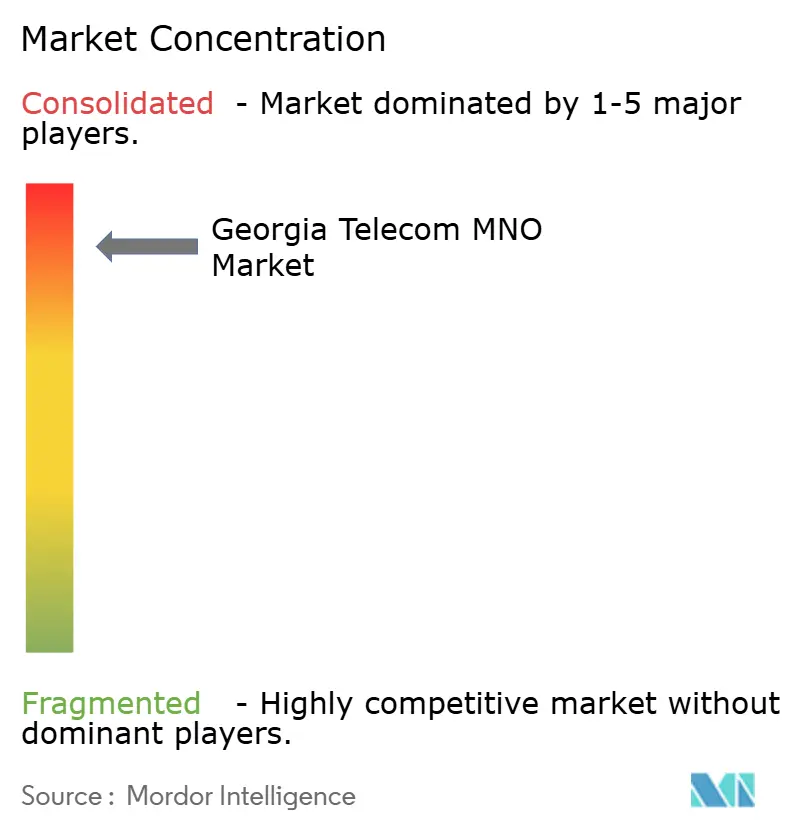

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Georgia Telecom MNO Market Analysis by Mordor Intelligence

The Georgia Telecom MNO Market size is estimated at USD 537.58 million in 2025, and is expected to reach USD 657.63 million by 2030, at a CAGR of 4.11% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 5.67 million subscribers in 2025 to 6.65 million subscribers by 2030, at a CAGR of 3.22% during the forecast period (2025-2030). The moderate growth pace reflects a mature yet still evolving ecosystem, where 4G saturation gives way to 5G-led upgrades, rising data-only packages, and the first commercial Internet of Things (IoT) deployments. Revenue momentum stems mainly from mobile broadband adoption, the country’s role as a digital bridge on the Middle Corridor trade route, and government-funded rural fiber backhaul, all of which cushion operators against headwinds such as currency volatility and limited population scale. Competition centers on three full-service carriers, including MagtiCom, Silknet (Geocell), and Cellfie, whose 5G and IoT strategies are redefining differentiation within the compact Georgian economy. Regulatory alignment with European Union standards, combined with investments in subsea and terrestrial cables, secures robust international connectivity that further strengthens the Georgia Telecom MNO market’s appeal to regional enterprises and transit traffic customers. [1]Georgia Technology Authority, “Georgia's Approach to Broadband,” GTA.GEORGIA.GOV

Key Report Takeaways

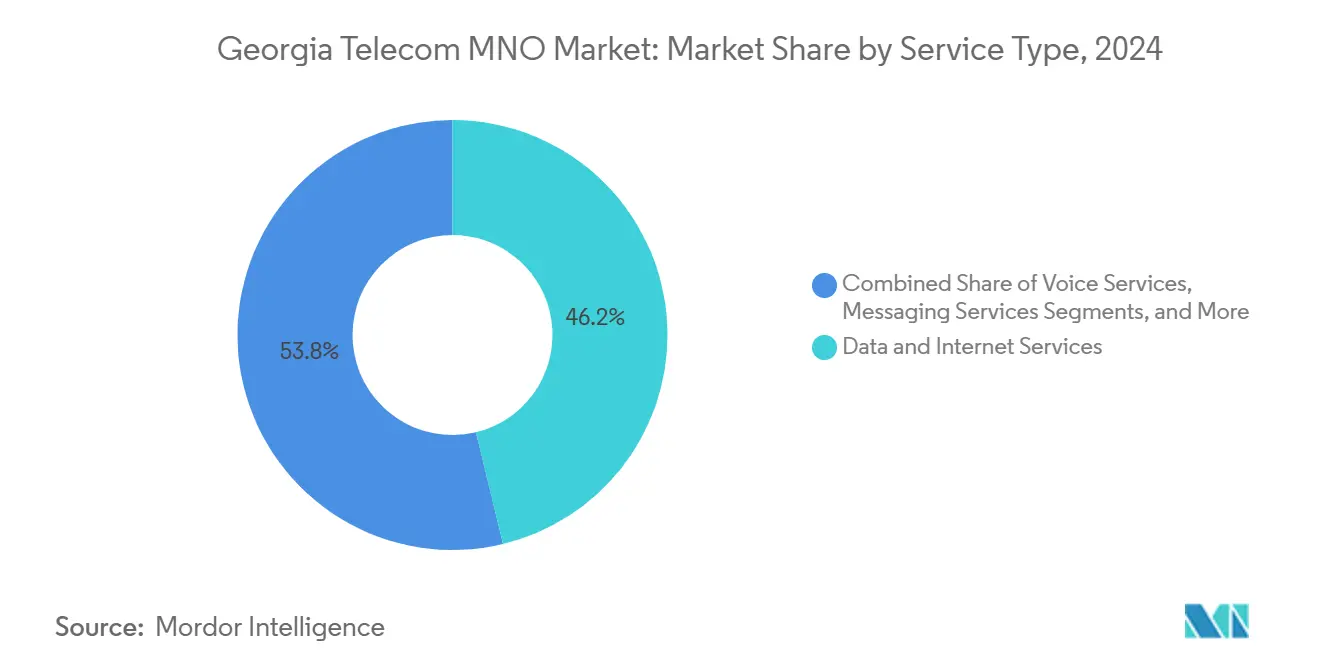

- By service type, data and internet services led the Georgia telecom MNO market with a 46.23% revenue share in 2024, while IoT and M2M are projected to advance at a 5.50% CAGR through 2030, the fastest among all offerings.

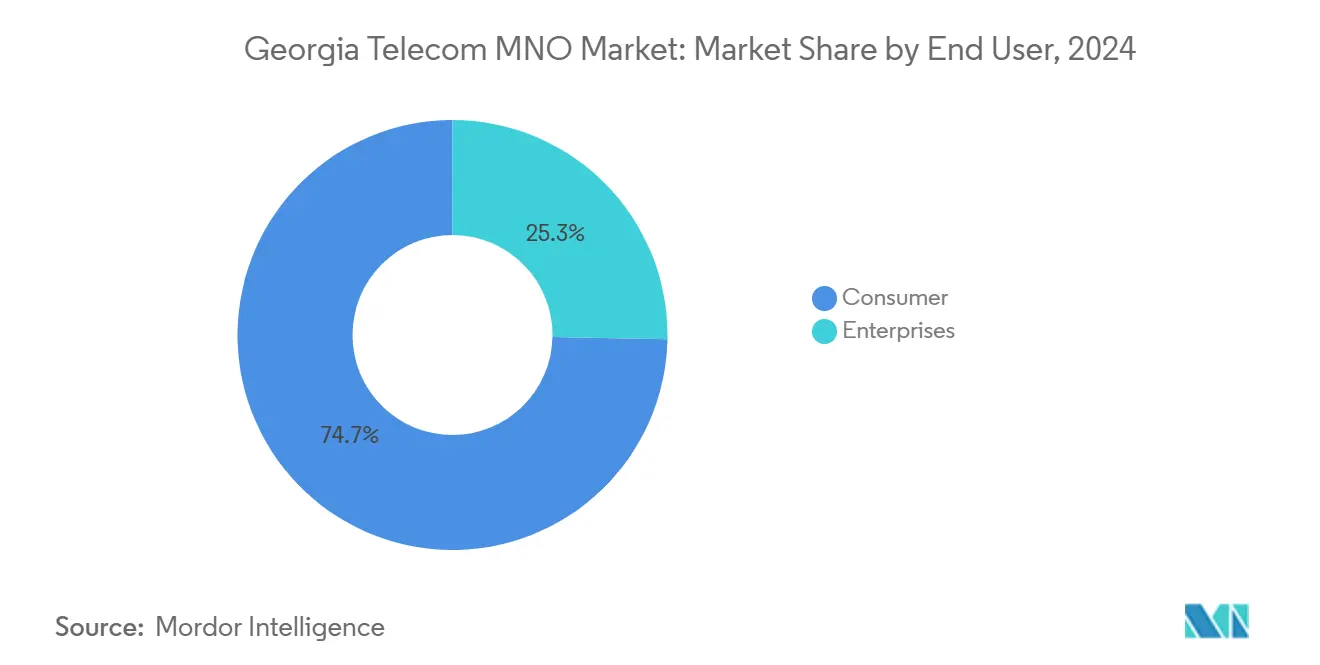

- By end user, the consumer segment captured 74.69% of the 2024 revenue; the enterprise segment is set to expand at a 4.52% CAGR to 2030, driven by logistics, mining, and energy modernization initiatives.

Georgia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Mobile Data Demand from OTT Video | +1.2% | Tbilisi and Batumi clusters | Short term (≤ 2 years) |

| 5G Spectrum Auction and Rollout Momentum | +0.8% | Urban and tourist districts | Medium term (2-4 years) |

| Government Universal-service Fiber Subsidies | +0.6% | Rural and underserved areas | Long term (≥ 4 years) |

| Growing Enterprise IoT Adoption (Logistics, Mining, Oil) | +0.5% | Industrial corridors | Medium term (2-4 years) |

| New Black-sea Subsea Cable Boosting Wholesale Backhaul | +0.3% | National with regional spillover | Long term (≥ 4 years) |

| Transit Roaming Growth Increases Fees, Profits for Georgian MNOs | +0.4% | National, with concentration along E60/E70 highway corridors and Tbilisi-Baku transit routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Mobile-Data Demand from OTT Video

Streaming consumption reshapes revenue composition as high-definition video traffic dominates peak-hour loads on all three networks. MagtiCom and Silknet each report seasonal congestion in Tbilisi and Batumi when 4K streams outstrip traditional capacity assumptions, prompting expedited fibre-to-tower upgrades and the migration of remaining 3G spectrum to 4G. Operators leverage the surge to upsell unlimited or premium-speed tiers that lift average revenue per user even as legacy voice usage declines. Content partnerships with regional platforms provide incremental wholesale bandwidth revenue and help curb piracy by tying subscriptions to mobile plans. The resulting virtuous cycle elevates data ARPU, validating continued investment in backhaul and caching infrastructure. [2]Speedtest, “Georgia's Mobile and Broadband Internet Speeds,” SPEEDTEST.NET

5G Spectrum Auction and Roll-out Momentum

The October 2024 commercial 5G launch marked a watershed, with MagtiCom first to market using EU-aligned equipment, closely followed by Cellfie on 703-708 MHz and 3550-3600 MHz bands. Early coverage focuses on airports, resort zones, and logistics hubs to capture international roamers and enterprise proof-of-concept trials. Lower latency and network slicing pilot programs are already enabling port-side automation at Poti and Batumi, underpinning broader ambitions to serve Middle Corridor freight flows. Despite limited domestic spending power, device subsidies and bundled video passes stimulate early consumer upgrades, while fixed-wireless access trials target rural households lacking fiber. [3]Cellfie, “5G,” CELLFIE.GE

Government Universal-Service Fiber Subsidies

Public subsidies totaling USD 408 million to reach 183,615 rural premises, lower backhaul costs for mobile operators, and unlock new addressable markets. The program’s “broadband as a utility” stance accelerates remote tower deployments across mountainous regions, enabling revenue diversification through fixed-wireless home broadband and boosting tourism offerings in wine-country villages. Shared infrastructure agreements reduce redundant capital expenditure, and a performance-based subsidy design ties funding to actual service adoption, safeguarding public returns. [4]Georgia Technology Authority, “Georgia's Approach to Broadband,” GTA.GEORGIA.GOV

Growing Enterprise IoT Adoption (Logistics, Mining, Oil)

Logistics firms exploiting Georgia’s east-west transit role account for the bulk of new IoT connections, deploying telematics to track rail wagons and cross-border trucks. Mining sites embed sensor networks for safety and predictive maintenance, while pipeline operators integrate remote leak-detection solutions. MNOs respond with dedicated NB-IoT and LTE-M tariffs, application programming interfaces, and managed service bundles, positioning themselves as end-to-end partners rather than simple connectivity resellers. Empirical studies in peer economies link a 10-percentage-point rise in IoT density to a 0.7% GDP uplift, a dynamic that local policy makers highlight in investment promotion campaigns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small Population Limits Scale Economics | -0.7% | Nationwide | Long term (≥ 4 years) |

| GEL Depreciation Inflates CAPEX Costs | -0.5% | Nationwide | Medium term (2-4 years) |

| Regulated Copper-loop Tariffs Drag Fixed ARPU | -0.3% | Legacy copper clusters | Long term (≥ 4 years) |

| Piracy Curbs PayTV Revenue Growth | -0.2% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Small Population Limits Scale Economics

A subscriber base of 3.7 million constrains economies of scale and stretches unit network costs. Tower sharing and vendor financing mitigate capital intensity, yet operators still face sub-optimal utilization compared with peers in Turkey or Poland. The dynamic is most acute for 5G where densification yields marginal revenue in low-density rural areas. To counterbalance, carriers pivot to wholesale transit and enterprise IoT where incremental traffic carries higher margins than mass-market mobile broadband. Investor presentations increasingly highlight these non-retail revenue streams as justification for sustained network modernization expenditure.

GEL Depreciation Inflates CapEx Costs

Network gear imported in USD or EUR exposes carriers to exchange-rate swings, with the Georgian Lari projected to average 2.86 per USD in 2025. Hedging instruments and vendor credit lines partially offset forex pressure, yet budget overruns still postpone non-essential upgrades such as small-cell roll-outs in secondary towns. Currency weakness equally inflates license fees denominated in hard currency, prompting staggered payment schedules and, in some cases, joint bids for future spectrum blocks. The economic reality forces a disciplined investment roadmap focused on high-return corridors and tourist districts where payback periods remain attractive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Growth

Data and internet services contributed 46.23% of 2024 revenue, anchoring the Georgia Telecom MNO market. Video streaming, cloud gaming, and mobile-first commerce combine to push average monthly usage beyond 10 GB per SIM, encouraging operators to price speed tiers rather than volume caps. The shift de-emphasizes legacy SMS and accelerates the decline of traditional voice, though rural adoption keeps circuit-switched minutes relevant. IoT and M2M, while currently a single-digit share, are forecast to expand at a 5.50% CAGR, supporting logistics tracking, smart metering, and industrial automation roll-outs that diversify operator income. OTT and Pay-TV bundling remains a nascent upsell avenue, yet piracy continues to cap premium uptake despite network-level content protection measures.

Diversification into roaming, wholesale backhaul, and enterprise managed services cushions carriers from retail price competition. The New Black Sea subsea link promises incremental traffic that leverages existing domestic transport grids, further improving the Georgia Telecom MNO market size outlook by 2030. Operators also explore mobile-edge computing pilots tied to 5G slicing to serve minimally latency-tolerant applications such as drone-assisted pipeline inspection, turning capacity investments into value-added service revenues.

By End-User: Consumer Dominance with Enterprise Acceleration

Consumer subscriptions generated 74.69% of 2024 turnover, affirming smartphones as an essential utility across demographics. Seasonal tourism uplift, especially during summer festivals and ski season, can raise active SIMs by double-digit percentages, underpinning promotional eSIM bundles priced down to USD 0.87 per GB that attract short-stay visitors and diaspora returnees. However, price elasticity remains high; MagtiCom discounts number-porting packages up to 50% to defend share, eroding margins on commoditized voice offerings.

Enterprise revenue, though smaller, is scaling faster at a 4.52% CAGR. Logistics firms digitize fleet operations, energy companies deploy remote monitoring, and government agencies integrate secure mobile broadband for public-safety communications. These specialized needs command multi-year service-level agreements that stabilize cash flows and support premium ARPU. As more industrial players align with the Middle Corridor freight renaissance, the Georgia Telecom MNO market share attributed to enterprises is expected to rise steadily through 2030, aided by bundled connectivity, analytics dashboards, and managed security options.

Geography Analysis

Urban concentration around Tbilisi, Kutaisi, and Batumi delivers efficient spectrum reuse and underpins the bulk of revenue, yet mountainous terrain covering two-thirds of the landmass complicates rural delivery. Universal-service fibre subsidies mitigate this gap by financing middle-mile links that mobile operators extend through microwave, fixed-wireless, and low-band 4G, materially improving coverage KPIs in Kakheti wine districts and remote ski resorts. These expansions encourage higher tourist dwell times and associated data consumption, reinforcing the Georgia Telecom MNO market’s cross-sectoral impact.

Internationally, Georgia positions itself as a gateway between Central Asia and Europe. The new 1,850 km EXA-SOCAR terrestrial route through Turkey adds redundancy to existing Black Sea cables, enhancing wholesale attractiveness and enabling competitive IP transit pricing that amplifies operator wholesale margins. Plans for a subsea power-and-data line linking South-Caucasus renewables to Romania may further elevate the Georgia Telecom MNO market size by attracting hyperscale data centers seeking multi-path resiliency.

Seasonal mobility shapes geographic traffic patterns: Batumi’s coastal strip and the Greater Caucasus resorts demand pop-up small cells during tourist peaks, while agrarian heartlands exhibit steady but low intensity usage. Operators segment networks accordingly, assigning 700 MHz low-band 5G for broad rural coverage and mid-band 3.5 GHz for urban capacity layers. Spectrum-sharing frameworks allow rural cell sites to repurpose bandwidth for fixed-wireless access during off-peak mobile periods, integrating universal-service objectives with commercial returns.

Competitive Landscape

The tri-opoly structure drives vigorous service innovation as each player seeks non-price avenues to outflank rivals. MagtiCom leverages early 5G first-mover status and extensive fibre footprint to pitch converged broadband offers that bundle mobile, TV, and fixed voice. Silknet, fortified by its USD 151.7 million Geocell acquisition, markets whole-home Wi-Fi and premium video packs to defend family-segment loyalty. Cellfie positions itself as a digital-native challenger, highlighting Nokia-powered network excellence and aggressive data allowances for price-sensitive users while investing in narrow-band IoT gateways for industrial clients.

Strategic collaborations broaden addressable revenue. MagtiCom and Silknet each hold capacity swaps on Caucasus Cable Systems, lowering international transit costs, while Cellfie explores tower-sharing deals to trim rural roll-out CapEx. All three develop mobile money wallets and loyalty apps to deepen customer engagement and monetize transaction fees. The anticipated 2026 spectrum tender could reshape competitive dynamics if a foreign entrant or wholesale-only player emerges, yet high upfront license fees and limited population scale cut the odds of sustainable four-player competition.

Operators intensify enterprise focus by offering managed SD-WAN, private LTE campuses, and cyber-security add-ons, targeting logistics hubs at Poti port, the Baku–Tbilisi–Kars rail corridor, and pipeline facilities. Cross-border 5G roaming arrangements with Turkish and Azerbaijani carriers further enhance the service proposition for freight companies traversing Georgia. Vendor ecosystem partnerships with Ericsson, Huawei (legacy), and Nokia underpin network modernization, while open-radio-access-network pilots seek future cost savings.

Georgia Telecom MNO Industry Leaders

MagtiCom LLC

Silknet JSC

Cellfie Mobile LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: More than 135 international eSIM providers launched tourist-focused data plans in Georgia, with entry pricing of USD 0.87 per GB, amplifying competition for short-stay visitor spend.

- January 2025: MagtiCom experienced a nationwide mobile and fixed network outage after infrastructure damage in Turkey and sabotage at three Georgian sites; services were fully restored by 28 January following emergency repairs and police investigation.

- July 2024: EXA Infrastructure partnered with SOCAR Fiber to build a 1,850 km terrestrial fiber route from Greece to Georgia, enhancing regional path diversity for Black Sea connectivity.

Georgia Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Georgia Telecom MNO market?

The Georgia Telecom MNO market size is USD 537.58 million in 2025.

How fast is the market expected to grow?

Revenue is projected to reach USD 657.63 million by 2030, implying a 4.11% CAGR over the forecast period.

Which service type generates the most revenue?

Data and internet services hold the largest slice at 46.23% of 2024 revenue.

Who are the main mobile network operators in Georgia?

MagtiCom, Silknet (Geocell) and Cellfie account for the entire nationwide subscriber base.

Why is enterprise IoT important for operators?

Industrial IoT connections in logistics, mining and energy are forecast to grow at 5.50% CAGR, delivering higher-margin revenue and diversifying income sources.

How will 5G influence market dynamics?

5G roll-outs in key cities and tourist sites improve network capacity, enable low-latency enterprise applications and reinforce Georgia’s transit-hub positioning, supporting steady market expansion.

Page last updated on: