Japan Tire Manufacturing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

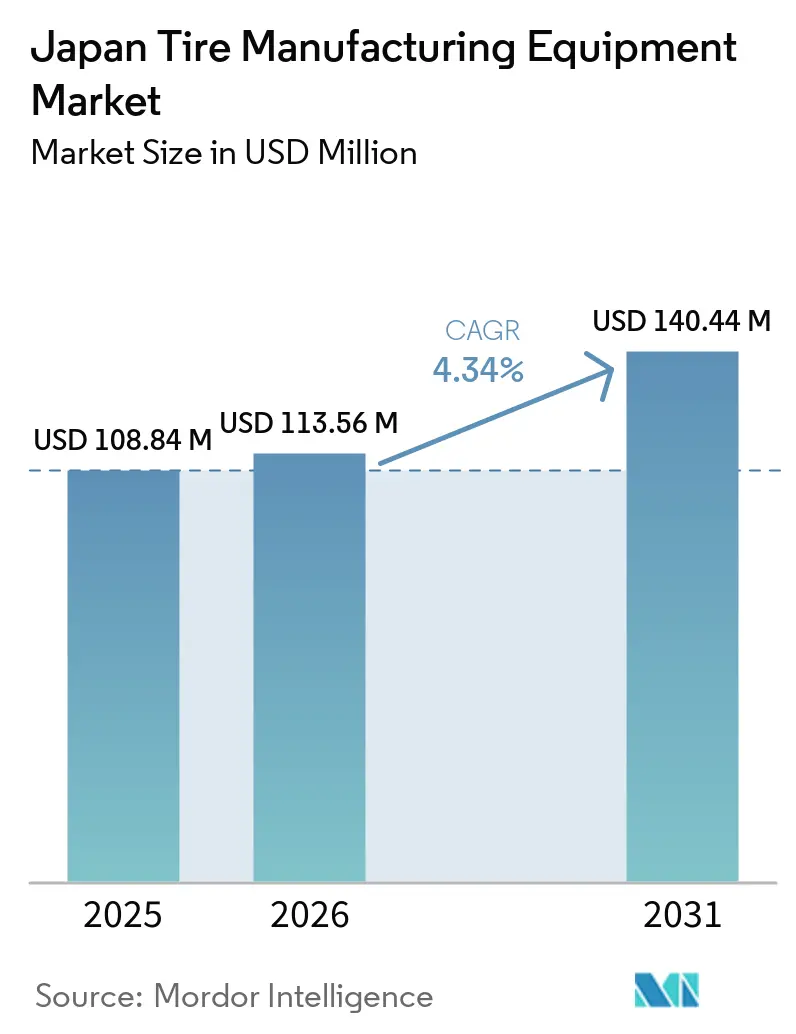

| Base Year Market Size (2025) | USD 108.84 Million |

| Market Size (2026) | USD 113.56 Million |

| Market Size (2031) | USD 140.44 Million |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Tire Manufacturing Equipment Market Analysis by Mordor Intelligence

The Japanese tire manufacturing equipment market size is projected to expand from USD 108.84 million in 2025 and USD 113.56 million in 2026 to USD 140.44 million by 2031, registering a CAGR of 4.34% between 2026 and 2031. Domestic shifts towards electric vehicles (EVs) and high-performance tires are fueling momentum, emphasizing the need for tighter dimensional tolerances, reduced rolling resistance, and integrated sensor capabilities. Rather than establishing new factories, Japanese manufacturers are modernizing older production lines with Industry 4.0 controls, energy-efficient hydraulics, and automated inspection systems, maximizing value from their current setups. For instance, Bridgestone is implementing its ENLITEN compound technology and Bridgestone Common Modular Architecture (BCMA) in several of its older passenger-car plants, highlighting a trend of prioritizing incremental upgrades over new constructions.

Key Report Takeaways

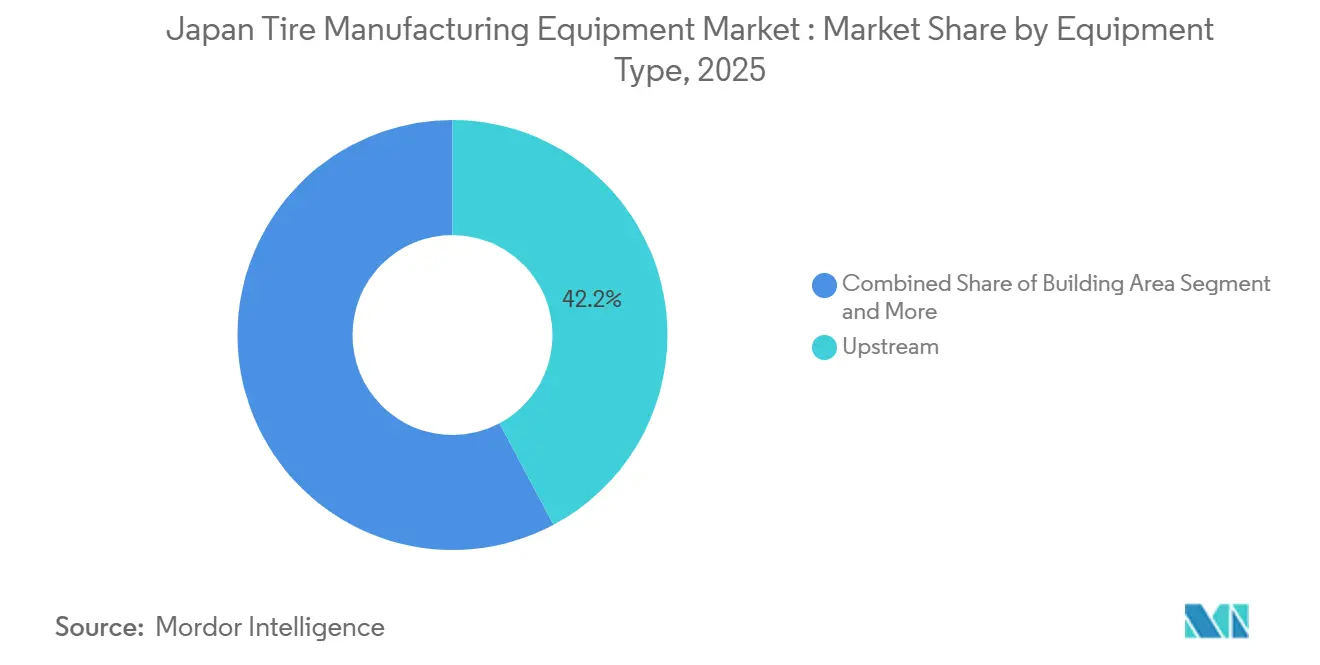

- By equipment type, upstream machinery accounted for 42.21% of the Japanese tire manufacturing equipment market share in 2025, while curing and inspection equipment is projected to advance at a 6.22% CAGR through 2031.

- By tire design, radial technology dominated the Japanese tire manufacturing equipment market in 2025, with a 89.22% share, and is expected to grow at a 6.39% CAGR through 2031.

- By vehicle type, passenger-car tire lines led the Japanese tire manufacturing equipment market with 48.65% share in 2025, while off-road vehicles are expected to be the fastest-growing sub-sector with a 7.21% CAGR through 2031.

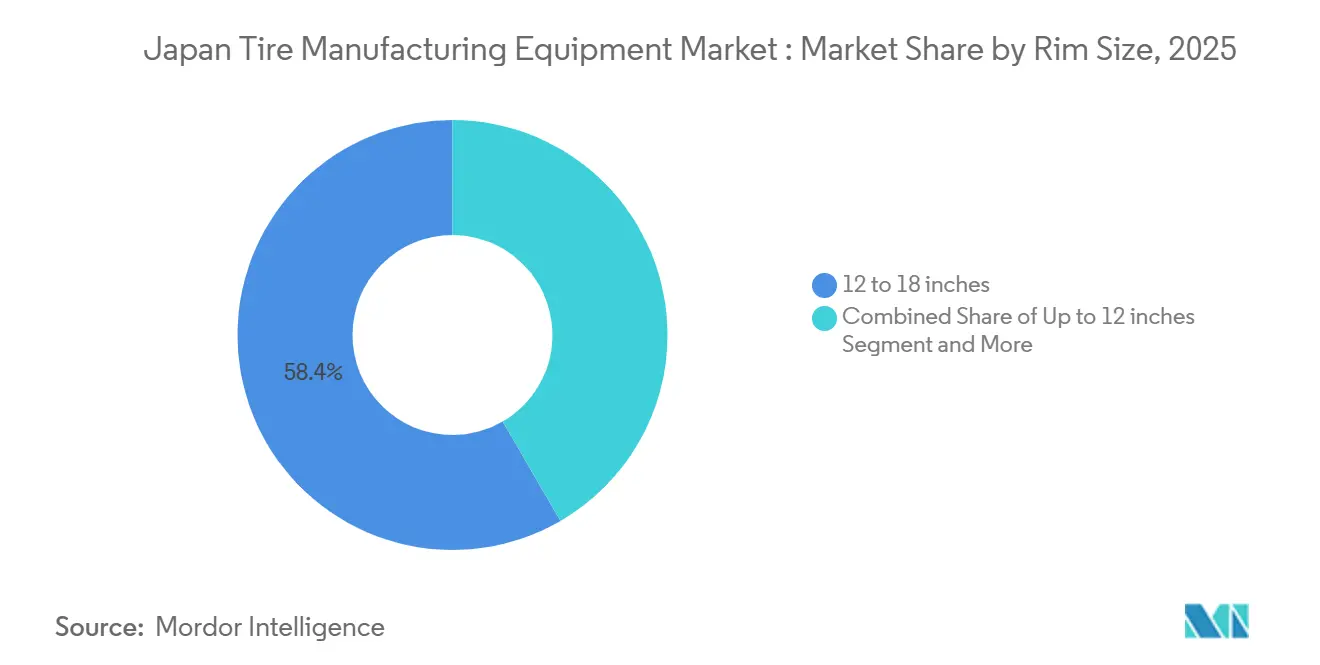

- By rim size, the 12-to-18-inch segment captured 58.37% of the Japanese tire manufacturing equipment market in 2025, yet equipment for above-18-inch rims is slated to advance at 7.89% CAGR through 2031 as SUVs and premium EVs proliferate.

- By end user, original equipment manufacturers accounted for 61.27% of the Japanese tire manufacturing equipment market share in 2025. Still, replacement and aftermarket buyers are projected to grow faster at a 6.82% CAGR through 2031, as aging domestic vehicles necessitate steady tire replacement.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Japan includes both locally based firms and those operating across multiple regions. The market landscape in the global tire manufacturing equipment industry research shows how these players are arranged internationally.

Japan Tire Manufacturing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 Automation in Japan | +1.2% | National, concentrated in major manufacturing hubs | Long term (≥ 4 years) |

| Demand for Fuel-Efficient, High-Performance Tires | +1.5% | Japan, with spillover to Asia-Pacific export markets | Medium term (2-4 years) |

| Modular EV/AV Tire Customization Equipment | +1.1% | Japan, with technology export potential | Medium term (2-4 years) |

| Novel Mixing Tech for Sustainable Rubber Blends | +0.9% | Japan, with global technology licensing opportunities | Long term (≥ 4 years) |

| Capacity Expansions by Major Japanese Tire Makers | +0.8% | Japan domestic, with strategic overseas implications | Short term (≤ 2 years) |

| Government Subsidies for Energy-Efficient Machinery | +0.6% | National, with regional manufacturing clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Fuel-Efficient, High-Performance Tires

Tires for electric and hybrid vehicles must balance low rolling resistance with higher load ratings. This need pushes manufacturers to adopt silica-rich treads and maintain calendering tolerances. Bridgestone’s ENLITEN compound showcases this industry shift, necessitating co-extrusion heads to manage durometer variance across tread layers [1]“ENLITEN—The New Premium in the EV Era,” Bridgestone Corporation, bridgestone.com. Meanwhile, Yokohama Rubber is investing in a motorsports line to boost capacity. This expansion highlights the growing demand for precision curing presses. Tires tailored for EVs now feature sensor pockets for RFID chips and tire-pressure monitoring. These innovations not only enhance vehicle performance but also extend replacement cycles for traditional building and cutting machines. In response, equipment suppliers are rolling out advanced tools like laser-guided bias cutters and servo-driven tread extruders, both boasting micron-level accuracy. Additionally, pilot-produced bio-based sulfur copolymers are achieving a reduction in rolling resistance. However, these copolymers modify cure kinetics, necessitating upgrades to mixers for lower-temperature processing to prevent scorching.

Automation and Industry 4.0 Adoption in Japanese Tire Plants

Sumitomo Rubber deployed a Hitachi–PTC manufacturing execution system (MES) at its Shirakawa facility. This system aggregates live data from mixers, extruders, builders, and presses, leading to a significant reduction in unplanned downtime[2]“Sumitomo Rubber Adopts Hitachi & PTC MES Platform,” Sumitomo Rubber Industries, srigroup.co.jp. Bridgestone's BCMA module further enhances efficiency, cutting changeover time substantially. This allows a single building machine to seamlessly switch between SKUs without manual drum changes. Kobe Steel is promoting bolt-on IoT sensor kits that transmit data on torque, viscosity, and temperature to cloud-based AI dashboards. These digitally optimized cycles have already achieved notable energy savings per mixing batch. While new machines come equipped with embedded sensors, a large portion of Japan's existing machines were installed earlier, presenting a significant retrofit opportunity. Financing options are becoming more accessible, especially with METI subsidies covering a portion of qualifying energy-efficient equipment. This support has significantly shortened the payback period.

Flexible Modular Equipment for EV/AV Tire Customization

As autonomous vehicles approach a longer service life, the demand for enhanced durability and noise reduction intensifies. HF Group has introduced reconfigurable tire builders, which are now being shipped to customers in Japan. These builders facilitate swift module swaps for bead setting and ply application, slashing changeover times from hours to mere minutes. Bridgestone, in collaboration with Einride, is embedding telematics-grade sensors into smart truck tires right at the point of manufacture. This innovation has enabled the integration of RFID readers and conductive pathways into presses, while maintaining uniform curing. While modular equipment comes with a price premium, it mitigates the risk of stranded assets amidst evolving EV specifications. Additionally, early adopters are experimenting with 3D-printed molds, reducing lead times and enabling quick iterations on tread designs tailored for quieter electric drive trains.

Capacity-Expansion Programs by Leading OEMs

Bridgestone has made a significant move in the tire industry, investing heavily in premium passenger tires and ultra-large off-the-road (OTR) tires. This marks Japan's largest single-company investment in recent years. While neither project increases overall tire tonnage, both focus on enhancing product quality and safety, and on integrating advanced embedded-sensor capabilities. Meanwhile, Toyo Tires is set to invest in a new truck-and-bus radial (TBR) plant, complete with cutting-edge production lines. This strategic roadmap underscores a robust demand for large-diameter builders and automated X-ray inspection units. Given that most projects are retrofitting existing facilities in locations like Hikone, Tosu, Tochigi, Kitakyushu, and Mishima, suppliers adept at maneuvering equipment, such as modular presses, stackable extruders, and compact bead winders, through these constrained spaces are poised to gain a strategic edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Long Payback for Machinery | -0.7% | Japan, with implications for equipment financing | Medium term (2-4 years) |

| Raw Material Price Swings | -0.5% | Japan, influenced by global commodity markets | Short term (≤ 2 years) |

| Factory Space Limits | -0.4% | Japan, concentrated in established manufacturing regions | Long term (≥ 4 years) |

| Slow METI Approvals | -0.3% | National, affecting international equipment suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Long Payback Period for Curing Presses

In Japan, a modern hydraulic curing press equipped with RFID tagging comes with a high price tag. When installation is factored in, costs rise further. Mid-sized firms grapple with extended payback horizons. This duration not only surpasses standard financing tenors but also inches perilously close to the timelines for technological obsolescence. While leasing models are available, they remain a rarity in Japan. This is largely due to a prevailing preference for outright ownership, championed by both suppliers and accountants. As a result, larger OEMs capitalize on this landscape, placing multi-press orders to secure volume discounts.

In contrast, smaller producers find themselves in a bind, delaying replacements and extending the life of their older presses through third-party service contracts. This pronounced divergence in approach dampens immediate demand for new presses. However, it simultaneously amplifies interest in sensor-retrofit kits, predictive-maintenance software, and partial hydraulic upgrades.

Raw-Material Cost Volatility Squeezing Equipment Budgets

As output declines in key producing countries, natural rubber spot prices are projected to rise, surpassing previous levels. In contrast, synthetic rubber and carbon black prices closely track crude oil fluctuations, with significant quarterly swings. For tire manufacturers, an increase in rubber prices results in a substantial diversion of cash flow, funds that could have been allocated to machinery investments. In response, manufacturers are shifting their focus towards mixers and extruders that enhance compound yield and minimize scrap. They're postponing investments in expensive building and curing systems, as the return on investment for these is more closely linked to product quality than immediate material savings. Meanwhile, suppliers are attempting to cushion the impact through deferred payments and performance-based contracts tied to energy-saving benchmarks. However, these arrangements come with higher monitoring costs and greater complexity in managing receivables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Upstream Dominance Drives Precision Manufacturing

In 2025, upstream mixing and preparation assets accounted for 42.21% of the Japanese tire manufacturing equipment market. This dominance underscores the surging demand for precise compound control, especially as electric vehicle (EV) tires become increasingly mainstream. Projects in Japan's tire manufacturing equipment market are now integrating recycled fillers and bio-polymers into mixing lines, all while ensuring batch uniformity. Suppliers are also adopting torque analytics and automated feed hoppers, crucial for maintaining the consistent viscosity needed in low-rolling-resistance treads.

Systems for cutting and inspection are projected to expand at a 6.21% CAGR through 2031, outpacing all other categories. This growth is driven by camera-guided knife stations, X-ray tread scanners, and AI-driven defect classifiers, especially as OEMs enforce zero-defect standards for tires in autonomous vehicles. Additionally, portable smart sensors are being retrofitted onto legacy drums, enabling plants to gather predictive maintenance data without replacing older equipment. This capability is particularly appealing for shops with limited space.

By Tire Design: Radial Technology Maintains Market Leadership

Radial-tire technology commanded 89.22% of the Japanese tire manufacturing equipment market in 2025 and is expected to grow at a 6.39% CAGR through 2031, keeping the Japanese tire manufacturing equipment market firmly aligned with global radially-skewed automotive production. Servo-driven belt applicators now ensure the 90-degree cord angle remains within a minimal margin by monitoring tension in real-time. This precision is crucial for meeting OEM-specified rolling resistance metrics.

Holding a notable market share, the bias-tire gear caters to specialty farm, construction, and two-wheeler segments, with exports primarily directed to Southeast Asia. While growth remains modest due to limited unit volumes, Japanese manufacturers like Kawata Engineering find profitability by exporting compact bias cutters, priced significantly lower than their radial counterparts. Although national sustainability regulations target energy-intensive bias curing, potentially stifling future investments, a transitional demand endures as emerging markets gradually shift towards radial adoption.

By Vehicle Type: Passenger Cars Lead While Off-Road Vehicles Accelerate

The passenger car segment accounted for 48.65% of the 2025 market share in the Japanese tire manufacturing equipment market. Uniform building accuracy below 1 mm and RFID-embedded modules are now standard, reflecting OEM agreements with Toyota, Nissan, and Honda. Tooling sets automatically adjust across drum widths for specific SKUs, boosting throughput without manual resets.

The off-road vehicles segment is expected to grow at a 7.21% CAGR, buoyed by a recovery in construction and mining. Japan's OTR tire manufacturing equipment market is poised for significant growth in the coming years. With each OTR builder priced so high, even modest sales volumes have a notable impact on overall revenue. Meanwhile, machines for medium and heavy commercial vehicles, bolstered by Toyo's upcoming TBR plant, are experiencing steady growth, positioning them between the two extremes.

By Rim Size: Mid-Range Dominance with Premium Growth

The 12-to-18-inch band accounted for 58.37% of the revenue share in 2025. Its dominance stems from its broad utility across mass-market sedans and last-mile vans, allowing one press to accommodate dozens of SKUs. Yet sales tick upward only mildly, in line with replacement cycles of Japan’s aging car parc.

Above-18-inch equipment, by contrast, is poised to accelerate at a 7.89% CAGR through 2031. Premium electric vehicles (EVs) and SUVs are now opting for larger wheels. These larger tires come with a significant price premium compared to their smaller counterparts. This price difference has led to wider profit margins, justifying higher capital costs for presses. For example, Yokohama’s Mishima motorsports line is focusing on larger molds, featuring asymmetric patterns designed for enhanced lateral grip. This strategic shift has consequential effects on upstream processes, particularly in bead-winder and tread-extraction modules.

By End-User: OEM Leadership with Aftermarket Acceleration

The OEM segment accounted for 61.27% share of the Japanese tire manufacturing equipment market in 2025 as automakers refresh hybrid and EV lineups. Because each tire must trace back to a build batch, factories are buying MES-integrated presses that print QR codes at cure, ensuring cradle-to-grave traceability under ISO 9001:2015.

The replacement/aftermarket segment is expected to expand at a faster rate, at a 6.82% CAGR through 2031, as domestic vehicles age past 8.7 years. Smaller plants opt for refurbished presses, spending a fraction of the cost of new units. They complement these with cloud-based analytics, maximizing uptime from older equipment. Suppliers in Japan's tire manufacturing equipment industry now offer simplified building machines priced significantly lower than OEM-grade equivalents, replacing servo modules with mechanical drives while still accommodating bolt-on IoT kits when subsidy opportunities arise.

Geography Analysis

Japanese tire production and, therefore, equipment demand cluster in three industrial belts that track historic auto assembly hubs. The Kanto corridor hosts Bridgestone’s Tochigi plant and numerous component suppliers, keeping delivery radii tight and enabling just-in-time logistics that minimize buffer inventories. The Chubu belt intertwines Yokohama’s Mishima complex with Toyota’s Nagoya ecosystem. At the same time, the Kyushu region houses Bridgestone’s Tosu and Kitakyushu facilities, as well as an emergent EV supply chain anchored by battery and semiconductor fabs.

A retrofit-over-relocation mentality dominates these mature zones because brownfield permits are simpler to obtain than greenfield approvals inside environmentally sensitive coastal prefectures. Skilled labor also concentrates here; many operators boast 20-plus years of experience calibrating bead winders and setting cure profiles, tacit know-how that would take years to replicate elsewhere. Space scarcity pushes equipment makers toward compact, vertically stacked extruders and servo-hydraulic presses that can squeeze into legacy bay widths.

Export dynamics operate in the opposite direction. Kobe Steel ships mixers to Thailand, Indonesia, and Vietnam, leveraging Japanese process credentials to penetrate rapidly expanding plants serving ASEAN auto hubs. European specialists such as VMI Holland install modular builders in Japan to secure OEM mandates. Yet, they still face METI conformity testing delays that extend lead times by up to one month. Chinese vendors are gaining share only in price-sensitive segments, mainly replacement-tire lines, because their 20-30% capital-cost advantage evaporates once subsidy-linked energy audits, customs delays, and after-sale service gaps are factored in.

Mordor Intelligence tracks the tire manufacturing equipment market across other major regions such as Europe, with additional country-level coverage spanning China, South Korea, and United States, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The top suppliers, Kobe Steel, Mitsubishi Heavy Industries, VMI Holland, HF Mixing Group, and Mesnac, collectively control a significant portion of the market, highlighting a moderately concentrated field. Japanese players, leveraging vertical integration and robust domestic service networks, fortify their market positions. For instance, Kobe Steel integrates mixers with its proprietary steel-cord output, while Mitsubishi markets both presses and hydraulic drives. Meanwhile, European competitors emphasize modular design and energy efficiency. Notably, HF Group touts a substantial reduction in electricity consumption per tire compared to its baseline.

Chinese contenders Mesnac and Guilin Rubber Machinery aggressively price their offerings below those of established players, targeting mid-tier clients with attractive bundled financing options through Japanese trading partners. However, their inability to provide pre-certified energy data delays METI approvals and hinders their entry into OEM lines. Additionally, new-age software vendors are disrupting the landscape by introducing MES and digital twin platforms that seamlessly integrate multi-brand equipment, challenging the dominance of traditional, proprietary control systems.

Today's strategic focus is on retrofit kits, AI-driven process controls, and service contracts to ensure long-term parts supply. Kobe Steel is already reaping benefits from its sensor-upgrade initiative, boosting software revenue streams. Concurrently, VMI is testing 3-D-printed mold services, significantly reducing prototyping durations. On the client front, industry giants Bridgestone, Toyo Tires, Sumitomo, and Yokohama are not only steering market volumes but also pivoting towards smaller EV tire batches and eco-friendly compounds, reshaping performance standards across the board [3]“Toyo Tires Announces Mid-Term Plan,” Japan Rubber Weekly, japanrubberweekly.com.

Japan Tire Manufacturing Equipment Industry Leaders

Kobe Steel Ltd.

Mitsubishi Heavy Industries

HF Mixing Group

VMI Holland B.V.

Mesnac Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Toyo Tires unveiled a bold capex initiative, channeling funds into next-gen production systems and expanding its truck-and-bus radial offerings, a move that doubles its prior budget. This development is expected to significantly impact the tire equipment market by driving demand for advanced manufacturing technologies and machinery.

- February 2025: Bridgestone Corporation (Bridgestone) has announced its intention to establish a pilot demonstration plant in Seki City, located in Gifu Prefecture, Japan. This facility will specialize in the precise pyrolysis of end-of-life tires, aiming to extract tire-derived oil and recycled carbon black. This development is expected to influence the tire equipment market by driving advancements in chemical recycling technology and promoting sustainable practices within the industry.

Japan Tire Manufacturing Equipment Market Report Scope

The Japan tire manufacturing equipment market report is segmented by equipment type (upstream, building area, and curing & inspection), tire design (bias and radial), vehicle type (two-wheelers, three-wheelers, passenger cars, light commercial vehicles, medium & heavy commercial vehicles, and off-road vehicles), rim size (up to 12 inches, 12 to 18 inches, and above 18 inches), and end-user (original equipment manufacturers (OEMs) and replacement/aftermarket). The market forecasts are provided in terms of value (USD).

| Upstream (Mixer & Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | |

| Extrusion Machines | |

| Cutting Machines | |

| Others (Cooling Units, etc.) | |

| Building Area | Bead Winding Machine |

| Tire Building Machine | |

| Others (Strip Winding Machine, etc.) | |

| Curing & Inspection (Testing Area) | Curing Press Machines |

| Tire Painting Machines | |

| Others (Inspection Machines, etc.) |

| Bias |

| Radial |

| Two-wheelers |

| Three-wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Off-Road Vehicles |

| Up to 12 inches |

| 12 to 18 inches |

| Above 18 inches |

| Original Equipment Manufacturers (OEMs) |

| Replacement / Aftermarket |

| By Equipment Type | Upstream (Mixer & Component Preparation) | Mixing Machines / Rubber Mixers |

| Calendaring Machines | ||

| Extrusion Machines | ||

| Cutting Machines | ||

| Others (Cooling Units, etc.) | ||

| Building Area | Bead Winding Machine | |

| Tire Building Machine | ||

| Others (Strip Winding Machine, etc.) | ||

| Curing & Inspection (Testing Area) | Curing Press Machines | |

| Tire Painting Machines | ||

| Others (Inspection Machines, etc.) | ||

| By Tire Design | Bias | |

| Radial | ||

| By Vehicle Type | Two-wheelers | |

| Three-wheelers | ||

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| Off-Road Vehicles | ||

| By Rim Size | Up to 12 inches | |

| 12 to 18 inches | ||

| Above 18 inches | ||

| By End-User | Original Equipment Manufacturers (OEMs) | |

| Replacement / Aftermarket | ||

Key Questions Answered in the Report

What is the projected CAGR for Japan’s tire-manufacturing equipment through 2031?

The compound annual growth rate is forecast at 4.34% between 2026 and 2031.

Which equipment segment is expanding most rapidly?

Curing and automated-inspection systems are advancing at a 6.22% CAGR, outpacing upstream and building-area machinery.

What share do radial-tire machines hold in current equipment demand?

Radial-construction equipment commanded 89.22% of 2025 revenue and continues to grow at a 6.39% pace.

Why is the aftermarket buyer segment growing faster than OEM demand?

Japan’s aging vehicle fleet and small tire shops’ preference for low-cost retrofit kits are accelerating aftermarket equipment purchases at a 6.82% CAGR.

What drives demand for above-18-inch rim equipment?

Rising sales of premium and performance vehicles require larger, specialized tires that push equipment orders in this rim class

Page last updated on: