Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 62.99 Billion |

| Market Size (2026) | USD 64.56 Billion |

| Market Size (2031) | USD 73.66 Billion |

| Growth Rate (2026 - 2031) | 2.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Facility Management Market Analysis by Mordor Intelligence

The Japan Facility Management Market size is expected to grow from USD 62.99 billion in 2025 to USD 64.56 billion in 2026 and is forecast to reach USD 73.66 billion by 2031 at 2.5% CAGR over 2026-2031. A maturing demand base, persistent labor shortages, and higher input costs are slowing topline expansion, yet structural reforms are nudging the industry toward technology-enabled service integration, seismic retrofitting programs, and mandatory energy-efficiency upgrades. Hard Services retained dominance, but Soft Services are outpacing the overall market as occupiers raise expectations for hospitality-style amenities, workplace wellness, and data-driven quality control. Outsourced contracts continue to gain traction because clients wish to transfer operational risk, comply with stricter ESG disclosure rules, and access specialized skillsets without capital outlay, especially as record construction-material inflation of 32-35% since 2021 squeezes internal budgets. Competitive intensity is escalating as legacy providers consolidate to defend scale while technology-first entrants leverage IoT sensors, AI-powered analytics, and mobile work order platforms to reduce site visits and combat workforce constraints. These intertwined forces keep the Japan facility management market on a deliberate but unmistakably modernizing path.

Key Report Takeaways

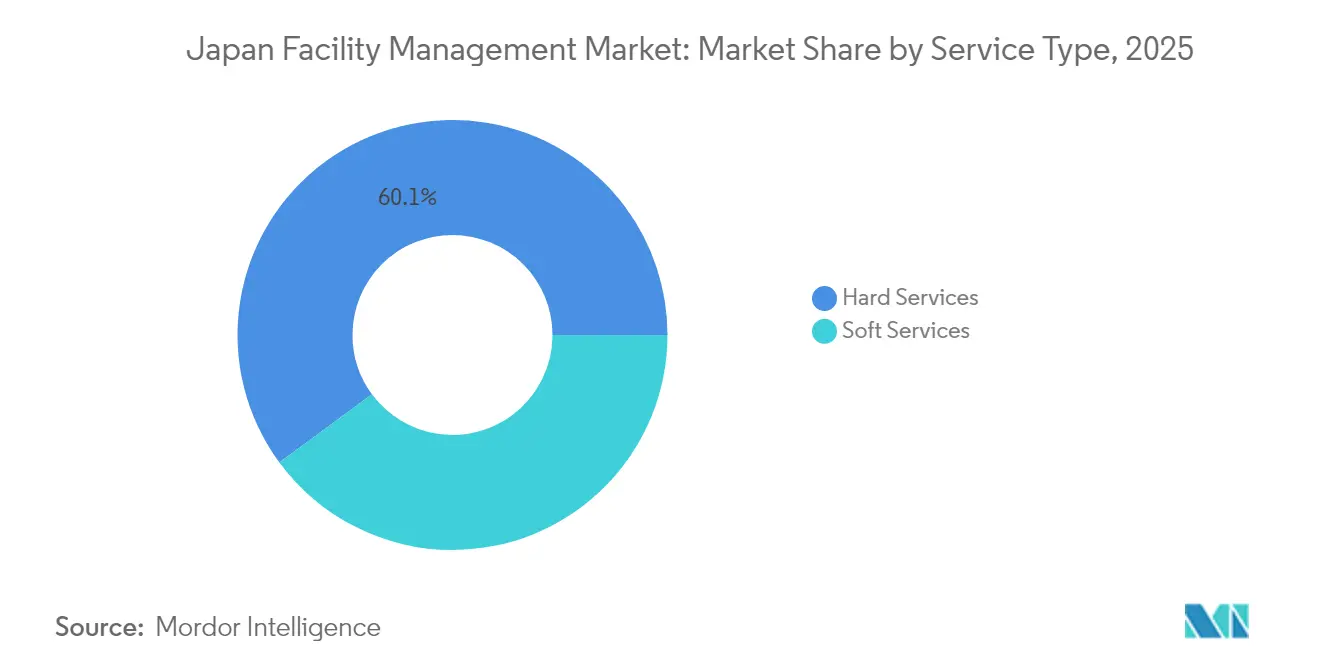

- By service type, Hard Services captured 60.10% of the Japan facility management market share in 2025, while Soft Services are forecast to advance at a 4.72% CAGR to 2031.

- By offering, outsourced models held 67.60% of the Japan facility management market size in 2025 and are expanding at a 4.12% CAGR through 2031.

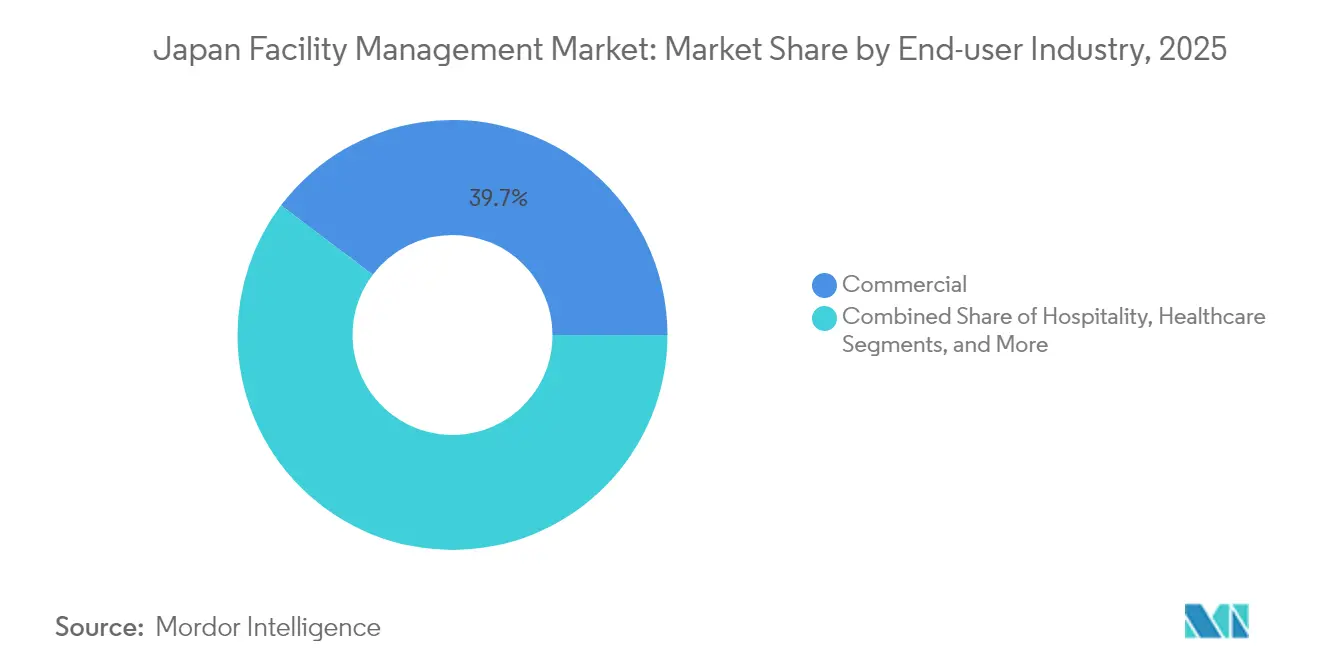

- By end-user industry, commercial facilities led with 39.70% revenue share in 2025; industrial and process sites record the fastest growth at a 4.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanisation and population growth in major metros | +0.8% | Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Profitability rates of major FM players | +0.6% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Current occupancy rates | +0.4% | Commercial districts in major cities | Short term (≤ 2 years) |

| Regulatory drivers specific to labour and safety standards | +0.5% | National implementation | Long term (≥ 4 years) |

| Growth in outsourcing to Integrated FM contracts | +0.7% | National, early adoption in Tokyo region | Medium term (2-4 years) |

| Aging building stock driving seismic and sustainability retrofits | +0.9% | National, priority in earthquake-prone areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanisation and Population Growth in Major Metros

Rapid metropolitan concentration is swelling service volumes and complexity across the Japan facility management market as rural depopulation funnels residents and businesses into Tokyo, Osaka, and Nagoya. Commercial real-estate investment in Tokyo alone exceeded JPY 4 trillion in 2025, prompting landlords to upgrade office stock with smart-building infrastructure, wellness amenities, and flexible layouts that raise the operational bar for facility managers. [1]Japan Mobility, “2025 Market Trends and Predictions,” japan-mobility.com Dense portfolios let providers deploy standardized IoT-enabled building systems and AI-driven predictive maintenance tools across clusters, extracting data-led efficiencies while meeting higher occupant expectations. Urban campuses are thus becoming living laboratories where scalable, technology-rich models are refined before wider rollout. This dynamic, in turn, accelerates consolidation as firms chase critical mass to serve multi-site contracts while absorbing escalating compliance and ESG reporting obligations. Cumulatively, metropolitan growth adds 0.8 percentage points to forecast CAGR, underscoring its pivotal role in sustaining the Japan facility management market.

Aging Building Stock Driving Seismic and Sustainability Retrofits

Roughly 65% of Japan’s office inventory now exceeds 20 years of age, pushing owners toward simultaneous seismic reinforcement and decarbonization projects to comply with the amended Building Energy Efficiency Act and achieve net-zero emissions by 2050. [2]ITmedia, “Breaking the Myth of Costly Energy Retrofits,” itmedia.co.jp Facility management contracts increasingly bundle long-horizon retrofitting oversight, energy-performance monitoring, and tenant liaison into integrated offerings. Providers that command both structural engineering know-how and energy-analytic capability are winning multi-year engagements to safeguard asset value while ensuring operational continuity. Client appetite for turnkey coordination—from design consultation through commissioning and ongoing performance verification—magnifies the role of data governance and remote monitoring. As these opportunities widen, aging stock contributes the single-largest positive lift (+0.9%) to the Japan facility management market CAGR.

Growth in Outsourcing to Integrated FM Contracts

Integrated FM (IFM) agreements are supplanting fragmented single-service deals because occupants prefer consistent service levels, unified reporting, and cost transparency. Japan Kanzai Holdings, for example, controls 46% of public-facility IFM assignments, demonstrating the consolidation headroom created by economies of scale. Clients transferring risk to external partners gain access to specialized digital platforms for work-order automation, energy benchmarking, and compliance dashboards. Providers reap route-density efficiencies and can cross-train staff to mitigate acute labor shortages. IFM thus adds 0.7 percentage points to sector CAGR and helps stabilize margins amid rising wage bills.

Regulatory Drivers Specific to Labour and Safety Standards

A tightening regulatory net—from mandatory workplace-accessibility upgrades under the Disabilities Discrimination Act (April 2024) to more stringent IAQ, water-safety, and cleaning protocols under the Building Sanitation Law—is reshaping baseline service scopes. Larger providers are investing in compliance management systems, staff certification programs, and digital audit trails to satisfy inspection regimes while containing overhead. Smaller incumbents, lacking such resources, risk displacement or acquisition as regulatory complexity pushes them toward capital-heavy modernization. The heightened compliance burden contributes a +0.5% uplift to sector CAGR by standardizing expectations and elevating the market value of certified expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce indicators – labour participation | -0.7% | National, acute in rural areas | Long term (≥ 4 years) |

| Sector investment priorities in infrastructure pipeline | -0.4% | National, regional variations | Medium term (2-4 years) |

| Rising labour costs amid ageing workforce | -0.6% | National, concentrated in urban areas | Short term (≤ 2 years) |

| Stringent bid-price caps in public FM tenders | -0.3% | Public sector nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Labour Costs Amid Ageing Workforce

The facility management payroll base is swelling faster than revenue growth. Wage hikes were implemented by 85.6% of companies in 2024, yet median increases of 3% failed to ease recruitment gaps as retirement accelerates. Labor-shortage bankruptcies hit a record 350 during the same year, with construction and logistics insolvencies disrupting subcontracting networks feeding facility operations. Providers must now layer retraining incentives, retention bonuses, and automation investments onto cost structures already burdened by inflation in materials. The squeeze erodes margins and knocks 0.6 percentage points off the Japan facility management market CAGR.

Stringent Bid-Price Caps in Public FM Tenders

Local-government procurement imposes fixed-price ceilings that leave little room to pass rising wage or compliance costs to clients. The designated-manager framework stipulates uniform service levels yet mandates price competitiveness, effectively compressing profitability. Municipal contracts, while volume rich, discourage advanced technology adoption because payback periods stretch beyond concession tenures. That constraint removes 0.3 percentage points from the projected CAGR, especially for providers heavy in public-sector portfolios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Market Foundation

Hard Services accounted for 60.10% of the Japan facility management market share in 2025. They encompass asset management, MEP and HVAC maintenance, fire-safety systems, and other technical functions essential for operational resilience. Demand remains steady because aging assets must meet tighter seismic and energy-efficiency codes, pushing asset owners to adopt predictive maintenance regimes and retro-commissioning campaigns. Asset-performance dashboards and digital twins help providers prioritize interventions, while IoT-enabled sensors deliver real-time condition data that reduces unscheduled downtime. The Japan facility management market size for Hard Services is expected to expand moderately as providers shift from reactive repairs to outcome-based contracts tied to uptime and energy-saving metrics.

Soft Services, covering cleaning, security, office support, catering, and concierge functions, are growing at a 4.72% CAGR to 2031, faster than Hard Services. Occupier expectations for wellness, hygiene, and hospitality-style amenity packages raise the strategic weight of Soft Services and justify premium pricing. Digital work-order platforms and robotics—such as autonomous floor scrubbers—are improving productivity and mitigating labor constraints. Providers able to fuse hospitality skills with data-driven quality control gain competitive leverage, broadening the revenue mix and accelerating integration across service silos within the Japan facility management market.

By Offering Type: Outsourcing Dominance Accelerates

Outsourced solutions commanded 67.60% of the Japan facility management market size in 2025 and are climbing at 4.12% CAGR as corporations offload non-core operations to specialists. Single-service contracts remain prevalent for basic janitorial or HVAC tasks, but bundled packages and Integrated FM (IFM) grow fastest, offering unified governance, KPI alignment, and technology harmonization across multi-site portfolios. IFM consolidates vendor footprints, enabling better procurement leverage and accountability while supplying clients with consolidated ESG metrics. The trend reflects board-level emphasis on operational resilience, risk transfer, and data visibility.

In-house management still holds a 32.40% share, primarily among asset-heavy conglomerates with legacy capability or mission-critical confidentiality needs. However, rising technological complexity and wage escalation pressure internal teams to adopt hybrid arrangements, subcontracting specialized tasks such as predictive analytics or vertical-transport maintenance. In-house operators increasingly deploy AI building-management systems and IoT sensor networks to stay cost-competitive, yet the structural drift toward outsourcing remains clear across the Japan facility management market.

By End-user Industry: Commercial Leadership Faces Industrial Challenge

Commercial facilities—spanning offices, retail, and warehousing—held 39.70% of total revenues in 2025 as corporate tenants sought workplace modernization, energy optimization, and occupant-experience enhancements. IT and telecom sites demand high-availability services, redundancy planning, and regulatory compliance around data security; retail centers focus on foot-traffic flows, asset protection, and experiential upgrades; warehouse operators prioritize throughput and environmental monitoring. These varied needs sustain robust spending yet expose providers to occupancy swings inherent in consumer demand cycles.

Industrial and process plants are posting the fastest growth at 4.63% CAGR due to manufacturing digitalization and predictive maintenance adoption. Production downtime carries steep financial penalties, pushing plant managers toward sensor-rich, data-visible facility programs that maximize uptime and comply with stringent safety mandates. Energy and mining projects also require specialist skills in hazardous-area management, environmental mitigation, and emergency response. As industry 4.0 initiatives proliferate, industrial sites will narrow the revenue gap with commercial properties within the Japan facility management market.

Hospitality assets—hotels, restaurants, and entertainment venues—demand guest-centric service quality, rapid issue resolution, and brand protection. Healthcare institutions require infection-control protocols, statutory compliance, and equipment uptime guarantees. Institutional and public-infrastructure operators—schools, transport hubs, museums—offer stable but price-sensitive revenue streams. Collectively, these verticals diversify provider portfolios and buffer macroeconomic volatility.

Geography Analysis

Tokyo remains the epicenter of the Japan facility management market, commanding the highest concentration of grade-A commercial properties, mixed-use developments, and public-facility complexes. High building densities create economies of scale for IFM contracts and accelerate the adoption of advanced analytics platforms, robotics, and energy-optimization tools. The Tokyo area thus sets the technological tempo for national service standards, influencing up-skill requirements across the country.

Osaka and Nagoya form secondary hubs, anchored by sizable industrial bases and growing life-science clusters that require clean-room maintenance, regulatory documentation, and continuous improvement methodologies. Local governments in both metros encourage sustainable-building retrofits through incentives, creating additional opportunities for energy-audit services and cap-ex advisory engagements. The Japan facility management market size attributed to these two regions is projected to rise steadily as manufacturing digitization and logistics expansion spur complex service demand.

Regional prefectures face an opposite challenge: demographic decline, shrinking municipal budgets, and scattered facility footprints complicate service delivery and profitability. Providers deploy mobile task forces and cloud-based work-order systems to combat distance inefficiencies, but higher travel time and lower asset density trim margins. This disparity encourages remote-monitoring centers and edge-computing gateways that permit predictive maintenance without constant on-site presence, enabling scalable service coverage despite personnel shortages.

Natural-hazard exposure dictates region-specific service differentiation. Earthquake-prone zones in central and southern Honshu necessitate seismic-monitoring installations and rapid-response protocols, increasing demand for real-time structural-health data and post-event inspection capacity. Coastal prefectures vulnerable to tsunamis invest in flood-barrier maintenance, back-up power systems, and emergency evacuation planning, adding specialized skillsets to provider offerings. Climate-change considerations, such as rising temperatures and intensifying typhoons, are starting to shape asset-hardening strategies and may drive incremental spending on resilience upgrades throughout the Japan facility management market.

Government-backed regional revitalization projects, including localized smart-city pilots and rural digital-infrastructure rollouts, offer growth pockets outside the megacities. Yet service-delivery economics require partnerships with local construction firms, utility operators, and community groups to align workforce availability and cultural norms. Providers with flexible labor models and standardized digital toolkits can replicate metropolitan-grade service quality across smaller towns, tapping untapped segments of the Japan facility management market.

Competitive Landscape

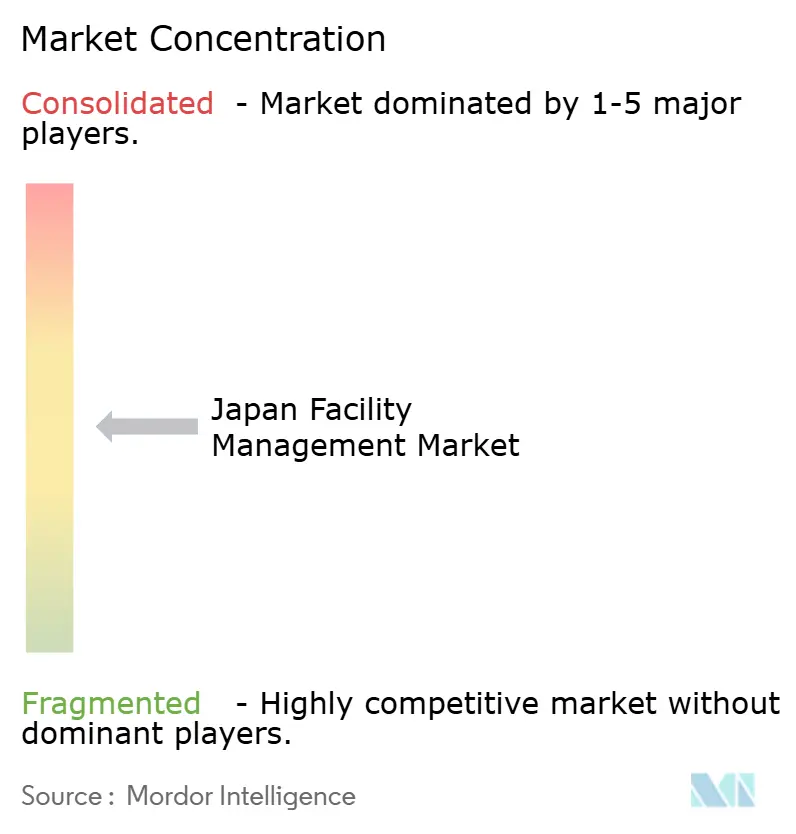

Japan’s facility management market exhibits moderate concentration, with several established conglomerates—such as Japan Kanzai Holdings, Nomura Real Estate Partners, and Tokyo Biso—holding multiregional IFM portfolios that deliver scale efficiencies in procurement, training, and technology deployment. These incumbents leverage proprietary digital platforms like “KANNA” to centralize work-order dispatch, track asset performance, and synthesize compliance documentation, thereby enhancing transparency and client retention. [4]PR Times, multiple facility-management press releases, prtimes.jp M&A activity is rising, illustrated by Nomura Real Estate’s 2025 merger and Daiwa House Realty Management’s acquisition of Sealex Facilities, both designed to internalize technical capabilities and bolster nationwide coverage.

Technology-enabled disruptors—often spin-offs from IT integrators or building-systems vendors—focus on niche pain points such as AI-driven energy analytics, robotic cleaning fleets, or real-time indoor environmental monitoring. Their asset-light models and cloud-native platforms attract clients seeking rapid deployment and subscription pricing. Partnerships between such specialists and legacy FM providers multiply, creating hybrid ecosystems that bundle hardware, software, and frontline workforce into unified SLA structures.

Strategic differentiation centers on four pillars: vertical integration that reduces subcontract layers; data analytics that quantify KPI attainment; workforce augmentation through automation and cross-training; and sustainability services that help clients decarbonize operations. Outsourcing propositions embedding these pillars command premium pricing and longer tenures, reshaping competitive benchmarks across the Japan facility management market.

Despite intensifying rivalry, barriers to entry remain formidable. Providers must hold national building-maintenance licenses, meet strict insurance requirements, and comply with health-and-safety training standards. As regulatory complexity deepens, smaller regional players face rising administrative costs and may seek alliances or exits. Consequently, the combined revenue of the top five providers is estimated near 55%, signaling a moderately consolidated field where scale and innovation coexist with pockets of fragmentation in rural or highly specialized services.

Japan Facility Management Industry Leaders

Globeship Sodexo

Compass Group Japan

RISE Corp. Tokyo

Nippon Kanzai Co.

ISS Facility Services Japan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Japan Kanzai Holdings debuted “KANNA,” a digital transformation platform that centralizes multisite facility data, reducing on-site visit frequency and countering staff shortages.

- July 2025: Nomura Real Estate Partners merged with Nomura Real Estate Amenity Service to unify cleaning services and strengthen operational management across national portfolios.

- July 2025: Sekisui Chemical launched “Heim Sweet” smart-resilient residential projects with ZEH-M Oriented standards, integrating IoT comforts and 20% energy-use reduction.

- June 2025: Fudial Creation commenced sales of “RELUXIA Yokohama Motomachi,” an IoT-ready condo secured by facial-recognition access and ZEH-M Oriented certification.

- June 2025: Hitachi secured an order for 173 elevators and escalators for Torch Tower, integrating the FIBEE destination-floor reservation system and FI-700 management software for future-proof operations.

- June 2025: Obayashi Corporation’s IoT-based “WELCS place” smart-building platform was adopted for two pavilions at the 2025 Osaka-Kansai Expo, supporting automated environmental control and visitor-flow analytics.

- May 2025: Daiwa House Realty Management acquired Sealex Facilities, expanding in-house building maintenance expertise and operational efficiency.

- May 2025: Panasonic EW Networks launched “SGNIS,” a smart-building service unifying lighting, surveillance, and access-control systems via secure networks to advance carbon-neutral objectives.

- April 2025: Tokyo Biso Holdings partnered with Builpo to deploy cleaning robots and the “BILLMS” management system, enhancing DX initiatives for building upkeep.

- April 2025: Hitotohito Holdings allied with Mitsui Fudosan to boost facility-management staffing flexibility for arenas and retail complexes via a 10,000-person talent pool.

Japan Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through its responsibility for often maintaining an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres.

Both in-house facility management and outsourced FM services are considered in the scope. The integrated facility management service (IFM) market, along with single and bundled services, is included in the outsourced FM services segment.

The Japan facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Japan facility management market?

The Japan facility management market size reached USD 64.56 billion in 2026.

How fast is the Japan facility management market expected to grow?

The market is projected to register a 2.50% CAGR, expanding to USD 73.66 billion by 2031.

Which service type holds the largest share?

Hard Services led with 60.10% share in 2025, mainly due to mandatory seismic and energy-efficiency upgrades.

Why is outsourcing gaining popularity in Japan’s facility management industry?

Outsourcing allows organizations to transfer operational risk, tap specialized technology, and control costs, giving outsourced contracts 67.60% share in 2025.

Which end-user segment is growing fastest?

Industrial and process facilities are growing at 4.63% CAGR as manufacturing embraces predictive maintenance and digitalization.

Page last updated on: