Japan Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

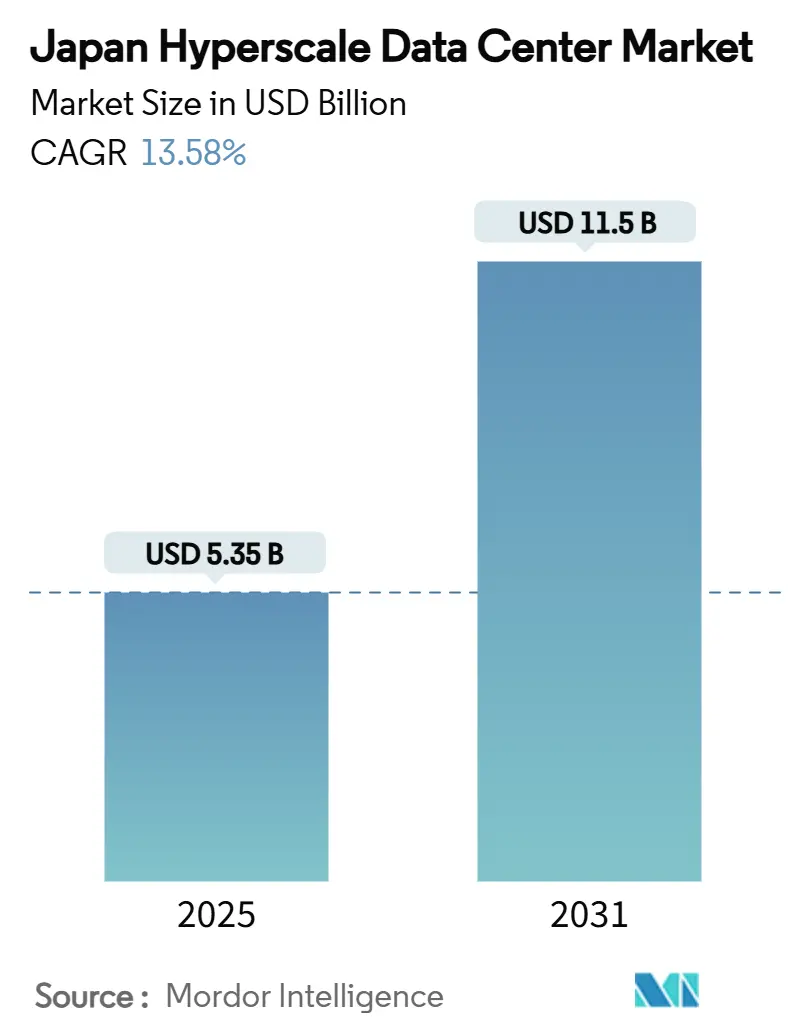

| Market Size (2025) | USD 5.35 Billion |

| Market Size (2031) | USD 11.5 Billion |

| Growth Rate (2025 - 2031) | 13.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Hyperscale Data Center Market Analysis by Mordor Intelligence

The Japan hyperscale data center market size stands at USD 5.35 billion in 2025 and is forecast to reach USD 11.50 billion in 2031, expanding at a 13.58% CAGR. The value trajectory reflects a combined uplift from sovereign-cloud incentives, large-scale AI training demand, and grid-reinforcement programs that are steadily easing long-standing power-allocation bottlenecks. Heightened Gen-AI rack densities are pushing operators toward liquid cooling, while joint-venture land aggregation across inland Chiba and Ibaraki is opening parcels greater than 100 MW that were previously unattainable. Deep-tier grid upgrades, especially the 66 kV feed-ins planned for Greater Tokyo, underpin capacity expansion after 2027. Tightened environmental standards, including zero-liquid-discharge rules for Kanto aquifers, are steering designs toward water-saving technologies. Meanwhile, entrenched GPU shortages and construction-cost inflation temper near-term build velocity but ultimately reinforce long-term pricing power for operators with secured supply chains.

Key Report Takeaways

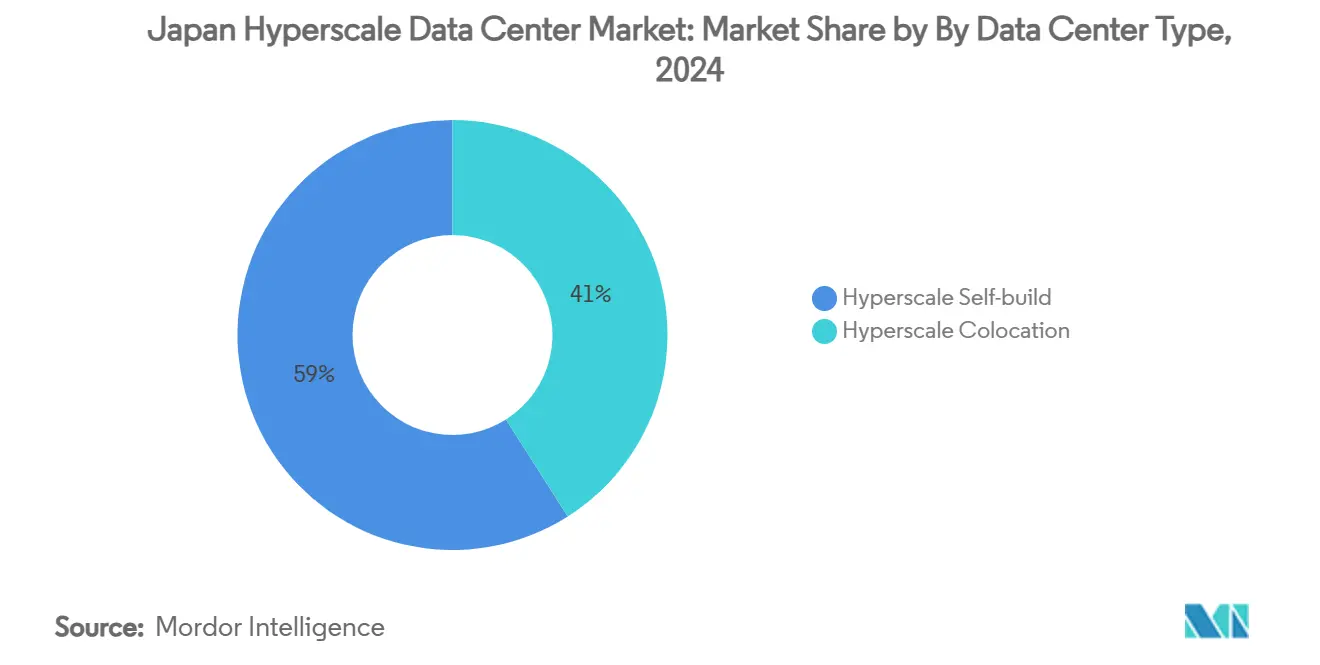

- By data center type, hyperscale self-build operations held 59% of the Japan hyperscale data center market share in 2024, whereas hyperscaler colocation is projected to expand at a 13.8% CAGR through 2030.

- By component, IT infrastructure accounted for a 45% share of the Japan hyperscale data center market size in 2024, while cooling systems are advancing at a 16.01% CAGR through 2030.

- By tier standard, Tier III facilities led with 65% revenue share in 2024; Tier IV is forecast to post the fastest 14.58% CAGR to 2030.

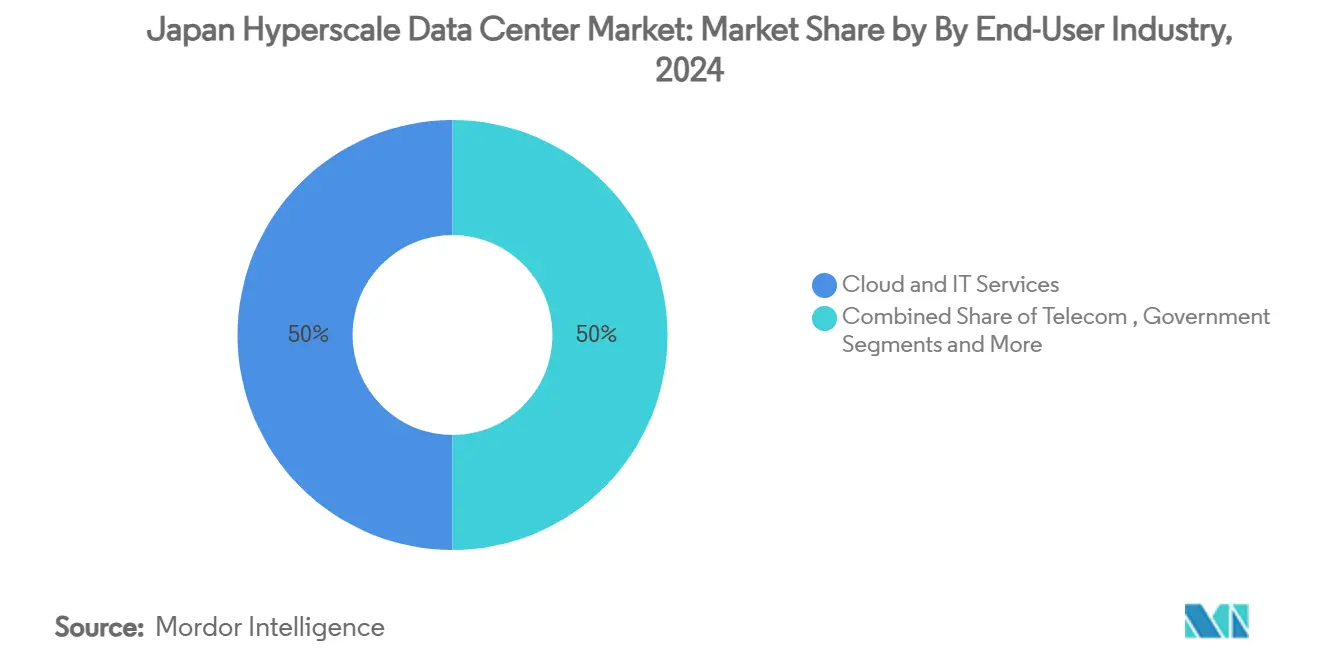

- By end-user industry, e-commerce applications captured 15.5% of the Japan hyperscale data center market size growth in 2024 and are set to expand at the highest 15.5% CAGR through 2030.

- By data center size, mega-scale (greater than 60 MW) buildouts are projected to increase at a 15.58% CAGR, even as massive-scale (25-60 MW) sites command 55% of the current Japan hyperscale data center market size.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Japan representing one among them. The global report on hyperscale data center market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Japan Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Soaring Gen-AI inference loads (greater than 70 kW/rack) driving campus-scale liquidity-cooled builds | +3.2% | Greater Tokyo, Kansai core regions | Medium term (2-4 years) |

| Sovereign-cloud mandates (GovCloud) boosting hyperscale localisation | +2.8% | National, with concentration in Tokyo-Osaka corridor | Short term (≤ 2 years) |

| Tokyo-grid reinforcement and 66 kV feed-ins unlocking greater than100 MW parcels | +2.1% | Greater Tokyo metropolitan area | Long term (≥ 4 years) |

| JV-led land aggregation around inland Chiba and Ibaraki ("Inland Edge") | +1.4% | Chiba, Ibaraki prefectures | Medium term (2-4 years) |

| Waste-heat offtake PPAs with district heating schemes, esp. Sapporo | +0.8% | Hokkaido, northern regions | Long term (≥ 4 years) |

| "Green ammonia" generators for N-1 resiliency (proof-of-concept 2025-28) | +0.6% | National pilot sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Gen-AI inference loads driving liquid-cooling adoption

Rack power density surpassing 70 kW is forcing a pivot from air to immersion or direct-to-chip liquid cooling. KDDI’s field trials delivered a 94% electricity reduction and a PUE of 1.05, aligning with the Ministry of Economy, Trade and Industry’s national PUE target.[1]Nikkei Asia, “Japan’s Utilities Pour Billions into Power Grid Amid Data Center Growth,” Nikkei, asia.nikkei.com NTT Facilities opened its Products Engineering Hub in 2025 to qualify multi-vendor liquid systems tailored for GPU clusters. These innovations unlock higher revenue per square meter, especially in land-scarce Tokyo, and strengthen operator margins as utility rates rise.

Sovereign-cloud mandates accelerating localization

Under the Economic Security Promotion Act, METI approved JPY 72.5 billion in subsidies for domestic cloud projects to reduce foreign-provider dominance.[2]Ministry of Economy, Trade and Industry, “Approval of Plans Under the Economic Security Promotion Act,” METI, meti.go.jp Oracle’s alliance with Fujitsu and NRI illustrates how international hyperscalers are re-architecting stacks to satisfy data-residency and operational-control clauses. The policy shift is already spawning parallel premium-priced sovereign zones within existing campuses, fostering a differentiated service tier across the Japan hyperscale data center market.

Tokyo grid reinforcement unlocking mega-scale development

Utilities are tackling seven-year connection queues by investing more than JPY 150 billion from 2026 to upgrade four Osaka-area substations and expand Greater Tokyo’s 66 kV network. Hitachi’s VSC technology will triple Higashi-Shimizu’s capacity by fiscal 2027. These projects lower connection risk and incentivize greater than 100 MW campuses, altering the location calculus for future builds.

JV-led land aggregation creating Inland Edge opportunities

Digital Realty and Mitsubishi’s JV model is consolidating fragmented parcels in inland Chiba and Ibaraki, delivering contiguous tracts suitable for hyperscale footprints.[3]Digital Realty, “Digital Realty and Mitsubishi JV,” Digital Realty, digitalrealty.com Google’s Inzai data center validates latency performance for metropolitan workloads while benefiting from lower land costs. The approach diversifies risk away from congested urban wards yet keeps operators inside Japan’s critical economic corridor.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Seven-year power-queue backlog (154 kV) | −2.4% | Greater Tokyo, metros | Medium term (2–4 years) |

| Construction-cost inflation (+8% YoY) | −1.8% | National, urban hotspots | Short term (≤ 2 years) |

| Tightened water-draw caps in Kanto aquifers | −1.2% | Kanto region | Medium term (2–4 years) |

| GPU/HBM supply crunch delaying energization | −1.6% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Seven-year power-queue backlogs constraining market entry

Demand for 154 kV connections now exceeds supply, creating multiyear queues that tilt advantage toward incumbents with pre-allocated capacity. Industry groups estimate grid-equipment lead times at 18–24 months, while Hitachi Energy calls for USD 600 billion yearly global grid spend to close the gap. New entrants are resorting to on-site generation and demand-response strategies, but these add capital burden and lengthen payback periods.

GPU/HBM supply crunch delaying critical infrastructure

Micron sold its entire HBM3E production for 2024 and most of 2025, and NVIDIA’s Blackwell delays are compelling hyperscalers to revert to interim H200 deployments. Pods delivered as powered shells cannot monetize until compute is installed, extending IRR breakeven timelines and affecting developer cash flows across the Japan hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Self-Build Dominance, Colocation Upswing

The Japan hyperscale data center market size attributed to self-build facilities reached USD 3.16 billion in 2024, equal to 59% of total value, while colocation captured the remainder. Self-build projects appeal for bespoke power topologies and proprietary security layers, especially for AI training workloads that exceed 70 kW per rack. AWS’s ongoing JPY 2.26 trillion investment signals continued preference for full-stack control. However, hyperscaler colocation is advancing at a 13.8% CAGR through 2030 as operators leverage specialist providers such as Equinix or Digital Realty to accelerate market entry and mitigate development risk. The shift broadens demand visibility for wholesale providers and injects new design standards—liquid cooling corridors and high-voltage feeds—across multi-tenant campuses.

Second-order effects include a tighter leasing market in metropolitan zones as sovereign-cloud tenants secure reserved halls within existing builds. Colocation operators are responding by forward-power-reserving with utilities and by pre-installing liquid-cooling manifolds to cut fit-out windows. In rural adjacencies, self-build activity is spurring ancillary industrial revitalization as data-center campuses reinstate dormant substations and rail links. Together, both build models ensure the Japan hyperscale data center market maintains a balanced capacity pipeline through the forecast horizon.

By Component: Cooling Systems Outpacing Core IT Spend

IT infrastructure retained 45% share of Japan hyperscale data center market size in 2024, but cooling systems registered the fastest 16.01% CAGR and are on pace to surpass electrical infrastructure spend by 2029. Liquid immersion and direct-chip loops dominate new builds, driven by Gen-AI density and a national PUE target of 1.4. KDDI’s immersion prototype achieved 94% energy savings versus air cooling. Operators are also adding thermal-storage tanks to shift chiller load to off-peak hours, trimming grid draws during summer peaks.

Electrical infrastructure continues steady growth as projects standardize on 66 kV primary feeds and 415 V rack-level delivery, while mechanical infrastructure beyond cooling contracts marginally because liquid systems reduce air-handling footprints. General construction spend remains elevated due to imported steel costs, yet value-engineering via modular skids offsets part of the inflation. Finally, DCIM/BMS platforms that integrate CFD models with AI-driven workload placement are gaining traction for optimizing mixed air-and-liquid environments. Collectively, component mix evolution will re-shape procurement strategies across the Japan hyperscale data center industry.

By Tier Standard: Tier IV Gaining Ground

Tier III sites commanded 65% of Japan hyperscale data center market size in 2024, fulfilling most cloud and SaaS latency-availability trade-offs. Yet Tier IV capacity is projected to grow 14.58% CAGR through 2030 as sovereign workloads, high-frequency trading, and uninterrupted AI training require fault-tolerant configurations. Oracle’s sovereign deployments demonstrate feasibility of Tier III for government workloads via application-level redundancy, but several ministries now mandate Tier IV for sensitive systems. Seismic resiliency standards and tsunami-elevation codes also prompt Tier IV adoption, particularly in coastal Osaka facilities. Over time, hybrid campus models—Tier IV core pods flanked by Tier III edge halls—will optimize capital spend while satisfying workload diversity.

By End-User Industry: E-Commerce Momentum

Cloud and IT led with a 50% contribution to Japan hyperscale data center market share in 2024, reflecting the country’s deep cloud-services penetration. However, e-commerce workloads show the quickest expansion at 15.5% CAGR, fuelled by AI-powered personalization engines and stricter electronic payment standards. Government digital-transformation budgets are also rising under the Digital Agency’s multi-cloud blueprint, steering sovereign traffic into domestic facilities. BFSI maintains stable demand for low-latency, multi-region redundancy, while media streaming and telecom 5G edge cases stimulate distributed buildouts. Manufacturing’s smart-factory analytics rely on high-bandwidth interconnects, leveraging emerging IOWN photonic links for remote process control. End-user diversification thus anchors long-term demand fundamentals for the Japan hyperscale data center market.

By Data Center Size: Mega-Scale Ascendance

Mega-scale facilities above 60 MW recorded the fastest 15.58% CAGR, even as massive-scale (25–60 MW) sites retained 55% of Japan hyperscale data center market size in 2024. SoftBank’s 150 MW Osaka conversion illustrates scale economics and aligns with GPU cluster co-location strategies. Mega campuses benefit from power-purchase agreements that secure renewable supply at sub-yen per kWh rates, offsetting high upfront grid-connection fees. Smaller ≤25 MW builds thrive in edge-latency use cases but will represent a diminishing share of new MW added after 2027. Overall, size stratification reflects evolving workload footprints and accentuates the need for diversified regional power planning.

Geography Analysis

Greater Tokyo remains the nucleus of the Japan hyperscale data center market, pairing proximity to financial exchanges with a widening array of Inland Edge sites in Chiba and Ibaraki. Grid-reinforcement projects introducing 66 kV feeds are unlocking parcels capable of hosting greater than 100 MW campuses. Yet the region confronts strict water-draw caps, pushing operators to adopt zero-liquid discharge and rain-harvest systems. Kansai is emerging as a credible dual-hub, propelled by Kansai Electric’s JPY 150 billion substation upgrade to support 900 MW of aggregate capacity and by EdgeConneX’s 140 MW entry plan. Lower seismic risk in inland Kyoto further enhances the region’s attractiveness.

Kyushu and Western Honshu appeal through land affordability and renewable-rich grids. Global Compute’s Kyushu hub signals fresh interest in tapping under-utilized transmission lines connected to solar parks. Hokkaido and Tohoku capitalize on cool ambient temperatures and wind power availability; Ishikari’s near-zero-CO₂ data center serves as a proof point. Chubu, Shikoku, and Okinawa remain niche, catering to disaster-recovery zones and localized edge nodes. Geographic diversification consequently reduces systemic risk while broadening the addressable footprint for the Japan hyperscale data center market.

Mordor Intelligence provides coverage of the hyperscale data center market across other key regional markets, including North America, Middle East, and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Australia, Taiwan, Canada, Israel, South Africa, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

Competition is moderate, with global hyperscalers, domestic telcos, and specialized colocation firms battling for power reservations, land access, and GPU allocations. AWS heads capital intensity with a JPY 2.26 trillion pledge through 2027. Oracle’s USD 8 billion sovereign-cloud build enhances tiered service strategies for regulated clients. Domestic incumbents like NTT leverage long-standing utility partnerships, while KDDI differentiates via immersion-cooling breakthroughs, achieving 1.05 PUE. New entrants such as EdgeConneX rely on joint ventures to navigate zoning and cultural nuances.

Supply-chain disruptions favor players with locked-in GPU or transformer contracts. Some operators sign multi-year HBM futures to de-risk project schedules, effectively raising barriers for latecomers. Meanwhile, white-space exists in district-heat reuse and green-ammonia power modules, where innovators may leapfrog incumbents. Ecosystem collaborations—Digital Realty with Mitsubishi, Sakura Internet with JERA—illustrate how partnership depth increasingly dictates success in the Japan hyperscale data center industry.

Japan Hyperscale Data Center Industry Leaders

Amazon Web Services (AWS)

Google LLC

Microsoft Corporation

Digital Realty Trust, Inc.

Equinix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NTT DATA completed its USD 16.4 billion buy-out by parent NTT, integrating nearly 1 GW of planned capacity, including 100 MW in Tochigi.

- June 2025: KDDI and HPE announced an Osaka AI data center launch by FY 2025, incorporating NVIDIA Blackwell chips.

- June 2025: Sakura Internet and JERA signed an MoU to explore data-center co-location at LNG plants in Tokyo Bay.

- May 2025: AirTrunk opened its second Tokyo hyperscale data center, expanding domestic capacity.

Japan Hyperscale Data Center Market Report Scope

Hyperscale data centers, also known as Enterprise Hyperscale facilities, are large-scale infrastructures owned and managed by the companies they support. These centers deliver a wide range of scalable applications and storage services to meet the needs of individuals and businesses. Designed for efficiency, they house thousands of servers alongside critical hardware like routers, switches, and storage disks. To ensure seamless operations, these facilities are equipped with advanced support systems, including power and cooling solutions, uninterruptible power supplies (UPS), and air distribution networks.

The Japan Hyperscale Datacenter Market is Segmented by Data Center Type (Hyperscale Colocation, Enterprise/Hyperscale Self Build), By Service Type (IaaS ( Infrastructure-as-a-Service), PaaS ( Platform-as-a-Service), SaaS( Software-as-a-Service)), By End User (Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce, Other End User). The Report Offers the Market Size and Forecasts for all the Above Segments in Terms of USD (millions).

| Hyperscale Self-build |

| Hyperscale Colocation |

| IT Infrastructure | Server Infrastructure |

| Storage Infrastructure | |

| Network Infrastructure | |

| Electrical Infrastructure | Power Distribution Units |

| Transfer Switches and Switchgear | |

| UPS Systems | |

| Generators | |

| Other Electrical Infrastructure | |

| Mechanical Infrastructure | Cooling Systems |

| Racks | |

| Other Mechanical Infrastructure | |

| General Construction | Core and Shell Development |

| Installation and Commissioning | |

| Design Engineering | |

| Fire Detection, Suppression and Physical Security | |

| DCIM/BMS Solutions |

| Tier III |

| Tier IV |

| Cloud and IT |

| Telecom |

| Media and Entertainment |

| Government |

| BFSI |

| Manufacturing |

| E-commerce |

| Other End Users |

| Large ( Less than or equal to 25 MW) |

| Massive (Greater than 25 MW and Less than equal to 60 MW) |

| Mega (Greater than 60 MW) |

| By Data Center Type | Hyperscale Self-build | |

| Hyperscale Colocation | ||

| By Component | IT Infrastructure | Server Infrastructure |

| Storage Infrastructure | ||

| Network Infrastructure | ||

| Electrical Infrastructure | Power Distribution Units | |

| Transfer Switches and Switchgear | ||

| UPS Systems | ||

| Generators | ||

| Other Electrical Infrastructure | ||

| Mechanical Infrastructure | Cooling Systems | |

| Racks | ||

| Other Mechanical Infrastructure | ||

| General Construction | Core and Shell Development | |

| Installation and Commissioning | ||

| Design Engineering | ||

| Fire Detection, Suppression and Physical Security | ||

| DCIM/BMS Solutions | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-User Industry | Cloud and IT | |

| Telecom | ||

| Media and Entertainment | ||

| Government | ||

| BFSI | ||

| Manufacturing | ||

| E-commerce | ||

| Other End Users | ||

| By Data Center Size | Large ( Less than or equal to 25 MW) | |

| Massive (Greater than 25 MW and Less than equal to 60 MW) | ||

| Mega (Greater than 60 MW) | ||

Key Questions Answered in the Report

What is the current value of the Japan hyperscale data center market?

The market is valued at USD 5.35 billion in 2025 and is forecast to reach USD 11.50 billion by 2031.

Which segment is growing fastest within the market?

Hyperscaler colocation is expanding at a 13.8% CAGR, reflecting demand for rapid deployment without self-build complexities.

Why are liquid-cooling systems gaining popularity?

Gen-AI racks exceeding 70 kW require immersion or direct-chip cooling, delivering power-usage-effectiveness as low as 1.05 and enabling higher rack densities.

What is the biggest barrier to new entrants?

A seven-year power-queue backlog for 154 kV connections in metropolitan areas significantly delays project timelines and favors incumbents with pre-secured capacity.

Which regions outside Tokyo are seeing major growth?

Kansai (Osaka-Kyoto) is rapidly emerging due to large substation upgrades, while Kyushu and Hokkaido attract capacity for their renewable energy and land availability advantages.

Page last updated on: