Japan Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

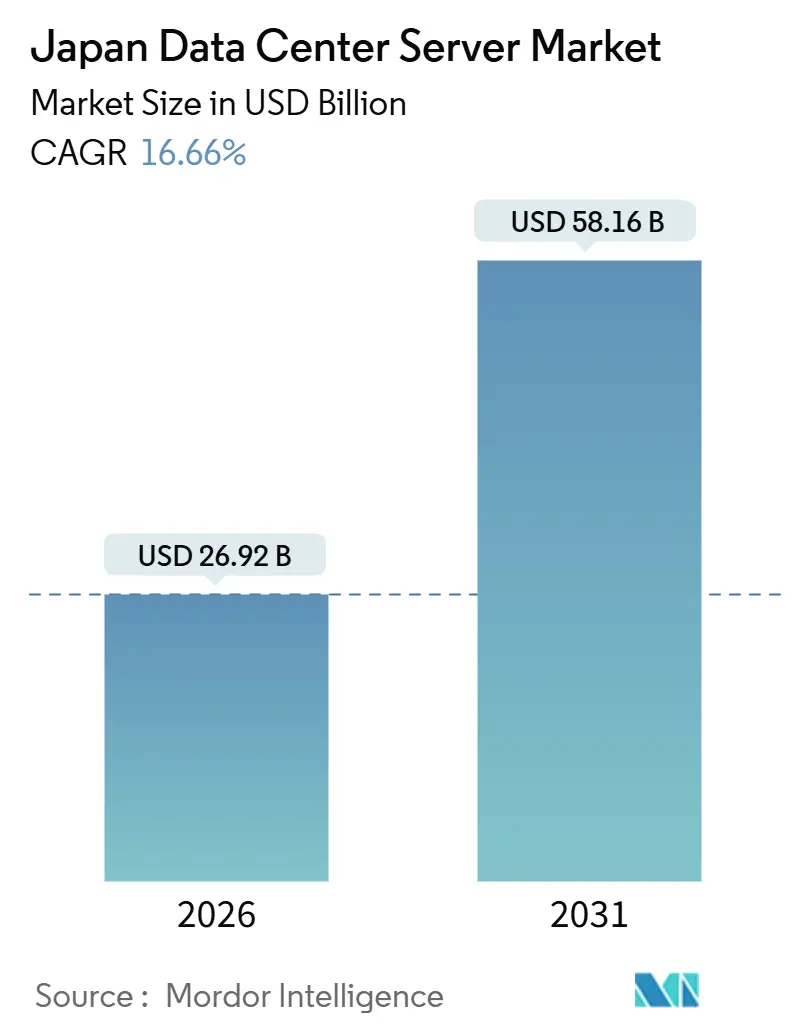

| Market Size (2026) | USD 26.92 Billion |

| Market Size (2031) | USD 58.16 Billion |

| Growth Rate (2026 - 2031) | 16.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Data Center Server Market Analysis by Mordor Intelligence

The Japan data center server market size stood at USD 26.92 billion in 2026 and is forecast to reach USD 58.16 billion by 2031, expanding at a 16.66% CAGR. Robust capital outlays by hyperscale cloud providers are accelerating fresh server deployments, while sovereign semiconductor programs shorten component lead times and encourage proprietary silicon adoption. Rapid densification of racks above 100 kilowatts, stricter energy-efficiency mandates, and growing availability of renewable power outside Tokyo and Osaka are reshaping investment priorities. Competitive tension is intensifying as global OEMs introduce liquid-cooled GPU systems to counter domestic incumbents embedding Arm-based processors. Simultaneously, edge-computing use cases in smart-factory automation foster demand for compact micro-blade servers that can fit inside industrial enclosures.

Key Report Takeaways

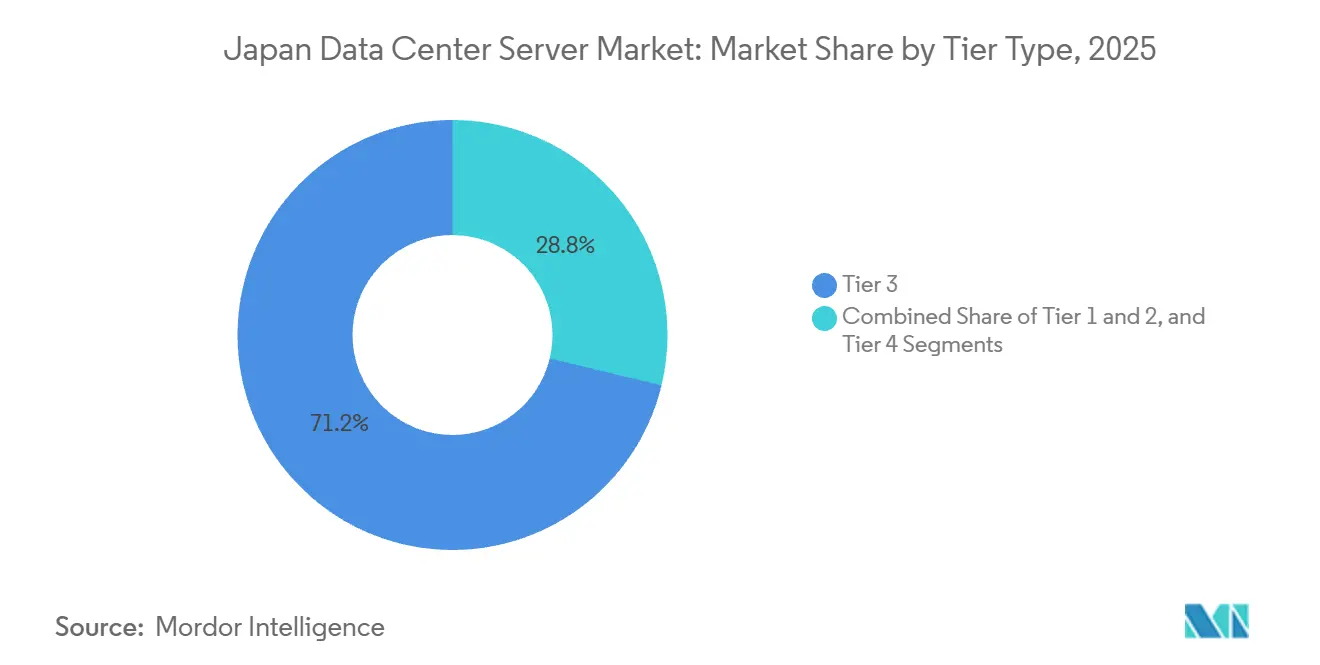

- By tier type, tier 3 facilities held 71.24% of 2025 revenue, while tier 4 deployments are projected to climb at a 17.21% CAGR through 2031.

- By data center size, hyperscale campuses commanded 44.54% of 2025 capacity and will expand at a 17.45% CAGR through 2031.

- By data center type, colocation operators controlled 56.87% of 2025 turnover, yet hyperscalers are expanding direct builds at a 17.63% CAGR through 2031.

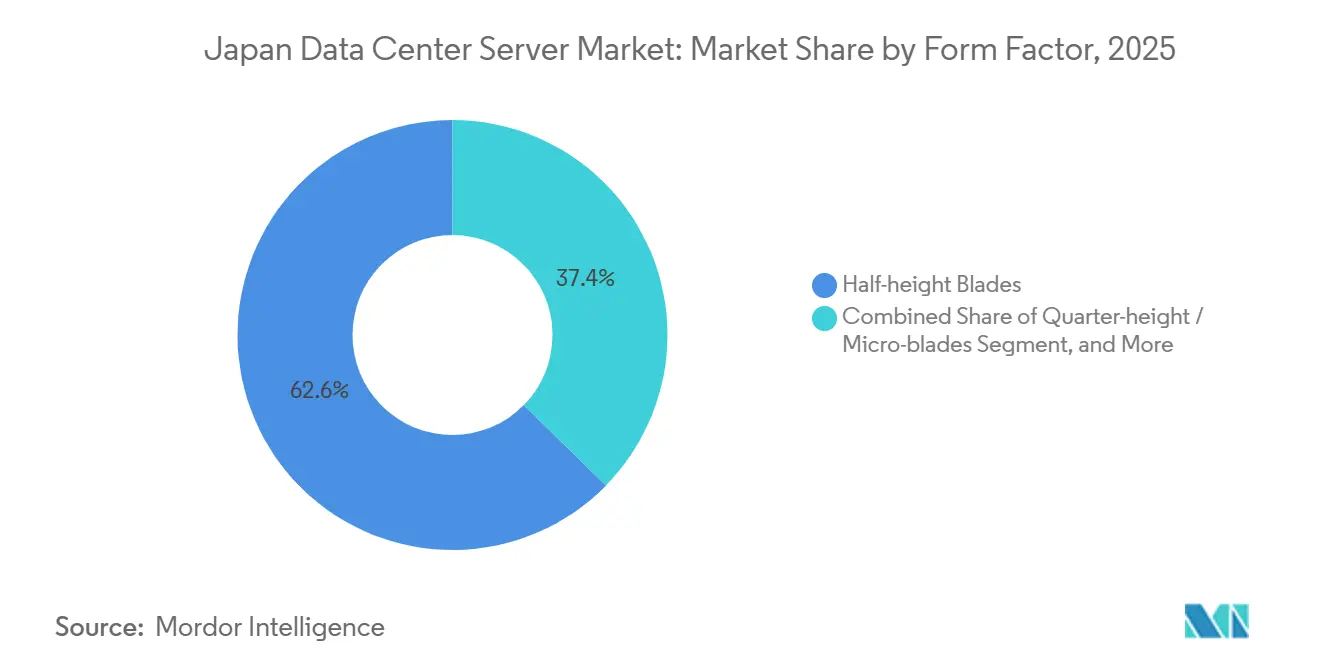

- By form factor, half-height blades captured 62.65% of 2025 shipments; quarter-height and micro-blade servers are rising at a 17.87% CAGR through 2031.

- By application, artificial intelligence and machine learning workloads represented 36.76% of 2025 demand, while virtualization and private cloud segments are growing at a 17.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Anticipated developments are shaped at a system level, with Japan signals feeding into a larger global picture. The outlook on global data center server market consolidates these expectations.

Japan Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of hyperscale facilities by US cloud giants | +4.5% | National, with concentration in Greater Tokyo, Osaka, and emerging Hokkaido clusters | Medium term (2-4 years) |

| Accelerated refresh cycle to AI-optimized GPU servers | +4.2% | National, led by Tokyo and Osaka metro regions | Short term (≤ 2 years) |

| Rising edge-computing nodes for smart-factory rollouts | +2.8% | National, with early gains in manufacturing hubs: Aichi, Kanagawa, Shizuoka | Medium term (2-4 years) |

| Strategic semiconductor self-sufficiency programs | +2.1% | National, anchored in Kumamoto (TSMC) and Hokkaido (Rapidus) | Long term (≥ 4 years) |

| Corporate tax incentives for datacenter energy efficiency | +1.5% | National, with higher uptake in regional prefectures offering supplemental subsidies | Medium term (2-4 years) |

| Mandatory green procurement rules for government IT | +1.2% | National, driven by central government agencies and prefectural administrations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion Of Hyperscale Facilities By US Cloud Giants

Amazon Web Services, Microsoft Azure, and Oracle pledged more than USD 26 billion of capital between 2024 and 2026, dwarfing the previous decade’s cumulative investment and signaling a pivot toward in-country availability zones for regulated workloads.[1]AWS Press Center, “AWS Announces Plans to Invest USD 15.24 Billion in Japan by 2027,” amazon.com NTT DATA responded with a USD 10 billion build program targeting roughly 1 gigawatt by 2027, while EQUINIX deployed 3,700 cabinets at its TY15 site to satisfy rising interconnection demand. Mitsui Fudosan and Ares Management have likewise financed large campuses in Kanagawa and Tokyo. Faster project cycles favor modular racks that ship pre-integrated, enabling deployment in 90 days rather than 12 months, which benefits vendors with local assembly.

Accelerated Refresh Cycle To AI-Optimized GPU Servers

Japanese operators installed more than 10,000 NVIDIA H200 GPUs during 2025. Notable rollouts include GMO Internet’s 1,000-GPU cluster in May, SAKURA Internet’s 3,072-unit expansion in August, and AIST’s 6,128-GPU ABCI 3.0 supercomputer in January. Generative AI inference pushes rack power well beyond 100 kilowatts, compelling operators to retrofit liquid-cooling. Fujitsu and Super Micro Computer formed an April 2025 pact to embed direct liquid cooling in PRIMERGY servers, aiming for 40% lower energy use.[2]Fujitsu Ltd., “Fujitsu and Super Micro Computer Announce Collaboration on Direct Liquid Cooling,” fujitsu.com The refresh interval is compressing to 2.5 years as firms reap real-time analytics benefits.

Rising Edge-Computing Nodes For Smart-Factory Rollouts

NTT Communications and Toshiba proved a cloud-programmable logic controller in November 2025, cutting deployment cost by 30% against conventional distributed control systems.[3]NTT Communications, “Cloud-Programmable Logic Controller Demonstration,” ntt.com Demographic pressures and a working-age population that fell 0.6% annually through 2025 are driving manufacturers toward automated visual inspection and predictive maintenance. Internet Initiative Japan’s Phase 3 campus incorporates 10-kilowatt edge racks scheduled for 2026 start-up. Compact micro-blades that tolerate tighter thermal envelopes now outpace half-height blades in new edge nodes.

Strategic Semiconductor Self-Sufficiency Programs

TSMC’s first Kumamoto fab went live in December 2024 with 55,000 wafers per month, while a second line for 6-nanometer processes completes in 2027, bringing total spend to USD 20 billion. Rapidus, funded by a USD 33 billion commitment, targets 2-nanometer production in Hokkaido by 2027 to reclaim advanced-node capability. Domestic fabs promise shorter lead times for custom ASICs, letting hyperscalers field proprietary silicon that boosts power efficiency and lowers total cost of ownership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High land and power costs in metro regions | -2.3% | Greater Tokyo, Osaka, and Nagoya metropolitan areas | Short term (≤ 2 years) |

| Escalating grid-power curtailment risks | -1.8% | National, most acute in Tokyo and Osaka service territories | Medium term (2-4 years) |

| Lengthy environmental approval timelines | -1.1% | National, with stricter enforcement in urban prefectures | Medium term (2-4 years) |

| Talent shortage in advanced server maintenance | -0.9% | National, concentrated in regions with semiconductor and AI infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Land And Power Costs In Metro Regions

Data-center build costs climbed to USD 13.2 million per megawatt in Greater Tokyo during 2024, 35% above Singapore, fueled by scarce land and premium grid tariffs from TEPCO. Developers respond by densifying existing footprints with liquid-cooled racks and by expanding to Hokkaido and Kyushu, where land is 40% cheaper and renewable penetration exceeds 30%.

Escalating Grid-Power Curtailment Risks

Tokyo Electric Power Company and Kansai Electric Power Company impose connection waits of up to 10 years for projects above 10 megawatts, stalling hundreds of megawatts in the pipeline. SoftBank secured a JPY 30 billion (USD 200 million) subsidy in February 2024 to build a 50-megawatt site in Tomakomai, Hokkaido to tap surplus hydro and wind. Containerized, modular halls that scale with incremental power availability help operators avoid idle white space.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Mission-Critical Uptime Reshapes Infrastructure Mix

Tier 3 assets dominated the Japan data center server market share at 71.24% in 2025, a reflection of cost-sensitive colocation and enterprise deployments. Tier 4 facilities are projected to expand at a 17.21% CAGR as banks and government agencies demand 99.995% uptime, especially after the 2024 Noto Peninsula earthquake. NEXTDC’s TK1 campus launched in 2024 illustrates tenant willingness to pay 25% premium lease rates for higher redundancy.

Vendor strategies now emphasize direct liquid-cooled PRIMERGY and DLC-2 racks that temper the 250-kilowatt densities needed for GPU clusters. The Japan data center server market size for Tier 4 is therefore on track to outpace overall growth. Meanwhile, Tier 1 and Tier 2 rooms continue to decline as enterprises consolidate into regional colocation hubs.

By Data Center Size: Hyperscale Dominance Masks Regional Fragmentation

Hyperscale campuses controlled 44.54% of the Japan data center server market in 2025 and will grow at a 17.45% CAGR, buoyed by AWS and NTT DATA programs exceeding 1 gigawatt. Large 10-50 megawatt sites trail as grid delays impede metro builds. Medium facilities face margin pressure amid cloud migration, while small legacy rooms are being decommissioned.

The Japan data center server market size for hyperscale assets is further supported by long-term sale-leaseback deals such as Keppel DC REIT’s USD 707 million Tokyo DC 3 purchase, ensuring stable cash flows that attract institutional capital. Edge-oriented operators use modular 10-megawatt designs to match tenant ramp-up and grid schedules.

By Data Center Type: Colocation Leadership Faces Hyperscaler Vertical Integration

Colocation providers held 56.87% revenue in 2025; however, hyperscalers are expanding self-build capacity at a 17.63% CAGR, compressing third-party margins. Equinix pre-leased 60% of its 3,700-cabinet TY15 site, underscoring colocation’s interconnection appeal. NTT DATA’s USD 10 billion pipeline reflects a defensive stance to retain enterprise clients.

Conversely, Amazon Web Services and Microsoft favor sovereign-cloud compliance and latency gains through owned campuses. The Japan data center server market share for colocation will therefore erode moderately, although hybrid edge nodes embedded inside hyperscale compounds offer a new growth avenue.

By Form Factor: Density Demands Drive Micro-Blade Adoption

Half-height blades delivered 62.65% of shipments in 2025, yet quarter-height and micro-blade servers are growing at a 17.87% CAGR as factories and 5G sites pursue compact designs. Super Micro Computer’s DLC-2 solution supports 250-kilowatt racks and cuts energy use 40%.

The Japan data center server market size for micro-blades is lifted by Fujitsu’s Arm-based Monaka roadmap and Dell’s PowerEdge XE9712 launch with NVIDIA GB200 compatibility. Full-height blades retreat as GPU-dense rack-scale systems replace legacy chassis.

By Application And Workload: AI Inference Reshapes Compute Priorities

AI and machine learning workloads owned 36.76% of 2025 demand, while virtualization and private cloud functions are advancing at a 17.38% CAGR. GMO Internet, SAKURA Internet, and AIST collectively installed over 10,000 GPUs to support generative applications. The Japan data center server market size for AI inference is therefore poised to remain the fastest growing slice.

High-performance computing persists in academia, exemplified by Tohoku University’s 20-petaflop HPE Cray EX, while storage-centric workloads adopt NVMe-over-Fabrics for 8K video editing. Edge IoT gateways grow rapidly as manufacturers need sub-10-millisecond response times.

Geography Analysis

Greater Tokyo still hosts roughly 55-60% of installed capacity, but build costs of USD 13.2 million per megawatt motivate operators to densify rather than expand greenfield. Osaka benefits from lower land prices, though grid queues of 3-5 years delay large projects. Hokkaido and Kyushu, supported by renewable surpluses and government subsidies up to JPY 30 billion per project, are set to capture 10-15% of new capacity by 2027.

SoftBank’s 50-megawatt Tomakomai facility leverages hydro and wind resources, while EdgeConneX phases a 350-megawatt Osaka platform to grid-upgrade timelines. TSMC’s Kumamoto fab catalyzes a Kyushu ecosystem that shortens server-assembly supply chains. Rapidus’ 2-nanometer project is expected to attract co-located data centers near Chitose by 2027, exploiting Hokkaido’s cool climate to meet the 1.4 PUE ceiling mandated under the Act on Rationalizing Energy Use.

Latency-sensitive workloads like electronic trading remain Tokyo-centric, while AI training and archival storage shift to cooler northern sites. Operators race to lock grid capacity in secondary prefectures before hyperscalers internalize supply.

Mordor Intelligence delivers a comprehensive view of the data center server market across all major regions such as Africa, North America, and Americas, alongside country-level analysis for Taiwan, Indonesia, South Africa, Canada, United States, and Sweden, each offering a view of the local market realities.

Competitive Landscape

The Japan data center server market features moderate fragmentation. Global OEMs like Dell Technologies, Hewlett Packard Enterprise, and Lenovo counter local incumbents Fujitsu and NEC by supplying liquid-cooled GPU systems. Fujitsu’s April 2025 pact with Super Micro Computer embeds direct liquid cooling in PRIMERGY racks, priming Arm-based Monaka servers for 2027 launch. HPE’s Cray EX at Tohoku University showcases liquid-cooling expertise, whereas Dell’s XE9712 readies for NVIDIA GB200 adoption.

Hyperscalers increasingly commission white-box gear from Quanta and Wistron, squeezing traditional margins. Hitachi’s October 2025 alliance with OpenAI extends its power-distribution and cooling portfolio into AI hubs. Edge opportunities invite automation vendors such as Siemens to integrate compute-embedded controllers.

Colocation leaders Equinix and NTT DATA deploy hybrid edge nodes within hyperscale campuses to retain enterprise tenants, yet Amazon Web Services and Microsoft continue vertical integration, signaling sustained pressure on third-party yields. Rapid liquid-cooling adoption, modular designs, and Arm CPU roadmaps emerge as key competitive differentiators.

Japan Data Center Server Industry Leaders

Dell Technologies Inc.

Hewlett Packard Enterprise

Cisco Systems Inc.

Lenovo Group Limited

Quanta Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cisco Systems activated new Tokyo 3 and Osaka 3 data centers to bolster its Secure Access fabric, improving redundancy for zero-trust migrations.

- October 2025: Hitachi and OpenAI formed a partnership to expand AI infrastructure, with Hitachi providing power distribution, cooling, and modular designs.

- August 2025: SAKURA Internet deployed 3,072 NVIDIA H200 GPUs to enhance generative AI services.

- June 2025: Internet Initiative Japan began Phase 3 construction at Shiroi campus, adding 10 megawatts expandable to 25 megawatts with liquid cooling.

Japan Data Center Server Market Report Scope

A data center server is basically a high-capacity computer without peripherals like monitors and keyboards. It is a hardware unit installed inside a rack, having a central processing unit (CPU), storage, and other electrical and networking equipment, making them powerful computers that deliver applications, services, and data to end-user devices.

The Japan Data Center Server Market Report is Segmented by Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers and CSPs, and Enterprise and Edge), Form Factor (Half-height Blades, Full-height Blades, and Quarter-height and Micro-blades), Application and Workload (Virtualization and Private Cloud, HPC, AI and ML and Data Analytics, Storage-centric, and Edge and IoT Gateways). Market Forecasts are Provided in Terms of Value (USD).

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| Half-height Blades |

| Full-height Blades |

| Quarter-height / Micro-blades |

| Virtualisation and Private Cloud |

| High-Performance Computing (HPC) |

| Artificial Intelligence/Machine Learning and Data Analytics |

| Storage-centric |

| Edge / IoT Gateways |

| By Tier Type | Tier 1 and 2 |

| Tier 3 | |

| Tier 4 | |

| By Data Center Size | Small Data Center |

| Medium Data Center | |

| Large Data Center | |

| Hyperscale Data Center | |

| By Data Center Type | Colocation Data Center |

| Hyperscalers Data Center/CSPs | |

| Enterprise and Edge Data Center | |

| By Form Factor | Half-height Blades |

| Full-height Blades | |

| Quarter-height / Micro-blades | |

| By Application / Workload | Virtualisation and Private Cloud |

| High-Performance Computing (HPC) | |

| Artificial Intelligence/Machine Learning and Data Analytics | |

| Storage-centric | |

| Edge / IoT Gateways |

Key Questions Answered in the Report

How large is the Japan data center server market in 2026?

The market reached USD 26.92 billion in 2026 and is on a trajectory to surpass USD 58 billion by 2031.

What is the forecast CAGR for servers deployed in Japanese data centers?

The compound annual growth rate is projected at 16.66% through 2031.

Which server form factor is growing fastest in Japan?

Quarter-height and micro-blade servers are expanding at a 17.87% CAGR as edge deployments proliferate.

Why are Tier 4 data centers becoming more popular in Japan?

Financial institutions and government agencies require higher uptime, driving Tier 4 capacity to grow at 17.21% annually.

How are power constraints shaping data center locations?

Limited grid capacity in Tokyo and Osaka diverts hyperscale builds to Hokkaido and Kyushu, where renewable energy is abundant and land costs are lower.

What cooling technologies are most in demand?

Direct liquid cooling and immersion systems are being adopted rapidly to support racks exceeding 100 kilowatts and to meet efficiency mandates.

Page last updated on: