China Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

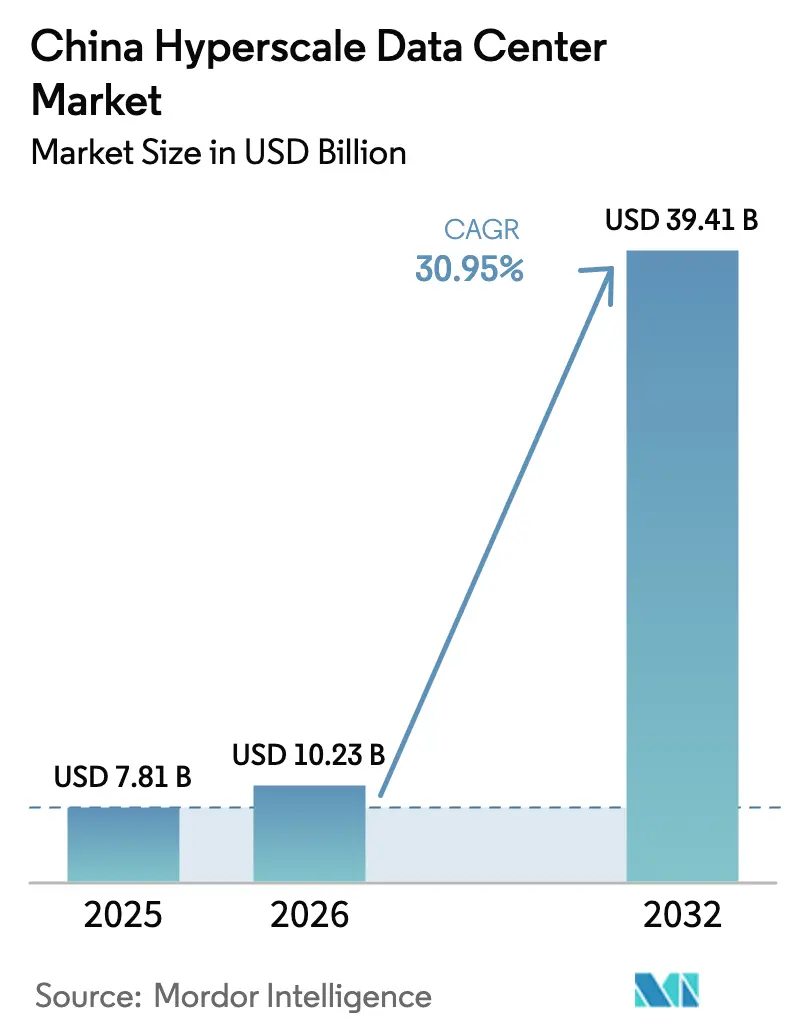

| Base Year Market Size (2025) | USD 7.81 Billion |

| Market Size (2026) | USD 10.23 Billion |

| Market Size (2032) | USD 39.41 Billion |

| Growth Rate (2026 - 2032) | 30.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Hyperscale Data Center Market Analysis by Mordor Intelligence

China hyperscale data center market size in 2026 is estimated at USD 10.23 billion, growing from 2025 value of USD 7.81 billion with 2031 projections showing USD 39.41 billion, growing at 30.95% CAGR over 2026-2031. Robust growth is supported by artificial-intelligence workload expansion, sovereign-computing mandates, and the Eastern Data Western Computing program that channels capacity toward renewable-rich western provinces. Total installed IT load will more than double from 5.327 thousand MW in 2025 to 11.942 thousand MW by 2031, reflecting a 14.40% volume CAGR. Liquid-cooled racks exceeding 100 kW are proliferating in Beijing-Tianjin-Hebei and the Yangtze Delta as operators adapt to large-language-model training requirements. Carrier initiatives such as China Mobile’s 6.7 EFLOPS supercomputing hub in Inner Mongolia underscore the AI-optimized buildout.

Key Report Takeaways

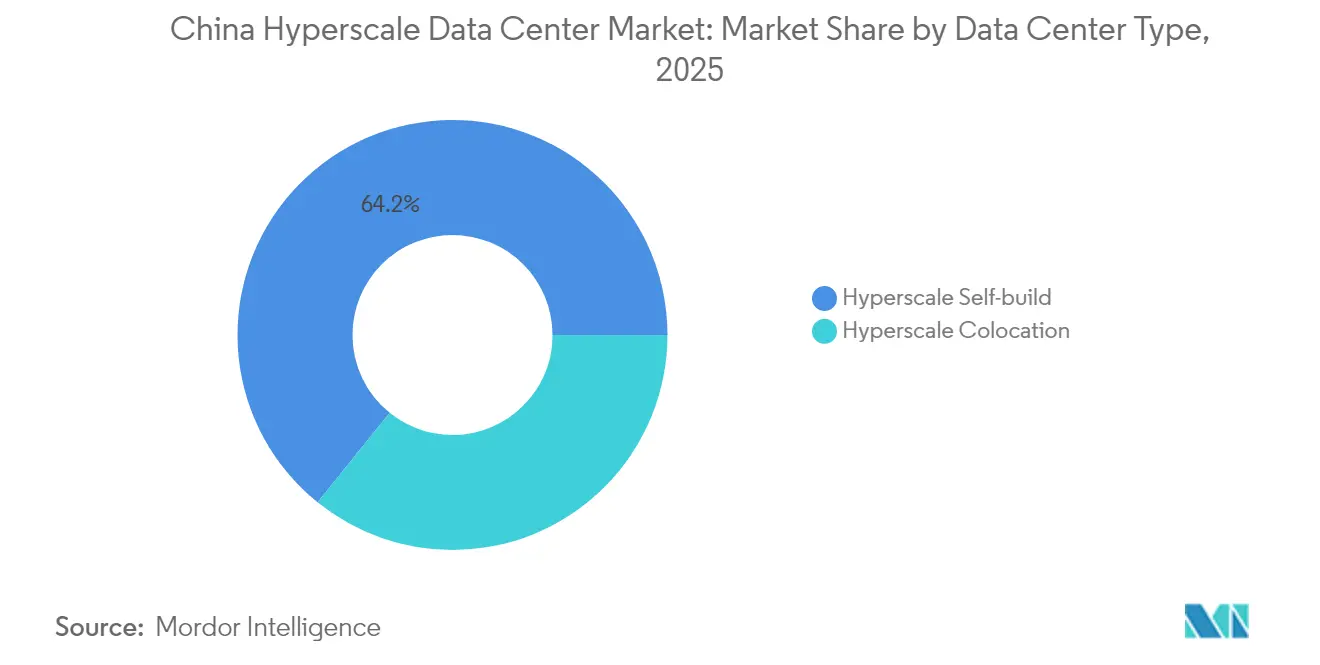

- By data center type, hyperscale self-build held 64.20% of the China hyperscale data center market share in 2025; hyperscale colocation is projected to expand at a 31.85% CAGR through 2031.

- By component, IT infrastructure accounted for 47.10% share of the China hyperscale data center market size in 2025, while DCIM/BMS solutions are forecast to grow at a 32.25% CAGR to 2031.

- By tier standard, Tier III facilities captured 72.30% revenue share in 2025; Tier IV deployments are advancing at a 31.10% CAGR through 2031.

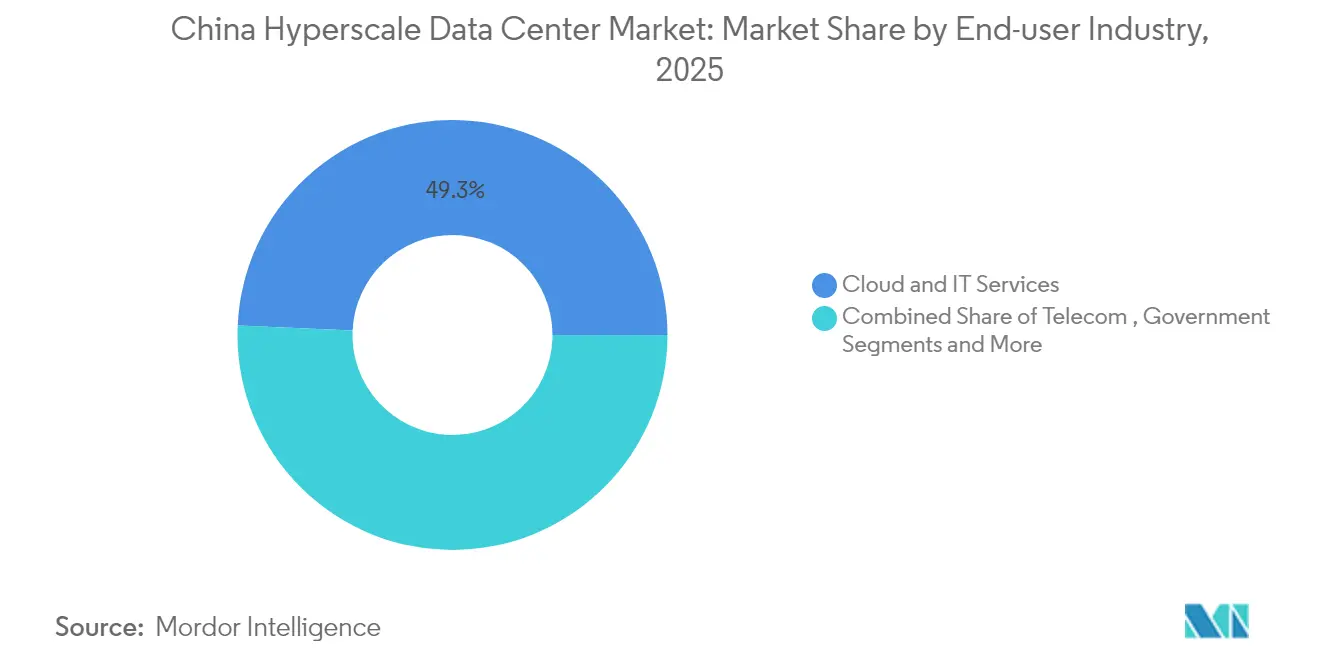

- By end-user industry, cloud and IT services held 49.30% share of the China hyperscale data center market size in 2025, whereas government demand is rising at a 32.60% CAGR to 2031.

- By data center size, massive sites (25-60 MW) led with 39.20% revenue share in 2025; mega-scale facilities (>60 MW) are recording the fastest CAGR at 33.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China contributes to a system defined not by any single country or region but by the interaction of many. The global hyperscale data center market data by Mordor Intelligence represents that combined structure.

China Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| GenAI and LLM training racks (>100 kW, liquid cooled) in Beijing-Tianjin-Hebei and Yangtze Delta | +8.5% | Beijing-Tianjin-Hebei, Yangtze Delta | Medium term (2-4 years) |

| State "New-Infrastructure" push extending hyperscale builds to 2nd-tier western cities | +6.2% | West China, Central China | Long term (≥ 4 years) |

| 400G/800G optical backbone upgrades cutting latency for real-time cloud apps | +4.8% | Global, with concentration in East China | Short term (≤ 2 years) |

| Renewable-energy quotas enabling GW-scale wind/solar data parks in Inner Mongolia and Gansu | +5.1% | Inner Mongolia, Gansu, West China | Long term (≥ 4 years) |

| Pilot SMR (small-modular-reactor) micro-nukes co-located with coastal campuses | +2.3% | Coastal regions, East China | Long term (≥ 4 years) |

| AI-for-semiconductor yield clusters demanding sovereign on-prem compute | +3.8% | Beijing-Tianjin-Hebei, Yangtze Delta | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GenAI and LLM training racks fuel liquid-cooling adoption

Liquid-cooling has shifted from pilot projects to mainstream practice as hyperscalers prepare for racks exceeding 100 kW. China plans 39 AI data centers hosting over 115,000 Nvidia Hopper GPUs, 70% of which will be sited in Xinjiang.[1]Tom’s Hardware, “China plans 39 AI data centers with 115,000 restricted Nvidia Hopper GPUs,” tomshardware.com Alibaba proved immersion-cooling viability at scale, showing the method can dissipate 10-20 times the heat of legacy air-cooled systems. ZutaCore’s dielectric direct-chip solution lowers cooling energy by 80% and supports 1,500 W GPUs, helping operators meet government PUE targets. Beijing-Tianjin-Hebei and the Yangtze Delta are early adopters as cloud providers try to shorten model-training cycles. Huawei’s CloudMatrix 384 architecture, delivering 300 petaflops in a single supernode, demonstrates how domestic vendors integrate liquid-cooling with AI accelerators.

Eastern Data Western Computing redistributes capacity

The national plan mandates that 60% of new compute resources be located in eight western hubs by 2025. China Mobile alone budgeted CNY 47.5 billion for computing-network infrastructure in 2024, establishing intelligent-computing centers across the west. Ningxia’s target to grow from 30,000 to 720,000 racks by 2025 illustrates the migration scale. Operators such as Tencent and Alibaba have expanded in Gui’an and Ulanqab, respectively, leveraging low-cost wind and solar power. National facilities already achieve up to 80% green-electricity usage, easing Tier-1 power congestion.

400G/800G optical backbone enables real-time cloud

China activated the world’s first 1,200G backbone spanning Beijing, Wuhan, and Guangzhou, cutting long-haul latency for AI inference.[3]Xinhua, “China launches ultra-high-speed next-generation Internet backbone,” xinhuanet.com Huawei and China Mobile built the globe’s largest 400G all-optical network, supporting deterministic bandwidth for GPU clusters. H3C’s 800G Ethernet test delivered 51.2 Tbps switching at 1.085 µs latency, confirming readiness for multi-regional AI training. China Broadnet’s deployment of Huawei OTN Kepler technology demonstrates carriers' shift toward photonic switching to meet the demands of cloud gaming and real-time analytics.

Renewable-energy quotas spur GW-scale parks

Government guidance sets an average PUE below 1.5 by 2025 and orders that green electricity use rise at least 10% annually. Inner Mongolia and Gansu together host gigawatt wind-solar bases that backstop hyperscale campuses.[2]Cambridge Core, “Low-carbon Frontier: Renewable Energy and the New Resource Boom in Western China,” cambridge.org Gansu’s Qingyang industrial park has attracted more than 300 enterprises, underscoring how data-center clustering builds local ecosystems. Advanced centers already meet the 80% green-power threshold, aided by direct-supply agreements with new energy farms. Analysts forecast that China hyperscale data center market operators will see energy savings flow through to total cost of ownership as renewable penetration rises.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Power-access quotas in Tier-1 metros (caps greater than 50 MW) | -4.2% | Beijing, Shanghai, Guangzhou, Shenzhen | Short term (≤ 2 years) |

| Water-use licensing limits on evaporative cooling in North-China plain | -3.1% | North China, Beijing-Tianjin-Hebei | Medium term (2-4 years) |

| GPU and HBM export-control shortages (A/H series) | -5.8% | Global, with concentration in AI clusters | Short term (≤ 2 years) |

| Mandatory 2027 carbon-peak forcing decommission of PUE > 1.6 halls | -2.9% | National, with focus on legacy facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power quotas cap Tier-1 expansion

Beijing, Shanghai, Guangzhou, and Shenzhen enforce strict allocation schemes that limit new builds over 50 MW and require PUE of 1.3 or lower. Shanghai capped standard-rack additions at 60,000 to balance grid stability and digital-economy growth. Coordinated policies in Guangdong target 1 million racks by 2025, yet confine projects to designated clusters to protect urban power security. These limits divert investment toward western provinces aligned with Eastern Data Western Computing. Operators respond by adopting liquid-cooling and on-site renewables to raise per-rack density inside constrained metros.

GPU export controls create supply bottlenecks

US rules restricting high-bandwidth-memory GPUs hinder rapid AI-cluster deployment, delaying model training schedules. Nvidia introduced H20, L20, and L2 chips tuned for the Chinese market to comply with regulations. Sales restarted in 2025, yet allocation remains tight, prompting cloud providers to prioritize domestic Ascend 910B GPUs. China Mobile’s Inner Mongolia hub runs 85% locally produced accelerators, illustrating substitution trends. Continued export uncertainty pushes operators to build inventory buffers and explore non-GPU architectures while the China hyperscale data center market absorbs higher procurement costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: self-build remains dominant as colocation accelerates

Self-builds controlled 64.20% revenue in 2025 because cloud majors seek bespoke architectures for AI clusters reaching 20-130 kW per cabinet. They integrate proprietary fabrics, liquid-cooling manifolds, and automation suites to optimize training throughput. Hyperscale colocation grows quickly at a 31.85% CAGR, giving enterprises immediate access to AI-ready rooms without multi-billion-yuan capex. Foreign-ownership liberalization in Beijing, Shanghai, and Shenzhen is expected to introduce global landlords, widening service choice. As a result, the China hyperscale data center market sees dual-track expansion: hyperscalers keep building owner-operated campuses, while colocation specialists scale suburban and western plots.

DCIM suites underpin both models. Operators deploy AI-driven orchestration that monitors power, coolant flow, and GPU utilization in real time. This operational maturity attracts financial investors; GDS’s C-REIT drew orders 166 times subscribed, signalling confidence in stable cash flows. Over the forecast period, the China hyperscale data center industry will balance the agility of colocation with the control of self-builds, creating hybrid capacity procurement strategies.

By Component: IT infrastructure leads and DCIM/BMS surges

Servers, storage, and GPUs represented 47.10% of spending in 2025. China Mobile procured 2,454 AI servers in the 2023-2024 cycle, reflecting urgency to resource knowledge-graph and video-analysis workloads. Network upgrades to 400G/800G Ethernet switches, such as IEIT SYSTEMS’ X400, lift east-west traffic capacity to 102.4 Tbps. Electrical gear—PDUs and UPS—follows server density upward, while direct-chip cooling skids, cold plates, and immersion tanks dominate mechanical budgets.

DCIM/BMS grows fastest at 32.25% CAGR because facilities exceeding 100 kW per rack require telemetry granularity unmatched by legacy SCADA tools. Huawei’s intelligent-analysis network locates faults automatically and advises energy-saving actions, shrinking mean-time-to-repair. As AI cluster complexity rises, advanced management software becomes foundational, ensuring the China hyperscale data center market operates within energy and carbon constraints.

By Tier Standard: Tier III dominates yet Tier IV accelerates

Tier III halls occupied 72.30% of floor space in 2025, offering 99.982% availability at moderate cost. Operators enhance basic Tier III by doubling backup lines and adding closed-loop liquid-cooling to accommodate AI loads, yielding “Tier III+” specifications. Mission-critical inference and financial records prompt Tier IV adoption, expanding at 31.10% CAGR. China Mobile’s Inner Mongolia campus exemplifies Tier IV design with dual power grids and N+2 chilled-water capacity. Regulatory frameworks in banking and government also steer deployments toward Tier IV equivalence, further diversifying the China hyperscale data center market.

By End-user Industry: cloud services lead, government demand surges

Cloud and IT services captured 49.30% revenue in 2025 as Alibaba, Huawei, Tencent, and Baidu scaled large-model inference platforms. China’s cloud-infrastructure spending will rise 15% to USD 11.1 billion in 2025, ensuring steady occupancy rates. The government segment, expanding at 32.60% CAGR, aggregates ministry systems onto unified computing backbones, following the “1+N+N+1” model championed by H3C. BFSI upgrades modernize core ledgers for digital yuan settlement, while manufacturers implement predictive-maintenance algorithms that cut downtime by 70 %, echoing Midea Group’s achievements. This diversified user portfolio underpins long-term growth for the China hyperscale data center industry.

By Data Center Size: massive sites lead, mega-scale accelerates

Massive campuses of 25-60 MW held a 39.20% stake in 2025, balancing modular replication with economies of scale. Operators favour this range to match grid-connection quotas while leaving headroom for phased expansion. Mega-facilities above 60 MW progress fastest at 33.10% CAGR. ByteDance’s USD 614 million Shanxi build showcases mega-scale economics where one campus aggregates compute power otherwise spread across many city blocks. Large facilities below 25 MW continue to serve edge analytics and provincial e-government but are losing revenue share as the China hyperscale data center market consolidates into multi-module giants.

Geography Analysis

East China remains the principal hub by value, anchored by Shanghai’s financial ecosystem and Zhejiang’s e-commerce networks. Power quotas spur advanced cooling and offshore-wind solutions, such as HiCloud’s underwater unit near Shanghai that sidesteps land constraints. North China records the fastest CAGR as Inner Mongolia pairs cool climate with wind-solar abundance. China Mobile’s Hohhot hub aligns with policy that channels 60% of new racks westward, demonstrating scale with 6.7 EFLOPS compute. Beijing sustains premium demand from AI research institutes, reinforcing inter-regional traffic growth on upgraded optical backbones.

South China grows steadily thanks to Guangdong’s plan for 1 million racks by 2025, leveraging proximity to Hong Kong for cross-border cloud trade. West China benefits from Qingyang’s industrial park attracting 300 firms under east-data-west-computing incentives. Central China emerges as a transit node; Zhengzhou targets a USD 56 billion digital economy by 2025, catalysing prefabricated data-center clusters near fibre crossroads . These regional dynamics confirm that the China hyperscale data center market diversifies geographically while staying tethered through national 1.2-terabit backbones.

The hyperscale data center market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Middle East, Africa, and South America. This is complemented by country-specific insights for Taiwan, South Korea, Saudi Arabia, South Africa, Chile, and Canada, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Market concentration is moderate. Alibaba Cloud, Huawei Cloud, Tencent Cloud, and Baidu AI Cloud account for 71% of public-cloud revenue, securing anchor-tenant status at most hyperscale sites. State-owned operators—China Mobile, China Telecom, China Unicom—exploit network assets to win government and enterprise contracts, intensifying bidding wars. Data-center specialists like GDS, Chindata, and VNET differentiate via AI-ready colocation, renewable-energy sourcing, and capital-markets innovation such as China’s first data-center C-REIT.

Strategic moves include vertical integration—Alibaba pledged USD 53 billion over three years for global AI infrastructure—and horizontal alliances, with GDS opening suburban Tianjin capacity through a tripartite deal with two telcos. Emerging disruptors pursue niche technologies: HiCloud experiments with submerged modules, while Zhitiao Network patents distributed-storage acceleration. Technology adoption speed, rather than asset count, is becoming the decisive advantage across the Chinese hyperscale data center industry.

China Hyperscale Data Center Industry Leaders

Alibaba Cloud

Tencent Holdings Ltd.

Huawei Technologies Co., Ltd.

GDS Holdings

Chindata Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: China Mobile acquired a 15% stake in HKBN, strengthening Hong Kong connectivity for hyperscale operations.

- July 2024: GDS Holdings completed its C-REIT IPO on the Shanghai Stock Exchange, raising CNY 1.933 billion

- June 2024: Huawei Cloud unveiled Pangu 5.5 models and AI Cloud Service using CloudMatrix 384 supernodes.

- June 2025: Alibaba Cloud announced a second South Korea data center by the end of June 2025

China Hyperscale Data Center Market Report Scope

Hyperscale data centers, also known as Enterprise colocation/cloud hyperscale facilities, are large-scale infrastructures owned and managed by the companies they support. These centers deliver a wide range of scalable applications and storage services to meet the needs of individuals and businesses. Designed for efficiency, they house thousands of servers alongside critical hardware like routers, switches, and storage disks. To ensure seamless operations, these facilities are equipped with advanced support systems, including power and cooling solutions, uninterruptible power supplies (UPS), and air distribution networks.

The China Hyperscale Datacenter Market is Segmented by Data Center Type (Hyperscale Colocation, Enterprise/Hyperscale Self Build), By Service Type (IaaS ( Infrastructure-as-a-Service), PaaS ( Platform-as-a-Service), SaaS( Software-as-a-Service)), By End User (Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce, Other End User). The Report Offers the Market Size and Forecasts for all the Above Segments in Terms of USD (millions).

| Hyperscale Self-build |

| Hyperscale Colocation |

| IT Infrastructure | Server Infrastructure |

| Storage Infrastructure | |

| Network Infrastructure | |

| Electrical Infrastructure | Power Distribution Unit |

| Transfer Switches and Switchgear | |

| UPS Systems | |

| Generators | |

| Other Electrical Infrastructure | |

| Mechanical Infrastructure | Cooling Systems |

| Racks | |

| Other Mechanical Infrastructure | |

| General Construction | Core and Shell Development |

| Installation and Commissioning | |

| Design Engineering | |

| Fire, Security and Physical Protection | |

| DCIM / BMS Solutions |

| Tier III |

| Tier IV |

| Cloud and IT Services |

| Telecom |

| Media and Entertainment |

| Government |

| BFSI |

| Manufacturing |

| E-Commerce |

| Other End-users |

| Large ( Less than or equal to 25 MW) |

| Massive (Greater than 25 MW and Less than equal to 60 MW) |

| Mega (Greater than 60 MW) |

| By Data Center Type | Hyperscale Self-build | |

| Hyperscale Colocation | ||

| By Component | IT Infrastructure | Server Infrastructure |

| Storage Infrastructure | ||

| Network Infrastructure | ||

| Electrical Infrastructure | Power Distribution Unit | |

| Transfer Switches and Switchgear | ||

| UPS Systems | ||

| Generators | ||

| Other Electrical Infrastructure | ||

| Mechanical Infrastructure | Cooling Systems | |

| Racks | ||

| Other Mechanical Infrastructure | ||

| General Construction | Core and Shell Development | |

| Installation and Commissioning | ||

| Design Engineering | ||

| Fire, Security and Physical Protection | ||

| DCIM / BMS Solutions | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | Cloud and IT Services | |

| Telecom | ||

| Media and Entertainment | ||

| Government | ||

| BFSI | ||

| Manufacturing | ||

| E-Commerce | ||

| Other End-users | ||

| By Data Center Size | Large ( Less than or equal to 25 MW) | |

| Massive (Greater than 25 MW and Less than equal to 60 MW) | ||

| Mega (Greater than 60 MW) | ||

Key Questions Answered in the Report

What is the current value of the China hyperscale data center market?

The market is valued at USD 10.23 billion in 2026.

How quickly is the market expected to grow?

It is projected to post a 30.95% CAGR and reach USD 39.41 billion by 2031.

Which segment expands fastest?

Hyperscale colocation shows the highest projected CAGR at 31.85% through 2031.

Why are western provinces attracting data centers?

Policy incentives and abundant renewable energy under Eastern Data Western Computing shift 60% of new capacity westward.

How are power-density challenges addressed?

Operators deploy liquid-cooling technologies capable of handling racks above 100 kW and adopt AI-driven DCIM for resource management.

What impact do GPU export controls have?

Restrictions slow high-performance cluster deployments, prompting greater use of domestic GPU alternatives and inventory strategies.

Page last updated on: