Japan HVAC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

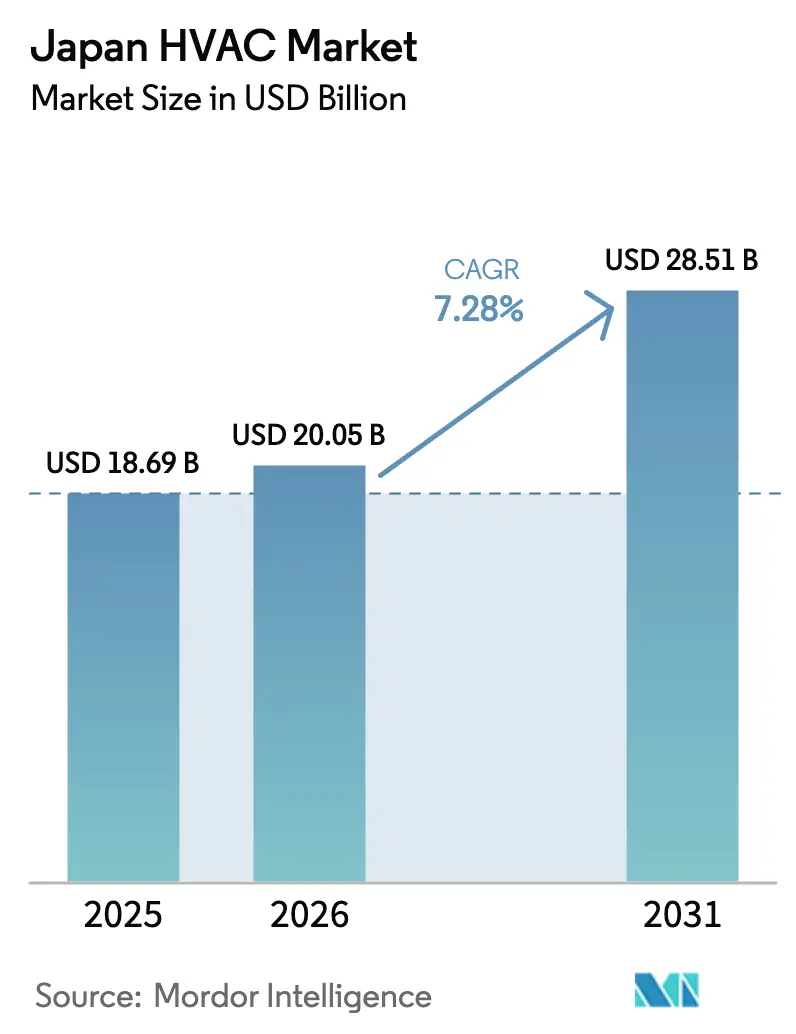

| Base Year Market Size (2025) | USD 18.69 Billion |

| Market Size (2026) | USD 20.05 Billion |

| Market Size (2031) | USD 28.51 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

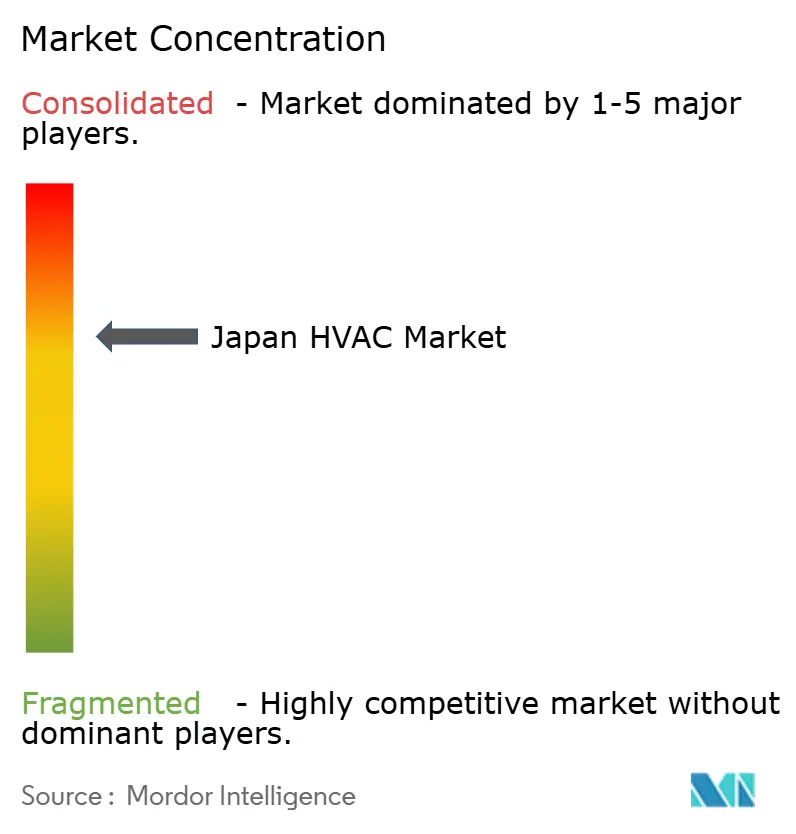

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan HVAC Market Analysis by Mordor Intelligence

The Japan HVAC market size is expected to grow from USD 18.69 billion in 2025 to USD 20.05 billion in 2026 and is forecast to reach USD 28.51 billion by 2031 at 7.28% CAGR over 2026-2031. Demand momentum is powered by the country’s 2050 carbon-neutral target, the Green Growth Strategy, and a nationwide shift toward high-efficiency electric heat-pump technology. [1]Ministry of Economy, Trade and Industry, "Green Growth Strategy Through Achieving Carbon Neutrality in 2050", meti.go.jp Tighter Top Runner efficiency standards, accelerating ZEB/ZEH retrofits, and natural-refrigerant innovation further reinforce growth. Opportunity hotspots include compact systems engineered for dense urban buildings, data-center cooling platforms designed for AI workloads, and service contracts built around predictive maintenance. Competitive intensity remains high as domestic leaders push R&D aimed at energy savings, smart controls, and refrigerant transition, while labour shortages and rural grid bottlenecks continue to temper near-term installation volumes.

Key Report Takeaways

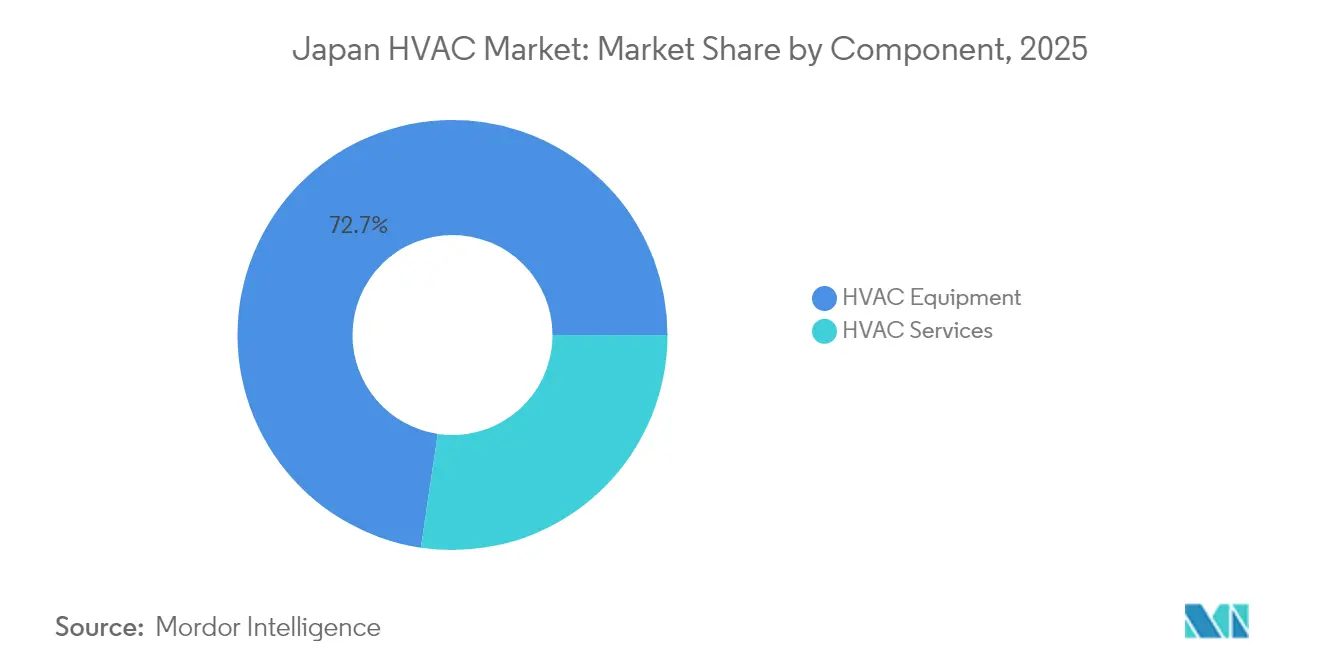

- By component, HVAC equipment led with 72.65% of the Japan HVAC market share in 2025, while services are forecast to grow at an 8.62% CAGR to 2031.

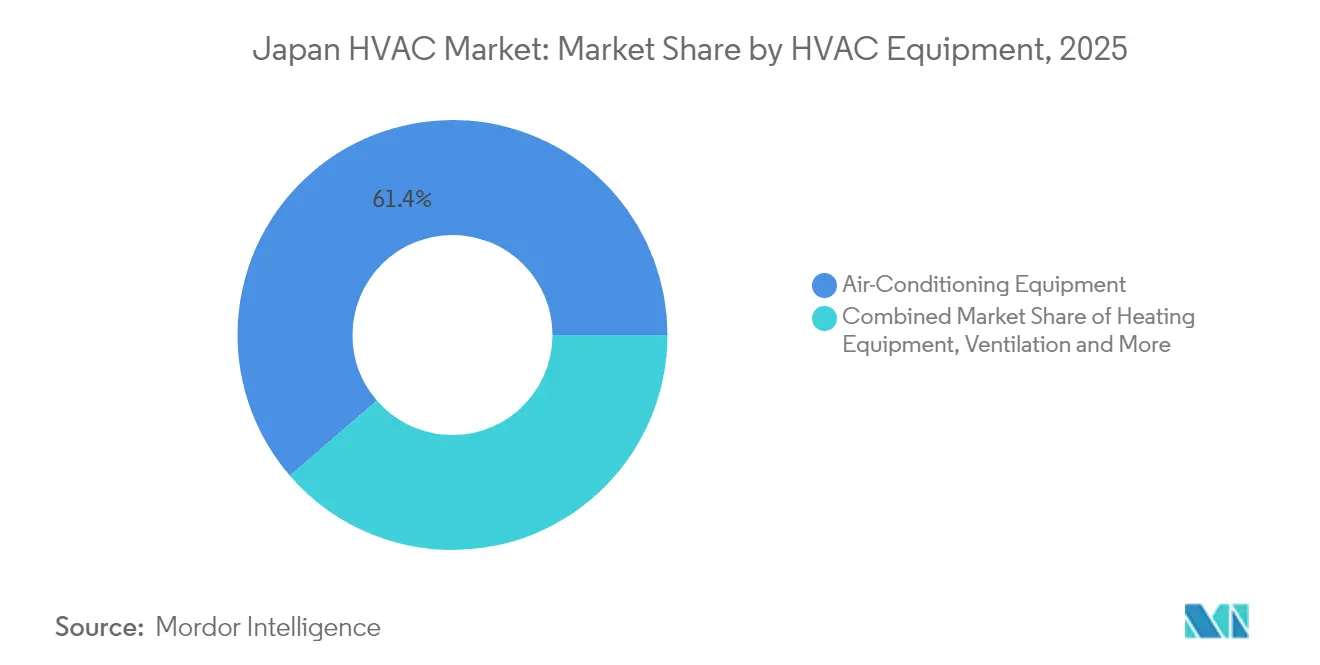

- By HVAC equipment type, air-conditioning accounted for 61.35% share of the Japan HVAC market size in 2025; heat pumps are projected to expand at a 9.12% CAGR through 2031.

- By end-user industry, residential commanded 44.55% revenue in 2025; data centers & cleanrooms record the fastest 8.42% CAGR between 2026-2031.

- By region, Kanto held 34.65% of the Japan HVAC market in 2025; Kyushu & Okinawa are advancing at a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive "ZEB/ZEH" (Zero-Energy Building/Home) mandates accelerating high-efficiency HVAC retrofits | +1.5% | National, with concentration in urban centers | Medium term (2-4 years) |

| Tokyo metropolitan heat-island mitigation policies boosting district cooling adoption | +0.9% | Kanto (Greater Tokyo) | Medium term (2-4 years) |

| Rapid electrification of home heating spurred by Japan's Green Growth Strategy | +1.2% | National, with early adoption in Kanto and Kinki regions | Long term (≥ 4 years) |

| Shift toward CO₂ and propane natural-refrigerant systems after F-gas phasedown | +0.7% | National | Medium term (2-4 years) |

| 2025 Osaka World Expo construction wave creating temporary HVAC demand spike | +0.6% | Kinki (Kansai), with spillover to adjacent regions | Short term (≤ 2 years) |

| Aging population driving demand for air-quality-focused HVAC in healthcare and senior housing | +0.5% | National, with concentration in urban and suburban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive ZEB / ZEH mandates accelerating high-efficiency HVAC retrofits

ZEB and ZEH policies require all new public buildings to reach zero-energy status by 2030. They have lifted demand for advanced heat pumps and smart control platforms that connect with building energy-management systems. ZEB-ready floor space grew 43% year on year in 2024, driving a cascading effect across component suppliers. Subsidies, certification schemes, and SHASE technical guidance simplify compliance, while dual-track standards emphasize both passive design and renewable integration. The result is a clear preference for HVAC units delivering top-quartile COP under Japan’s humid conditions, giving domestic manufacturers an edge.[2] World Business Council for Sustainable Development

Tokyo metropolitan heat-island mitigation policies boosting district cooling adoption

The ‘Kaze-no-Michi’ ventilation-path framework underpins a neighbourhood-scale cooling shift. Connections to district systems in central Tokyo rose 27% since 2024, reflecting commercial landlords’ move away from stand-alone chillers. New thermal-environment simulation tools from the National Institute for Land and Infrastructure Management enable hotspot-specific deployment, aligning HVAC load with urban-planning objectives. Health considerations for an ageing population add urgency, tying HVAC investments to public-wellness outcomes.

Rapid electrification of home heating spurred by the Green Growth Strategy

Residential adoption of electric heat pumps climbed 38% in 2024 on the back of policy incentives and rising gas-price volatility. Prefectures with strong distribution networks lead uptake, while grid-constrained rural localities adopt hybrid units that switch fuels during peak demand. Compact, humidity-tolerant Japanese heat-pump models now match European efficiency with 40% less footprint, and thermal-storage add-ons support demand-response events. The shift embeds HVAC hardware within smart-home ecosystems, deepening aftermarket software revenue potential.

Shift toward CO₂ and propane natural-refrigerant systems after the F-gas phasedown

More than 10,200 commercial CO₂ heat-pump water-heater units were in service by end-2024, evidencing technical maturity. Manufacturers have raised CO₂ system efficiency to parity with HFC benchmarks, clearing the last adoption hurdle. Market bifurcation sees CO₂ dominate commercial refrigeration while propane gains residential share thanks to workable flammability controls. Product-portfolio realignment is now a core competitive differentiator as firms pivot R&D to natural-refrigerant-optimised compressors and heat-exchangers.[3]Japan Refrigeration and Air Conditioning Industry Association, "Current status of Japan's legislation on F-gases and RACHP using Low-GWP Refrigerants", jraia.or.jp

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction labour shortage | −0.8% | National, acute in rural zones | Short term (≤ 2 years) |

| High upfront cost of inverter heat pumps | −0.6% | National, stronger in price-sensitive areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction-sector labour shortage inflating HVAC installation lead times

The job-offer-to-seeker ratio hit 1.62 in 2024, lengthening installation queues by 30%. Skilled-technician scarcity pushes up wages and compresses contractor margins. Prefabricated HVAC modules and drone-enabled site mapping mitigate delays, cutting onsite hours by 40% yet cannot fully close the gap. Project owners are sequencing retrofits earlier in construction schedules to hedge labour risk.

High cost of inverter-based heat-pump solutions versus legacy gas boilers

Advanced heat-pump units priced at a 20% to 40% premium over gas alternatives challenge adoption in cost-sensitive prefectures. Although lifetime savings from superior efficiency are positive, budget-constrained residential buyers often seek subsidies or hybrid arrangements. Manufacturers promote financing bundles and performance-contracting models that share energy-saving returns to overcome the price barrier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Equipment dominance meets service acceleration

HVAC equipment commanded 72.65% of the Japan HVAC market in 2025, reflecting domestic engineering leadership and constant Top Runner pressure for higher efficiency. Air-conditioning, heating, and ventilation products all benefited from consumer expectations for precise indoor comfort. Continuous R&D investment has lifted seasonal performance ratings across product lines, sustaining the equipment revenue core.

The service segment is poised for faster expansion at an 8.62% CAGR through 2031 as the installed base ages and digital diagnostics move maintenance from reactive to predictive. Service providers bundle IoT sensors with AI analytics to flag faults before failure, which reduces downtime and positions multiyear performance contracts as value-add propositions. This shift opens recurring-revenue streams that stabilize cash flow across economic cycles.

By HVAC Equipment: Air-conditioning leads while heat pumps surge

Air-conditioning contributed 61.35% of the Japan HVAC market size in 2025 on the back of humid summers, high urban density, and cultural expectations for thermal precision. Domestic shipments of room units reached 794,808 in April 2025, up 15.2% year on year, with a shipment value of JPY 74.71 billion (USD 498.7 million). Smart controls and connectivity with home-automation hubs are now standard selling points.

Heat pumps record the fastest 9.12% CAGR forecast, propelled by electrification policy, compact design advances, and growing cold-climate efficiency. Daikin plans to quadruple output to 1 million air-to-water units by 2025.Scale-up is lowering per-unit costs, narrowing the price gap versus gas boilers, and accelerating substitution.

By End-user Industry: Residential base meets commercial innovation

Residential buyers held 44.55% of the Japan HVAC market share in 2025, driven by near-universal penetration of room air-conditioners and growing adoption of heat-pump water heaters. The ZEH program steers households toward net-zero targets, boosting demand for HVAC units that integrate with rooftop photovoltaics and battery storage. Indoor-air-quality features such as PM2.5 filtration appeal to Japan’s health-conscious homeowners.

Data centers and cleanrooms inside the industrial mix post the fastest 8.42% CAGR to 2031. NEC’s facilities achieved a 1.16 PUE using indirect free cooling and magnetic-bearing chillers, cutting power use by 12%. Semiconductor-sector expansion amplifies cleanroom orders that require ultra-tight temperature and particulate control, rewarding suppliers with deep application know-how.

Geography Analysis

Regional HVAC demand mirrors Japan’s climatic diversity, urbanisation patterns, and grid readiness. Kanto’s 34.65% share benefits from concentrated commercial floor space, the highest share of super-high-rise buildings, and municipal mandates that favour advanced cooling systems. University of Tokyo research finds compact towers run lower surface temperatures than mid-rise blocks, guiding product sizing and airflow management. Targeted cooling corridors in Nakano, Nerima, and Suginami drive localised procurement surges as developers comply with ventilation-path zoning.

Kyushu and Okinawa’s 9.05% CAGR reflects subtropical humidity, industrial cluster growth, and support for renewable energy policy. On-site solar complements heat-pump adoption in factories and resorts, while semiconductor fabs and new data hubs require precision HVAC with redundancy to ensure uptime. The tourism sector adds year-round pressure on occupancy, amplifying the efficiency imperatives for hotel owners facing rising power tariffs.

Kinki gains a temporary lift from Expo 2025 Osaka, a project expected to inject JPY 2 trillion (USD 13.4 billion) and draw 30 million visitors. Tohoku and Hokkaido face extended heating seasons and network constraints that slow all-electric transitions, prompting interest in hybrid systems. Chubu’s manufacturing concentration sustains demand for process-specific HVAC, while Chugoku and Shikoku exhibit steady residential replacement cycles. Across regions, about 60% of buildings predate the 1979 Energy Saving Act, ensuring a robust retrofit pipeline.

Competitive Landscape

The Japan HVAC market is concentrated around domestic champions whose combined expertise, patent portfolios, and channel strength reinforce entry barriers. Daikin leads by refocusing on core air-conditioning and divesting non-strategic units, a realignment that sharpens resource allocation. Mitsubishi Electric and Panasonic leverage integrated-electronics capability to advance inverter controls and IoT connectivity, sustaining differentiation on system intelligence and energy management.

Intense innovation cycles fuel R&D outlays directed at refrigerant transition and miniaturisation suited to cramped urban installations. Players expand M-and-A activity to capture overseas growth as the mature home market tightens. Examples include Daikin’s Goodman deal and Mitsubishi Electric’s De’Longhi acquisition, both aimed at technology stacking and distribution footprint extension. IoT and AI integration transform HVAC units into data-rich assets, attracting collaborations between hardware firms and digital platform providers.

Self-reported shipment statistics from nine large manufacturers underscore consolidation while acknowledging niche specialists in areas such as healthcare, HVAC, and energy-storage-integrated systems. Competitive focus now tilts toward lifecycle services and outcome-based contracting, which lock in clients and stabilise margins against raw-material cost swings.

Japan HVAC Industry Leaders

-

Daikin Industries, Ltd.

-

Mitsubishi Electric Corporation

-

Hitachi Ltd.

-

Panasonic Corporation

-

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Daikin Industries reported record sales of EUR 28 billion (USD 30.2 billion), underscoring its scale advantage and sustained investment in efficient technologies.

- April 2025: Daikin unveiled plans to create an Ice Cool Spot at Expo 2025 Osaka using ice-thermal storage and solar power.

- April 2025: Nikkei noted intensified expansion by Japanese HVAC makers in India’s fast-growing air-conditioning market.

- April 2025: JRAIA reported a 15.2% rise in domestic room-air-conditioner shipments to 794,808 units valued at JPY 74.71 billion (USD 498.7 million).

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Japan heating, ventilation and air-conditioning (HVAC) market as revenue generated within the country from the sale of new comfort-conditioning equipment, heating units, air-conditioning systems, dedicated ventilation/indoor-air-quality devices, and the full suite of installation, maintenance, and efficiency-retrofit services that keep those assets operational across residential, commercial, and selected light-industrial facilities.

Scope exclusion: refrigeration for cold-chain logistics and on-vehicle climate systems sits outside this assessment.

Segmentation Overview

-

By Component

- HVAC Equipment

-

HVAC Services

- Installation and Commissioning

- Maintenance and Repair (AMC)

- Energy-Efficiency and Performance Contracting

-

By HVAC Equipment

-

Heating Equipment

- Heat Pumps (Air-Source, Ground-Source)

- Boilers and Furnaces

-

Air-Conditioning Equipment

- Room Air Conditioners

- Packaged / Ducted Split Units

- Chillers and VRF Systems

-

Ventilation and IAQ Equipment

- Air Handling Units and ERVs

- Fans, Blowers and Ducting

-

Heating Equipment

-

By End-user Industry

- Residential

-

Commercial

- Offices and Co-working Spaces

- Retail and Shopping Malls

- Hospitality and Entertainment Facilities

- Healthcare and Senior-care Facilities

- Educational Institutions

-

Industrial

- Manufacturing Plants

- Data Centers and Cleanrooms

-

By Region

-

Hokkaido

- Tohoku

- Kanto (Greater Tokyo)

- Chubu

- Kinki (Kansai)

- Chugoku

- Shikoku

- Kyushu and Okinawa

-

Hokkaido

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Japanese OEM engineers, facility managers in Tokyo, Osaka, and Fukuoka, and specialist installers that service VRF and inverter heat-pump fleets. These conversations confirmed typical selling prices, retrofit labor ratios, and region-specific demand swings, letting us fine-tune assumptions surfaced during desk work.

Desk Research

We began with granular trade statistics from Japan Customs and the Ministry of Economy, Trade and Industry, which publish shipment volumes and factory gate prices for room air-conditioners, heat pumps, boilers, and ventilation fans. Building-code releases from the Ministry of Land, Infrastructure and Transport clarified ZEH and ZEB adoption targets, while regional power utilities supplied tariff trends that influence running-cost payback. Additional context flowed from trade bodies such as the Heat Pump & Thermal Storage Technology Center of Japan, JRAIA annual outlooks, peer-reviewed studies in Energy & Buildings, plus company filings available via D&B Hoovers and Dow Jones Factiva. The sources cited above illustrate our desk work; many others supported data validation.

Market-Sizing & Forecasting

A top-down model converts production and trade data into an installed-base inventory that is linked to new-build floor space, heat-pump penetration, average equipment life, and household AC saturation. Sampled supplier roll-ups and distributor channel checks act as a selective bottom-up cross-check. Key variables include domestic room-AC shipments, heat-pump unit imports, ZEH completion starts, average cooling-degree-days, electricity price index, and VRF share of commercial projects. Multivariate regression projects each driver through 2030, and a scenario layer tests policy or price shocks. Where bottom-up estimates diverge, gap ratios are redistributed using rolling three-year averages of ASP movement.

Data Validation & Update Cycle

Outputs pass through anomaly screens, senior-analyst peer review, and variance reconciliation against independent KPIs before sign-off. We refresh models every twelve months, revisiting them sooner if material policy, weather, or merger events shift market dynamics.

Why our Japan HVAC Baseline earns confidence

Published Japanese HVAC figures often differ because firms choose distinct product baskets, service inclusions, and currency treatments.

Key gap drivers include whether ventilation services and retrofit labor are counted, the handling of ductwork fabrication, and the inflation adjustment applied to yen data before conversion. Faster or slower forecast refresh also widens spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.69 B (2025) | Mordor Intelligence | - |

| USD 9.37 B (2023) | Regional Consultancy A | Omits ventilation and retrofit spend; equipment-only scope |

| USD 20.91 B (2024) | Industry Journal B | Adds ductwork and building-automation revenue; uses nominal-rate FX without inflation realignment |

The comparison shows how disciplined scope setting, driver selection, and an annual refresh give Mordor's numbers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Japan HVAC market in 2026?

The Japan HVAC market is valued at USD 20.05 billion in 2026.

How fast is the Japan HVAC market expected to grow through 2031?

The market is projected to expand at a 7.28% CAGR, reaching USD 28.51 billion by 2031.

Which equipment segment holds the largest Japan HVAC market share?

Air-conditioning equipment led with 61.35% of Japan HVAC market size in 2025.

Why are heat pumps gaining traction in Japan’s HVAC landscape?

Policy-driven electrification, compact design improvements and better cold-climate performance support a 9.12% CAGR for heat pumps from 2026-2031.

Which region is forecast to be the fastest-growing Japan HVAC market?

Kyushu and Okinawa are set to record a 9.05% CAGR as industrial relocation and renewable-energy synergies spur demand.

How are labour shortages affecting HVAC installations in Japan?

Skilled-worker scarcity has extended installation lead times by 30%, prompting wider use of prefabricated modules and digital productivity tools.

Page last updated on: