Japan Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

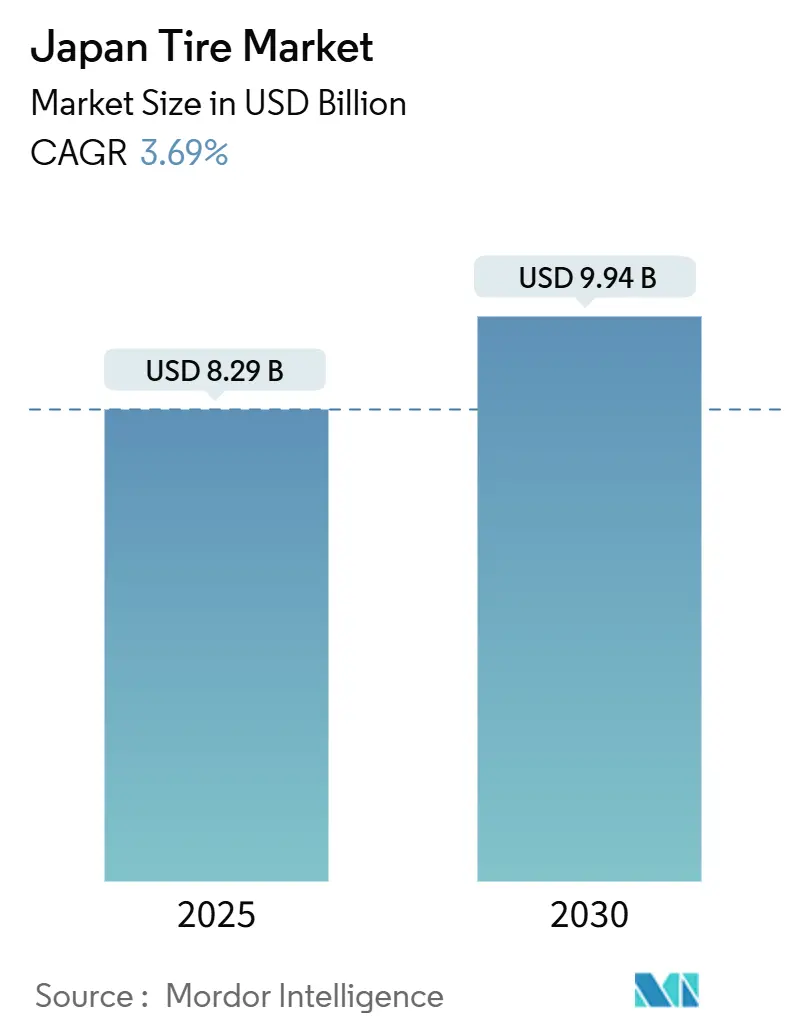

| Market Size (2025) | USD 8.29 Billion |

| Market Size (2030) | USD 9.94 Billion |

| Growth Rate (2025 - 2030) | 3.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Tire Market Analysis by Mordor Intelligence

The Japanese tire market size stood at USD 8.29 billion in 2025 and is expected to advance to USD 9.94 billion by 2030, registering a 3.69% CAGR over the forecast period. Rising SUV and crossover registrations, accelerating battery-electric vehicle (BEV) sales, and stricter fuel-efficiency rules are reshaping specifications, rim-size preferences, and rubber compound choices across every distribution channel. Larger-diameter fitments above 20 inches, low-rolling-resistance summer compounds, and smart-tire sensor packages are capturing a growing share of replacement spending, while OEM demand expands fastest as automakers formalize long-term supply partnerships to meet WLTP-aligned efficiency targets. Raw-material cost volatility and warm-winter variability continue to squeeze operating margins, yet industry leaders maintain pricing power through premium positioning and vertically integrated retail strategies.

Key Report Takeaways

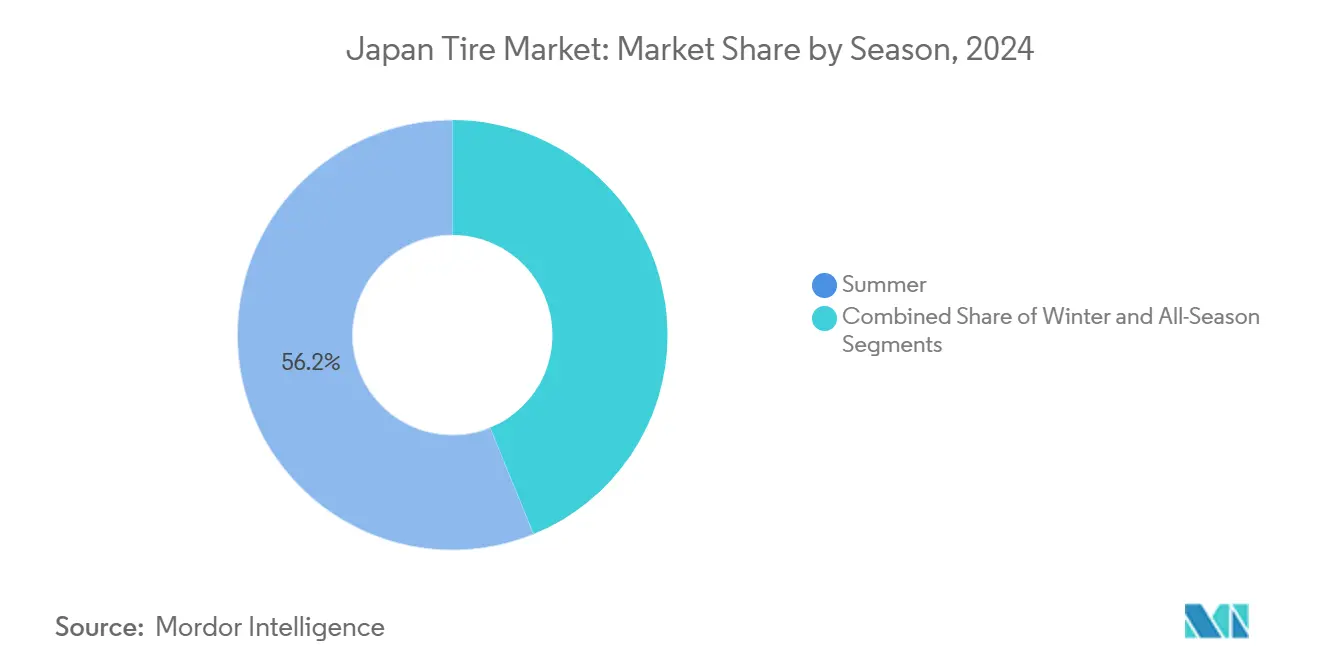

- By season, summer tires led with 56.17% revenue share of the Japanese tire market in 2024; all-season products are projected to expand at a 4.61% CAGR through 2030.

- By tire design, radial construction held 97.03% of the Japanese tire market demand in 2024, while non-pneumatic concepts are forecasted to log the quickest 7.64% CAGR.

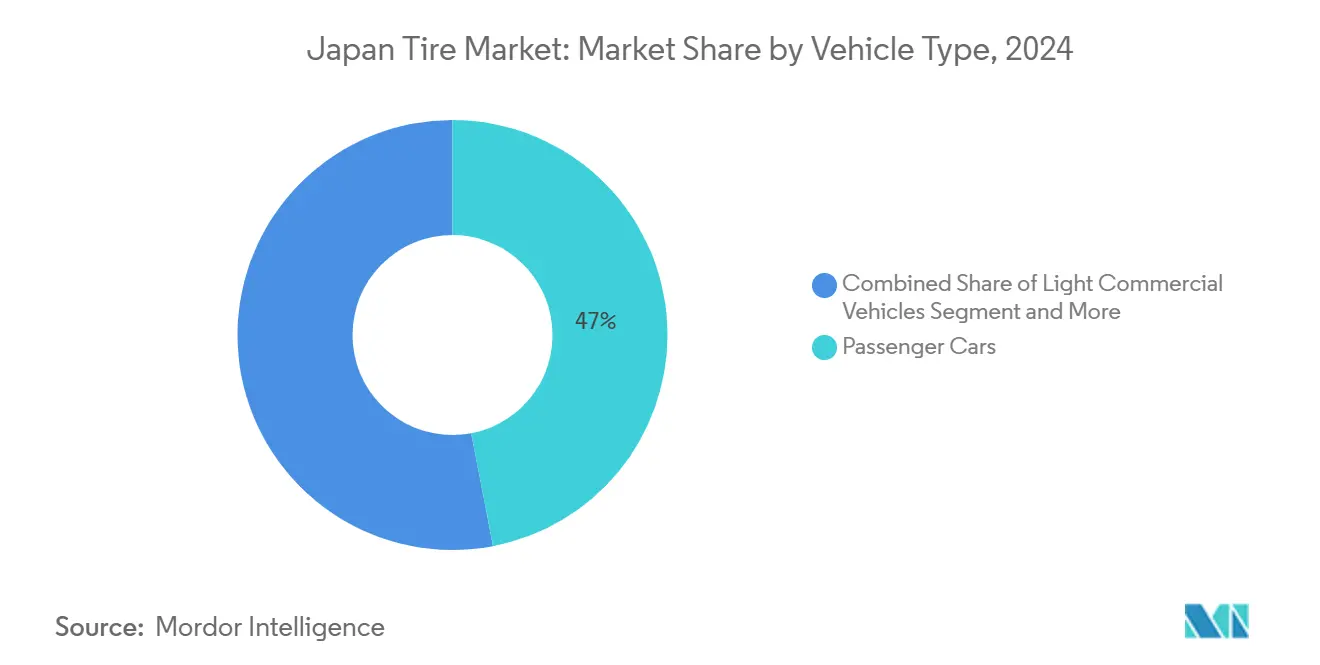

- By vehicle type, passenger cars captured 46.98% of the Japanese tire market's 2024 sales, and are expected to post the highest 5.13% CAGR to 2030.

- By application, on-road uses dominated with an 89.88% stake in the Japanese tire market in 2024; off-road fitments are projected to grow at a 3.84% CAGR.

- By end user, the aftermarket commanded 62.30% of the Japanese tire market's 2024 turnover, whereas OEM channels are projected to record the swiftest 5.24% CAGR.

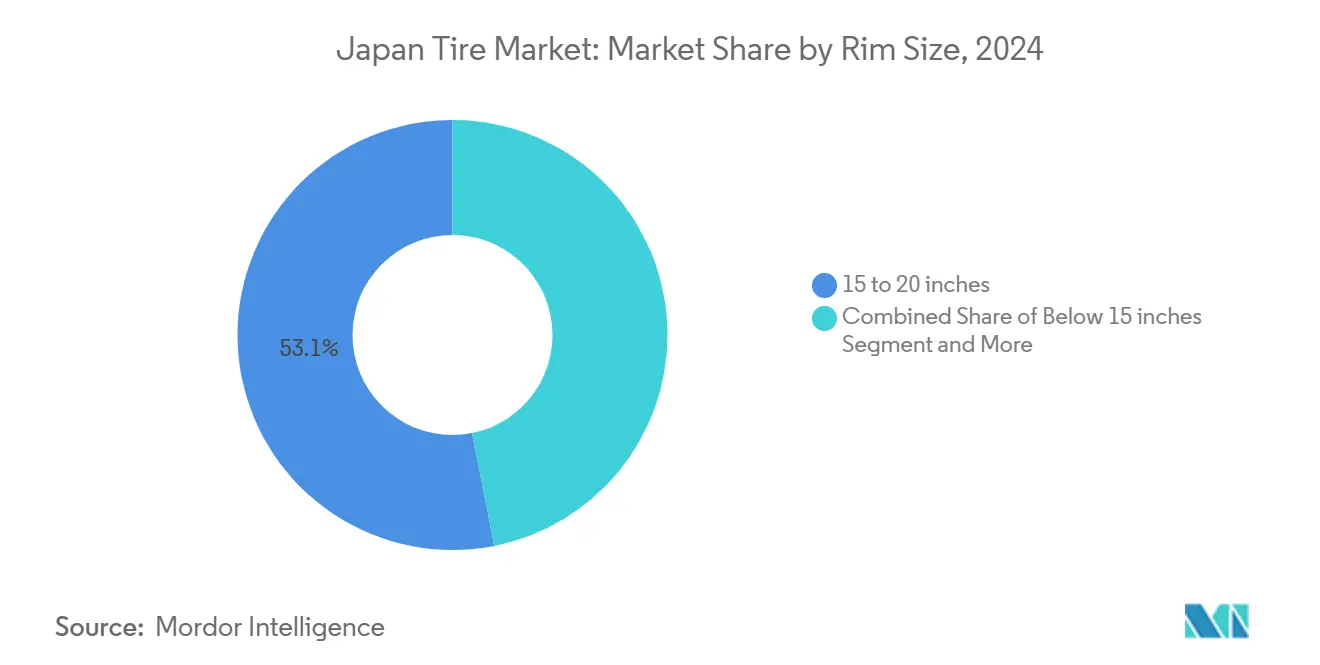

- By rim size, the 15 to 20 inch band accounted for 53.11% of the Japanese tire market size in 2024; sizes above 20 inches are projected to accelerate at a 5.84% CAGR.

- By propulsion, internal-combustion vehicles represented 79.66% of the Japanese tire market size in 2024, yet battery-electric vehicles are projected to surge at a 13.75% CAGR.

Japan Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel-Efficiency and Labelling Mandates | +1.2% | Kanto, Kansai, Chubu | Medium term (2-4 years) |

| Low-Rolling-Resistance Tires | +1.0% | Kanto, Kansai, Aichi | Long term (≥ 4 years) |

| Surge in SUV/CUV Registrations | +0.8% | Kanto, Kansai, Chubu, Kyushu | Short term (≤ 2 years) |

| LCV and HCV Replacement Cycles | +0.6% | Kanto, Kansai, Chubu | Medium term (2-4 years) |

| Digital Fitment Platforms | +0.4% | Kanto, Kansai, Chubu | Short term (≤ 2 years) |

| Smart-Tire Sensor Integration | +0.3% | Aichi, Kanagawa, Shizuoka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Fuel-Efficiency and Labeling Mandates

Japan’s shift to WLTP testing anchors tougher 2030 fleet targets, compelling automakers and fleets to specify A-rated rolling-resistance tires that directly aid compliance. Japan's Ministry of Economy, Trade and Industry (METI) target an average 25.4 km/L (gasoline-equivalent) fuel economy for passenger vehicle fuel economy forces tire makers to refine silica dispersion, tread aerodynamics, and internal construction[1]“Subsidies Upgraded for the Purchase of Clean Energy Vehicles,” Ministry of Economy, Trade and Industry, meti.go.jp . Heavy-duty rules that embed rolling-resistance coefficients into type approval broaden pressure beyond passenger models. As corporate sustainability reporting gains prominence, logistics firms mandate certified low-resistance replacements across mixed fleets, linking fuel savings to emissions disclosures and elevating their share of the Japanese tire market. The cascading effect makes rolling resistance a boardroom issue rather than a service-bay afterthought.

Electrification-Driven Demand for Low-Rolling-Resistance Tires

BEVs currently represent roughly 2% of new registrations, yet already command bespoke compound programs because vehicles weigh up to 50% more than ICE equivalents and deliver torque instantaneously. Bridgestone’s ENLITEN series illustrates how tread stiffness, cavity shape, and pattern noise must converge to satisfy high-weight, low-noise criteria while preserving EU-label A rolling-resistance grades. Subsidies for BEVs accelerate adoption and give tire makers a predictable OE pipeline. Toyota’s commitment to fuel-cell freight vehicles extends these specifications to commercial classes, reinforcing long-term demand for advanced low-resistance designs[2]“Partnerships & Mass Production—Harnessing Scale to Enrich Mobility,” Toyota Motor Corporation, toyota-times.jp. Competitive advantage now hinges on balancing durability with range gains as BEV adoption accelerates.

Surge in SUV/CUV Registrations Expanding Larger-Rim Demand

SUV penetration keeps rising as suburban families favor high-stance vehicles that promise safety and cargo versatility. These vehicles often roll on 19- to 22-inch wheels, which carry premium replacement cost and wider profit margins. Tire makers respond with reinforced bead packages and low-profile carcasses that balance stiffness and comfort. Marketing campaigns highlight reduced road noise and wet-grip gains, ensuring adoption among city drivers. Consequently, larger-rim units outpace total Japan tire market growth.

E-Commerce Logistics Boosting LCV and HCV Replacement Cycles

Last-mile parcel growth raises annual mileage for light vans and small trucks, cutting average replacement intervals below 18 months. Fleet managers require high-mileage compounds and robust casings suited to multiple retreads. Integrated telematics now flag tread wear in real time, guiding predictive maintenance schedules that lock in contracted supply deals. These dynamics create a steady pull for regional distributors serving dense Kanto and Kansai corridors. The Japan tire market benefits from stable commercial volumes even during passenger slowdowns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Studless-Tyre Volume Erosion | -0.8% | Hokkaido, Tohoku, Chubu | Short term (≤ 2 years) |

| Raw-Material Price Swings | -0.6% | Kanto, Kansai, Chubu | Medium term (2-4 years) |

| Aging Vehicle Parc | -0.4% | Chugoku, Shikoku, Kyushu | Long term (≥ 4 years) |

| Slow Adoption of Airless Designs | -0.2% | Kanto, Kansai, Aichi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Warm-Winter Volatility Eroding Studless-Tire Volumes

Climate anomalies are disrupting the predictable October-to-March demand window for studless tires, trimming retailer pre-season orders by up to 25% during mild years. The 2024-2025 season saw severe snowfall only on the Sea-of-Japan coast while Pacific-side cities stayed dry, forcing dealers to discount unsold inventory. Elevated inventory risk compels manufacturers to adopt flexible production scheduling and shared warehousing, but margin pressure remains acute because studless compounds carry higher raw-material costs. Meteorological agencies now offer two-year probabilistic outlooks, yet warm-winter uncertainty still weighs on near-term growth for the Japanese tire market.

Raw-Material Price Swings Squeezing Margins

Natural rubber shortages and petrochemical volatility raise input costs faster than retail price adjustments. Larger producers offset part of the impact through futures hedging and compound substitution, while smaller ones suffer disproportionate profit erosion. Frequent list-price revisions strain distributor relations and can spur short-term volume dips. Over the medium term, R&D in bio-based polymers aims to stabilize margins. Until then, cost pressure tempers overall Japan tire market profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Summer Dominance with All-Season Growth

Summer tires held 56.17% of the Japanese tire market share in 2024, underscoring climatic diversity and consumer commitment to optimized warm-weather grip in the Japanese tire market. Demand concentrates in Kanto and Kansai, where metropolitan motorists pursue low-noise and fuel-saving attributes that align with dense traffic realities, reinforcing premium summer compound uptake. Meanwhile, northern prefectures sustain winter-compound turnover thanks to mandatory usage rules, stabilizing year-end shipment peaks even as climate patterns shift. Manufacturers increasingly leverage voluntary wet-grip labeling to differentiate summer SKUs and justify 5–7% price premiums despite raw-material inflation.

All-season tires, though still niche, are projected to register a 4.61% CAGR to 2030 as dual-income households value the convenience of year-round fitments. Storage constraints in high-rise condominiums bolster this trajectory, and quick-fit retail models reposition all-season lines with predictable profit margins. The urban shift toward smaller households and parking scarcity further elevates penetration, particularly among kei-car owners. Regional promotional campaigns that bundle tire-hotel services with annual inspections also expand the Japan tire market footprint within the all-season segment.

By Tire Design: Radial Technology Supremacy

Radial construction accounted for 97.03% of the Japanese tire market share in 2024, reflecting decades of efficiency, durability, and ride-comfort advantages that underpin OE approvals across light-duty and heavy-duty platforms. Mandatory vehicle inspections every two years reinforce consumer trust in radial safety credentials, locking in consistent replacement frequency for the Japanese tire market. Bias-ply demand survives largely in farming and industrial contexts where initial purchase cost still outweighs mileage concerns. Manufacturers nonetheless sustain small bias lines to preserve market presence and fulfill specialized export orders.

Non-pneumatic airless prototypes are forecast to grow at a 7.64% CAGR from an extremely small base, spurred by autonomous-shuttle pilots at amusement parks and university campuses. Regulatory frameworks now under review could unlock public-road testing before 2028, positioning early movers for first-mover gains if rolling-noise and heat-dissipation hurdles are cleared. Toyo’s spoke-mesh breakthrough yields tenfold durability gains, signaling fast-approaching performance parity. Deployment in last-mile logistics fleets is a mid-term commercial target, promising puncture-free uptime and simplified maintenance that redefine total cost of ownership expectations within the Japan tire market.

By Vehicle Type: Passenger Cars Lead with EV Acceleration

Passenger cars captured 46.98% of the Japanese tire market share in 2024 and are projected to post the fastest 5.13% CAGR, driven by electrification incentives and premium-rim uptake. Aging demographics still favor compact models, but rising disposable income sparks demand for crossover SUVs and imported luxury sedans. BEV penetration, though modest, magnifies performance demands because heavier curb weights require stiffer sidewalls and superior heat management. OE cooperation ensures early lock-in of tailor-made compounds. This synergy cements the segment’s influence on the Japan tire market trajectory.

Light commercial vehicles benefit from e-commerce expansion, raising replacement cycles and creating a stable demand floor. Heavy trucks and buses log steady volume through freight corridors and intercity networks. Two-wheelers serve urban mobility needs, exhibiting seasonal spikes during spring commuting bursts. Specialty off-road vehicles add margin through high-value, low-volume runs, and recent consolidation moves highlight the attractiveness of niche supply. The diversity across vehicle classes, therefore, underpins resilience within the Japanese tire market.

By Application: On-Road Dominance with Off-Road Specialization

On-road fitments contributed 89.88% of the Japanese tire market share in 2024 as cities and expressways define national transportation patterns. Dense traffic accelerates wear, making rotation and replacement services core to retailer profitability. Premium touring lines integrate noise-dampening foam and vibration-eating cap plies that appeal to mid-life households. Regulation enforces strict tread-depth minimums, prompting timely changeovers and sustaining stable volume. Consequently, on-road demand forms the backbone of the Japanese tire market.

Off-road segments expand at a 3.84% CAGR as infrastructure renewal and quarry operations require robust casings and cut-resistant compounds. Government budget allocations for levee upgrades and seismic retrofits keep construction equipment fleets busy. Mining activity on Hokkaido’s coal seams also sparks specialized OTR demand. Suppliers invest in bead-to-shoulder reinforcement and heat-shield tread designs to tackle extreme loads. Though volume is small, unit pricing is multiple times higher, lifting average revenue per tire in the Japanese tire market.

By End User: Aftermarket Leadership with OEM Acceleration

The aftermarket commanded 62.30% of the Japanese tire market share in 2024 since average vehicle ownership exceeds eight years, producing predictable replacement rhythms. Retail chains provide value-added services such as alignment checks and nitrogen inflation, boosting basket size. Tiered pricing lets consumers choose among economy, standard, and premium options, improving inventory turnover. Retread capacity particularly benefits trucking fleets, extending carcass life and easing rubber cost pressure. This long-tail structure delivers stability to the Japanese tire market.

OEM channels rise at a swift 5.24% CAGR as new-vehicle launches center on connected, electrified platforms that demand bespoke compounds. Suppliers secure multiyear contracts by embedding co-engineering teams early in vehicle programs. Technology exclusivity then migrates to the aftermarket when replacement cycles begin, creating halo effects. Automakers also bundle prepaid maintenance plans that lock buyers into dealership tire sales. These practices tighten vertical integration and sustain premium value capture within the Japanese tire market.

By Rim Size: Mid-Range Dominance with Premium Growth

Rim diameters between 15 and 20 inches held 53.11% of the Japanese tire market share in 2024, reflecting mainstream passenger specifications that balance ride comfort and cost. Compact cars and kei models rely on 14- to 16-inch wheels, supporting large-volume SKUs that turn quickly in dealer stock. The segment benefits from economies of scale, keeping the average selling price moderate. Retailers advertise bundled seasonal sets to push volume. Mid-range rims will therefore remain central to the Japan tire market size discussion.

Diameters above 20 inches grow at a 5.84% CAGR as luxury SUVs and sports sedans crave aesthetic stance and sharp handling. Low-profile 22-inch tires cost two to three times standard sizes, expanding revenue disproportionally. Manufacturers reinforce bead fillers and longitudinal belts to curb flex and heat build-up. Marketing highlights quietness and hydroplaning resistance to justify premiums. Upsizing thus drives margin expansion in the Japanese tire market.

By Propulsion: ICE Dominance with BEV Transformation

Internal-combustion vehicles retained 79.66% of the Japanese tire market share in 2024, but hybrid and battery-electric adoption accelerates as incentives and charging infrastructure scale. ICE fitments remain volume bedrock for distributors, offering proven tread patterns and predictable wear. Yet BEV-optimized lines show 13.75% CAGR, aided by low-resistance rubber, aerodynamically trimmed sidewalls, and foam-based acoustic insulation. Hybrids blend both needs, demanding durability under regenerative braking and silent cabin standards. This propulsion mix reshapes product roadmaps in the Japanese tire market.

Fuel-cell vehicles, still niche, demand similar low-resistance traits and have hydrogen-specific cooling challenges that affect tread design. As commercialization widens, suppliers will leverage BEV learning to speed FCEV compound iterations. Over time, electrified platforms foster higher service frequency because torque-led wear shortens life cycles. This mechanical reality counterbalances any unit-volume shifts. The propulsion pivot, therefore, sustains overall value in the Japanese tire market.

Geography Analysis

Kanto dominates the Japanese tire market size in 2024, through Tokyo’s dense car park, affluent households, and extensive delivery fleets. Urban commuting accelerates tread wear, so owners replace tires sooner to maintain ride quality and fuel economy. Premium 19- to 22-inch sizes post double-digit growth as crossovers proliferate in suburbs. Digital fitment apps enjoy high adoption, enabling same-day installations that deepen loyalty. Kansai follows with strong industrial freight flows linked to Osaka and Kobe ports, boosting light commercial and heavy truck turnover despite shorter average rim diameters. Seasonal switching remains common, sustaining dedicated storage programs that lock in customers. Together, these two regions anchor revenue for the Japanese tire market and set benchmark pricing that echoes nationwide.

Chubu’s profile centers on Aichi’s automotive cluster, where OE fitment demand spikes during new-model ramp-ups. Local logistics providers support just-in-time assembly lines, creating rapid response expectations for tire suppliers. Replacement volumes also rise because factory workers often commute long distances by car. Meanwhile, Hokkaido and Tohoku exhibit the highest winter-compound penetration as legal requirements and heavy snowfall dictate studless adoption. Warm-winter variability, however, introduces uncertainty that challenges distributor stocking strategies. Retailers mitigate risk by partnering with national chains for inventory balancing, ensuring timely restock when snow episodes occur. These northern markets command higher unit prices because premium studless compounds dominate, contributing healthy margins to the Japan tire market even with uneven volume swings.

Southern prefectures Kyushu, Shikoku, and Okinawa experience milder climates that favor high-silica summer compounds. Additionally, its semiconductor and battery factories drive logistics volumes, expanding demand for durable commercial casings and retread services. Coastal ferry links and modal-shift policies lengthen service intervals for trucks, yet require enhanced heat-resistant tread to handle tropical asphalt. Rural areas, however, house older vehicles, keeping economy lines relevant and limiting upscale traction. Government disaster-resilience budgets for levee and bridge reinforcement support off-road tire demand across the archipelago’s construction sites. Mountainous regions in Shikoku also encourage specialty light-truck fitments with reinforced sidewalls for narrow, winding roads. These diverse conditions together create a mosaic of needs, ensuring the Japan tire market remains geographically balanced despite population shifts.

Competitive Landscape

The Japanese tire market features a concentrated structure. Bridgestone leverages global R&D scale, localized compound tuning, and a B-Select retail network. The chain provides alignment, sensor calibration, and subscription-based rotation packages, cementing customer stickiness. Yokohama accelerates product cycles for SUV and performance ranges while integrating its recent off-road acquisition to gain share in high-margin mining segments. Sumitomo focuses on simulation-driven design to cut time-to-market; its 1% prediction-error noise model allows fewer prototypes and lower development cost. Mid-tier players carve niches in economy lines or motorsport slicks, serving price-sensitive buyers and enthusiast circles.

Strategic alliances widen. Automakers lock in co-development deals that ensure WLTP compliance and EV range optimization. Suppliers exchange compound data early to secure exclusive OE positions, which later translate into aftermarket pull-through. Vertical integration trends continue as tire makers bundle leasing, telematics, and predictive maintenance, turning products into mobility solutions. Smaller disruptors exploit online marketplaces, offering door-to-door installation through gig-economy technicians. Incumbents counter by adding click-and-collect and mobile vans. These competitive motions enrich choice but also intensify price transparency in the Japan tire market.

Technology differentiation remains crucial. Hydrogen-powered curing lines shrink carbon footprints, and bio-sourced feedstocks test viability at pilot scale. Sensor embeddings progress from Bluetooth patches to embedded chips linked with vehicle CAN buses. Over-the-air firmware updates will refine pressure algorithms, creating post-sale revenue. Non-pneumatic progress promises puncture-free resilience that rides smoother each prototype cycle. Collectively, the sector walks a fine line between incremental refinement and disruptive leap, ensuring the Japan tire market stays a global innovation hub.

Japan Tire Industry Leaders

Bridgestone Corporation

Yokohama Rubber Co., Ltd.

Sumitomo Rubber Industries

Toyo Tire Corporation

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Yokohama Rubber began supplying BluEarth AE-01 tyres as OE for Honda’s N-ONE e: mini-EV launching in September.

- August 2025: Toyo Tire rolled out new Observe W/TR SUV studless sizes across domestic dealerships, targeting strong snowfall regions for the 2025-2026 season.

- May 2025: Sumitomo Rubber activated continuous green-hydrogen production at its Shirakawa plant, enabling 24/7 electrolyzer operations that lower CO2 emissions in tire manufacturing.

- February 2025: Yokohama Rubber completed the USD 905 million purchase of Goodyear’s off-the-road business, expanding mining and construction coverage.

Japan Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 to 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 to 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

What is the forecast value of the Japan tire market by 2030?

The Japan tire market is expected to reach USD 9.94 billion by 2030.

Which rim-size segment is growing the quickest?

Fitments above 20 inches show the fastest growth at a 5.84% CAGR due to SUV and premium-vehicle demand.

How fast are battery-electric vehicle tires growing?

BEV-specific tires are forecast to expand at a 13.75% CAGR through 2030, far outpacing other propulsion categories.

Why are all-season tires gaining popularity?

Urban consumers value the convenience of avoiding seasonal changeovers, and high-rise storage constraints favor year-round fitments.

What key restraint threatens studless-tire sales?

Warm-winter volatility is reducing predictable demand, especially in regions where snowfall patterns have become less severe.

Page last updated on: