Italy Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.54 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Chemical Warehousing Market Analysis by Mordor Intelligence

The Italy Chemical Warehousing Market size is expected to increase from USD 1.54 billion in 2025 to USD 1.65 billion in 2026 and reach USD 2.01 billion by 2031, growing at a CAGR of 4.08% over 2026-2031.

The growth outlook reflects Italy’s role as Europe’s third-largest chemical producer and the deep concentration of sites and jobs across Lombardy, Piedmont, Veneto, and Emilia-Romagna, where 77% of chemical employment is located. Structural specialization in fine and specialty chemicals, which represent 55% of Italy’s chemical output versus the European Union average of 37%, shapes demand for temperature-controlled and hazard-certified storage for high-value intermediates. Export-led pharmaceuticals add to the need for GMP-compliant and secure warehousing, since 90% of Italian pharmaceutical production is exported, and the country is ranked among the world’s top pharmaceutical exporters. Port investments in Genoa and Livorno, together with rail-linked capacity in Trieste, are improving sea-rail connectivity and supporting distributors with shorter lead times and lower landed costs across the Italy chemical warehousing market.

Key Report Takeaways

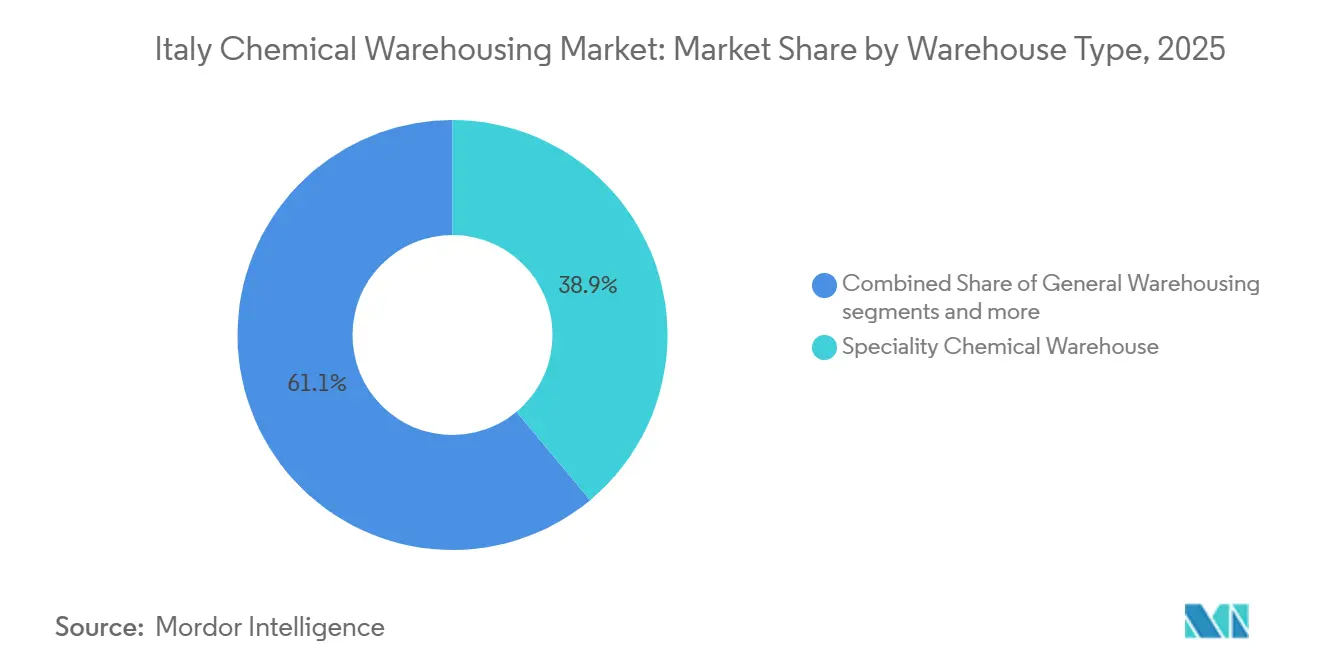

- By warehouse type, specialty chemical warehouses held 38.94% of Italy chemical warehousing market share in 2025, while temperature-controlled chemical warehouses are expanding at a 5.64% CAGR through 2031.

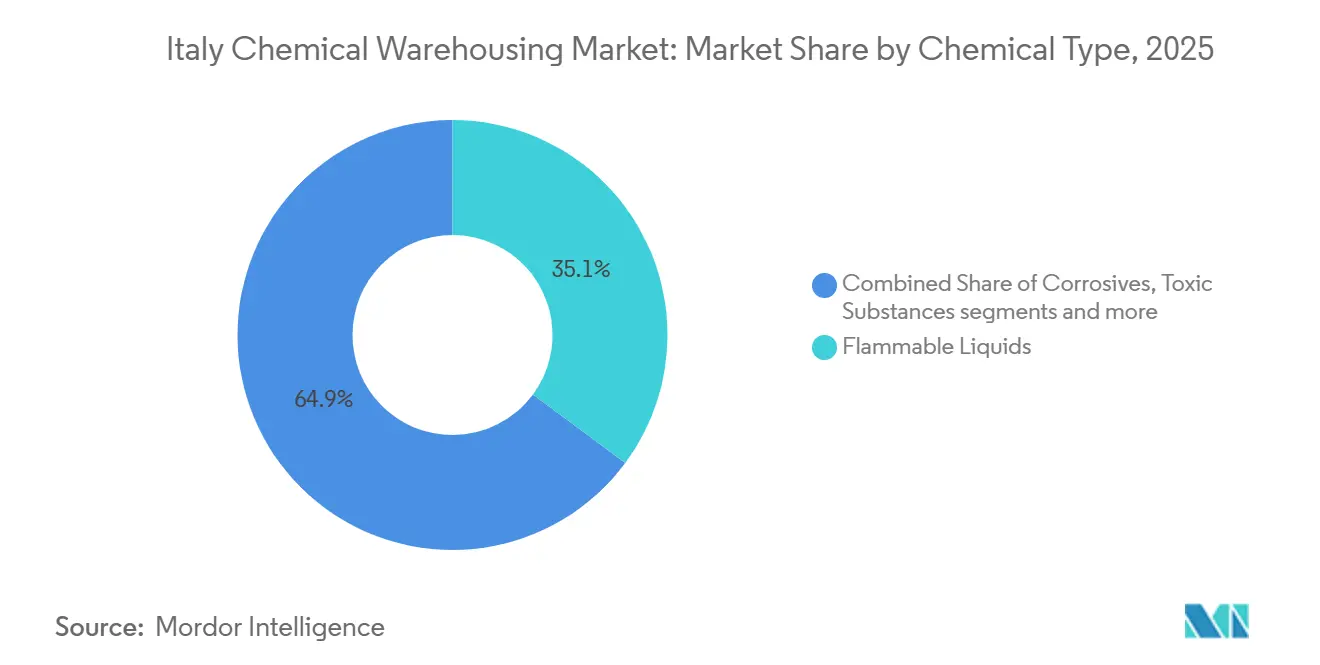

- By chemical type, flammable liquids captured 35.14% of Italy chemical warehousing market size in 2025; toxic substances are expanding at a 6.47% CAGR through 2031.

- By end-user industry, specialty chemicals manufacturing accounted for a 32.12% of Italy chemical warehousing market share in 2025, whereas pharmaceuticals & life sciences are advancing at a 6.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy participates in a competitive field that extends beyond its own borders. The market landscape in the global chemical warehousing industry outlined by Mordor Intelligence covers that wider structure.

Italy Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical and Fine Chemicals Leadership | + 1.3% | Northern Italy, export corridors via Ligurian and Tyrrhenian ports | Long term (≥ 4 years) |

| Strategic Mediterranean Trade Position | + 0.9% | Genoa, Livorno, Trieste, Ravenna, with inland spill-over | Medium term (2-4 years) |

| Specialty Chemicals Sector Growth | + 1.1% | Europe, particularly Northern Italy industrial clusters | Long term (≥ 4 years) |

| Northern Industrial Triangle Development | + 0.7% | Lombardy, Piedmont, Veneto, Emilia-Romagna | Medium term (2-4 years) |

| Agrochemical Manufacturing Base | + 0.4% | National, with early gains in Po Valley | Short term (≤ 2 years) |

| Green Transition and Bio-Based Chemicals | + 0.9% | Sicily, Veneto, Pavia, and circular economy hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical and Fine Chemicals Leadership

Export-led pharmaceuticals and Italy’s specialization in fine and specialty chemicals continue to propel high-spec storage, including temperature-controlled and GMP-compliant areas that meet serialization and product integrity requirements in the Italy chemical warehousing market. In 2025, the pharmaceutical sector’s 90% export orientation supported recurring demand for validated storage, customs-bonded zones, and quality-controlled staging aligned with global shipping lanes. CDMO capacity in Italy added higher-frequency product launches and small-batch complexity, requiring warehouses to add traceability, monitoring, and specialized handling for APIs and sensitive intermediates in the Italy chemical warehousing market. Third-party logistics providers are capitalizing on Lombardy's life sciences and chemical hubs by setting up dedicated pharma-grade operations near key research and manufacturing sites. The combined weight of pharma exports and fine chemicals strengthens demand visibility for premium storage across northern clusters in the Italy chemical warehousing market.[1]Farmindustria, “Indicatori Farmaceutici 2025,” Farmindustria, farmindustria.it

Strategic Mediterranean Trade Position

Port-led capacity additions reinforce Italy’s import and transshipment role for chemicals and intermediates flowing between the Middle East, Europe, and North America in the Italy chemical warehousing market. Genoa’s New Breakwater project is sized to accommodate ultra-large container vessels and increase throughput, with an investment of EUR 1.3 billion (USD 1.43 billion), supporting larger call sizes and scale economies from vessel upsizing. The import footprint ties into feedstock realities, given that a material share of Italy’s chemical inputs are naphtha-based and linked to Middle Eastern supply chains, which underpins consistent inbound demand for port-area storage and drayage in the Italy chemical warehousing market. Livorno’s Darsena Europa expansion, financed by the European Investment Bank at EUR 90 million (USD 99 million), provides additional container capacity and logistics optionality for specialty producers in Tuscany and central Italy. Trieste’s rail-linked infrastructure, co-financed through European programs, aligns Adriatic flows with Central and Eastern European corridors, creating cross-border distribution opportunities for chemical warehousing in the Italy chemical warehousing market.

Specialty Chemicals Sector Growth

Italy’s chemical output is skewed toward fine and specialty segments, with specialty and consumer chemicals accounting for 55% of production value, ahead of the European Union average of 37%, which changes the mix and standards of storage in the Italy chemical warehousing market. Companies active in waterborne coatings, additives, and bio-based intermediates require segregated storage with contamination controls and documentation-heavy workflows that reflect quality management norms such as ISO 9001. Regional champions like ERCA in specialty auxiliaries highlight the breadth of formulations that move through multi-compartment, hazard-segregated facilities in the Italy chemical warehousing market. Proximity to research centers in northern Italy sustains a cadence of product refresh and tailored batches that are better served by specialized operators that can balance compliance, throughput, and responsiveness. The shift in product mix, therefore, skews storage toward premium, adaptable, and traceable capacity in the Italy chemical warehousing market.

Northern Industrial Triangle Development

The historic concentration of chemical employment and production in Lombardy, Piedmont, Veneto, and Emilia-Romagna sustains demand visibility and scale for third-party logistics investments in the Italy chemical warehousing market. Lombardy’s leadership within this industrial triangle benefits providers that add purpose-built hazardous goods capacity close to chemical parks and downstream converters. TALKE’s hazardous-goods warehouse inaugurated in May 2025 at Filago in the Covestro Chemical Park exemplifies the specialization push in Lombardy, with Seveso permitting preparations signaling long-term deployment for the regional cluster in the Italy chemical warehousing market. Eni’s Versalis projects across the north, such as the recycled polystyrene plant at Porto Marghera, add new flows of circular materials that need dedicated storage and blending near production sites. The overall effect is to reinforce hub-and-spoke distribution anchored in the northern industrial triangle for the Italy chemical warehousing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bureaucratic Complexity and Permitting Delays | - 0.6% | National, acute in Southern regions and greenfield projects | Medium term (2-4 years) |

| Fragmented Logistics Network | - 0.5% | National, concentration gaps outside major hubs | Long term (≥ 4 years) |

| High Labor and Compliance Costs | - 0.7% | National, with premiums in the north | Short term (≤ 2 years) |

| Limited Greenfield Land Availability | - 0.4% | Lombardy, Piedmont, Veneto | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bureaucratic Complexity and Permitting Delays

Permitting timelines for hazardous goods facilities remain lengthy because operators must satisfy multi-agency reviews and external emergency planning requirements under SEVESO III in the Italy chemical warehousing market. The 2026 deadline for upper-tier Seveso establishments to update safety reports adds pressure on internal resources, prioritizing compliance over expansion in the near term. Warehouses that handle flammable, corrosive, or toxic substances must account for risk scenarios and external event modeling, which complicates approvals and inspections in the Italy chemical warehousing market. These obligations can stretch project critical paths, especially for greenfield builds that also need land-use variances and municipal alignment. As a result, brownfield conversions and capacity expansions at existing sites are often favored to maintain momentum in the Italy chemical warehousing market.[2]ISPRA, “The Seveso Directive and Emerging Risks from the Energy Transition,” ISPRA, isprambiente.gov.it

High Labor and Compliance Costs

Operating costs reflect higher energy, labor, and compliance outlays that weigh on margins, especially for temperature-controlled and hazard-segregated facilities in the Italy chemical warehousing market. Annual costs from the EU Emissions Trading System weigh heavily on chemical value chains and their associated logistics. While current burdens hover in the hundreds of millions of euros, projections indicate a significant uptick by 2030, coinciding with a reduction in free allowances. This translates to an immediate impact of approximately USD 660 million, with a potential trajectory leading to USD 1.65 billion. Electricity prices remained elevated, with Italian wholesale prices of EUR 120 (USD 132) per megawatt-hour in 2025, compared with EUR 60 (USD 66) in Spain and France, amplifying refrigeration and HVAC costs in the Italy chemical warehousing market. Compliance with SEVESO III and CLP reviews also requires skilled safety and quality staff, which adds to payroll pressure in core hubs. These inputs make automation and energy-efficiency retrofits strategic priorities across the Italy chemical warehousing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Specialty Segments Driven by GMP and Hazmat Mandates

Specialty chemical warehouses held the largest share of 38.94% of the warehouse type in 2025, reflecting Italy’s concentration in fine and specialty chemicals and the need for segregated, quality-assured storage in the Italy chemical warehousing market. Temperature-controlled facilities show the fastest expansion with 5.64% CAGR as pharma-related volumes require 2 to 8 degrees Celsius stability, validated storage zones, and audit trails to support export flows and clinical-to-commercial transitions in the Italian chemical warehousing market. Operators differentiate with dedicated Dangerous Goods management, documentation control, and product integrity assurance for small-batch, high-value shipments typical of biotech and advanced therapies. These requirements align with northern clusters where life sciences and specialty chemical producers scale production and export cycles. The Italy chemical warehousing market continues to reward sites that can combine GMP standards, risk controls for hazardous goods, and responsive service levels to manage frequent product refresh and short-lifecycle inventories.[3]European Chemical Industry Council, “Italy,” Cefic, cefic.org

Hazardous materials warehouses are pivotal for flammable, corrosive, toxic, and oxidizing substances, and regulatory regimes reinforce their demand, and circular economy flows in the Italy chemical warehousing market. In May 2025, TALKE opened a 20,000 square meter hazardous goods site at Filago within the Covestro Chemical Park, with preparations for Seveso permits and future tank and silo capacity, which underlines the long-term buildout of certified hazardous storage in Lombardy. The pivot to circular polymers and chemical recycling adds inbound and intermediate flows that require separation, traceability, and quality-control steps near refinery and polymer sites in the Italy chemical warehousing market. General-purpose warehousing remains relevant for packaged auxiliaries and consumer chemicals, although competition for logistics real estate encourages brownfield redevelopment close to major corridors. The Italy chemical warehousing industry, therefore, balances premium, compliance-heavy capacity with flexible general storage to serve a changing product portfolio.

By Chemical Type: Flammable Liquids Anchor Demand

Flammable liquids dominated the Italy chemical warehousing market, capturing a 35.14% share in 2025. This category encompasses storage capacities, solvent management, petroleum distillates, and monomers, all closely linked to prevailing feedstock patterns. Portfolio shifts at large value-chain players reinforce this pattern as sites invest in circular and bio-based outputs that also require dedicated flammable-liquid handling, tank segregation, and safety systems at or near production complexes. In the Italy chemical warehousing market, toxic substances are set to experience the most rapid growth, with a projected CAGR of 6.47% through 2031. The heightened demand for stringent containment drives this surge, validated environmental controls, and bolstered security protocols for pharmaceutical active ingredients and select agro-ingredients. Corrosives show steady movement linked to specialty intermediates for coatings, performance additives, and industrial cleaning solutions that need corrosion-proof containment and spill-management infrastructure. Oxidizers and other regulated materials, while smaller in volume, require strict segregation and documentation that favors certified third-party providers in the Italian chemical warehousing market.

Circular economy inputs and outputs create additional storage demand for secondary raw materials, pyrolysis oils, and recycled polymers around industrial hubs such as Porto Marghera and the Sicilian cluster, where Eni’s Versalis has commissioned and planned facilities that will reshape flows by 2028 in the Italy chemical warehousing market. These materials need documentation and quality-management practices that trace recycled content and feedstock origin, consistent with European circular goals. The mix of chemicals in transit suggests continued growth for adaptable warehousing that can switch between hazardous classes while maintaining compliance in the Italy chemical warehousing market. Facilities that align tank farms, packaged storage, and intermediate blending under one quality system will maintain an advantage as portfolio complexity increases. This composition of demand keeps the Italian chemical warehousing industry focused on capability breadth, audit readiness, and proximity to port and refinery assets.

By End-user Industry: Pharma-Life Sciences Premium Overshadows Mature Segments

Specialty chemicals manufacturing was the largest end-user industry, accounting for 32.12% market share, and reflecting Italy’s emphasis on fine and specialty categories, which need clean, segregated, and quality-managed storage in the Italy chemical warehousing market. Producers of dispersions, auxiliaries, and additives run frequent product rotations, lower lot sizes, and tighter contamination controls, all of which favor third-party logistics providers with specialized dangerous goods and quality management capabilities near northern clusters. Pharmaceuticals and life sciences are the fastest-growing end-user, accounting for 6.87% CAGR through 2031, owing to an export-heavy posture, a sizable CDMO base, and product types that require rigorous chain-of-custody and temperature management in the Italy chemical warehousing market. The sector’s continuous upgrades to packaging, serialization, and product integrity are pulling more value-added services into warehousing operations co-located with transport nodes and regulatory agencies. This is shifting the Italy chemical warehousing industry toward pharma-grade infrastructure that can pivot to biotech and advanced therapies.

Downstream portfolios in paints, coatings, and adhesives also sustain steady activity as consumer and industrial demand evolves, though these segments lean on established storage and handling standards in the Italy chemical warehousing market. Oil and gas-linked intermediates are gradually declining as large players phase down exposure to basic chemicals and reallocate capital to biorefining and circular products in Italy, which redirects warehousing to emerging supply chains and new compliance regimes. Food and feed additives maintain durable flows that often move alongside specialty portfolios under similar quality systems, helping stabilize base utilization in core hubs in the Italy chemical warehousing market. The net effect is a two-speed profile, where pharma and bio-based segments expand faster while mature categories anchor baseline storage requirements in the Italy chemical warehousing market.

Geography Analysis

Northern Italy continues to concentrate chemical activity with 77% of sector employment in Lombardy, Piedmont, Veneto, and Emilia-Romagna, which sustains the largest installed base of specialized warehousing capacity in the Italy chemical warehousing market. Lombardy’s role as the country’s leading life sciences and chemical region directs high-spec warehousing to sites that integrate dangerous goods handling with pharma-grade quality systems in the Italy chemical warehousing market. New hazardous goods capacity at Filago, within an established chemical park, reflects a broader pattern of brownfield and adjacent investments designed to stay close to producers and technical talent pools. The Italy chemical warehousing market also benefits from proximity to Versalis sites in Mantua, Ferrara, and Ravenna, which reinforces regional flows of both basic and circular chemicals that require certified storage and handling.

Port geographies are strategic nodes for inbound feedstocks, intermediates, and finished chemicals, as infrastructure upgrades in Genoa and Livorno expand options for ocean-imported cargoes in the Italy chemical warehousing market. Genoa’s New Breakwater, with EUR 1.3 billion (USD 1.43 billion) in investment, is designed to receive bigger vessels and higher call sizes, which reduces unit logistics costs and supports higher-capacity storage models near the port. Livorno’s Darsena Europa container terminal, supported by EUR 90 million (USD 99 million) in financing, provides alternative routing for central Italian manufacturers, including specialty chemical producers, while improving berth productivity and hinterland connectivity. In the northeast, Trieste’s rail-linked developments align the Adriatic with Central Europe, creating warehouse opportunities for cross-border consolidation and modal shift in the Italy chemical warehousing market.

Sicily and Veneto are increasingly important for circular and bio-based supply chains built around Versalis investments, including the recycled polystyrene facility in Porto Marghera and the planned biorefinery and chemical recycling plant in Priolo, scheduled to be completed by 2028 in the Italy chemical warehousing market. These projects redirect flows toward secondary raw materials and bio-intermediates that require storage systems with robust traceability, documentation, and quality testing. Southern regions also present opportunities for last-mile distribution and blending, as demonstrated by Brenntag’s acquisition of a chemical logistics site in Bari that expands access to Adriatic corridors in the Italy chemical warehousing market. Differences in permitting capacity and infrastructure depth persist across regions, which reinforces the strategic advantage of port-adjacent zones and mature industrial clusters in the Italy chemical warehousing market.

Mordor Intelligence provides coverage of the chemical warehousing market across other key regional markets, including Europe, Middle East, and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to France, United Kingdom, South Korea, Germany, Canada, and Mexico incorporating local coverage and market participation, as required.

Competitive Landscape

The market remains fragmented overall, although high-compliance and specialty storage segments are increasingly concentrated among certified operators serving industrial clusters. Operators differentiate through SQAS for chemical logistics, ISO 9001 and ISO 45001 for quality and safety, and pharma-grade authorizations where applicable, which align with the product mix in fine chemicals and life sciences. Hazard-segregated capabilities and digital monitoring are baseline expectations for large customers, especially those integrating temperature control and serialized product flows in the Italy chemical warehousing market. As a result, established players continue to invest in sites near northern clusters and key ports to ensure quick access, compliant handling, and reliable throughput in the Italy chemical warehousing market.

Recent strategic moves underscore capability expansion and geographic reach. TALKE opened a 20,000 square meter hazardous goods warehouse in Filago in May 2025, within Covestro Chemical Park, with Seveso permitting preparations underway and additional land reserved for tank and silo expansion in the Italy chemical warehousing market. On the producer side, Eni’s Versalis circular polymer platform in Porto Marghera and planned biorefinery and chemical recycling facilities in Priolo are creating new storage requirements for recycled and bio-based materials and co-products, with timelines through 2028 in the Italy chemical warehousing market.

Pharmaceutical and life sciences customers are adding specialized demand, including GMP-compliant zones, validated temperature control, and audit-ready documentation standards in the Italy chemical warehousing market. Manufacturers such as Chiesi are investing in new and upgraded production sites in northern Italy, which consolidates the need for nearby storage that can manage sterile product handling and sustainability commitments. CDMO expansions, such as Adare Pharma Solutions’ upgraded facility in Pessano with new packaging and warehousing capacity, highlight the blurring lines between manufacturing services and distribution readiness in the Italy chemical warehousing market. These moves point to a competitive field where certifications, circular readiness, and pharma-grade capabilities shape customer preferences in the Italy chemical warehousing market.

Italy Chemical Warehousing Industry Leaders

DHL Group

Talke Logistics

Den Hartogh Logistics

Corsini Srl

Chemical Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TALKE Logistics inaugurated a 20,000 square meter hazardous goods warehouse in Filago, Bergamo, within the Covestro Chemical Park, with storage capacity for 20,000 pallets across a total area of 30,000 square meters, including two 5,000 square meter compartments with modern sprinkler systems, preparations for SEVESO permits, and land reserved for future tanks and silos.

- March 2025: Chiesi Group announced a EUR 430 million (USD 473 million) investment, to acquire and revitalize a 124,000 square meter industrial area in Nerviano, Milan, to create a center of excellence for sterile biologicals and inhalers with on-site laboratories and a photovoltaic park targeting energy self-sufficiency by 2029.

- March 2025: Versalis, an Eni company, inaugurated a recycled polymer plant in Porto Marghera, Venice, with capacity up to 20,000 tonnes per year of r-GPPS and r-EPS within the Versalis Revive product range, supporting efficient logistics with nearby Versalis facilities in Mantua, Ferrara, and Ravenna.

Italy Chemical Warehousing Market Report Scope

The Italy Chemical Warehousing Market Report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, Hazardous Materials (HAZMAT) Warehouses, Temperature-Controlled Chemical Warehouses), by Chemical Type (Flammable Liquids, Corrosives, Toxic Substances, Oxidizers, Others), and by End-user Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, Paints, Coatings & Adhesives, Food & Feed Additives, Oil & Gas / Petrochemicals, Others). The Market Forecasts are Provided in Terms of Value (USD Billion).

| General Warehousing |

| Specialty Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals & Life Sciences |

| Agrochemicals |

| Paints, Coatings & Adhesives |

| Food & Feed Additives |

| Oil & Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Specialty Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals & Life Sciences | |

| Agrochemicals | |

| Paints, Coatings & Adhesives | |

| Food & Feed Additives | |

| Oil & Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the current size and growth outlook for the Italy chemical warehousing market?

The Italy chemical warehousing market size was USD 1.54 billion in 2025 and is expected to reach USD 2.01 billion by 2031, reflecting a 4.08% CAGR from 2026 to 2031.

Which end-users are driving the fastest growth in Italy’s chemical warehousing?

Pharmaceuticals and life sciences are the fastest-growing users due to export intensity and CDMO activity, which require GMP-compliant, temperature-controlled, and audit-ready storage.

Where is warehousing demand most concentrated within Italy?

Demand is concentrated in the northern industrial core of Lombardy, Piedmont, Veneto, and Emilia-Romagna, supported by port-adjacent infrastructure at Genoa, Livorno, and Trieste.

What trends are shaping facility specifications across the Italy chemical warehousing market?

A higher share of specialty and fine chemicals, export-led pharma volumes, and circular polymers are pushing demand for temperature control, hazard segregation, traceability, and proximity to ports and clusters.

How are port investments influencing chemical warehousing in Italy?

Genoa’s New Breakwater and Livorno’s Darsena Europa expansion are improving call sizes and routing options, which support larger-volume storage, faster customs processing, and better hinterland distribution.

Which compliance regimes are most relevant to operators in Italy?

Key regimes include SEVESO III requirements, REACH and CLP obligations, SQAS for chemical logistics, ISO 9001 and ISO 45001, and AIFA-related GMP oversight for pharma-linked storage.

Page last updated on: