Italy Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

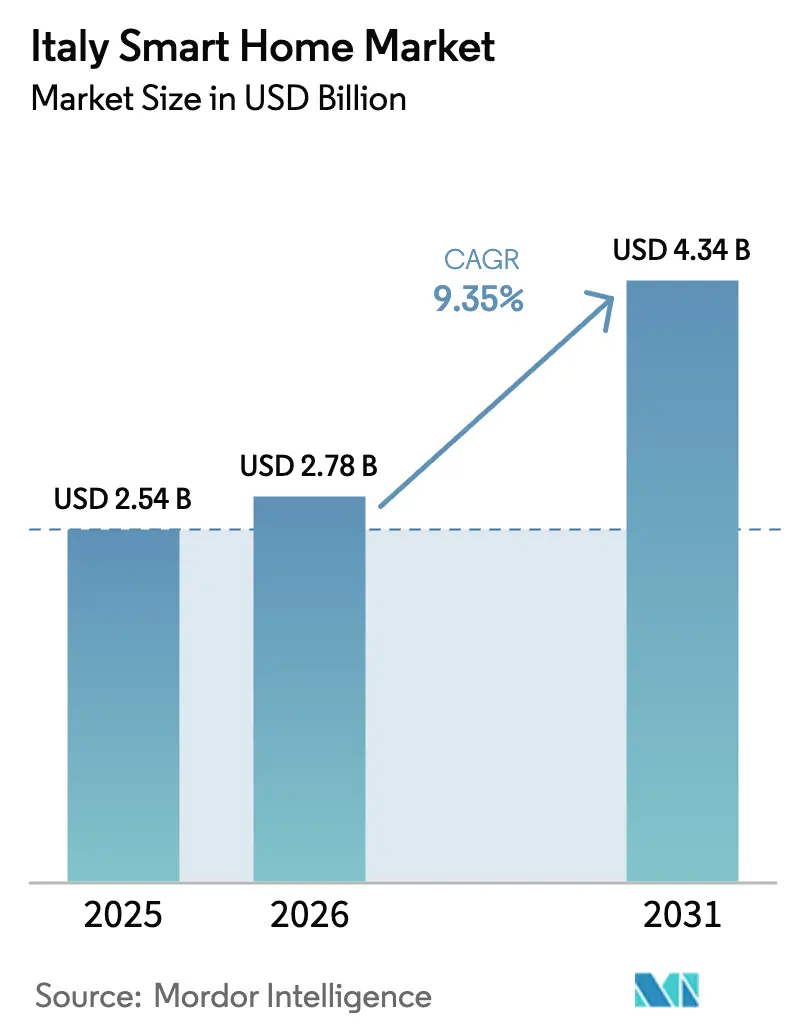

| Base Year Market Size (2025) | USD 2.54 Billion |

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 4.34 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

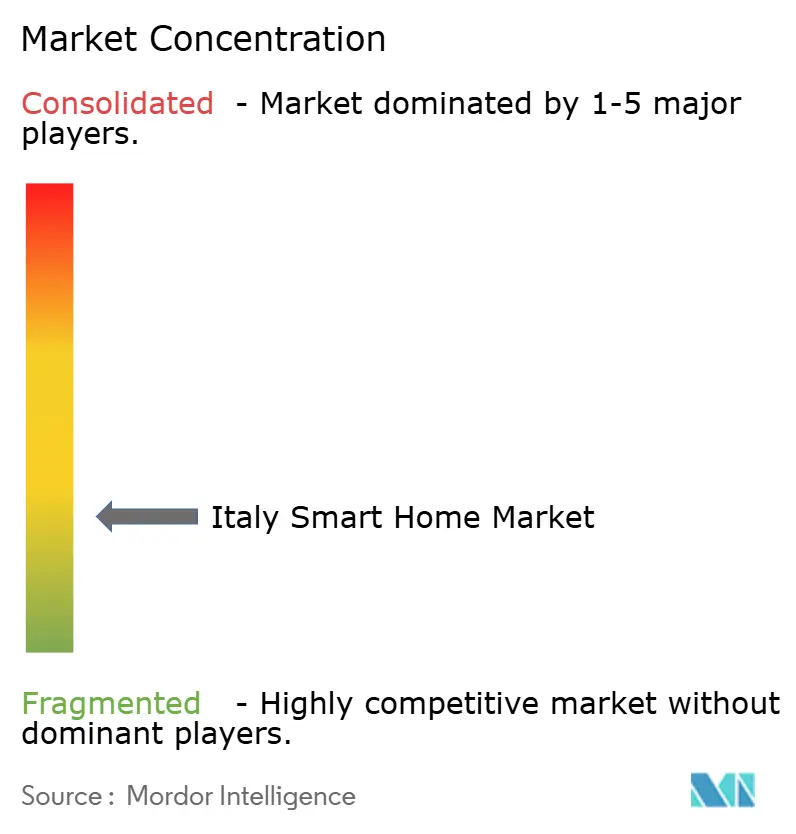

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Smart Home Market Analysis by Mordor Intelligence

Italy Smart Home Market size in 2026 is estimated at USD 2.78 billion, growing from 2025 value of USD 2.54 billion with 2031 projections showing USD 4.34 billion, growing at 9.35% CAGR over 2026-2031. This rapid expansion reflects the country’s accelerated digital transition, generous fiscal incentives, and rising consumer focus on energy savings. Government schemes such as the Ecobonus and Bonus elettrodomestici are spurring demand by trimming pay-back periods for connected devices and energy-efficient appliances. Consolidation among suppliers amplifies scale efficiencies, with BTicino (Legrand Group) alone holding 64% of the residential segment and using its 11 domestic plants to shorten time-to-market. A concurrent leap in datacenter investment, 5G coverage, and renewable energy communities is widening the addressable base for intelligent energy management, security, and home-health applications. At the same time, the aging housing stock ensures a large retrofit opportunity, while updated building codes nudge developers to pre-install open-protocol wiring in new residences.

Key Report Takeaways

- By product category, smart appliances led with 34.62% revenue share in 2025; energy management is forecast to expand at a 12.96% CAGR to 2031.

- By installation type, retrofit systems held 62.05% of the Italy smart home market share in 2025, while new-build integration is advancing at a 14.75% CAGR through 2031.

- By connectivity, Wi-Fi accounted for 58.75% share of the Italy smart home market size in 2025 and Thread/Matter protocols are projected to grow at an 17.2% CAGR during 2026-2031.

- By housing type, apartments captured 49.85% share in 2025, whereas detached houses are set to record a 12.55% CAGR to 2031.

- By distribution channel, retail & e-commerce dominated with 52.35% share in 2025; telecom-utility bundles exhibit the fastest growth at 15.45% CAGR through 2031.

- By region, North-West Italy led with 28.55% share in 2025; the Islands region is forecast to grow at a 12.05% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency & sustainability focus | +6.2% | Global, strongest in North-West and Central regions | Medium term (2-4 years) |

| Government incentives (Ecobonus/Superbonus 110%) | +5.5% | National, higher uptake in high-income regions | Short term (≤ 2 years) |

| Enhanced home security demand | +4.8% | National, premium adoption in North-West | Short term (≤ 2 years) |

| AI-IoT-5G convergence | +4.1% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Aging population & ambient assisted living (AAL) | +3.2% | National, concentrated in rural and suburban areas | Long term (≥ 4 years) |

| Smart-grid tariff pilots (Enel, etc.) | +2.8% | Pilot regions expanding nationally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency & Sustainability Focus

Italy tightened building codes in 2025 and kept a 50% tax deduction for energy-saving upgrades, prompting households to pair smart thermostats with heat pumps and photovoltaic systems. Renewable energy communities in regions such as Veneto already achieve 92% self-sufficiency, motivating residents elsewhere to install energy dashboards that optimize self-consumption. Utilities like Enel back the movement by deploying 45.4 million smart meters that share granular load data with residential hubs. These meters, built on the Meters & More protocol, enable automated tariff switching and remote diagnostics. As consumers see annual savings approaching EUR 900 in larger prosumer setups, the Italy smart home market gains an enduring economic pull.[1]MDPI, “Quantifying the Economic Advantages of Energy Management Systems for Domestic Prosumers with Electric Vehicles,” mdpi.com

Government Incentives (Ecobonus/Superbonus 110%)

The Ecobonus continues to reimburse up to 50% of eligible renovation costs, reducing payback periods for connected lighting, HVAC, and blinds. Although the generous Superbonus has begun tapering, its legacy remains visible: 500,000 energy retrofits completed by May 2024 embedded smart sensors and battery storage in existing dwellings. Incoming income caps push middle-income families toward targeted rebates such as the Bonus elettrodomestici’s EUR 200 point-of-sale discount on efficient appliances. Together, these schemes widen the funnel for plug-and-play devices while sustaining installer workloads. Developers respond by integrating wired BUS systems in new projects so buyers qualify automatically for future deductions.[2]Salone Milano, “Italy's 2025 financial manoeuvre and the building bonuses, what's changing?,” salonemilano.it

Enhanced Home Security Demand

Urbanization and rising property values stimulate demand for DIY-friendly cameras, sirens, and video doorbells that blend aesthetics with analytics. BTicino’s Home + Security suite links Netatmo cameras to MyHome alarms, adding facial recognition and geofencing without monthly fees.[3]BTicino International, “Smart products | Bticino International,” bticino.com Nice OS 8.9 brings multi-protocol support and predictive automation, notifying residents before perimeter breaches occur . Despite product simplicity, installation is often outsourced: more than 15,000 certified electricians install alarms yet operate as fragmented micro-firms, reinforcing distribution partnerships for ecosystem leaders. Their expertise ensures code compliance, which is critical because insurers now grant premium discounts only for certified systems. These dynamics keep the Italy smart home market on a technology-plus-services trajectory.

AI-IoT-5G Convergence

Rollout of standalone 5G enables low-latency links between sensors and edge gateways, letting AI models run locally for voice, vision, and energy-balancing tasks. Thread/Matter adoption grew sharply in 2024, with tests confirming more stable mesh coverage than conventional Wi-Fi in large Italian homes.[4]Thread Group, “Robust IoT Connectivity with Thread,” threadgroup.org BTicino’s Living Now range uses existing wires for power yet presents Wi-Fi or Thread radios for over-the-air updates. Research by Politecnico di Torino shows that multimodal command disambiguation, combining gestures and Italian voice cues, lifts smart speaker accuracy above 94%. This interoperability reduces vendor lock-in and paves the way for platform subscriptions around energy, security, and elder care, giving device makers additional monetization layers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device & installation costs | −4.2% | National, more pronounced in South and Islands | Medium term (2-4 years) |

| Data privacy & cyber-security concerns | −3.8% | National, heightened in urban centers | Short term (≤ 2 years) |

| Fragmented installer/system-integrator ecosystem | −2.9% | National, particularly affecting smaller municipalities | Medium term (2-4 years) |

| Limited Italian-language voice-assistant support | −1.8% | National, gradually improving | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy & Cyber-Security Concerns

Frequent media reports on IoT breaches heighten Italian consumer vigilance, especially after DDoS attacks exploited home routers in late 2024. Municipal smart-city pilots have also exposed gaps in GDPR compliance, eroding trust in cloud-based services. Vendors have answered with hardware-rooted encryption, Bluetooth Low Energy authentication, and ISO 27001-certified cloud storage, yet skepticism lingers for devices from lesser-known brands. The Italy smart home market therefore devotes rising R&D budgets to secure-by-design frameworks, hoping to reposition privacy as a selling point rather than a trade-off.

High Upfront Device & Installation Costs

Average household income in Sicily and Calabria remains 25% below the northern average, dampening adoption of whole-home systems costing EUR 2,500 to EUR 7,000. Installer fragmentation fuels price dispersion, with quotes varying up to 35% across provinces for the same package. Utilities now bridge the gap: Enel offers zero-interest loans bundled with EUR 600 bill credits for customers choosing integrated solar plus smart-home packages. Meanwhile, immediate cash-register rebates under Bonus elettrodomestici diffuse cost anxiety at the entry level. These measures soften resistance, yet affordability remains a gating issue for mass-scale penetration in the Italy smart home market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Smart Appliances Sustain Leadership While Energy Management Accelerates

Smart appliances held 34.62% of 2025 revenue as Italian consumers gravitated toward tangible energy and time savings such as auto-dosing washers and adaptive hobs. Brand alliances between appliance makers and connectivity platforms shorten setup time, reinforcing retail channel dominance. The Italy smart home market benefits when customers bundle refrigerators with voice-enabled sockets, thereby amplifying attachment rates. Energy management systems, while accounting for a smaller absolute base, are forecast to grow at 12.96% CAGR as RECs spread and solar paybacks compress. These platforms align cloud analytics with local controllers to maximize self-consumption, a feature valued by prosumers facing volatile time-of-use tariffs.

The segment also attracts utility partnerships: Enel X’s Waybox integrates EV charging curves with rooftop generation to flatten grid peaks. Italian start-ups focus on AI-driven load orchestration that learns occupancy patterns, lifting comfort without oversizing batteries. As a result, the Italy smart home market size for energy management is expected to touch USD 2.01 billion by 2031. Security, entertainment, and lighting remain complementary baskets, driving cross-sell momentum inside omnichannel showrooms.

By Installation Type: Retrofit Dominance Gives Way to Rising New-Build Integration

Retrofit projects captured 62.05% of 2025 spending because 70% of Italy’s housing stock predates 1980, and fiscal deductions continue to steer owners toward energy overhauls. Electricians retro-fit smart switches over existing back-boxes, while radio-based sensors avoid channelling walls, containing labor outlays. Nonetheless, fresh building codes compel developers to wire for future smart upgrades, which pushes new-build installations toward a 14.75% CAGR.

Property developers collaborate with BTicino and Vimar to pre-install BUS lines and central hubs that activate via software licences once occupants move in. This approach safeguards initial budgets while assuring scalability. Consequently, the Italy smart home market size for new-build projects is on track to close the share gap by 2030. Banks increasingly link green mortgages to pre-equipped dwellings, making connected-ready homes more attractive in resale valuations.

By Connectivity Technology: Wi-Fi Prevails but Thread/Matter Triggers Fastest Upswing

Wi-Fi retained 58.75% share owing to near-universal broadband penetration and familiar setup flows. Consumers appreciate router upgrades that now bundle Zigbee or BLE radios, simplifying onboarding through a single app. However, Thread/Matter edges ahead in growth with an 17.2% CAGR, thanks to its self-healing mesh and vendor-agnostic certification regime. The Italy smart home market thus sees retailers highlighting “Matter-Ready” icons to future-proof purchases.

Professionally installed Zigbee and Z-Wave networks stay relevant in larger villas demanding sub-second reliability for shutters, HVAC, and alarms. KNX remains the premium wired standard in architectural showpieces. Vendors now integrate multi-radio SoCs, letting installers swap protocols via firmware rather than hardware, which cuts truck rolls and accelerates payback.

By End-User Housing Type: Apartments Hold the Lead While Detached Houses Accelerate

Apartments and condominiums represented 49.85% of 2025 demand because shared fiber backbones, concierge services, and collective bargaining reduce per-unit costs. In Milan and Turin, management committees negotiate bulk purchases of video door entry systems, lifting penetration floor-by-floor. Yet detached houses are positioned for a 12.55% CAGR as Lombardy and Veneto homeowners invest in solar-plus-storage bundles to counter energy-price volatility.

Larger footprints in villas justify multi-zone climate control, irrigation automation, and perimeter security, raising average ticket sizes. Historic dwellings, a hallmark of Italian heritage, embrace non-invasive radio modules to avoid masonry work, and tax credits cover restoration that improves efficiency. These trends expand the Italy smart home market’s revenue diversity across housing archetypes.

By Distribution Channel: Retail & E-Commerce Continue to Dominate but Utility Bundles Surge

Retailers and marketplaces claimed 52.35% share in 2025 due to instant product availability and seasonal promotions. Hardware brands invest in end-cap displays and demo corners, driving impulse adoption of smart bulbs and plugs. Nonetheless, telecom and utility bundles display the quickest momentum at 15.45% CAGR as firms like TIM package fiber, 5G FWA, and home-automation kits under single invoices.

Utility bundles also capitalize on energy-efficiency KPIs: Enel credits monthly bills when usage stays below preset thresholds, reinforcing app engagement. Professional installers cater to complex retrofits and heritage sites, while direct-to-consumer webshops of niche brands attract tech enthusiasts. Collectively, these routes enlarge the Italy smart home market by aligning distribution with consumer confidence levels and wallet sizes.

Geography Analysis

North-West Italy keeps its leadership by pairing industrial know-how with consumer purchasing power; BTicino alone generated EUR 1 billion turnover in 2023 from domestic operations centered in this corridor. Local governments advance smart-city roadmaps that encourage integrated building permits, accelerating platform adoption among developers. This synergy lifts the Italy smart home market in cities such as Milan and Bergamo, where average spending per household is 35% above the national mean.

North-East regions follow with vibrant clusters in Veneto and Emilia-Romagna that export mechatronics globally and champion Industry 4.0 tax credits. These firms upskill workforces in IoT, indirectly fostering residential uptake as employees import know-how into personal projects. Cross-border trade with Austria and Slovenia also exposes households to interoperable standards, tightening demand for Thread-certified devices. Regional utilities pilot dynamic tariffs that reward consumption shifts, nudging users toward load-balancing hubs.

Central Italy adds steady volume through Rome’s metropolitan renovations and public-sector building upgrades. Historic architecture necessitates surface-mounted channels and wireless sensors that leave frescoes intact. Lazio’s cultural-heritage office now includes energy analytics in restoration guidelines, giving a formal stamp to smart retrofits. Meanwhile, the Apennine earthquake-relief program funds renewable energy communities that funnel surplus power to rebuilt houses, embedding automation from day one.

The South and Islands, historically under-served, accelerate thanks to digital-divide funding that laid high-speed fiber in 2024. Sicily’s Villafranca Padovana pilot logged 60% self-consumption via solar-optimized hubs, becoming a template for 200 upcoming communities nationwide mdpi.com. Sardinia’s rugged terrain favors radio protocols over new cabling, propelling multi-band gateways. Lower average incomes remain a drag, yet cash-register rebates and zero-interest loans narrow affordability gaps. This balancing act is vital for inclusive expansion of the Italy smart home market.

Competitive Landscape

The domestic arena shows moderate concentration, with the top five vendors accounting for about 70% of revenue. BTicino leads by combining Italian design credentials with deep installer relationships and a catalog spanning wiring accessories to cloud dashboards. Its Home + Project app, refreshed in May 2025, lets professionals design entire systems and export bills of material in minutes, streamlining tender cycles. The firm also funnels R&D learnings from its datacenter segment now 20% of group revenue into edge-computing gateways that cut latency for home automations.

Nice SpA positions itself as a full-stack platform supplier after consolidating ELAN, SpeakerCraft, and Panamax into a unified NiceOS, coupled with the OS 8.9 software released in October 2024. The update introduced geofencing routines that pre-cool rooms when residents near home, bolstering differentiation in the premium tier. Vimar banks on aesthetics, earning the 2025 IF Design Award for its Eikon Exé line, which integrates capacitive touch with customizable finishes for luxury interiors.

Enel X exploits utility customer intimacy by bundling solar arrays, EV chargers, and smart-home subscriptions under unified financing. TIM leans on its fiber footprint to cross-sell cloud backup and managed Wi-Fi plus a Matter-certified starter kit, boosting average revenue per user. Smaller local integrators remain competitive in heritage renovations requiring bespoke solutions, but they often rely on OEM partnership programs for certification. Thread and Matter standards reshuffle the deck, lowering entry barriers for agile newcomers, yet incumbents still wield brand trust and channel depth that underpin the Italy smart home market.

Italy Smart Home Industry Leaders

Legrand

ABB Ltd.

Samsung Electronics Co. Ltd

LG Electronics

Lutron Electronics Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BTicino launched the enhanced Home + Project app, expanding installer design and configuration features.

- May 2025: The Italian government activated the Bonus elettrodomestici 2025, offering immediate EUR 200 discounts on efficient appliances from a EUR 50 million fund.

- April 2025: BTicino issued the 2025 edition of its 2-Wires Video Door Entry Technical Guide to support system integrators.

- March 2025: BTicino’s Linea 5000 smart entrance panel won the IF Design Award for innovation and functionality.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italian smart home market as all network-connected consumer devices and software that allow residents to remotely monitor, automate, or optimize functions such as lighting, climate, entertainment, security, and major household appliances within detached houses, apartments, and heritage dwellings. According to Mordor Intelligence, this connected-device spend will reach about USD 2.54 billion in 2025 (mordorintelligence.com).

Scope exclusion: The model deliberately leaves out pure B2B building-automation systems installed in hotels, offices, or industrial premises.

Segmentation Overview

- By Product

- Comfort and Lighting

- Control and Connectivity

- Energy Management

- Home Entertainment

- Security

- Smart Appliances

- By Installation Type

- New-build Integrated

- Retrofit / Add-on

- By Connectivity Technology

- Wi-Fi

- ZigBee / Z-Wave

- Bluetooth Low Energy

- Thread / Matter

- Other Protocols

- By End-User Housing Type

- Apartments and Condominiums

- Detached Houses and Villas

- Heritage / Historic Buildings

- By Distribution Channel

- Professional Installers

- Retail and E-commerce

- Telecom and Utility Bundles

Detailed Research Methodology and Data Validation

Primary Research

Our analysts held structured calls with Italian smart-device installers, retail buyers, utility IoT program leads, and product managers of global OEMs operating local subsidiaries. These discussions clarified average selling prices, installation mixes (DIY versus professional), and the real-world impact of tax credits such as Superbonus 110 on future demand.

Desk Research

We began with national statistics from ISTAT for dwelling counts, age of housing stock, and disposable income trends, followed by device import data from Italian Customs and monthly broadband-penetration files released by AGCOM. Energy-savings baselines came from Gestore dei Servizi Energetici (GSE) and EU Fit-for-55 documentation, while adoption curves and pricing snapshots were cross-checked through the annual Internet of Things Observatory at Politecnico di Milano. Paid datasets from D&B Hoovers and Dow Jones Factiva helped us extract revenue splits and newsflow for leading OEMs. This list is indicative; many other public and proprietary sources supported validation efforts.

Market-Sizing & Forecasting

The topline value is first built top-down: household stock × smart-home penetration × mean annual spend, using granular inputs like broadband access rates, smart-meter rollout, and renovation incentive uptake. Select bottom-up checks, sampled vendor revenues and channel surveys, are then overlaid to fine-tune totals. Key variables include (1) average device ASP movements, (2) connected-appliance shipment growth, (3) security-system installation permits, (4) Matter-protocol adoption pace, and (5) regional GDP per capita shifts. A multivariate-regression model forecasts each driver and feeds a scenario engine that evaluates conservative, base, and accelerated uptake paths before locking the published CAGR. Gaps in sub-segment data are bridged with interpolation anchored on disclosed company splits and validated by retailer sell-through ratios.

Data Validation & Update Cycle

Every draft model is stress-tested against third-party indices and historical outliers. Senior reviewers sign off only after anomaly reconciliation and variance checks. Reports refresh yearly, and interim updates are triggered by material events such as incentive-scheme revisions or large M&A deals; a final analyst sweep is completed just before delivery.

Why Our Italy Smart Home Baseline Commands Trust

Published estimates often diverge because firms choose different device scopes, currency years, and refresh cadences.

Key gap drivers include whether retrofit spending is counted, how aggressively future ASP declines are assumed, and the timeliness of household-penetration inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.54 B (2025) | Mordor Intelligence | |

| USD 0.98 B (2024) | Regional Consultancy A | Counts only appliances and security; omits retrofit labor cost |

| USD 2.06 B (2023) | Global Consultancy A | Older base year and static FX conversion inflate gap |

| USD 3.39 B (2023) | Industry Association B | Includes small-commercial automation and hotel refurbishments |

The comparison shows that once scope, currency timing, and retrofit considerations are aligned, Mordor's disciplined mix of top-down modeling and primary validations delivers a balanced, transparent baseline clients can rely on for strategic decisions.

Key Questions Answered in the Report

What is the current value of the Italy smart home market?

The Italy smart home market size stood at USD 2.78 billion in 2026 and is projected to reach USD 4.34 billion by 2031.

How fast is the market growing?

It is expected to register a 9.35% CAGR during 2026-2031, driven by fiscal incentives, energy-efficiency goals, and technology convergence.

Which product segment is expanding the quickest?

Energy management solutions are forecast to grow at a 12.96% CAGR thanks to renewable energy communities and dynamic tariffs.

Who holds the largest market share among suppliers?

BTicino (Legrand Group) leads with 64% share of residential revenues, leveraging extensive installer networks and a broad product portfolio.

Why are Thread and Matter protocols important for Italian homes?

They deliver vendor-agnostic, self-healing mesh connectivity that improves reliability and simplifies setup, supporting the fast growth of interoperable devices.

Page last updated on: