France Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

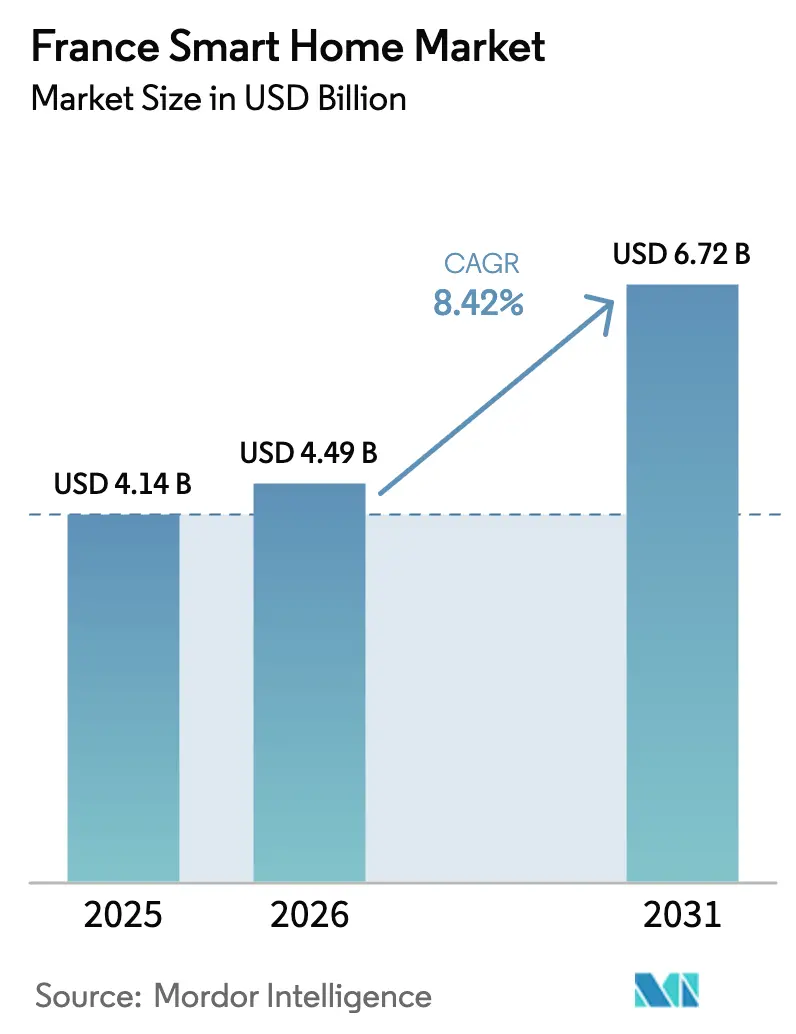

| Base Year Market Size (2025) | USD 4.14 Billion |

| Market Size (2026) | USD 4.49 Billion |

| Market Size (2031) | USD 6.72 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Smart Home Market Analysis by Mordor Intelligence

France Smart Home market size in 2026 is estimated at USD 4.49 billion, growing from 2025 value of USD 4.14 billion with 2031 projections showing USD 6.72 billion, growing at 8.42% CAGR over 2026-2031. Growth rests on three pillars: the MaPrimeRénov' incentives that refund up to 80% of eligible renovation costs, the rapid embrace of the Matter protocol that eases cross-brand pairing, and a 5G backbone that already covers 83.9% of licensed sites across the country. Together, these tailwinds are moving the France Smart Home market past the early-adopter stage toward mass-market uptake. Demand is strongest for security devices, yet government pressure to trim household energy use is shifting attention—and budgets—toward smart thermostats, lighting, and load-balancing services. Telecom carriers are bundling connected-home kits with broadband, turning subscription models into a new growth lever. Meanwhile, established French suppliers leverage their local installer networks and GDPR-ready data controls to defend share against global platform players.

Key Report Takeaways

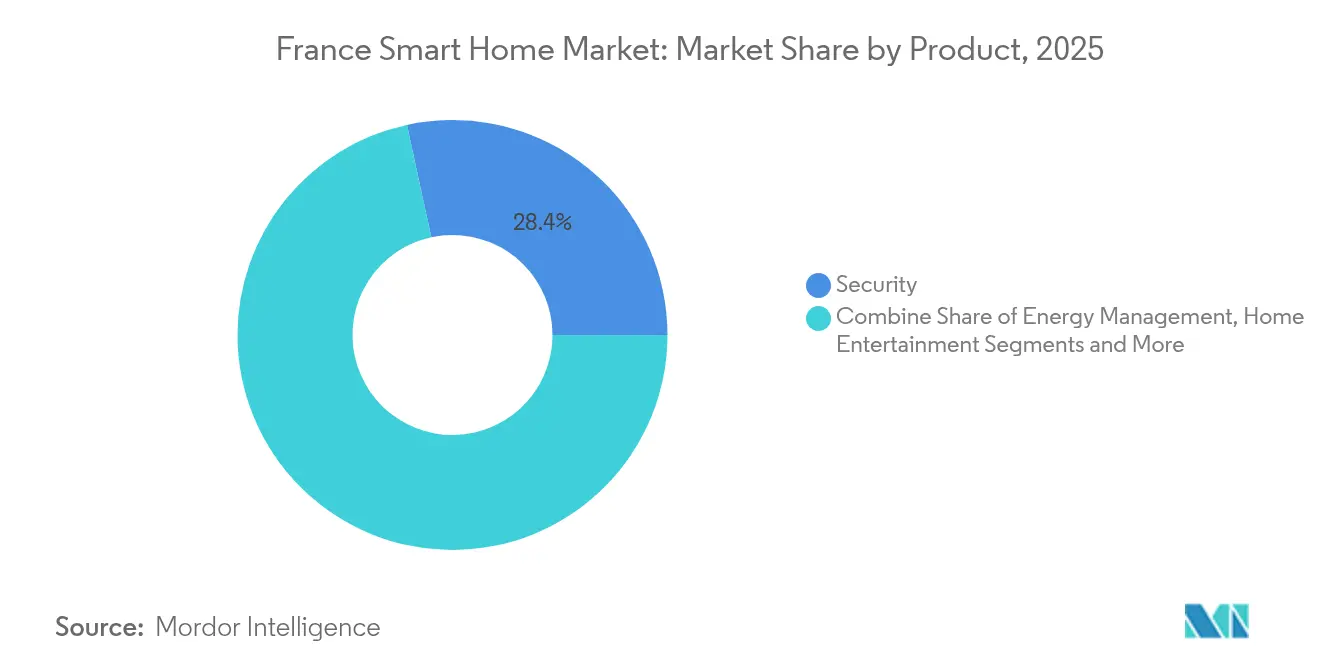

- By product category, security systems held 28.40% of the France Smart Home market share in 2025, whereas energy management solutions are forecast to grow at 13.9% CAGR through 2031.

- By connectivity technology, Wi-Fi led with a 61.90% share of the France Smart Home market size in 2025; Zigbee & Thread devices should expand at a 18.1% CAGR to 2031.

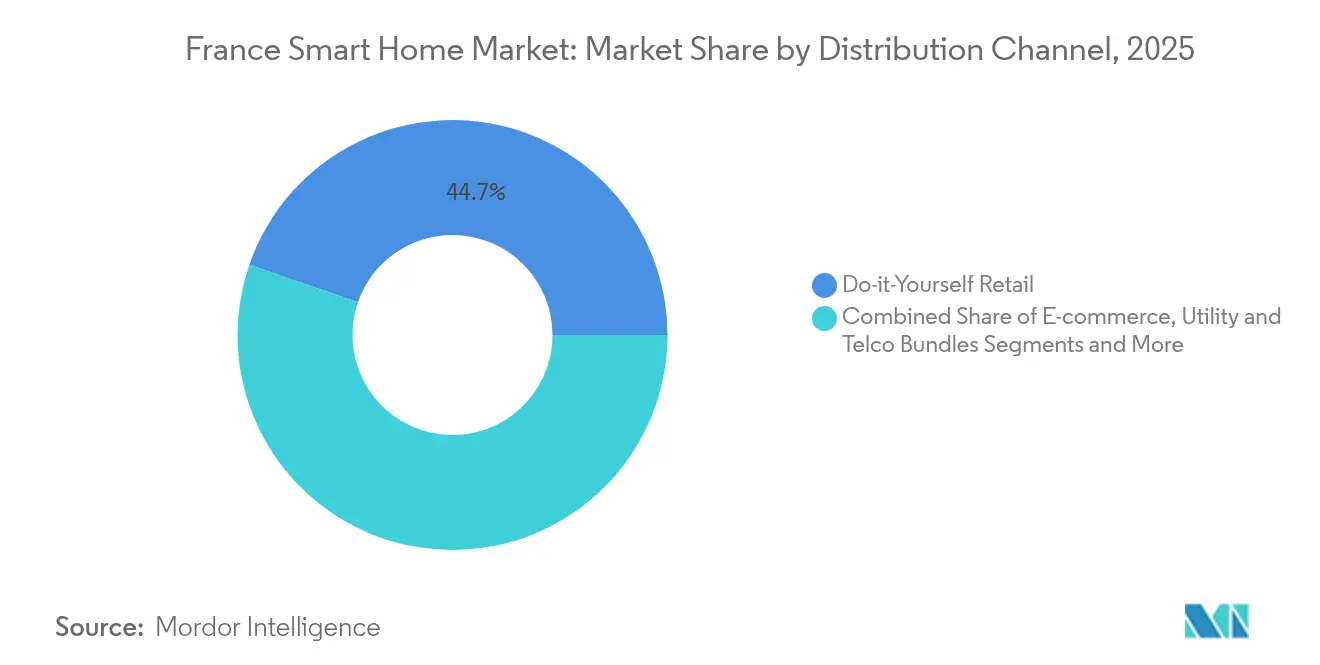

- By distribution channel, DIY retail accounted for 44.70% of the France Smart Home market size in 2025, while utility and telco bundles will post the quickest rise at 10.7% CAGR.

- By dwelling type, single-family homes represented 64.10% of the France Smart Home market share in 2025; multi-family apartments will advance at 11.3% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of voice assistants with French-language NLP | +3.2% | National, higher penetration in urban areas | Medium term (2–4 years) |

| Government tax credits for energy-renovation devices (MaPrimeRénov') | +4.8% | National, enhanced benefits for energy-inefficient homes | Short term (≤2 years) |

| Growing consumer focus on burglary deterrence & surveillance | +2.9% | National, premium uptake in Île-de-France and Provence-Alpes-Côte d'Azur | Medium term (2–4 years) |

| Interoperable Matter standard speeding multi-brand compatibility | +3.7% | Global, early adoption in tech-forward regions | Medium term (2–4 years) |

| Utility-led demand-response programs using smart thermostats | +2.6% | National, coordinated through Enedis smart grid infrastructure | Long term (≥4 years) |

| 5G fixed-wireless roll-out enabling rural smart-home broadband | +2.1% | Rural France, particularly underserved departments | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of voice assistants with French-language NLP

Voice assistants are moving from novelty to necessity in the France Smart Home market. Roughly 30% of households already own a smart speaker, with usage up 20% year on year. Amazon’s Alexa+ upgrade promises richer French dialogue and on-device processing that eases privacy fears.[1]Numerama, “Amazon annonce Alexa+,” numerama.com Local AI ventures such as Mistral AI reinforce the domestic ecosystem with language models tuned to regional idioms. Easier voice control opens connected-home benefits to seniors and first-time users, enlarging the addressable base for the France Smart Home market.

Government tax credits for energy-renovation devices (MaPrimeRénov')

MaPrimeRénov' disbursed EUR 3.4 billion in 2025, reimbursing up to 80% of smart thermostats, zoning controls, and energy-monitoring kits for middle-income households.[2]Service-Public, “Quelles sont les conditions pour bénéficier du dispositif MaPrimeRénov' en 2025 ?,” service-public.fr By waiving an energy-performance audit, the 2025 update cut paperwork and accelerated retrofit timelines, particularly in aging suburban housing. Coupled with 37.5 million Linky meters already in place, the subsidy ties connected devices directly to lower utility bills—a persuasive argument that keeps the France Smart Home market on its steep climb.

Growing consumer focus on burglary deterrence & surveillance

Property crime headlines have boosted demand for smart cameras, video doorbells, and learning-enabled lighting scenes. Security devices captured the largest slice of France Smart Home market revenue in 2024. Insurance rebates for certified systems and AI-based motion analytics that flag anomalies in real time underpin continued momentum. Yet privacy oversight remains strict: CNIL’s 2024 probe on QR code verification in cameras reminds vendors that compliance is non-negotiable.[3]CNIL, “Délibération SAN-2024-019 du 14 novembre 2024,” legifrance.gouv.fr

Interoperable Matter standard speeding multi-brand compatibility

Matter 1.4 extends certification to heat pumps and solar inverters, unifying device discovery across Apple, Google, Amazon, and Samsung ecosystems.[4]The Verge, “Matter 1.4 tries to set the smart home standard back on track,” theverge.com French heavyweights Somfy, Schneider Electric, and Legrand contributed to the spec, ensuring their catalogs remain first-choice options in the France Smart Home market. Installation ease lifts DIY sales and curbs buyer hesitation over brand lock-in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of certified installers outside major metros | -2.8% | Rural France and smaller metropolitan areas | Medium term (2–4 years) |

| Heightened data-privacy concerns (CNIL enforcement) | -1.9% | National, stricter compliance requirements | Short term (≤2 years) |

| Fragmented UX for senior citizens & non-tech users | -1.4% | National, higher impact in aging rural communities | Long term (≥4 years) |

| Inflation-driven cut-back on discretionary renovation spend | -2.3% | National, varies by economic conditions | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Scarcity of certified installers outside major metros

Complex projects—panel upgrades, HVAC integration, EV charger tie-ins—still need pros. Yet most Qualifelec-accredited electricians cluster in Paris, Lyon, and Marseille, leaving rural homeowners with long wait times. Even as 5G fixed-wireless solves connectivity gaps, human-capital bottlenecks cap the France Smart Home market’s full potential in outlying departments.

Heightened data-privacy concerns (CNIL enforcement)

CNIL fined Orange EUR 50 million over cookie mismanagement, underscoring a tough stance on personal data. Connected-home suppliers must build consent granularity and local storage options into products, adding cost and time to launches. Consumers remain wary: polls show 62% fear voice recordings could be misused. Unless vendors sustain transparent practices, privacy anxieties could stall uptake in the France Smart Home industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Security Dominance Masks Energy Management Surge

Security solutions commanded 28.40% of 2025 revenue, anchoring the France Smart Home market through doorbells, cameras, and locksets that integrate with mobile alert apps. High-definition video and AI scene recognition justify premium pricing, particularly in urban centers. Yet energy management units are scaling faster at 13.9% CAGR as households chase lower bills and MaPrimeRénov' refunds. In value terms, the energy segment could eclipse home security before 2030, turning kilowatt savings into a primary adoption trigger. Control hubs and voice assistants maintain baseline demand because they serve as the connective tissue linking lighting scenes, appliance schedules, and security routines. Home entertainment devices ride the broadband boom, while smart appliances—fridges, ovens, dishwashers—record rising basket sizes thanks to bundled warranties and predictive-maintenance alerts. Health and wellness gear, from indoor-air sensors to fall-detection wearables, lags behind due to interoperability gaps with medical ecosystems, though demographic aging suggests future upside for the France Smart Home market.

By Connectivity Technology: Wi-Fi Stability Enables Thread Innovation

Wi-Fi remained the anchor protocol with 61.90% share of the France Smart Home market size in 2025, favored for bandwidth-heavy video feeds and its ubiquity in ISP routers. Thread and Zigbee, however, are expanding at a 18.1% CAGR on the back of Matter. Thread’s self-healing mesh reduces latency for light switches and sensors while prolonging battery life, a clear selling point for apartment dwellers who avoid rewiring. Bluetooth Low Energy continues as the preferred commissioning pathway, letting users onboard gadgets from a phone within seconds. Z-Wave sees attrition as openness wins mindshare, yet bridges preserve installed bases in high-end builds. 5G indoor coverage plus network-slicing trials by Free and Orange hint at future service tiers that guarantee packet priority for alarms or medical alerts, reinforcing the France Smart Home market’s evolution toward utility-grade reliability.

By Distribution Channel: DIY Retail Leads While Utilities Accelerate

DIY outlets such as Leroy Merlin and Castorama delivered 44.70% of 2025 sales. Shelf-edge QR codes now launch explainer videos, removing installation anxiety and boosting basket conversion for the France Smart Home market. Product returns fell after Matter shrugged off pairing errors, improving retailer margins. Utility and telco bundles, though smaller, will outpace all channels at 10.7% CAGR through 2031. Enedis links tariffs to consumption targets, while Bouygues and SFR bundle camera kits with fiber or 5G home internet. E-commerce holds steady on breadth and price transparency, yet complexity drives many shoppers to hybrid models—buy online, install via vetted partners. Pro-install system integrators defend luxury niches, offering concealed cabling and centralized racks for villas along the Côte d’Azur.

By Dwelling Type: Single-Family Leadership Faces Multi-Family Challenge

Detached houses owned 64.10% of revenue in 2025, reflecting higher per-home device counts and freedom to rewire. Owners view automation as both lifestyle upgrade and resale booster, sustaining average order values above USD 1,200 per project. Apartments, however, bring the fastest growth at 11.3% CAGR. Wireless switches, battery-powered blinds, and stick-on sensors avoid landlord objections, opening a path for renters to join the France Smart Home market. Condominium associations also deploy shared access control and energy metering that spread costs across units. As RE2020 standards push for thermal efficiency, developers now pre-wire smart ventilation in new multi-family builds, shrinking the capability gap with single-family homes.

Geography Analysis

Île-de-France generated 30.90% of national revenue in 2025. High disposable incomes, dense installer networks, and 95% 5G population coverage create ideal adoption conditions. Residents allocate larger budgets to multi-sensor security and load-balancing EV chargers that coordinate with household demand curves Alternative Fuels Observatory . Occitanie stands out with a 25.6% forecast CAGR. Fixed-wireless 5G bridges the countryside, bringing bandwidth to farmhouses and second homes once beyond DSL range ANFR . Coupled with abundant solar rooftops, households adopt optimizers that juggle self-consumption, storage, and grid export. Rural installers partner with energy cooperatives to bundle panels, batteries, and connected load controllers—extending the France Smart Home market into villages once off the radar. Elsewhere, Auvergne-Rhône-Alpes benefits from a robust electronics cluster and higher property values, driving premium renovations. Normandy and Brittany trail but gain ground through government digital-divide funding that subsidizes fiber backbones. Across regions the adoption map aligns less with urban versus rural labels and more with the intersection of broadband reach, installer availability, and renovation budgets, highlighting where the France Smart Home market can scale next.

Competitive Landscape

The France Smart Home market shows moderate fragmentation. Domestic champions Somfy, Schneider Electric, and Legrand pair century-old electrical know-how with cloud dashboards and Matter bridges, creating end-to-end propositions that global tech giants cannot easily replicate. Legrand’s 2018 Netatmo buy unlocked consumer-grade design, now integrated into switchgear and panelboards. Schneider builds energy stacks that span breakers to EV chargers, while Somfy leans on 60 million installed motors to upsell automation via its TaHoma hub.

International platforms Amazon, Google, Samsung command the software layer with voice, search, and AI recommendation engines. They woo French buyers by offering local-language assistants and bundling cloud storage for camera footage. Yet GDPR and CNIL oversight tilt the playing field toward firms with localized servers and explicit consent flows, advantages French incumbents already bank on.

White-space is forming around apartment-centric packages, elder-care routines, and renewable orchestration. Comwatt markets AI energy managers that shave peak usage and monetize surplus solar. Overkiz embeds cloud APIs for OEMs that lack digital muscle. As platforms congeal, hardware margins shrink; ecosystem control and recurring analytics fees look set to decide long-term winners in the France Smart Home market.

France Smart Home Industry Leaders

Siemens AG

ABB Ltd

Schneider Electric SE

Honeywell International Inc.

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Legrand reported 11.2% sales growth and 20.7% adjusted operating margin in Q1 2025, with data centers accounting for 20% of sales in 2024 as the company accelerates organic growth in digital infrastructure markets. The company confirmed its 2025 full-year targets and announced two acquisitions since the beginning of the year, strengthening its position in connected building solutions Legrand.

- February 2025: Amazon announced Alexa+ featuring generative AI capabilities powered by Amazon Nova and Anthropic's Claude models, initially limited to the United States but representing significant advancement in voice assistant technology that will eventually impact French smart home markets. The enhanced assistant includes capabilities for ordering groceries, sending invitations, and analyzing photos, with integration planned for Echo devices and mobile applications Numerama.

- January 2025: ACWA Robotics raised EUR 4.8 million from investors including Banque des Territoires to advance robots for mapping and inspecting water networks, addressing infrastructure efficiency challenges where nearly 20% of drinking water is lost annually in France's distribution networks. The funding supports technical development and commercial launch of the Pathfinder robot for water supply networks Banque des Territoires.

- November 2024: CNIL fined Orange SA EUR 50 million for violations of data protection regulations concerning commercial prospecting via electronic means and cookie usage, demonstrating heightened regulatory enforcement that impacts smart home companies' data collection practices. The decision includes injunctions requiring effective consent withdrawal mechanisms and public disclosure requirements CNIL.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines France's smart home market as the annual value generated by connected devices and integrated software platforms that automate security, energy, comfort, entertainment, and wellness functions inside residential dwellings. The boundary covers device sales, installation revenues, and subscription-based digital services that enable in-home or remote control.

Scope exclusion: Standalone white goods without connectivity modules are outside our numbers.

Segmentation Overview

- By Product

- Comfort and Lighting

- Control and Connectivity

- Energy Management

- Home Entertainment

- Security

- Smart Appliances

- Health and Wellness Devices

- By Connectivity Technology

- Wi-Fi

- Bluetooth and BLE

- Zigbee and Thread

- Z-Wave

- Proprietary / Other

- By Distribution Channel

- Do-it-Yourself Retail

- Pro-install / System Integrators

- E-commerce

- Utility and Telco Bundles

- By Dwelling Type

- Single-family Houses

- Multi-family Apartments

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers, telecom aggregators, energy utilities, and insurers across Île-de-France, Occitanie, and Provence. These conversations, complemented by an online consumer survey, clarified device replacement cycles, average selling prices, and evolving service bundles, allowing us to challenge and refine desk findings before locking assumptions.

Desk Research

We began by mapping the device universe through public sources such as France's National Institute of Statistics, Eurostat energy-usage datasets, the French Digital Council's IoT adoption briefs, and trade association releases from GIFAM and FIEEC. Company filings, investor decks, and reputable press added shipment clues, while paid databases like D&B Hoovers and Dow Jones Factiva provided revenue splits for leading vendors. Patent families from Questel, household broadband penetration data from ARCEP, and customs imports retrieved via Volza helped us size cross-border inflows of hubs and sensors. The sources listed illustrate the breadth; many further references informed smaller checks and clarifications.

Market-Sizing & Forecasting

A national demand pool was assembled through a top-down construct that starts with French households, layers security system penetration, smart-meter rollout rates, and average connected-device count per home, and then multiplies by validated ASPs. Supplier roll-ups on cameras and thermostats acted as bottom-up guardrails. Key variables tested in the model include residential electricity tariffs, fiber broadband coverage, new-build completions, and insurance rebates for monitored alarms. Forecasts rely on multivariate regression, where device uptake is explained by disposable income growth, broadband speed improvement, and tariff inflation scenarios that were vetted with our primary-research panel. Gaps from smaller installers were bridged using weighted channel mark-ups derived from Pro-install invoices shared confidentially.

Data Validation & Update Cycle

Outputs face automated variance scans, peer review, and a senior analyst sign-off. We refresh every twelve months and trigger interim updates when France adjusts energy tariffs, enacts major IoT security mandates, or when two consecutive quarters show greater than 5% variance versus shipment trackers.

Why Mordor France Smart Home Baseline Earns Everyday Decision Trust

Published estimates rarely align because firms differ on which devices belong, how service revenue is booked, and how often numbers get refreshed.

We recognize these moving parts and purposefully anchor our baseline in 2025, the first full year after France's nationwide Linky smart-meter installation crossed 95% of households, ensuring today's device-energy interplay is fully captured.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.14 billion (2025) | Mordor Intelligence | - |

| USD 3.45 billion (2023) | Regional Consultancy A | Security-centric scope, excludes subscription apps, older base year |

| USD 4.51 billion (2023) | Global Consultancy B | Retail ASPs only, no service revenue, counts repairs within totals |

| USD 3.20 billion (2024) | Industry Association C | Smart-appliance focus, static tariff assumption, limited channel coverage |

Taken together, the comparison shows how Mordor's disciplined scope selection, current data vintage, and dual-stage validation provide a balanced, transparent baseline that decision-makers can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the current value of the France Smart Home market?

The market is valued at USD 4.49 billion in 2026 and is forecast to climb to USD 6.72 billion by 2031 at a 8.42% CAGR.

Which product category generates the most revenue today?

Security devices lead with 28.40% market share, driven by connected cameras, smart locks, and alarm systems.

How do MaPrimeRénov' incentives influence adoption?

The scheme refunds up to 80% of eligible smart energy devices, sharply lowering payback periods and accelerating thermostat and monitoring sales.

Why is Matter important for French consumers?

Matter certification assures that devices from Apple, Google, Amazon, Samsung, and French brands interoperate, reducing installation friction and future-proofing investments.

What role do utilities play in distribution?

Utilities and telecom operators bundle smart-home kits with broadband or dynamic tariffs, and this channel is expected to expand at 10.70% CAGR through 2031.

Page last updated on: