Germany Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

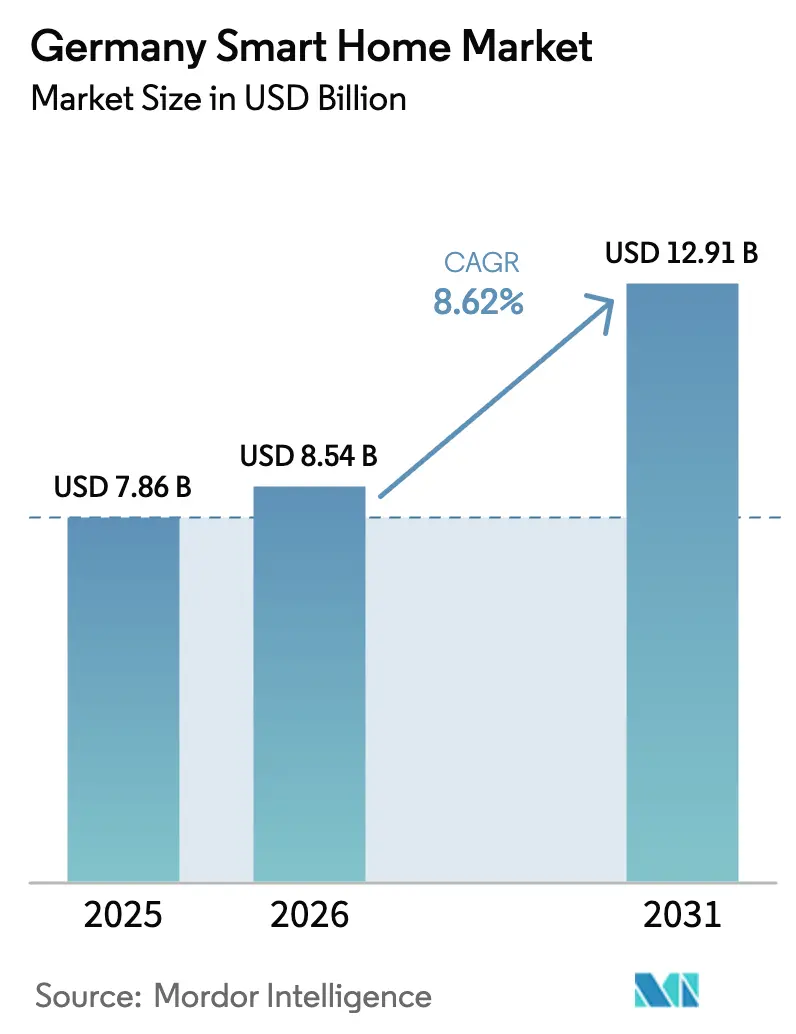

| Base Year Market Size (2025) | USD 7.86 Billion |

| Market Size (2026) | USD 8.54 Billion |

| Market Size (2031) | USD 12.91 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Smart Home Market Analysis by Mordor Intelligence

Germany Smart Home Market size in 2026 is estimated at USD 8.54 billion, growing from 2025 value of USD 7.86 billion with 2031 projections showing USD 12.91 billion, growing at 8.62% CAGR over 2026-2031. Demand remains resilient despite broader construction headwinds because mandatory smart-meter rollouts and energy-efficiency incentives create a clear investment case. Rising smartphone and broadband penetration ensures that connectivity bottlenecks diminish, while the Matter protocol jump-starts device interoperability. Competitive momentum intensifies as global technology groups enter a field once dominated by domestic engineering firms, prompting faster product cycles and price competition. At the same time, shortages of qualified installers temper near-term growth, encouraging do-it-yourself solutions and hybrid service models.

Key Report Takeaways

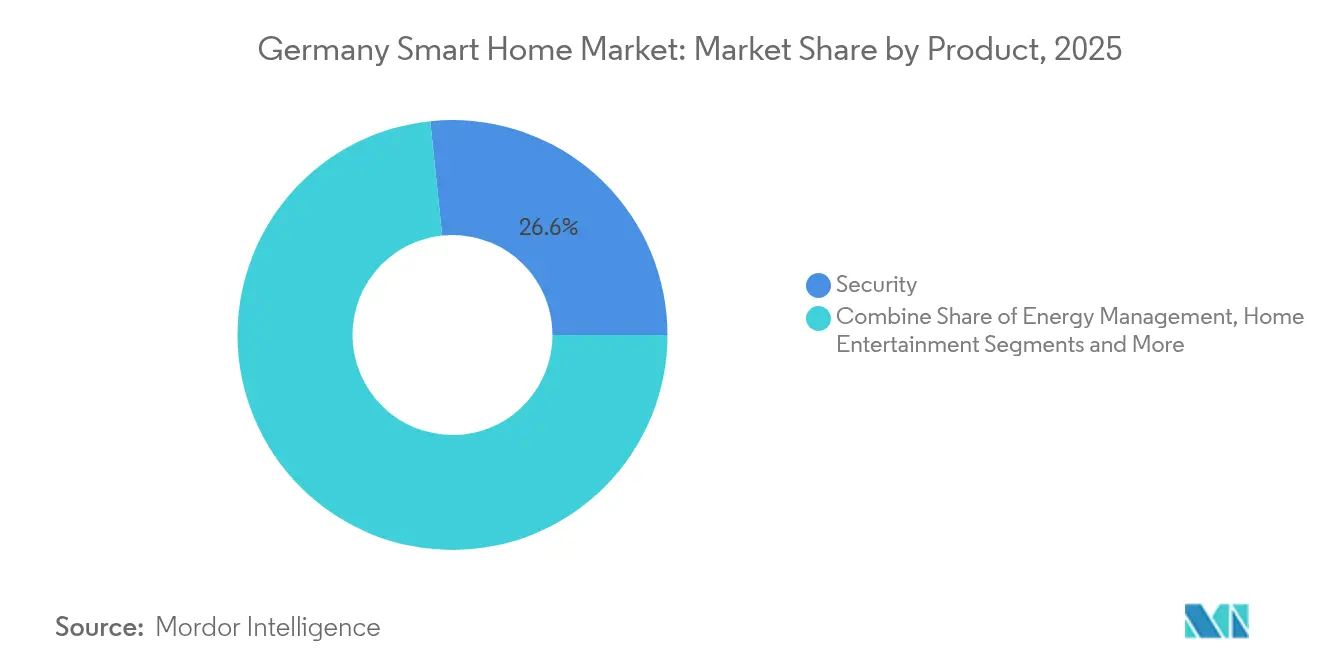

- By product category, security systems led with 26.65% revenue share in 2025, whereas energy management is projected to expand at a 13.78% CAGR through 2031.

- By connectivity technology, Wi-Fi held 43.35% of the Germany smart home market share in 2025, while Broadband PLC is expected to grow at an 17.1% CAGR to 2031.

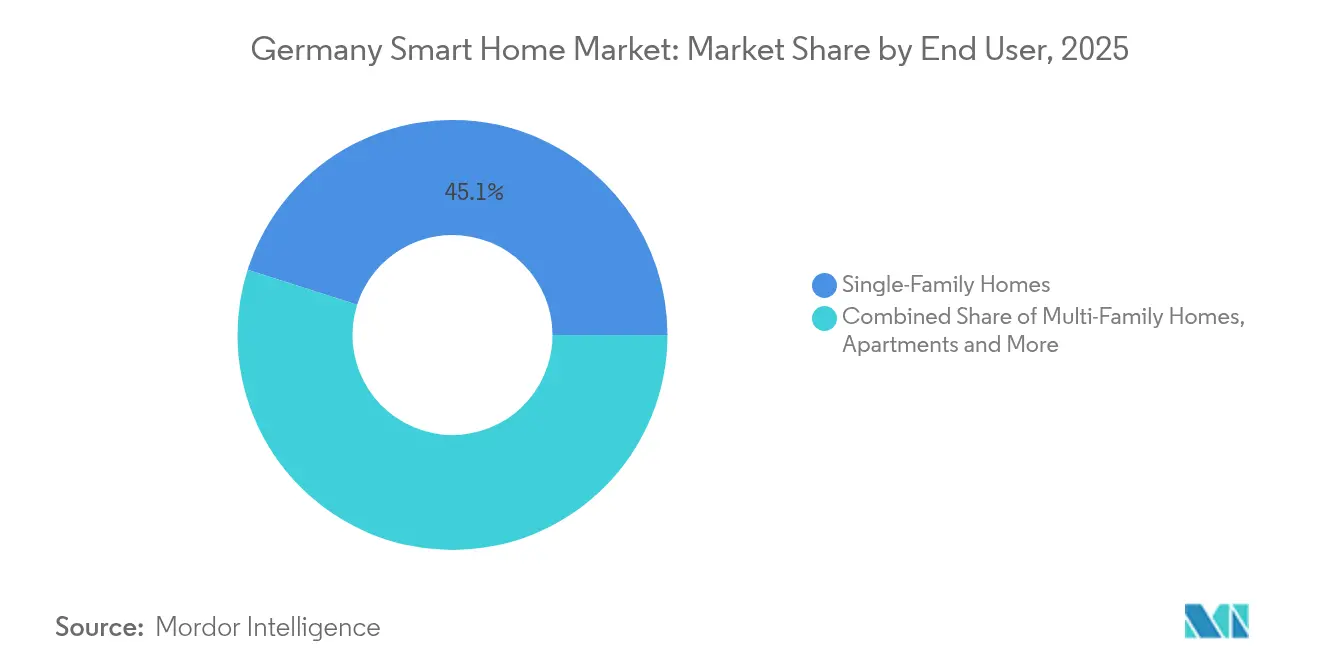

- By end user, single-family homes accounted for 45.10% of the Germany smart home market size in 2025; apartments post the fastest growth at 13.2% CAGR through 2031.

- By sales channel, online retail commanded 57.65% share and is rising at a 18.2% CAGR to 2031.

- By geography, Western Germany captured 32.10% revenue share in 2025, and Eastern Germany is projected to advance at 11.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for energy-efficient upgrades | +1.8% | Nationwide, strongest where renovation activity is high | Medium term (2–4 years) |

| Growing consumer focus on energy savings | +1.5% | Country-wide, led by high-income western states | Long term (≥4 years) |

| Near-universal smartphone and broadband access | +1.2% | All regions, with urban centers in the lead | Short term (≤2 years) |

| Federal “Building Renovation Wave” incentives | +2.1% | Nationwide, sharpest uptick in Eastern Germany | Medium term (2–4 years) |

| Insurance discounts tied to smart security devices | +0.8% | Premium markets such as Bavaria and Baden-Württemberg | Long term (≥4 years) |

| Dynamic utility pricing that rewards demand response | +1.4% | Rolling out nationally; early benefits in smart-meter zones | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Government subsidies for energy-efficient homes drive market acceleration

Germany’s KfW and BAFA programs cut the upfront cost of energy-management gear and reward smart-ready renovations with grants of up to EUR 15,000. The 2024 Building Energy Act amendments require smart-ready wiring in new builds and accelerate smart-meter deployment, which jumped from 272,024 units in 2022 to more than 1 million by September 2024. Multi-family developers tap these subsidies to bundle thermostats and energy monitors, achieving the 20–30% efficiency gains that secure maximum funding. Subsidy uptake is strongest in renovation-intensive regions where housing stock dates from before 1990, reinforcing the Germany smart home market growth.[1]Bundesnetzagentur, “Smart Meter Rollout Accelerates in Germany,” bundesnetzagentur.de

Rising consumer awareness of energy savings transforms purchase decisions

Higher carbon levies lifted the cost of household energy, making connected thermostats and smart heat-pump controllers financially compelling. Surveys show that 42% of 2025 device purchases target energy efficiency, up from 28% in 2022. In western states, households invest EUR 3,000–5,000 each year in integrated solutions that link rooftop solar, battery storage, and adaptive heating. These patterns heighten demand for analytics-driven platforms that quantify real-time savings and align with consumers’ sustainability goals.

High smartphone & broadband penetration enables seamless integration

Smartphone penetration stands at 95% and fiber now passes 10 million homes, removing access barriers for cloud-linked devices. Deutsche Telekom added 472,000 fiber customers and 311,000 IPTV subscribers in 2024, offering seamless onboarding for Matter-compliant gear. Urban households exhibit 78% smart-home adoption compared with 45% in rural districts, yet the gap narrows as fiber builds extend to smaller towns and 5G fixed wireless picks up the slack.

Building Renovation Wave incentives accelerate smart integration

The EUR 2.5 billion federal program ties insulation funding to installation of smart-ready systems, spurring developers to specify automation packages in retrofit projects. Eastern Germany sees the largest boost because 60% of its housing stock requires modernization. Demonstration projects such as Future Living Berlin show that modular construction plus pre-installed controls lower per-square-meter costs by 40% while meeting subsidy criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation & retrofit costs | -2.3% | Nationwide; renters and Eastern Germany feel it most | Medium term (2–4 years) |

| Data-privacy & cybersecurity worries | -1.7% | Country-wide, strongest where privacy concerns run high | Long term (≥4 years) |

| Interoperability & standards fragmentation | -1.2% | Across Germany, hitting premium buyers and early adopters | Short term (≤2 years) |

| Shortage of skilled installers & technicians | -2.8% | Nationwide, acute in Eastern provinces and rural districts | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High installation & retrofit costs constrain mass-market adoption

A full-featured system costs EUR 8,000–12,000 to install, and older buildings often need EUR 3,000–5,000 in wiring upgrades before devices go in. With 54% of households renting, split-incentive problems persist: landlords pay for hardware while tenants reap lower bills. Starter kits priced under EUR 500 from brands such as Homematic IP soften the barrier, yet the Germany smart home market still relies on financing and subsidy schemes to broaden reach.

Installer/technician talent shortage creates a market bottleneck

Electrical trade vacancies reached 96,580 in early 2024 and continue to rise, pinching project timelines and inflating labor rates. Photovoltaic installers compete for the same electricians, so smart-home providers pivot to DIY modules and remote-support programs that empower general contractors. Regional pay gaps send skilled labor from eastern states to southern factories, leaving rural districts underserved and slowing adoption in precisely those regions targeted for energy upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Security keeps the lead while energy management accelerates

Security platforms generated 26.65% of 2025 sales as insurers rewarded customers who deploy intrusion sensors and connected cameras. The segment bundles door-window contacts, motion detectors, and cloud video for subscription revenue streams that improve retention. Energy-management devices now register the fastest expansion at 13.78% CAGR through 2031, buoyed by dynamic utility tariffs that favor automated load shifting. Smart thermostats, heat-pump controllers, and PV inverters integrate through Matter, shrinking installation times and boosting interoperability. Growth dynamics vary across price tiers. Entry-level sensor packs dominate e-commerce, whereas premium villas specify whole-house lighting scenes and integrated audio. Smart appliances enter mainstream portfolios after BSH launched the first Matter-enabled refrigerator at CES 2025, signalling that white goods will become core nodes in the Germany smart home market.

By Connectivity Technology: Wi-Fi dominates as Broadband PLC surges

Household routers make Wi-Fi the default, underpinning 43.35% of device links. PLC technology rides on power lines, so utilities adopt it for demand-response pilots that precede the 2025 dynamic-pricing mandate. With an 17.1% CAGR, PLC meets edge-meter latency requirements without new wiring, supporting the Germany smart home market size allocated to energy dashboards. Thread and Zigbee scale through Matter as vendors migrate from proprietary hubs. Deutsche Telekom embeds smart-home control in standard routers, fostering hub-less set-ups that simplify ownership. Bluetooth and sub-GHz RF fill niche roles such as locks and water leakage alarms where low power or long battery life matters. Z-Wave persists in custom-integrator circles but shows limited new-device momentum because license fees raise bill-of-materials cost.

By End User: Single-family homes still dominate yet apartments accelerate

Ownership autonomy keeps single-family dwellings at a 45.10% revenue stake in 2025. Yard sensors, garage openers, and garden irrigation add peripheral sales unknown in flats. Still, apartment complexes grow at 13.2% CAGR as urbanization lifts multi-family construction. Developers install central gateways that aggregate metering, lighting, and access control for operational savings and green-building certifications. Growing rental demand lets landlords command premium rents on smart-equipped units, offsetting hardware expenses. Luxury villas remain a small but lucrative niche: high-net-worth owners spend EUR 25,000-50,000 per build for bespoke scenes and voice-driven controls, helping integrators maintain double-digit margins despite rising component costs.

By Sales Channel: Online retail dominates amid installer shortage

E-commerce captures 57.65% of 2025 turnover and grows 18.2% per year as skilled-labor deficits push consumers toward self-installation. Marketplaces bundle how-to videos and optional onsite services booked at checkout, closing the last-mile gap. Brick-and-mortar DIY chains adapt through kiosks that demo connected devices and schedule partner electricians for larger jobs. Specialist integrators retain premium customers and commercial projects but face escalating wage bills that compress profitability. Brands such as Homematic IP cultivate 2,800 installation partners and maintain direct-to-consumer storefronts, executing an omnichannel play that balances reach with quality control. Regional disparities persist: southern states rely on store-based consultation, whereas the East leans heavily on digital ordering because of thinner installer density.

Geography Analysis

Western Germany held 32.10% of 2025 turnover owing to higher disposable income and entrenched technology adoption. Bavaria and Baden-Württemberg contribute strong luxury-system sales, often exceeding EUR 40,000 per project. North Rhine-Westphalia benefits from a dense population and industrial automation spillovers that validate connected-device reliability. CAGR in the West hovers at 8-9%, reflecting market maturity and replacement cycles for early adopters.

Eastern Germany is the fastest-growing territory at 11.3% CAGR. Federal and EU renovation funds unlock investments in aging housing stock built before unification. Installation costs trend 15% lower than in the South because labor rates are modest, encouraging comprehensive upgrades during refurbishment. Yet installer scarcity limits throughput, so developers increasingly choose modular pre-wired wall panels that slash onsite fit-out times.

Northern Germany exploits renewable-energy synergies. Households connect smart meters to offshore-wind feeds and district heating grids, optimizing load based on real-time tariffs. Hamburg’s smart-city projects incubate residential pilots; rural Schleswig-Holstein farms repurpose LoRaWAN sensors from agriculture for water-leak detection in farmhouses. Fiber penetration in port cities exceeds 85%, powering 4K security and AI surveillance regimes.

Southern Germany represents the premium tier. Automotive suppliers parlay embedded-electronics prowess into residential comfort and security lines. Bosch’s Energy and Building Technology division booked EUR 7.5 billion revenue in 2024, despite a 3% dip amid supply-chain constraints, and funnels R&D from vehicle electronics to home energy controllers. Siemens invests EUR 750 million in Berlin’s Siemensstadt Square, using live apartments as testbeds for AI energy analytics before rolling them out nationwide.

Competitive Landscape

Competition intensifies as domestic engineering heavyweights confront digital-platform giants. Bosch, Siemens, and BSH remain influential through deep local manufacturing and compliance knowledge, yet they now face Amazon, Google, and Samsung, which bundle hardware with cloud AI at consumer-friendly price points. First-mover advantage accrues to BSH for commercializing Matter in refrigerators in 2025; the launch encourages appliance peers to shift roadmaps toward protocol conformity.

Strategic alliances redefine boundaries. ABB links its InSite platform to Samsung SmartThings for unified energy dashboards. Siemens leverages 17.3% profit margins in its Smart Infrastructure division to cross-fund residential software that scales down from commercial building management. tado° partners with Panasonic to harmonize heat-pump and thermostat algorithms, cutting installation complexity for HVAC contractors.

Start-ups fight on integration simplicity and sustainability branding. 1KOMMA5° raised EUR 150 million to bundle rooftop PV, battery storage, and smart-home gateways. Eve Systems markets privacy-first accessories that avoid mandatory cloud log-ins, targeting consumers wary of data harvesting. Local service firms such as SchlauesHaus offer remote design and on-call engineering to mitigate electrician shortages, widening the funnel for mainstream adoption in the Germany smart home market.

Germany Smart Home Industry Leaders

Schnieder Electric

Honeywell International Inc.

Siemens AG

Google LLC (Alphabet Inc.)

Robert Bosch Smart Home GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: EWE AG pledged EUR 1.3 billion for fiber and EV-charging expansion, enhancing connectivity for northern households.

- March 2025: Deutsche Telekom presented an AI-enabled smartphone with embedded smart-home control on its Magenta AI platform.

- February 2025: ABB integrated its InSite energy-management suite with Samsung SmartThings for real-time consumption analytics.

- February 2025: Amazon introduced Alexa+ at USD 19.99 per month, adding generative-AI scene recommendations for German users.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany smart home market as total revenue from connected devices that let residents monitor, control, and automate lighting, heating, energy management, security, entertainment, and major domestic appliances in single- and multi-family dwellings. Our team counts hardware sales at retail prices and the embedded control software that ships with each unit.

Scope exclusion: commercial building automation in offices, hotels, or factories is not included.

Segmentation Overview

- By Product

- Comfort and Lighting

- Control and Connectivity

- Energy Management

- Home Entertainment

- Security

- Smart Appliances

- By Connectivity Technology

- Wi-Fi

- Bluetooth and RF

- Zigbee

- Z-Wave

- Broadband PLC

- Other Protocols

- By End User

- Single-Family Homes

- Multi-Family Homes

- Apartments

- Luxury Villas

- By Sales Channel

- Online Retail

- Organised Retail Chains

- Specialty Stores

- Direct Installer Network

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed installers, device makers, power utilities, insurers, and leading e-retailers across Bavaria, North Rhine-Westphalia, and Berlin. They then validated early assumptions through an online survey of urban homeowners and tenants to fine-tune penetration ratios and average selling prices.

Desk Research

We began with public data from the Federal Statistical Office, the Federal Network Agency, Eurostat, and the European Commission that quantify dwelling stock, broadband access, and energy targets. Trade bodies such as Bitkom and ZVEI supplied adoption surveys and shipment indices, while UN Comtrade imports, Questel patent counts, and company filings anchored supply trends. Paid libraries that Mordor analysts subscribe to, including D&B Hoovers and Dow Jones Factiva, rounded out vendor financials and channel performance. This list is illustrative; many additional open and subscription sources supported every cross-check and clarification.

Market-Sizing & Forecasting

A top-down model converts occupied dwellings with broadband into an addressable base, applies product-level penetration curves and weighted device prices, and then reconciles totals with selective bottom-up supplier roll-ups. Key variables include new housing completions, KfW retrofit incentive uptake, smart speaker attachment rates, burglary incidence, and Wi-Fi household coverage. Forecasts use multivariate regression plus scenario analysis to reflect energy-price policy shifts. Any variance in bottom-up checks is adjusted only after two independent confirmations.

Data Validation & Update Cycle

Outputs pass automated anomaly scans, senior peer review, and research-manager sign-off. We refresh annually and trigger interim updates when subsidy rules, taxation, or macro shocks materially alter demand. A final sense-check precedes each release so clients receive the latest view.

Why Mordor's Germany Smart Home Baseline Deserves Trust

Published estimates often diverge because firms choose different device baskets, mix wholesale with retail revenue, or lock exchange rates at separate points in time. We flag these factors upfront so buyers see exactly what is being measured.

Key gap drivers include scopes that drop DIY kits, the blending of small commercial installs, single price assumptions across channels, and slower refresh cycles that miss subsidy revisions. Our yearly cadence, residential-only scope, and double-sourced ASPs keep the baseline grounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.86 B (2025) | Mordor Intelligence | - |

| USD 4.67 B (2023) | Global Consultancy A | Excludes streaming devices and holds 2023 FX rates |

| USD 6.58 B (2024) | Regional Consultancy B | Mixes small commercial installs; single ASP used |

| USD 7.80 B (2024) | Trade Journal C | Relies on vendor press releases without shipment checks |

Taken together, once scope, device breadth, and update cadence are normalized, Mordor's balanced approach provides the most dependable starting point for strategic and investment decisions.

Key Questions Answered in the Report

What is the current size of the Germany smart home market?

The Germany smart home market is valued at USD 8.54 billion in 2026.

How fast will the market grow through 2031?

Revenue is projected to rise to USD 12.91 billion by 2031, reflecting a 8.62% CAGR.

Which product segment is expanding the quickest?

Energy-management devices exhibit the fastest momentum at a 13.78% CAGR, driven by tariff reforms and subsidy support.

Why is installer availability a constraint?

Vacancies in the electrical trades exceed 96,000 positions, slowing professional installation and pushing consumers toward DIY options.

How important is the Matter protocol for future growth?

Matter boosts interoperability, shortens installation time, and reduces hub requirements, accelerating mainstream adoption across all buyer groups.

Page last updated on: