Spain Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

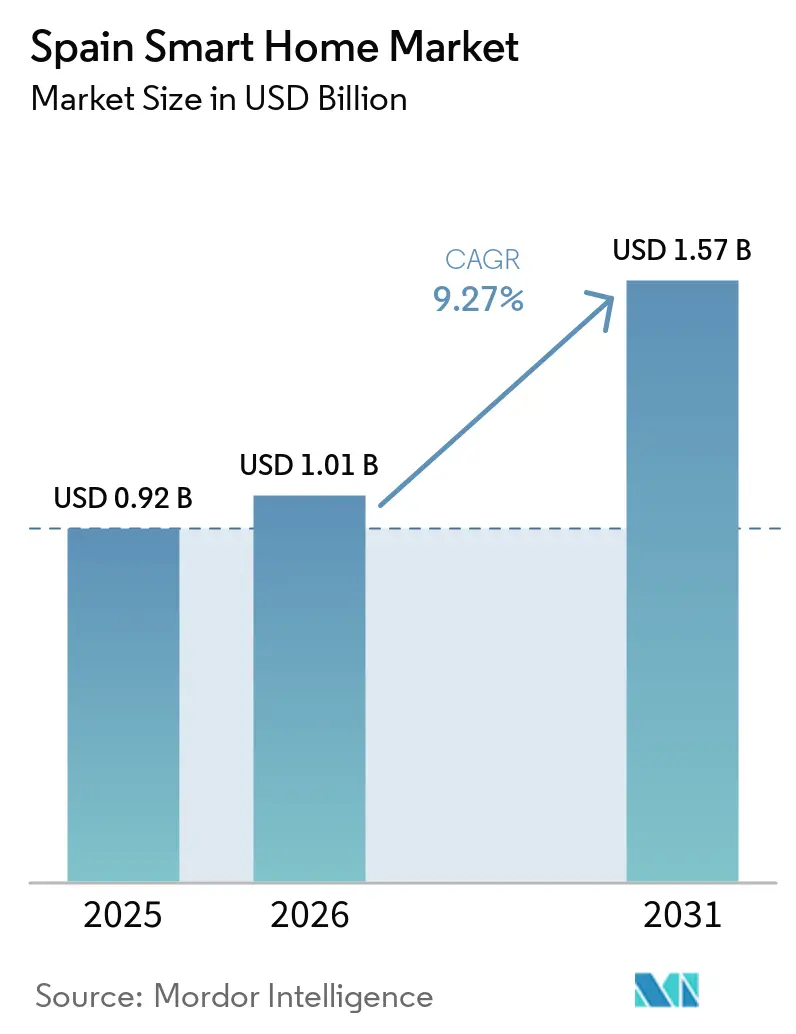

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 9.27% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Smart Home Market Analysis by Mordor Intelligence

Spain smart home market size in 2026 is estimated at USD 1.01 billion, growing from 2025 value of USD 0.92 billion with 2031 projections showing USD 1.57 billion, growing at 9.27% CAGR over 2026-2031. Growth ties closely to government retrofit incentives, near-universal fiber-to-the-home coverage, and Mediterranean climate considerations that keep energy management at the fore.[1]Instituto para la Diversificación y Ahorro de la Energía, “Programa PREE 5000,” idae.es Spain’s demographic pivot toward single-person households and a rising share of residents aged 65 years and older is accelerating demand for safety monitoring, voice-controlled automation, and health-tracking devices.[2]Fundación General CSIC, “Informe Entornos inteligentes envejecimiento activo y saludable,” fgcsic.es Time-of-use electricity tariffs, adopted by one-third of households, encourage load-shifting behavior that cuts annual bills by 8-11% and positions connected appliances as practical cost-saving tools.[3]Clean Energy Wire, “What are dynamic electricity tariffs and why are they…,” cleanenergywire.org Rapid cloud infrastructure investments in Aragon and Zaragoza enhance domestic data-processing capacity and reduce latency for AI-driven services, reinforcing the Spain smart home market’s competitive edge.

Key Report Takeaways

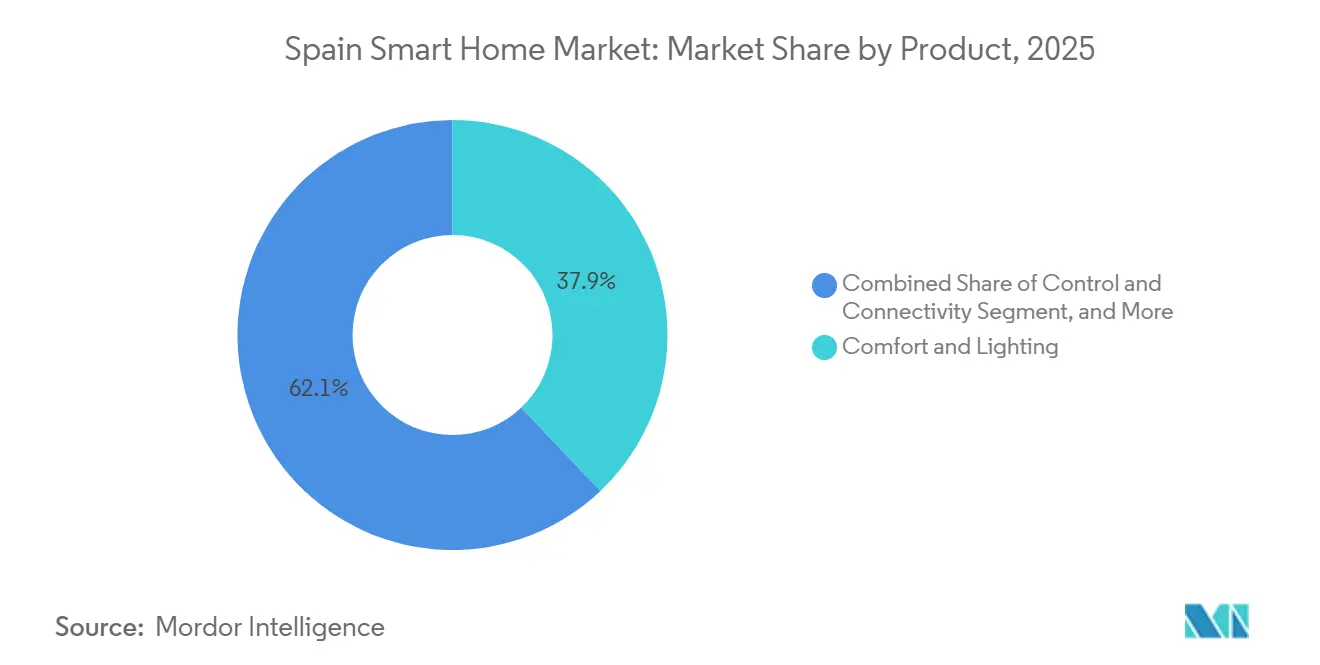

- By product, Comfort and Lighting solutions led with 37.92% of Spain smart home market share in 2025, while Smart Appliances are projected to grow at 10.18% CAGR through 2031.

- By connectivity, Wi-Fi devices held 45.88% revenue share in 2025; Thread/Matter solutions exhibit the fastest pace at 11.62% CAGR to 2031.

- By installation type, Retrofit projects accounted for 54.62% of Spain smart home market size in 2025, whereas New Construction installations are forecast to expand at 10.34% CAGR between 2026 and 2031.

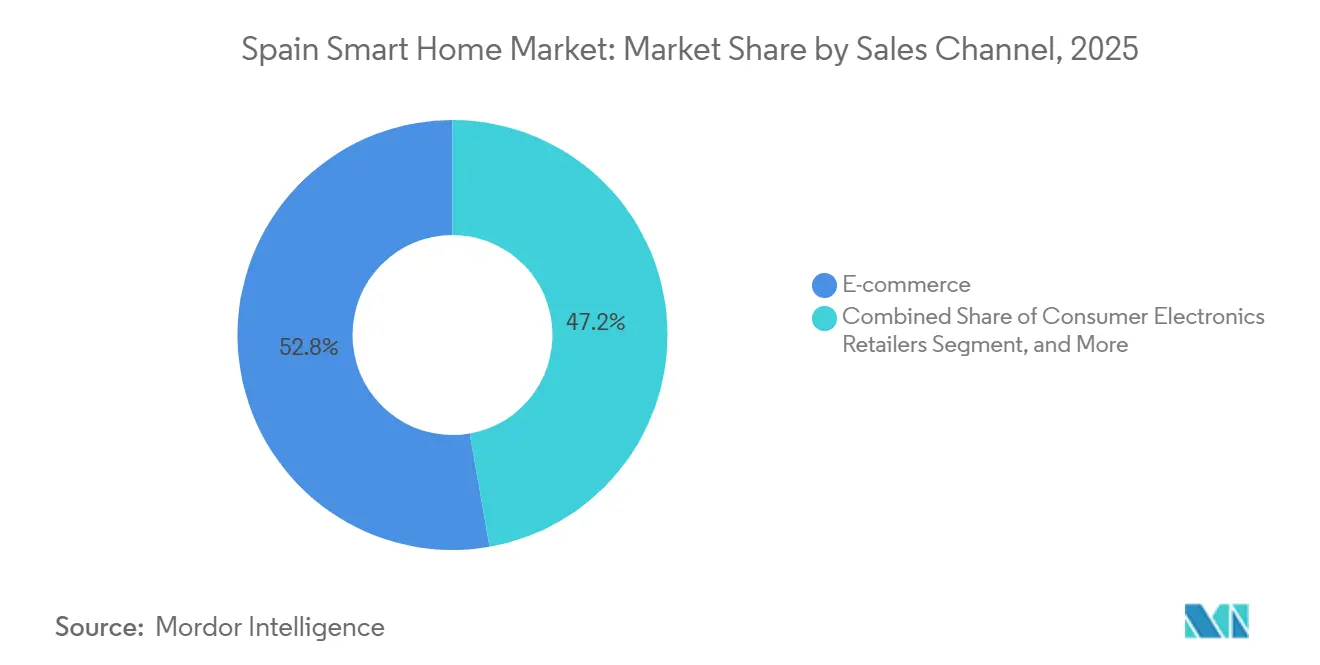

- By sales channel, E-commerce dominated with 52.76% share in 2025; Professional Installers/Integrators are advancing at an 11.14% CAGR to 2031.

- By End-user Profile, single-family houses captured 65.12% market share in 2025, while multi-dwelling units are set to post the fastest regional CAGR of 10.98% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed energy-efficiency subsidies | +2.1% | National, strongest in municipalities <5,000 residents | Medium term (2-4 years) |

| Rapid FTTH and 5G rollout | +1.8% | National, early uptake in Madrid, Barcelona, Valencia | Short term (≤2 years) |

| Growth in single-person and elderly households | +1.4% | Urban centers and coastal regions | Long term (≥4 years) |

| Matter-enabled interoperability | +1.2% | Tech-forward Spanish cities | Medium term (2-4 years) |

| Time-of-use electricity pricing adoption | +1.0% | National | Medium term (2-4 years) |

| Surging renewable-energy integration | +0.9% | National, highest in southern regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government-backed Energy-efficiency Subsidies for Residential Retrofits

Incentives such as the PREE 5000 program and income-tax deductions covering up to 60% of qualifying costs narrow payback periods for connected energy-management systems, converting latent interest into active demand. The ERESEE 2030 target of 1.2 million dwelling upgrades ensures a persistent pipeline, while staged renovation roadmaps common in Spanish households translate into recurring opportunities for device add-ons.

Rapid FTTH and 5G Rollout Boosting Device Reliability

With 93% population coverage in fiber, Spain leads Europe in very-high-capacity network reach, delivering low-latency performance critical for cloud-dependent voice assistants and security cameras. Digital Spain 2026 allocates additional 5G funding to rural provinces, enabling Spain smart home market growth beyond metropolitan hubs.[4] Restraint (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline Persistent data-privacy scepticism -1.6% National, most acute among rural and older consumers Long term (≥4 years) High upfront device costs -1.3% National, heavier outside Madrid and Barcelona Medium term (2-4 years) Limited installer availability in smaller cities -0.9% Interior regions Short term (≤2 years) Competing ecosystems raising choice paralysis -0.8% National Medium term (2-4 years)

Growth in single-person and elderly households

Household structures are shifting toward single occupancy and senior residency, stimulating demand for unobtrusive fall-detection sensors, voice-first interfaces, and telemedicine integrations that extend independent living. PropTech developers in Madrid increasingly market turnkey smart apartments tailored to these demographics, weaving in basic automation as standard fixtures.

Matter-enabled interoperability

Matter’s IPv6 core lets Spanish shoppers combine products from Schneider Electric, Google, and local brands under one app, stripping away the complexity that previously discouraged multi-device setups. Local test labs certified by UL Solutions reinforce buyer confidence that devices will interwork flawlessly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-privacy scepticism | -1.6% | National, most acute among rural and older consumers | Long term (≥4 years) |

| High upfront device costs | -1.3% | National, heavier outside Madrid and Barcelona | Medium term (2-4 years) |

| Limited installer availability in smaller cities | -0.9% | Interior regions | Short term (≤2 years) |

| Competing ecosystems raising choice paralysis | -0.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data-privacy Scepticism Among Spanish Consumers

Despite GDPR safeguards, 30% of Spanish Internet users report technical concerns when interacting with connected services, reinforcing caution toward always-listening devices Eurostat. Manufacturers pursuing the Spain smart home market must offer transparent data handling and local processing options to ease trust barriers.

High Upfront Device Costs vs Average Household Income

Household installations exceeding EUR 2,000 remain aspirational for many families outside the wealthiest provinces, with GDP per capita at EUR 28,300 in 2022 limiting discretionary spend. Financing plans and modular, app-driven platforms are slowly addressing affordability but price sensitivity continues to temper premium feature uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Comfort and Lighting Dominance Drives Adoption

Comfort and Lighting solutions contributed 37.92% of Spain smart home market share in 2025, reflecting widespread acceptance of smart LEDs, thermostats, and shading controls that align with daily lifestyle patterns. Smart Appliances hold the strongest upside, expanding at 10.18% CAGR as energy-label rules tighten and dynamic tariffs reward intelligent scheduling. Home Entertainment adoption rides on ubiquitous broadband, though growth moderates with saturation in larger cities. Security systems sustain steady uptake, especially in holiday rentals seeking remote monitoring assurance. Integrated Energy Management platforms link rooftop PV, heat pumps, and household loads, positioning the Spain smart home market for grid-interactive services that complement the national solar boom. Spanish firms such as Fermax tailor intercom-linked lighting packages for multi-dwelling units, underscoring local design preferences shaped by Mediterranean building traditions.

Innovations in appliance-embedded Wi-Fi chips and cost-effective single-board controllers expand entry-level options, lowering barriers for first-time buyers. Voice assistant tie-ins with refrigerators and washing machines amplify convenience, while regulator-mandated eco-modes foster adoption among cost-sensitive households. The Spain smart home market size for appliances could represent a fifth of all connected-device revenue by 2030 if EU eco-design proposals progress, introducing time-of-use optimization as a default feature. Insurance firms piloting premium discounts for leak-sensing dishwashers illustrate new monetization pathways. Manufacturers that integrate over-the-air updates and Matter compliance from launch are best placed to capture cross-brand households seeking future-proof investments.

By Connectivity Technology: Thread/Matter Protocols Accelerate Interoperability

Wi-Fi remains the backbone, hosting 45.88% of installed nodes in 2025, yet Thread/Matter-ready chip shipments are posting 11.62% CAGR as brands race to offer frictionless pairing and lower standby power. Bluetooth Low Energy underpins wearables and portable sensors, while Zigbee and Z-Wave sustain modest use in legacy hubs. The Spain smart home market values devices capable of switching intelligently between protocols, hence chipset makers bundle Wi-Fi, BLE, and 802.15.4 radios on a single die. Edge-AI processors that run local intent recognition reduce cloud traffic, answering privacy worries. Telecom providers bundle multi-protocol routers with new fiber contracts, cementing their gatekeeper role and nudging households toward unified ecosystems.

Matter’s gradual reach into appliances, HVAC, and security cameras simplifies purchase decisions and cuts return rates at retail. Retailers report drop-in support calls once customers migrate to single-app environments. Furthermore, utility-managed demand-response pilots exploit Thread border routers embedded in smart speakers to deliver rapid load-shed signals without extra hardware. The Spain smart home market continues to reward vendors that maintain over-the-air upgradability, positioning products for regulatory changes around cybersecurity labeling proposed by the EU.

By Installation Type: New Construction Gains Momentum

Retrofit projects represented 54.62% of Spain smart home market size in 2025, driven by national renovation incentives. New Construction installations, however, are growing faster at 10.34% CAGR as property developers pre-wire networks and market energy-smart apartments to young professionals. Municipal building codes in Madrid and Catalonia increasingly prescribe ducting and junction boxes for sensors at the shell stage, reducing incremental costs. PropTech platforms bundle white-label resident apps that provide door access, maintenance tickets, and metering dashboards.

The Spain smart home market benefits when developers negotiate volume discounts with equipment makers, trimming per-unit hardware cost by up to 25%. Shared-services models in apartment blocks, such as solar-plus-storage communal rooftops, multiply returns on energy systems. Retrofit growth remains resilient in Spain’s ageing housing stock, yet reliance on professional installers triggers bottlenecks in secondary cities. Expanding vocational training for electricians is thus pivotal to sustaining retrofit momentum.

By Sales Channel: Professional Installers Emerge as Growth Leaders

E-commerce held a 52.76% share in 2025, reflecting strong online retail culture and price transparency. Professional Installers/Integrators, however, log the fastest rise at 11.14% CAGR, handling multi-zone HVAC, PV coupling, and building-wide access control for both single-family homes and multi-dwelling units. Installer demand is strongest among elderly homeowners prioritizing reliability and after-sales support, turning advisory services into a revenue differentiator.

Major energy utilities now partner with certified installers to market subscription bundles that include hardware, monitoring, and maintenance. Consumer electronics chains complement their traditional retail model with in-home setup services. Peer-review platforms help buyers vet technicians, easing trust barriers that historically slowed uptake in smaller towns. The Spain smart home market observes that brands negotiating exclusive installer affiliations can embed their ecosystems deeper into renovations, limiting competitor entry at household level.

By End-user Profile: Single-family Houses Dominate, MDUs Accelerate

Single-family Houses accounted for 65.12% of 2025 revenue, reflecting Spain’s enduring detached-home culture in suburban belts around Madrid, Barcelona and Seville. Detached dwellings allow owners to dictate retrofit schedules, install rooftop solar, and add high-amp circuits for EV chargers without association votes. Ample roof area aligns with battery storage and HVAC zoning, raising average order values.

Multi-dwelling Units, however, represent the fastest-growing cohort at 10.98% CAGR through 2031. Shared infrastructure discounts installation costs, and centralised building management systems handle lift maintenance, gate access and community solar allocation with one software stack. Developers increasingly brand MDUs as “smart-ready,” marketing mobile apps that integrate door entry, parcel lockers and fault reporting. Residents appreciate lower per-unit energy bills when whole-building demand management shifts loads outside PVPC peak windows. These economic and convenience levers underpin robust segment expansion.

Geography Analysis

Madrid and Centre retained major regional revenue, helped by higher disposable incomes, flagship developer projects and near-universal gigabit connectivity. Tourist accommodation operators embraced self-check-in locks and thermostat automation, aiming to curb energy waste between guest stays. Pilot smart-grid initiatives funded by Digital Spain 2026 provide a showcase for bidirectional EV-to-home schemes, anchoring first-mover advantage.

Valencia and Murcia deliver the sharpest growth trajectory in the country, underpinned by industrial diversification, sunny climate and burgeoning solar-panel supply chains. EU rural broadband subsidies stitch fibre lines into hinterland towns, unlocking new markets. Rooftop solar’s popularity dovetails with battery-ready hybrid inverters that integrate seamlessly into Matter ecosystems, enabling appliance-level dispatch.

Catalonia’s Barcelona-centred base remains solid yet maturing; upgrades shift from initial smart-speaker installs to deeper integrations such as sub-metering and predictive maintenance. Andalusia deploys EU structural funds on city-scale energy-efficiency retrofits, bundling thermostat and shading controls for its hot summers. Basque Country and Navarre leverage industrial incomes to adopt premium automation, including integrated AV-lighting scenes in architectural restorations. Galicia plus the Balearic and Canary archipelagos focus on hospitality applications that protect vacant holiday homes while trimming utility spend during variable occupancy cycles.

Competitive Landscape

The Spain smart home ecosystem is moderately fragmented. Traditional automation brands—Schneider Electric, ABB and Siemens-tap professional-installer relationships to position energy-management gateways and distribution-board mounted controllers, posting mid-single-digit growth in 2024. Global platform giants-Google, Amazon and Apple-dominate consumer mindshare via voice-assistant ecosystems, pushing recurring software-service revenues. Matter forces proprietary stacks to interoperate, nudging hardware makers toward differentiation via machine-learning algorithms that refine comfort-versus-savings trade-offs.

Start-ups backed by regional accelerators concentrate on AI-driven demand response, smart-meter analytics and PropTech orchestration, offering utilities and developers white-label solutions. Iberdrola extends beyond commodity supply into connected-home bundles delivered through its smart-meter roll-out and mobile app. Mid-tier Asian entrants challenge incumbents on price, yet strict data-protection laws give domestic or EU-based providers a compliance edge. Vendors blending on-device AI, transparent privacy policies and solar-aware load control remain best positioned for long-term relevance under Spain’s dynamic-tariff regime.

Spain Smart Home Industry Leaders

-

Schneider Electric SE

-

ABB Ltd

-

Siemens AG

-

Signify Holding

-

Google Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Amazon Web Services pledged EUR 17.5 billion for cloud campuses in Aragón, adding 6,800 jobs and reinforcing Spain’s AI compute backbone.

- February 2025: Microsoft confirmed EUR 7.16 billion data-centre investment near Zaragoza, boosting edge-compute capacity for latency-sensitive home-security feeds.

- January 2025: EU Code of Conduct for Energy Smart Appliances launched with Arçelik, Daikin and Electrolux committing to interoperable, energy-responsive devices.

- December 2024: Spain’s rooftop solar installs dipped 17% following expiration of EU recovery funds, shifting focus to utility-scale assets and self-consumption optimisation

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spain smart home market as the total annual value of connected devices and control hubs installed within Spanish residences that enable occupants to monitor or automate lighting, climate, security, entertainment, and energy-management functions through IP-based communication. The estimate covers hardware sales, embedded firmware, and first-purchase application licenses delivered through retail, e-commerce, utilities, and professional-installer channels.

Scope exclusion: wearables, on-premise service fees, and stand-alone consumer electronics that lack remote connectivity lie outside this assessment.

Segmentation Overview

-

By Product

- Comfort and Lighting

- Control and Connectivity

- Energy Management

- Home Entertainment

- Security

- Smart Appliances

-

By Connectivity Technology

- Wi-Fi

- Bluetooth

- Zigbee

- Z-Wave

- Thread/Matter-ready ICs

-

By Installation Type

- New Construction

- Retrofit/Existing Homes

-

By Sales Channel

- E-commerce

- Consumer Electronics Retailers

- Electrical Wholesalers

- Professional Installers/Integrators

-

By End-user Profile

- Single-family Houses

- Multi-dwelling Units (MDUs)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with Spanish installers, energy retailers, IoT chipset vendors, and property developers across Madrid, Barcelona, Valencia, and Seville. These conversations clarified real-world installation rates, average selling prices, and the impact of subsidies like PREE 5000, which we then reconciled with survey feedback from early adopters and senior citizens considering aging-in-place solutions.

Desk Research

We initiated desk work by gathering baseline data from tier-one sources such as Spain's National Statistics Institute for dwelling stock and broadband penetration, Red Eléctrica de España for household electricity tariffs, and Eurostat's smart meter rollout files. Trade-group portals, including AFME for electrical equipment shipments and Domotys for home-automation installers, helped us trace domestic supply.

Next, our team mined company 10-Ks, investor decks, and respected media archives on Dow Jones Factiva to benchmark unit prices and channel splits. Select paid databases (D&B Hoovers for financials and Questel for recent Matter-related patents) completed the landscape. This list is illustrative; many additional open and subscription sources were checked for cross-validation.

Market-Sizing & Forecasting

A top-down build started with occupied-dwelling counts, FTTH plus 5G household coverage, and smart-device penetration tiers. Results were stress-tested through bottom-up snapshots that multiplied sampled ASPs by shipment volumes from customs data and distributor checks. Key variables include retrofit subsidy uptake, average household size, Matter-enabled device share, residential electricity price swings, and e-commerce share of appliance sales; each is projected with multivariate regression and scenario analysis. Gaps in bottom-up inputs, notably on DIY kits, were bridged using weighted averages from installer interviews.

Data Validation & Update Cycle

Outputs pass three filters: automated variance screens, peer review by a second analyst, and management sign-off. Models refresh annually, yet we trigger mid-cycle updates if Spain revises energy-efficiency grants or if large vendors release material product lines. A short reconfirmation call precedes every client delivery to ensure figures remain current.

Why Mordor's Spain Smart Home Baseline Stands Reliable

Published estimates differ because firms pick dissimilar device baskets, pricing paths, and refresh timings.

By anchoring volume to Spain-specific housing and connectivity metrics that we update yearly, Mordor Intelligence minimizes such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.92 B (2025) | Mordor Intelligence | - |

| USD 1.23 B (2023) | Regional Consultancy A | broader product roster and older base year inflate value |

| USD 3.26 B (2023) | Global Consultancy B | counts subscription services and applies aggressive penetration curve |

These contrasts show that when scope, timing, and validation discipline align, our balanced baseline offers decision-makers a dependable footing for growth planning.

Key Questions Answered in the Report

What is the Spain smart home market’s current value and growth forecast?

The Spain smart home market is worth USD 1.01 billion in 2026 and is projected to reach USD 1.57 billion by 2031, tracking a 9.27% CAGR over 2026-2031

Which household type leads adoption?

Single-family Houses dominate with 65.12% revenue in 2025 thanks to easier retrofit flexibility and rooftop solar capacity.

Why are Multi-dwelling Units growing faster?

MDUs benefit from shared infrastructure, lower per-unit costs and developer-driven “smart-ready” branding, expanding at an 10.98% CAGR through 2031.

How do retrofit subsidies influence uptake?

Programs such as PREE 5000 and generous tax deductions reduce capital outlay by up to 40%, accelerating connected-device installation timelines.

What connectivity standards should buyers prioritise?

Matter-compliant devices running over Wi-Fi or Thread assure cross-brand compatibility and future-proof purchases against ecosystem changes.

Which regions are advancing most rapidly

Valencia and Murcia lead with a 9.96% projected CAGR, fuelled by solar adoption, industrial diversification and expanding fibre coverage.

Page last updated on: