Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

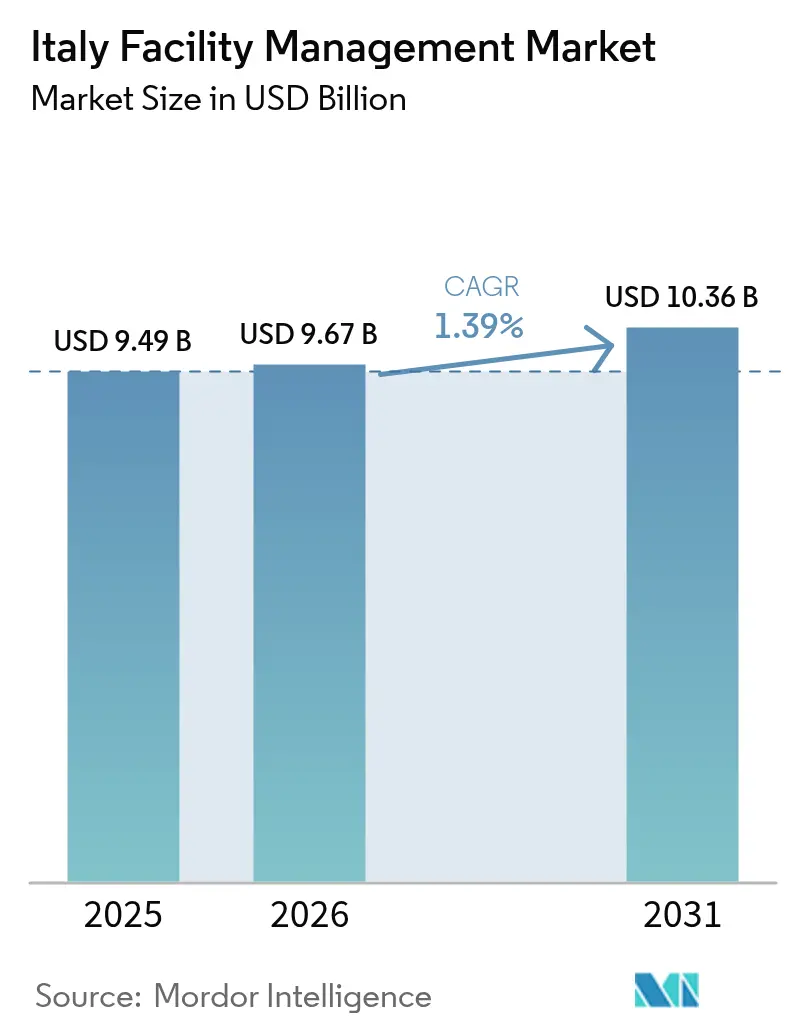

| Base Year Market Size (2025) | USD 9.49 Billion |

| Market Size (2026) | USD 9.67 Billion |

| Market Size (2031) | USD 10.36 Billion |

| Growth Rate (2026 - 2031) | 1.39% CAGR |

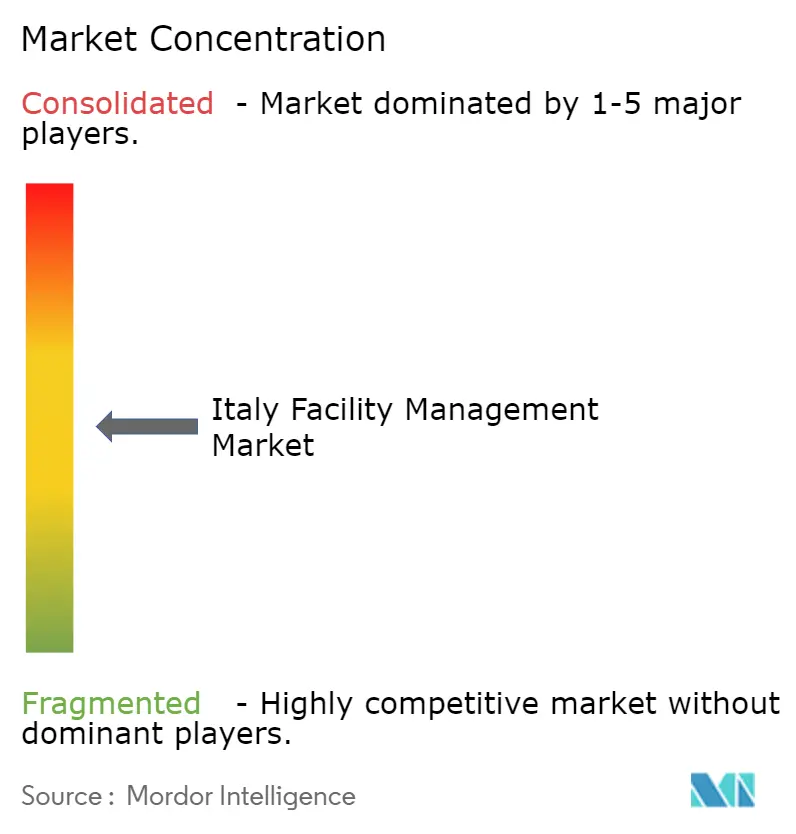

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Facility Management Market Analysis by Mordor Intelligence

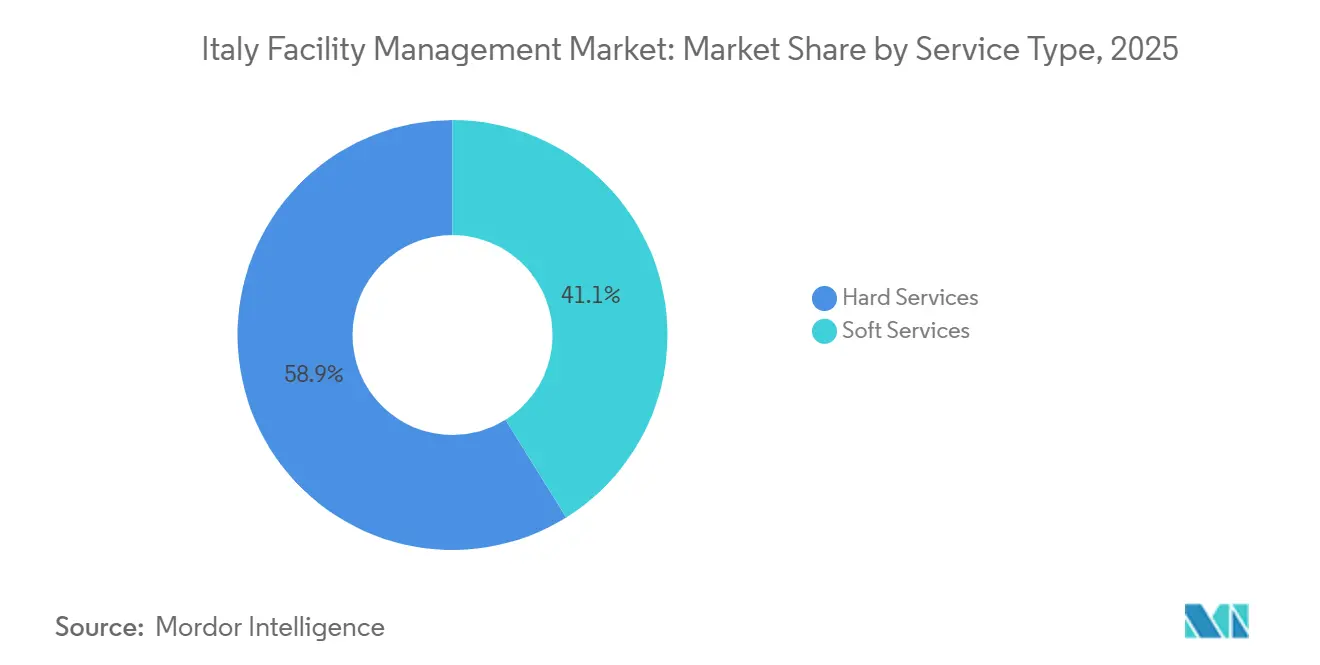

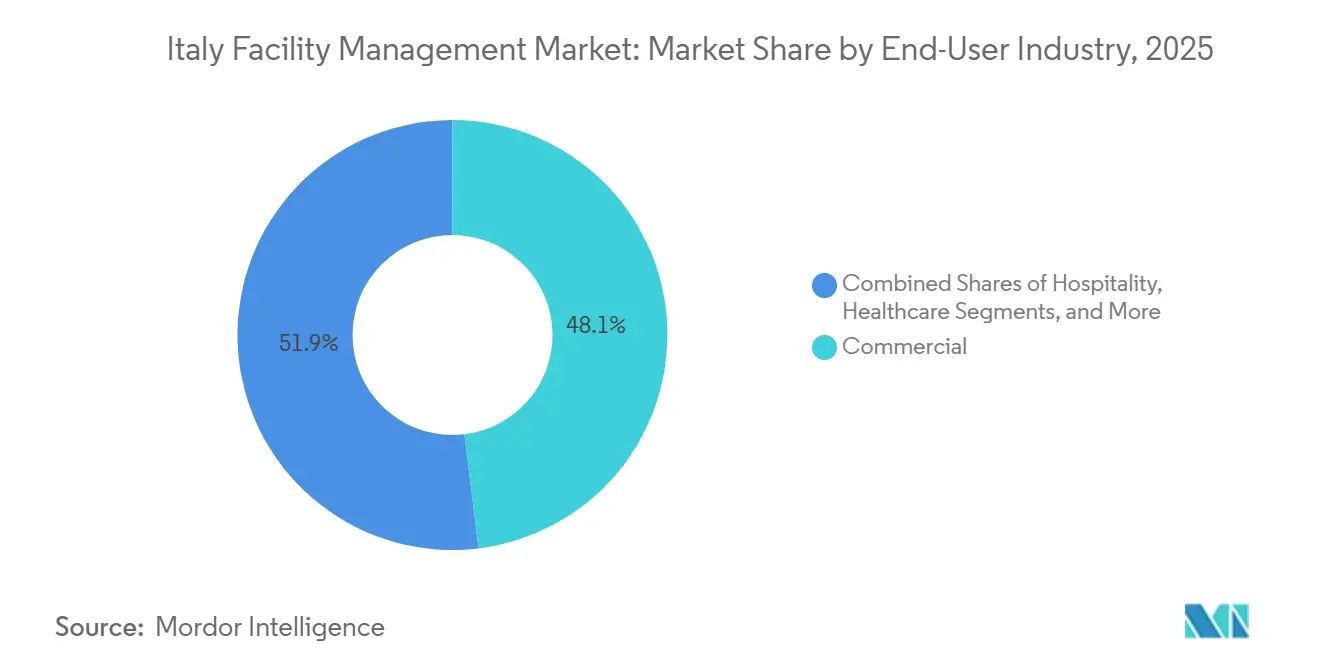

The Italy facility management market size is expected to increase from USD 9.49 billion in 2025 to USD 9.67 billion in 2026 and reach USD 10.36 billion by 2031, growing at a CAGR of 1.39% over 2026-2031. A gradual expansion reflects a mature sector that is balancing municipal budget tightening, a mosaic of regional regulations, and persistent shortages of certified technicians. Growth pockets are forming around mandatory catastrophe-insurance compliance, data-center construction in Lombardy, and a rebound in tourism that is fueling demand for soft services. Hard services retained 58.87% of 2025 revenue, yet soft services are expanding faster on the back of bundled public catering and hospitality contracts. Outsourced delivery models already hold two thirds of spend and are gaining ground as public agencies shed non-core activities and private landlords migrate to outcome-based integrated contracts.

Key Report Takeaways

- By service type, hard services led with 58.87% of Italy facility management market share in 2025, while soft services are advancing at a 1.96% CAGR through 2031.

- By offering type, outsourced models held 66.59% share of Italy facility management market size in 2025 and integrated facility management is registering a 1.51% CAGR over the same period.

- By end-user industry, commercial facilities accounted for 48.07% share of Italy facility management market size in 2025 and are projected to expand at a 1.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing Trend Among Public-Sector Entities Expanding FM Market | +0.4% | National, Concentration In Lazio, Lombardy, Emilia-Romagna | Medium Term (2–4 Years) |

| Growth Of Italy's Tourism And Hospitality Sector Boosting Demand For Soft FM Services | +0.5% | National, Peaks In Veneto, Lazio, Tuscany, Campania | Short Term (≤ 2 Years) |

| Increasing Adoption Of Integrated Facility Management Contracts For Cost Optimization | +0.3% | National, Led By Lombardy, Piedmont, Lazio | Medium Term (2–4 Years) |

| Expansion Of Data-Center Industry In Northern Italy Spurring Specialized Technical FM Demand | +0.2% | Lombardy, Piedmont, Veneto | Long Term (≥ 4 Years) |

| Mandatory Disaster-Insurance Law Driving Resilience-Oriented FM Spend | +0.2% | National, Early Gains In Seismic Zones Such As Emilia-Romagna And Marche | Short Term (≤ 2 Years) |

| ARERA-Led Energy Price Reform Incentivizing Building-Level Energy-Efficiency FM Services | +0.2% | Northern Italy And Spill-Over To Emilia-Romagna | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Outsourcing Trend Among Public Sector Entities Expanding FM Market

Public administrations are accelerating outsourcing to meet fiscal targets linked to the National Recovery and Resilience Plan, channeling tasks such as cleaning, catering, and minor maintenance to private contractors Legislative Decree 209/2024 raised Building Information Modeling thresholds to EUR 2 million (USD 2.25 million), effectively steering large framework agreements toward bidders with digital capabilities.[1]Italian Government, “Law 15/2024 Catastrophe Insurance,” GOVERNO.IT School catering awards in Tuscany and Friuli during 2025 ran for up to four years, transferring performance risk to providers and locking in predictable public cashflows. Regional health authorities in Lombardy have extended hospital non-clinical FM contracts to ten-year terms, favoring ISO 41001-certified operators that can guarantee uptime of critical systems. These dynamics are widening the addressable base for integrated service providers and underpinning a steady rise in outsourced share inside the Italy facility management market.

Growth of Italy's Tourism and Hospitality Sector Boosting Demand for Soft FM Services

International visitor spending reached EUR 60.4 billion (USD 68.1 billion) in 2025, lifting hotel occupancy above 70% in core destinations and reigniting demand for cleaning, linen, and security contracts.[2]World Travel and Tourism Council, “Italy 2025 Economic Impact Report,” WTTC.ORG A majority of hotels diverted more than 15% of annual turnover into sustainability upgrades that require ongoing HVAC and waste-management support, often embedded in bundled deals that align with EU Taxonomy rules. The Milano-Cortina 2026 Winter Olympics attracted a EUR 110 million (USD 123.2 million) green loan for its Olympic Village, guaranteeing integrated FM work through at least 2028. Short-term rental platforms now command one fifth of accommodation nights and frequently outsource rapid-turnover cleaning to specialized providers, boosting contract frequency albeit at smaller ticket sizes. Safety regulations enforced by regional tourism boards obligate third-party fire inspections, further enlarging soft-service scope within the Italy facility management market.

Increasing Adoption of Integrated Facility Management Contracts for Cost Optimization

Corporate occupiers are consolidating vendor lists, shifting from single-service to holistic outcome-based agreements that bundle MEP, cleaning, security, and catering. Rekeep disclosed a EUR 2.3 billion (USD 2.59 billion) backlog in mid-2025, of which 60% stemmed from contracts that tie payment to uptime or energy-savings metrics. Siram Veolia secured EUR 265 million (USD 298.7 million) across 80 projects that finance lighting retrofits and boiler replacements in exchange for fifteen-year utility-savings shares.[3]Veolia, “Siram Italy Operations Update,” VEOLIA.COM ISO 50001 energy-management certification now yields bid-evaluation premiums of up to 10% in integrated tenders, tilting awards toward digitally mature providers. Smaller firms lacking multi-service breadth are exploring cooperatives or niche specializations to remain competitive. This migration to integrated contracting is steadily enlarging deal sizes throughout the Italy facility management market.

Expansion of Data-Center Industry in Northern Italy Spurring Specialized Technical FM Demand

Hyperscale and colocation operators announced more than EUR 1 billion (USD 1.13 billion) of Lombardy capacity additions in 2025, positioning Milan as a Mediterranean fiber hub. VIRTUS Data Centres is building a 36-megawatt campus that mandates 24/7 HVAC monitoring, redundant power testing, and EN 54-compliant fire suppression.[4]VIRTUS Data Centres, “Milan Campus Announcement,” VIRTUSDC.COM Uptime Institute Tier III requirements oblige FM partners to maintain rigorous preventive maintenance schedules and minute-by-minute reporting. Early adopters of AI-driven predictive analytics report downtimes cut by 40%, an operational edge that raises switching costs for clients. Specialized technical FM therefore represents a high-margin, long-duration niche within the Italy facility management market, especially across Lombardy and neighboring Piedmont.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regulatory Framework Across Italian Regions Complicating Compliance Costs | -0.3% | National, Acute in Sicily, Sardinia, Trentino-Alto Adige | Medium Term (2–4 Years) |

| Rising Costs of Skilled Technical Labor Squeezing FM Provider Margins | -0.4% | National, Most Severe in Lombardy, Veneto, Emilia-Romagna | Short Term (≤ 2 Years) |

| Slow Rollout of 5G Infrastructure Delaying Smart-Building FM Deployments | -0.2% | Southern Regions and Rural Areas | Long Term (≥ 4 Years) |

| Municipal Budget Constraints Reducing Outsourcing of Public Facility Upkeep in Smaller Cities | -0.2% | Southern and Central Municipalities Below 50,000 Population | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Framework Across Italian Regions Complicating Compliance Costs

Twenty regional governments maintain distinct building codes and fire-safety protocols, forcing providers to keep parallel compliance teams and document sets. Sicily and Sardinia diverge from national Decree 151/2011, while Trentino-Alto Adige mandates bilingual safety signage, inflating translation and audit expenses. A comparator study covering eight regional hospital contracts found overhead ranging from 4% to 11% of contract value, with the steepest burden in jurisdictions that demand extra on-site inspections. Non-recognition of regional certifications obliges technicians to repeat training when moving between regions, slowing scaling efforts inside the Italy facility management market.

Rising Costs of Skilled Technical Labor Squeezing FM Provider Margins

Vacancy rates for HVAC technicians and electricians exceeded 8% in Lombardy in 2025, and sector-wide wage floors rose 9% across 2024-2025 through collective bargaining. Labor accounts for 60-70% of soft service revenue and about half of hard service costs, eroding operating margins when contracts are locked at fixed prices. Rekeep reported EBITDA of 12.4% in H1 2025, down from 13.1% two years earlier despite top-line growth, attributing the slide to wage inflation. Providers are experimenting with robotic scrubbers and IoT-based workforce scheduling, yet the required capital intensifies competitive pressure on smaller firms inside the Italy facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Services Gain Momentum Amid Hospitality Revival

Hard services generated 58.87% of overall spend in 2025, anchored by mandatory MEP maintenance and fire-safety compliance in industrial and institutional estates. The Italy facility management market size for hard services is expected to expand marginally as energy-performance mandates drive boiler upgrades and LED retrofits. Within this basket, asset-management and predictive diagnostics are drawing premium pricing because they cut emergency interventions. Fire systems continue to post steady gains, underpinned by Law 15/2024 and tighter enforcement of EN 54 standards.

Soft services are registering the quickest advance, rising at a 1.96% CAGR through 2031 as hotels, airports, and museums reopen fully. Cleaning contracts are shifting from labor-hour models to output-based scorecards verified by ATP bioluminescence tests. Security firms are bundling video analytics with guard services to meet insurance requirements, while catering providers are differentiating via organic menus that align with regional green-procurement rules. Collectively, soft services are increasing their slice of the Italy facility management market share as bundled tenders become the norm.

By Offering Type: Outsourced Models Extend Lead Through Integrated Deals

Outsourced arrangements accounted for 66.59% of 2025 value and are widening their advantage as entities divest non-core operations. The Italy facility management market size for outsourced delivery is projected to grow 1.51% through 2031, fueled by public-private energy partnerships that transfer capex risk to contractors. Integrated facility management now forms 40% of new public awards, particularly for hospitals and schools that prefer single-point accountability.

In-house models persist in defense and pharma, yet hybrid solutions are emerging where core client staff integrate with outsourced teams to preserve institutional knowledge. Single-service purchasing remains popular among SMEs, but cooperatives of local firms are forming to bid bundled work. Digital twin mandates embedded in BIM requirements above EUR 2 million (USD 2.3 million) favor providers with 3D asset-management platforms, raising the technology bar across the Italy facility management market.

By End-User Industry: Commercial Real Estate Drives Retrofit Wave

Commercial buildings controlled 48.07% of spend in 2025 and will post the strongest incremental gains as landlords rush to meet Energy Performance Certificate Class E thresholds before 2030. Retail chains are outsourcing multi-site cleaning to contain costs while grappling with e-commerce margin pressure. Hotels and resorts are volume drivers for linen, HVAC, and waste-management services, with many properties targeting EU Ecolabel accreditation to attract climate-conscious travelers.

Healthcare and institutional segments contribute stable revenue streams through long-duration contracts for technical and catering services. Hospitals are adding predictive maintenance for medical-gas networks under UNI 11554, increasing the Italy facility management market share for specialized hard services. Industrial and logistics operators are pivoting to IoT-equipped predictive maintenance that trims downtime by up to 40%, a feature becoming standard in data-center FM packages around Milan. Other sectors, such as transport hubs and cultural sites, are turning toward integrated security and cleaning to cut fixed labor outlays and meet resilience mandates.

Geography Analysis

Northern Italy, led by Lombardy, Veneto, and Piedmont, generated roughly 55% of national expenditure in 2025. Data-center investments surpassing EUR 1 billion (USD 1.13 billion) and ARERA-aligned energy-community projects are pooling demand for high-spec technical FM. Milan’s business district is nurturing multilocation integrated contracts that lock in ten-year performance guarantees, while Turin’s automotive cluster is adopting energy-as-a-service packages that wrap installation, financing, and maintenance in one fee.

Central regions, anchored by Lazio and Tuscany, continue to rely on public-sector and hospitality contracts. Rome’s ministry complex secures multiyear cleaning and catering tenders that favor ISO-41001 operators, whereas Tuscany’s hotels channel sustainability upgrades through providers supplying EU Ecolabel consumables. The forthcoming Milano-Cortina 2026 Games, straddling Lombardy and Veneto, will extend integrated FM demand beyond the closing ceremony, especially for post-event conversion of venues.

Southern Italy, including the islands, trails in growth given weaker fiscal capacity, fragmented rules, and 5G coverage gaps at 46.8% versus the EU average of 89.8%. However, seismic regions such as Abruzzo and Marche are fast-tracking disaster-repair and resilience works under Law 15/2024, adding technical FM scope linked to insurance premium discounts. Budget limitations in smaller municipalities temper the pace, yet National Recovery funds are gradually flowing to shovel-ready projects, sustaining a baseline of outsourced opportunities across the Italy facility management market.

Competitive Landscape

The top five companies held an estimated 30-35% of 2025 revenue, underscoring a moderately fragmented structure where regional specialists thrive on localized know-how. Multinationals such as Sodexo and Apleona deploy global purchasing power and advanced digital platforms, capturing nationwide integrated contracts. Domestic leaders like Rekeep and Siram leverage entrenched municipal relationships and dense branch networks to shield share in healthcare and education tenders. Apleona’s December 2024 takeover of Galli Facility Management widened its Italian footprint, while Rekeep’s January 2026 purchase of a 60% stake in Euromex advanced its Iberian reach.

Technology serves as the main wedge between leaders and laggards. Front-runners invest in IoT sensors, AI-based predictive maintenance, and digital twins that slash reactive interventions by up to 40%. Legislative Decree 209/2024 lifted BIM thresholds, effectively trimming smaller, less digitized bidders from high-value public frameworks. Firms unable to finance automation retreat into niches such as landscaping, pest control, or low-risk cleaning. Certification trends reinforce the gap; ISO 41001 and ISO 50001 credentials have become table stakes in government procurement, raising barriers and consolidating share among technologically advanced players within the Italy facility management market.

White-space pockets persist, especially in performance-based energy contracts where providers front hardware costs in exchange for multiyear utility-savings splits. Siram Veolia pioneered this structure across 80 public-private projects worth EUR 265 million (USD 298.7 million) through 2027, a template now emulated by rivals. Margin pressure from labor inflation is nudging all tiers toward automation and remote monitoring, likely accelerating M&A as scale becomes necessary to fund technology adoption.

Italy Facility Management Industry Leaders

ATLAS I.F.M. S.R.L.

Sodexo Facilities Management Services (SODEXO GROUP)

Compass Group PLC

Euro & Promos Facility Management S.P.A (EURO & PROMOS)

Rekeep SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Rekeep acquired a 60% stake in Euromex, broadening its healthcare portfolio and extending operations into Portugal.

- January 2026: Rekeep and Alba Infra rolled out the Multisector Facility Management Circular II fund, deploying EUR 40 million (USD 44.8 million) for energy-efficiency and resilience retrofits in public buildings.

- May 2025: SAGAD s.r.l., the Italian subsidiary of B+N Referencia Zrt., has acquired the facility management operations of Verona-based L’Alleanza Società Cooperativa.

- October 2025: Sodexo posted FY 2025 revenue of EUR 24.1 billion (USD 27.2 billion), citing 94% client retention and expanded integrated FM activity in education and healthcare.

- October 2025: Rekeep reported H1 2025 revenue of EUR 622.1 million (USD 702.2 million) and a EUR 2.3 billion (USD 2.59 billion) backlog, with 60% tied to outcome-based integrated contracts.

Italy Facility Management Market Report Scope

The study tracks the facility management (FM) market-related trends in Italy by analyzing the turnover accrued through service providers' end-user contracts. The study tracks the revenues accrued from services offered for building operation and maintenance (mechanical and electrical services, heating and ventilation, plumbing, building services control and management systems, building fabric portable application testing, fire protection systems, fire alarm, and detection systems), environmental management (energy management services, waste management, recycling services), IT and telecommunication (establishment and maintenance of IT systems and the introduction of software packages), support services (cleaning, catering, vending, courier services, laundry services, post room staffing and management, reception staffing, and security) and property management (space planning and design, asset management, property acquisitions and disposals, and relocation management).

The Italy Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large is the Italy facility management market in monetary terms for 2026?

It is valued at USD 9.67 billion in 2026, on track to reach USD 10.36 billion by 2031.

What is the projected CAGR for facility management services in Italy between 2026 and 2031?

The compound annual growth rate stands at 1.39% for the forecast period.

Which service segment is growing fastest inside Italian facilities?

Soft services such as cleaning, security, and catering are advancing at a 1.96% CAGR thanks to tourism recovery and bundled public tenders.

Why are integrated facility management contracts gaining popularity?

Corporations and public bodies prefer single-point accountability and cost savings, which integrated contracts deliver along with performance-based payment models.

Which region of Italy shows the highest demand for technical FM linked to data centers?

Lombardy leads, with more than EUR 1 billion of committed data-center investments that require 24 hour high-spec maintenance.

What is driving resilience-oriented FM spending in seismic zones?

Law 15/2024 mandates catastrophe insurance, and insurers grant premium discounts for buildings that complete certified seismic and fire-safety upgrades.

Page last updated on: