Italy HVAC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 7.07 Billion |

| Market Size (2031) | USD 9.61 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

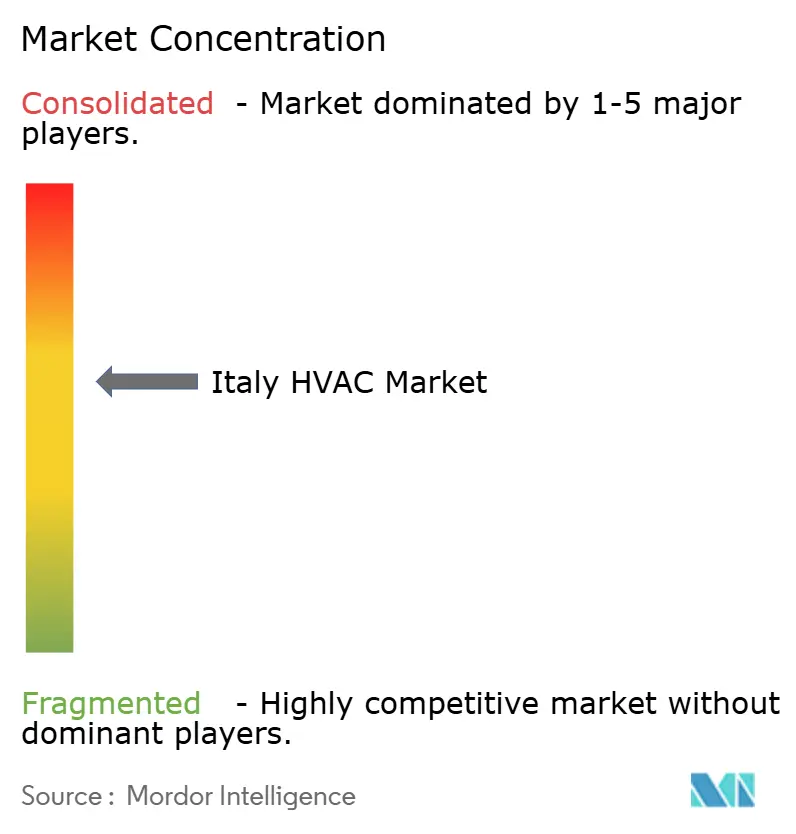

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy HVAC Market Analysis by Mordor Intelligence

The Italy HVAC market size stood at USD 7.07 billion in 2026 and is projected to reach USD 9.61 billion by 2031, reflecting a 6.34% CAGR over the forecast period. Robust retrofit activity in the country’s 12 million pre-1990 residential units, the phase-down of high-GWP refrigerants, and municipal fast-tracking of nearly-zero-energy new builds underpin the outlook. Cooling demand keeps rising because summer peak temperatures in southern provinces now exceed 40 °C for longer spells, while national policy targets 6.5 million installed heat pumps by 2030. Supply chains are adjusting to EU anti-dumping duties on Chinese heat pumps, prompting distributors to diversify sourcing and invest in low-GWP refrigerant inventory. Competition remains moderate, with five multinational brands controlling 38% of revenue, but regional specialists win custom projects through shorter lead times and proximity to northern Italy’s metalworking clusters.

Key Report Takeaways

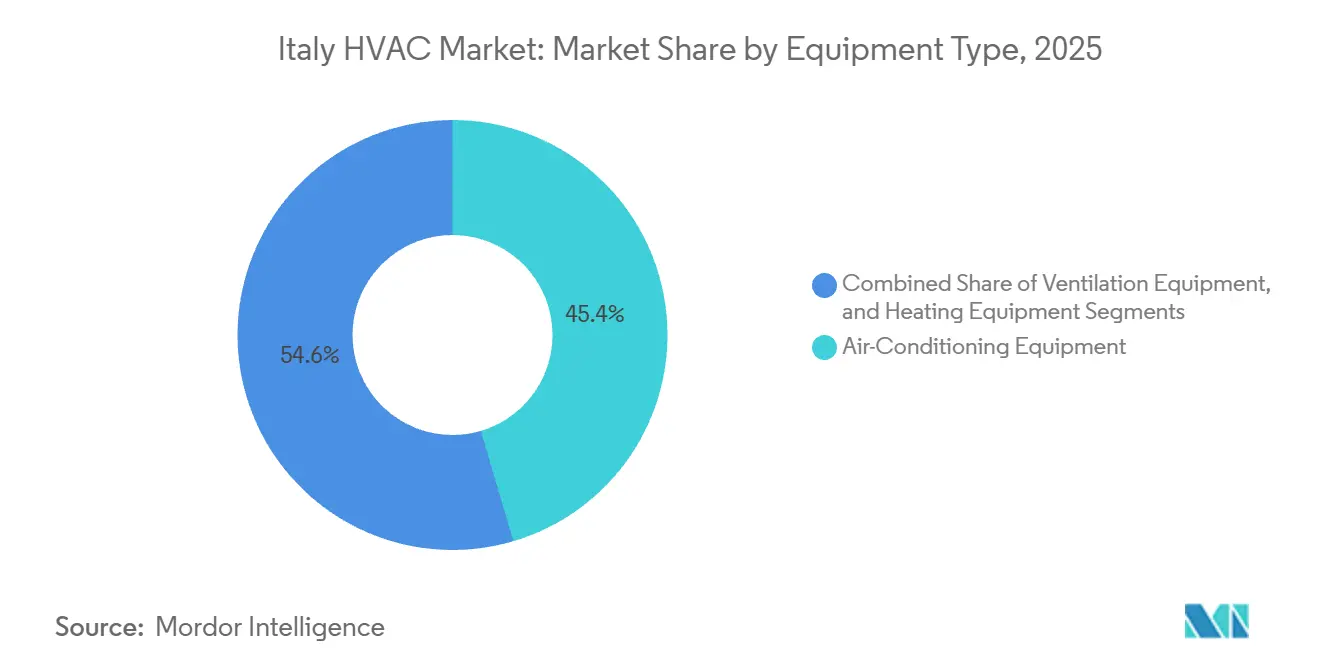

- By equipment type, air-conditioning led with a 45.43% revenue share in 2025, while heating equipment, anchored by heat pumps, is projected to deliver the fastest 7.14% CAGR through 2031.

- By installation type, retrofit and replacement captured 61.64% of the Italian HVAC market share in 2025; new construction remains the fastest-growing segment, with a 7.39% CAGR to 2031.

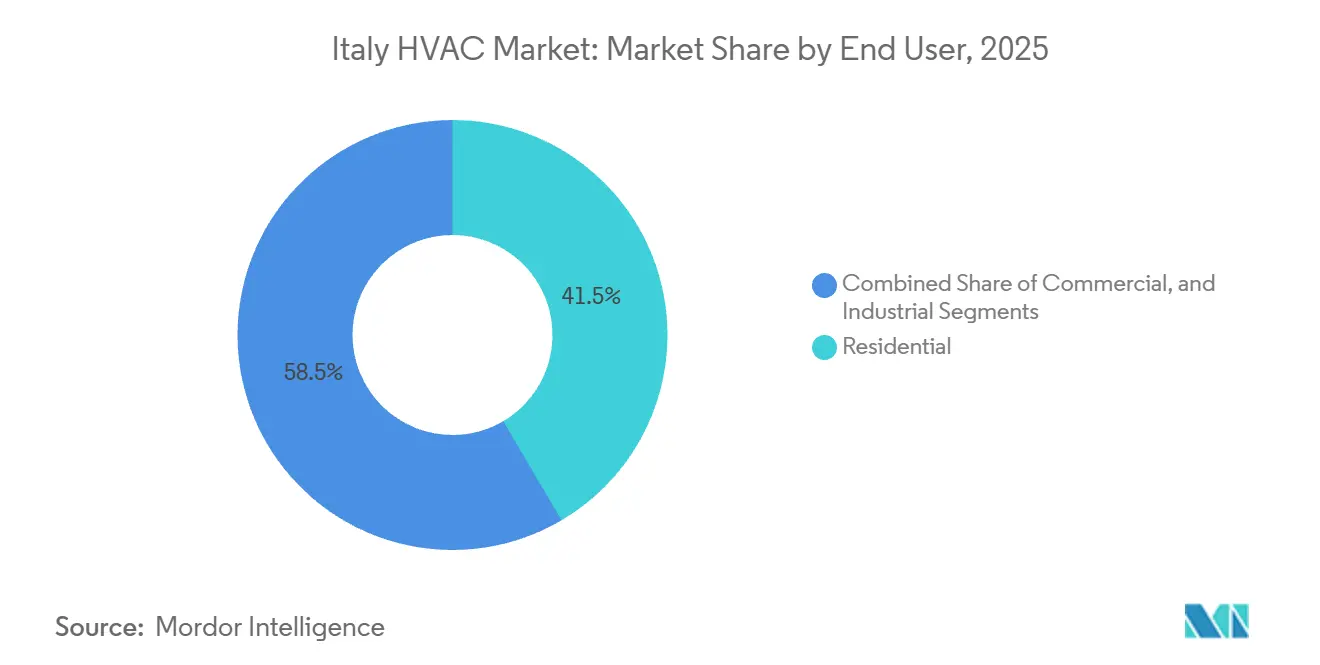

- By end user, residential retained 41.53% of 2025 revenue, whereas the commercial category shows the highest projected CAGR at 7.48% through 2031.

- By commercial building type, office properties held 34.23% of installations in 2025, while data centers exhibited the quickest 8.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive government incentives and tax credits for energy efficiency | +1.80% | National, higher uptake in Lombardy, Emilia-Romagna, Veneto | Medium term (2-4 years) |

| Growing demand for replacement and retrofit activity | +1.50% | National, concentrated in pre-1990 stock across northern and central regions | Long term (≥ 4 years) |

| Increasing heat pump adoption under EU climate targets | +1.30% | National, accelerated deployment in Piedmont, Friuli-Venezia Giulia | Medium term (2-4 years) |

| Growing residential construction under legacy Superbonus scheme | +0.70% | National, strongest in Lazio, Campania | Short term (≤ 2 years) |

| Emergence of low-GWP refrigerants creating early replacement cycle | +0.60% | National, driven by F-Gas compliance timelines | Medium term (2-4 years) |

| Demand for smart HVAC to comply with building-automation decree | +0.40% | National, mandatory for non-residential facilities above 290 kW | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supportive Government Incentives And Tax Credits For Energy Efficiency

Italy replaced the broad Superbonus 110% deduction with the targeted Ecobonus and Conto Termico 3.0 programs in 2025. Conto Termico disbursed EUR 320 million (USD 360 million) for thermal equipment in 2025, with heat pumps accounting for 58% of approved applications.[1]Italian National Agency for New Technologies Energy and Sustainable Economic Development, “Conto Termico 3.0 Annual Report 2025,” Enea.it Homeowners now prioritize boiler-to-heat-pump conversions because the incentive mix cuts capital outlay, and residential electricity-to-gas price ratios have widened to 3.2:1. A “trainability” clause that links incentives to F-Gas-certified installers tightens quality control and channels projects toward accredited contractors.

Growing Demand For Replacement And Retrofit Activity

Retrofit and replacement work accounted for 61.64% of 2025 revenue as 35% of Italian homes predate 1980 and face a 2033 deadline for Energy Performance Certificate class-E compliance.[2]Italian Ministry of Environment and Energy Security, “National Energy and Climate Plan Update,” Mase.gov.it The ministry’s 2025 Renovation Strategy projects that 1.8 million homes will need HVAC upgrades by 2030, totaling 360,000 units per year. Contractors complete boiler-to-heat-pump swaps in under a week, earning gross margins that averaged 32% in 2025, well above new-build margins. Shorter project cycles help installers smooth seasonal workloads and improve cash flow.

Increasing Heat Pump Adoption Under EU Climate Targets

The 2025 update to Italy’s National Energy and Climate Plan set a 6.5 million unit heat-pump target by 2030, up from 2.1 million units in place at end-2025. Air-to-water models hold 68% of sales because they integrate with legacy radiator networks at supply temperatures of 50-55 °C. Daikin reported 31% Italian heat-pump revenue growth in 2025, driven by its Altherma 3 H HT unit that delivers 70 °C water without emitter replacement. VAT exemptions on heat pumps through 2027 narrow the cost gap with condensing boilers to below EUR 1,200 (USD 1,350).

Emergence Of Low-GWP Refrigerants Creating Early Replacement Cycle

Regulation (EU) 2024/573 mandates a 95% reduction in HFCs by 2030 and bans high-GWP refrigerants in new single-split systems after 2027. Italy hosts 4.2 million installed R-410A units, and distributors are moving to R-32 and R-454B inventory. Mitsubishi Electric converted 85% of its Bassano del Grappa lines to R-32 production in 2025. Technicians must buy dual-refrigerant recovery tools and complete extra training for mildly flammable A2L gases, straining Italy’s limited installer pool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages | -1.20% | National, acute in Calabria, Sicily, Puglia | Medium term (2-4 years) |

| High initial costs of energy-efficient systems | -0.90% | National, heavier burden on rural single-family homeowners | Short term (≤ 2 years) |

| Lengthy municipal permitting for historic retrofits | -0.50% | UNESCO centers in Florence, Venice, Rome, Naples | Long term (≥ 4 years) |

| Supply-chain volatility for electronics post-tariffs | -0.40% | National, impacts imported VRF systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages

Italy counted only 18,000 F-Gas-certified installers in 2025, roughly 7,000 short of what is needed to support the planned heat-pump ramp. The shortfall is most acute in the south, where vocational enrollment lags and youth unemployment tops 30%. The new A2L certification requires 16 training hours per technician and has created nine-month waiting lists at accredited centers. Contractors bid wages up by 18% in Lombardy in 2025 just to secure crews.[3]Assoclima, “Distributor Market Structure Report 2025,” Assoclima.it

High Initial Costs Of Energy-Efficient Systems

A typical air-to-water heat pump for a 150 m² rural home costs EUR 12,000-18,000 (USD 13,500-20,300) in 2025, triple the price of a condensing boiler. Ecobonus deductions spread over 10 years exclude households with insufficient tax liability, a group that includes many retirees and low-income owners. The European Central Bank kept its deposit rate at 3.00% through early 2026, leaving renovation loans 120 basis points dearer than the 2019-2021 average. Cost barriers channel demand toward entry-level ductless splits that seldom meet top-tier efficiency targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Cooling Dominance Masks Heat-Pump Crossover

Air-conditioning equipment accounted for 45.43% of 2025 revenue, and the category is on track for a 7.14% CAGR through 2031. Rising Mediterranean heat and an 8% increase in cooling degree-days between 2020 and 2025 underpin growth. Ductless mini-splits captured 62% of air-conditioning revenue in 2025. Installers favor R-32 inverter models that exceed seasonal energy-efficiency ratios of 8.5 and remain eligible for Ecobonus tax relief. Variable refrigerant flow systems accounted for only 11% of units but 28% of sales value, due to average system prices above EUR 35,000 (USD 39,400). Heating hardware, including boilers and heat pumps, is growing more slowly in volume but benefits from Conto Termico grants that cover up to 40% of heat-pump costs. Ventilation remains a niche mostly found in hospitals and cleanrooms governed by UNI EN ISO 14644 standards that require 20-30 air changes per hour.

Packaged terminal and room air conditioners are declining at roughly 3% a year as window units give way to inverter splits, helping buildings reach EPC class E by 2033. Chiller demand is pivoting toward magnetic-bearing centrifugal compressors and adiabatic free-cooling towers that use up to 35% less energy than legacy screw models. Ariston’s NXTS chiller series, launched in 2025, illustrates the technology shift with integrated predictive maintenance algorithms that optimize part-load operation. Low-GWP refrigerants are reshaping product catalogs across the board, with Carrier aiming to have 60% of its commercial chillers on R-454B by end-2026.

By Installation Type: Retrofit Margins Eclipse New-Build Volume

Retrofit and replacement work delivered 61.64% of 2025 revenue thanks to Italy’s aging housing stock. Average gross margins reached 32% in 2025 because retrofit jobs involve diagnostics, custom ductwork, and integration with old hydronic circuits. The Italy HVAC market tied to new-build projects is growing at a 7.39% CAGR as municipalities accelerate approvals for nearly zero-energy developments under Legislative Decree 199/2021. Prefabricated HVAC modules that integrate heat pumps, ventilation, and controls are emerging in Lombardy and Veneto. Systemair’s 2025 joint venture with Algeco to supply 1,200 modular housing units in Milan cut on-site labor by 45%. While modularization trims contractor revenue, it speeds schedules, a key draw for developers.

Retrofit demand remains structurally strong because 1.8 million homes need HVAC upgrades by 2030 to satisfy the European Performance of Buildings Directive. Boiler-to-heat-pump swaps take less than a week, letting installers handle higher volumes during mild seasons when new-build work slows. New construction, however, wins on policy momentum. Energy-neutral projects must cover at least 60% of heating and cooling with renewables, ensuring that heat pumps and advanced ventilation stay core specifications in future building permits.

By End User: Commercial Outpaces Residential On Automation Mandates

Residential customers generated 41.53% of 2025 revenue, propelled by 340,000 Ecobonus-supported interventions that year. Yet commercial buildings are expanding faster at a 7.48% CAGR to 2031, driven by UNI EN 15232-1 automation mandates for facilities with more than 290 kW HVAC capacity. Variable refrigerant flow technology enables simultaneous heating and cooling across zones, reducing installed capacity by about 18%. Office buildings accounted for 34.23% of commercial installations but face a soft outlook amid a 14% vacancy in Milan’s CBD in late 2025.

Retailers deploy demand-controlled ventilation that cuts off-peak energy use by up to 35%, while hospitals invest in redundant chillers and high-efficiency filters. Industrial users focus on process cooling for food, pharmaceuticals, and data processing, where uptime requirements above 99.9% drive adoption of N+1 or 2N chiller redundancy. The Italy HVAC market share linked to industrial end users thus remains stable even as total building space grows.

By Building Type (Commercial): Data Centers Lead With Liquid Cooling

Data centers are the fastest-growing commercial sub-segment, advancing at an 8.01% CAGR. National capacity reached 180 MW in 2025, a 28% jump fueled by hyperscale investments in Milan’s Caldera Park and Rome’s Technopole clusters. Direct-to-chip liquid cooling is gaining traction because air systems cannot economically dissipate 50 kW per rack heat fluxes. Vertiv reported a 140% increase in Italian liquid-cooling revenue in 2025, with its Liebert DSE platform accounting for 60% of AI and HPC orders. Office, retail, hospitality, and education follow in share but show divergent technology adoption tied to occupancy patterns and regulatory demands.

Educational institutions, hospitality, retail, and healthcare facilities together account for the majority of commercial floor area outside data centers and offices, and each has distinct HVAC preferences that enhance the overall project value. Hospitals deploy redundant chiller arrays with N+1 configurations and HEPA filtration to ensure 99.9% uptime for critical-care zones, while boutique hotels prioritize variable refrigerant flow systems that offer per-room temperature control and occupancy sensing to cut energy costs by up to 30%. Retail chains invest in rooftop packaged units with demand-controlled ventilation, achieving energy savings near 25% during off-peak hours, and universities tap low-interest EIB Green Schools loans to modernize legacy plants, often specifying district-cooling links that future-proof multiple buildings at once. This diversification cushions suppliers against cyclical swings in any single building category and underpins steady order books for both multinational brands and regional custom-fabricators.

Geography Analysis

The northern regions of Lombardy, Veneto, Emilia-Romagna, and Piedmont accounted for roughly 52% of national HVAC turnover in 2025. Lombardy alone produced 18% on the back of Milan’s dense office stock and rapid data-center growth. The area issued 38,000 building permits in 2025, up 12% year on year, and often specifies factory-assembled HVAC cores that slash on-site labor. Veneto’s wine industry and Emilia-Romagna’s automotive suppliers invest heavily in ammonia and CO₂ transcritical systems that satisfy low-GWP mandates.

Central Italy accounted for about 24% of revenue in 2025. Rome’s historic center complicates retrofits because façade-mounted condensers require Superintendency approval that averaged 11 months in 2025. Concealed duct and rooftop units meet aesthetic rules but cost up to 40% more than standard splits, limiting adoption to premium projects. Tuscany’s hospitality sector, with 48 million overnight stays in 2025, prioritizes VRF systems for boutique hotels where individual room control is essential.

Southern Italy and the islands generated the remaining 24% of revenue. Cooling demand dominates because coastal provinces record more than 600 cooling degree-days annually. Lower per-capita incomes of EUR 18,200 (USD 20,500) in 2025 and sparse installer density, one technician per 3,800 households, extend project lead times to 12 weeks in peak season. Southern regions captured only 19% of Conto Termico grants in 2025 despite housing 34% of the population. Labor shortages and financing gaps thus temper growth even as climate conditions favor air-conditioning uptake.

Competitive Landscape

The market is moderately fragmented, with companies such as Daikin, Carrier, Mitsubishi Electric, Ariston, and Bosch. Daikin and others posted Italian heat-pump revenue growth, anchored by Altherma 3 H HT units capable of 70 °C water output. Carrier’s acquisition of Viessmann’s climate business in 2025 boosts its European capacity to 1.2 million heat pumps by 2027, positioning it to capture the looming R-410A replacement cycle. Regional manufacturers such as Clivet and Riello win bespoke projects through 14-day lead times and close ties to northern metalworking suppliers.

White-space opportunities lie in historic retrofits where concealed systems can command price premiums up to 40%. Rhoss and Aermec target this niche with modular chiller arrays sized for existing mechanical rooms, meeting Superintendency visual criteria while achieving seasonal energy-efficiency ratios above 4. Johnson Controls filed a patent in September 2025 for a predictive maintenance algorithm that cuts unplanned downtime by 60% in commercial deployments. Distributor consolidation is underway because complying with the revised F-Gas Regulation requires retooling recovery equipment and retraining staff. Italy’s distributor count fell from 1,840 in 2023 to 1,620 in 2025, while the top ten distributors grew their combined share to 51%.

Digital service models are becoming a decisive battleground. Leading manufacturers now bundle predictive-maintenance analytics and energy-performance guarantees into multi-year service contracts that lock in annuity revenue and raise switching costs for building owners. Bosch introduced a subscription-based monitoring platform in October 2025 that connects condensing boilers and heat pumps to a cloud dashboard, enabling remote firmware updates and alerting facility managers to efficiency drifts exceeding 5%. Ariston followed in December 2025 with a pay-per-use chiller program targeting data center operators, where monthly fees scale with measured cooling ton-hours, effectively shifting capital expenses to operating expenses and improving customer cash flow. These service-centric offerings intensify competition well beyond equipment price, favor suppliers with strong software capabilities, and marginalize small distributors that lack in-house digital expertise.

Italy HVAC Industry Leaders

Carrier Corporation

Daikin Industries, Ltd.

Midea Group Co., Ltd.

Johnson Controls International PLC

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Daikin committed EUR 45 million (USD 50.7 million) to expand its Ostend R and D center, targeting high-temperature R-32 and R-454B heat pumps for Italian retrofits.

- November 2025: Mitsubishi Electric opened a 12,000 m² logistics hub in Bologna, trimming delivery lead times for northern contractors to five days and adding training capacity for 240 technicians per year.

- October 2025: Ariston launched its NXTS magnetic-bearing centrifugal chiller line, manufactured in Osimo and optimized for data-center and district-cooling loads above 500 kW.

- September 2025: Carrier closed a EUR 12 billion (USD 13.5 billion) purchase of Viessmann’s climate unit, adding German and Polish heat-pump plants to its network.

- July 2025: Clivet won a EUR 28 million (USD 31.5 million) VRF contract for the Milan Expo 2015 site redevelopment, specifying simultaneous heating and cooling capability.

Italy HVAC Market Report Scope

HVAC (heating, ventilation, and air conditioning) refers to the broad array of heating and cooling systems homeowners employ to regulate indoor temperature and humidity. Beyond temperature control, these systems enhance indoor air quality through mechanical ventilation and filtration. The HVAC systems include central air conditioners, ductless mini-splits, furnaces, and boilers. Additionally, HVAC encompasses the extensive refrigeration systems found in commercial structures.

The Italy HVAC Market Report is Segmented by Equipment Type (Heating Equipment, Ventilation Equipment, and Air-Conditioning Equipment), Installation Type (New Construction, and Retrofit and Replacement), End User (Residential, Commercial, and Industrial), and Building Type (Commercial) (Office Buildings, Healthcare Facilities, Hospitality and Leisure, Retail Stores and Malls, Educational Institutions, and Data Centers). The Market Forecasts are Provided in Terms of Value (USD).

| Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | ||

| Unitary Heaters | ||

| Ventilation Equipment | Air Handling Units (AHUs) | |

| Air Filters | ||

| Fan Coil Units | ||

| Humidifiers and Dehumidifiers | ||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits |

| Ductless Mini-Splits | ||

| Packaged Rooftops | ||

| Variable Refrigerant Flow (VRF) Systems | ||

| Room Air Conditioners | ||

| Packaged Terminal Air Conditioners | ||

| Chillers | ||

| New Construction |

| Retrofit / Replacement |

| Residential |

| Commercial |

| Industrial |

| Office Buildings |

| Healthcare Facilities |

| Hospitality and Leisure |

| Retail Stores and Malls |

| Educational Institutions |

| Data Centers |

| By Equipment Type | Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | |||

| Unitary Heaters | |||

| Ventilation Equipment | Air Handling Units (AHUs) | ||

| Air Filters | |||

| Fan Coil Units | |||

| Humidifiers and Dehumidifiers | |||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits | |

| Ductless Mini-Splits | |||

| Packaged Rooftops | |||

| Variable Refrigerant Flow (VRF) Systems | |||

| Room Air Conditioners | |||

| Packaged Terminal Air Conditioners | |||

| Chillers | |||

| By Installation Type | New Construction | ||

| Retrofit / Replacement | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Building Type (Commercial) | Office Buildings | ||

| Healthcare Facilities | |||

| Hospitality and Leisure | |||

| Retail Stores and Malls | |||

| Educational Institutions | |||

| Data Centers | |||

Key Questions Answered in the Report

What is the forecast value of the Italy HVAC market in 2031?

The sector is projected to reach USD 9.61 billion by 2031, underpinned by a 6.34% CAGR.

How fast are data-center HVAC installations growing in Italy?

Data-center applications are expanding at an 8.01% CAGR thanks to hyperscale capacity additions in Milan and Rome.

Which equipment type currently leads sales in Italy?

Air-conditioning equipment holds 45.43% of 2025 revenue, led by ductless mini-splits.

Why are retrofit margins higher than new-build margins for contractors?

Retrofit jobs involve diagnostics and custom integration, lifting gross margins to 32% versus 21% for new construction.

What policy targets are driving heat-pump demand?

The updated National Energy and Climate Plan sets a goal of 6.5 million installed heat pumps by 2030.

Page last updated on: