Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

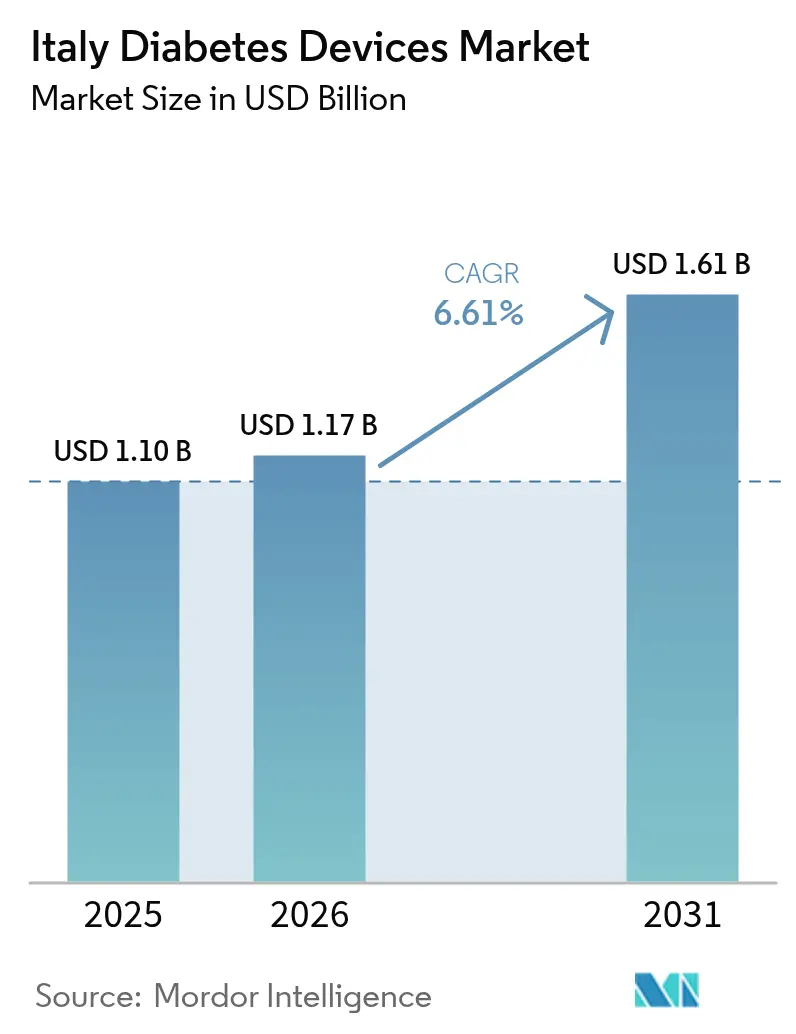

| Base Year Market Size (2025) | USD 1.1 Billion |

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Diabetes Devices Market Analysis by Mordor Intelligence

Italy diabetes devices market size in 2026 is estimated at USD 1.17 billion, growing from 2025 value of USD 1.1 billion with 2031 projections showing USD 1.61 billion, growing at 6.61% CAGR over 2026-2031. The steady rise reflects an aging population, a 92.14% dominance of Type 2 cases, and a policy environment that reimburses continuous glucose monitoring (CGM) for priority groups under the National Health Service. Adoption accelerates further as pharmacies become clinical hubs, telemedicine tools spread to 72% of facilities, and hybrid closed-loop pumps enter reimbursement formularies. Management products enjoy a 7.14% CAGR due to weekly insulin and tubeless automated delivery roll-outs, while monitoring devices retain scale leadership at 58.12% share in 2024. North–South funding gaps and stringent European accuracy rules temper momentum, yet targeted digital spending of EUR 1.6 billion keeps Italy among Europe’s most attractive pilots for advanced diabetes technology.

Key Report Takeaways

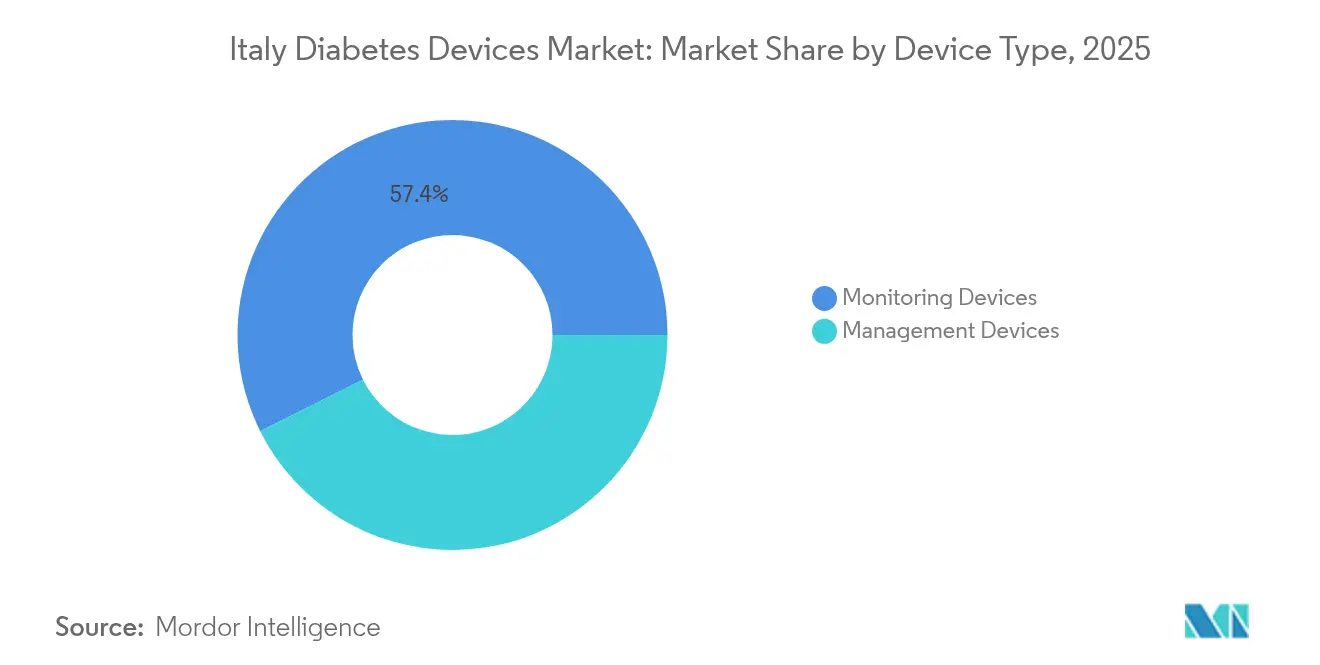

- By device type, monitoring solutions held 57.38% of Italy diabetes devices market share in 2025; management devices display the fastest 6.98% CAGR to 2031.

- By end user, homecare settings commanded 67.12% of Italy diabetes devices market size in 2025; hospitals and clinics lead growth at a 7.26% CAGR.

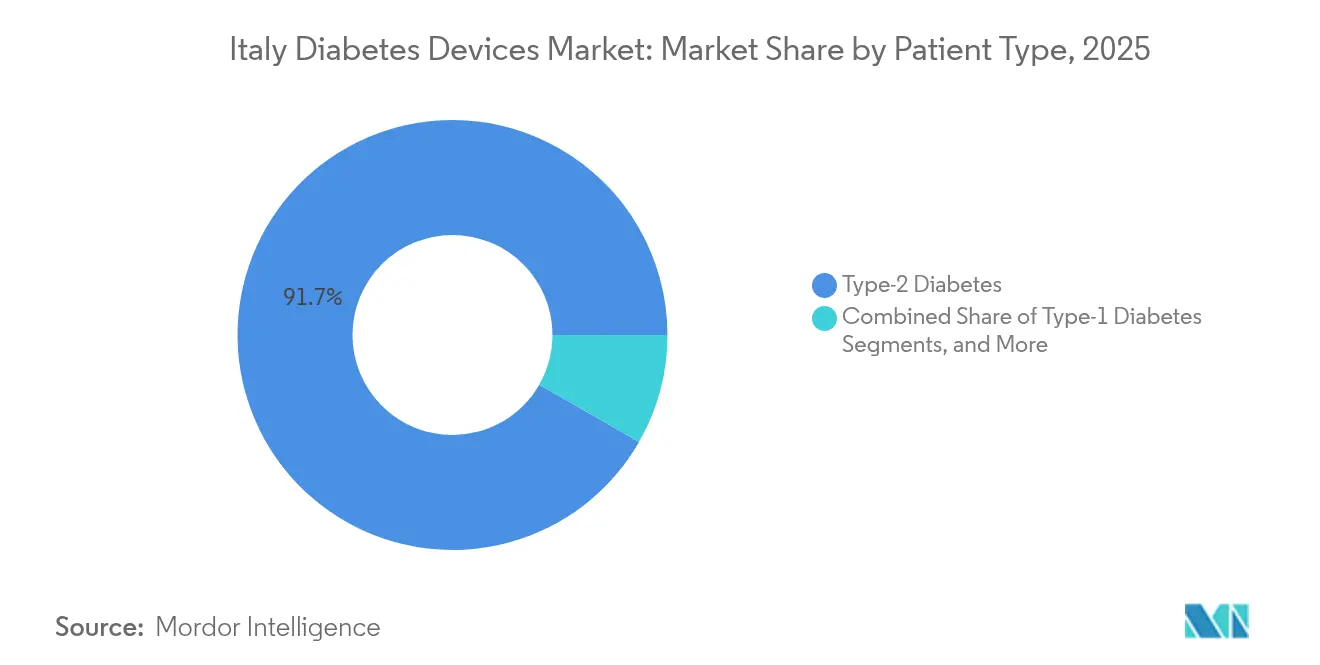

- By patient group, Type 2 cases accounted for 91.72% of Italy diabetes devices market size in 2025 and are advancing at 7.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement of CGM sensors for T1 & pediatric patients | +1.2% | National, with stronger uptake in Northern regions | Medium term (2-4 years) |

| Growing telemedicine adoption & home-care push post-PNRR | +1.8% | National, with digital gaps in Southern Italy | Long term (≥ 4 years) |

| Expansion of pharmacy-run diabetes clinics (Farmacie dei Servizi) | +1.1% | National, accelerated in urban centers | Medium term (2-4 years) |

| Rising Prevalence of Obesity Among Youth Increasing Earlier Onset Diabetes | +1.5% | National, with higher rates in Southern regions | Long term (≥ 4 years) |

| AI-powered decision-support in hybrid-closed-loop pumps | +0.9% | Northern Italy initially, expanding nationally | Long term (≥ 4 years) |

| Rising prevalence & earlier onset of Type-2 diabetes | +1.7% | National, with regional variation patterns | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement of CGM Sensors for T1 & Pediatric Patients

Parliamentary Law 130/2023 mandates national screening for citizens aged 1–17 years, routing newly diagnosed children swiftly toward CGM adoption [1]The Lancet Diabetes & Endocrinology, “Italy introduces nationwide paediatric diabetes screening,” thelancet.com. The Ministry of Health already funds FreeStyle Libre for both Type 1 and insulin-intensive Type 2 users, removing a key cost hurdle. Multi-center trials in Lombardy, Emilia Romagna, and Toscana report HbA1c falls of 0.4% at three months and 0.6% at six months with intermittently scanned CGM. Early CGM habituation in childhood is expected to lift lifetime adherence and enlarge long-term sensor revenue. Implementation lags occur in Calabria and Sardegna, yet national reimbursement rules give suppliers a clear demand signal.

Growing Telemedicine Adoption & Home-Care Push Post-PNRR

EUR 1.6 billion from the Recovery Plan modernizes electronic health records, enabling 72% of hospitals to activate tele-consults that directly feed glucose data into clinical portals. Surveys of 600 clinicians show 82% endorse tele-follow-up for routine glycemic reviews, while 80% cite infection-control gains in a post-COVID era. The Connected Care platform and Resilia app allow secure sharing of sensor feeds, though 66% of practitioners caution that digital care cannot replace critical in-person titration visits. Broadband blackspots in inland Basilicata slow real-time uploads, but pharmacy Wi-Fi stations increasingly bridge the gap. Overall, remote monitoring saves travel time for elderly patients and encourages continuous data flow that underpins closed-loop dosing algorithms.

Expansion of Pharmacy-Run Diabetes Clinics

June 2024 reforms authorize 19,000 community pharmacies to perform capillary blood tests, dispense devices, and renew chronic prescriptions on-site. Urban pilot programs in Milan and Turin cut hospital revisit rates by 14% within one year, according to regional health records. Pharmacies must satisfy hygiene and data-protection criteria, yet most chains can adapt quickly because of existing compounding rooms. Device makers benefit from a broader retail shelf, especially in regions where public hospitals schedule endocrinology appointments three months out. The model also supports weekend access, a gap previously highlighted by patient groups. Success ultimately hinges on structured pharmacist training in device troubleshooting.

Rising Prevalence & Earlier Onset of Type 2 Diabetes

Italy’s obesity rate among adolescents rose to 14.2% in 2024, driving earlier insulin resistance and a shifting onset age toward the mid-30s. Higher incidence clusters in Campania and Sicily mirror socioeconomic gradients, amplifying demand for both CGM and simplified pen needles. The Italian Institute of Statistics projects the 65+ demographic to exceed 24 million by 2030, enlarging the pool of multi-morbidity patients that require seamless glucose control. Employers also face USD 5.2 billion in productivity losses tied to diabetes absenteeism, spurring corporate insurance plans to subsidize sensors for at-risk staff. Earlier onset elongates therapy duration, translating to compounded device revenue over decades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regional funding disparity between North & South | -1.3% | Southern Italy primarily, spillover effects nationally | Long term (≥ 4 years) |

| Strict eCGM accuracy rules delaying new entrants | -0.8% | EU-wide, affecting Italian market access | Medium term (2-4 years) |

| Supply-chain exposure to single-use plastics legislation | -0.5% | National, with EU regulatory alignment | Medium term (2-4 years) |

| Data-privacy constraints on cloud glucose platforms | -0.7% | National, with GDPR compliance requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regional Funding Disparity Between North & South

Seven regions, including Calabria and Sardegna, failed minimum-care benchmarks in 2021, leading to rationed CGM allocations and longer waiting lists. New autonomy legislation of June 2024 allows wealthier regions to self-fund enhanced benefits, potentially widening access gaps. Out-of-pocket drug spending equals 23% of national healthcare costs but weighs heavier on lower-income households prevalent in the South. Clinician migration northward compounds capacity shortages. Device suppliers must therefore calibrate pricing tiers and co-pay support programs to avoid lost volumes in underfunded territories.

Strict eCGM Accuracy Rules Delaying New Entrants

Following adverse sensor events in Campania, European regulators require tighter Mean Absolute Relative Difference thresholds and larger pediatric datasets before market clearance. Start-ups without longitudinal data face approval cycles of 24–30 months, raising capital burn rates. Abbott, Dexcom, and Roche hold an advantage by leveraging extensive real-world evidence and established quality systems. While patient safety improves, slower launch tempos may restrict price competition and prolong incumbent dominance in the Italy diabetes devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Ongoing Innovation Fuels Management Segment Expansion

The monitoring category retained 57.38% of Italy diabetes devices market share in 2025, underpinned by the country’s entrenched self-testing culture and full reimbursement of FreeStyle Libre for intensive insulin users. Italy diabetes devices market size for monitoring solutions was USD 0.63 billion in 2025 and is set to climb at a 5.82% CAGR on the strength of sensor upgrades and wider pediatric coverage. Blood-glucose strips continue to sell because many seniors trust finger-prick verification, yet Libre 2 users showed HbA1c drops of 0.6% after six months in a 2,000-patient Lombardy cohort . Hospitals increasingly deploy professional CGM for in-patient titration, expanding the addressable volume of disposable sensors.

Management devices, valued at USD 0.47 billion in 2025, outpace monitoring with a 6.98% CAGR to 2031 as automated delivery platforms proliferate. Insulet’s Omnipod 5 launch in January 2025 introduced the first tubeless system with dual-sensor compatibility, extending choice for the 300,000 Italian Type 1 users eligible for public reimbursement. The weekly insulin Icodec debut in June 2025 slashes injection events by 86%, triggering needle-syringe replacement cycles and encouraging pump trials for dose accuracy. Italian comparative studies reveal MiniMed 780G achieves 71% Time-in-Range, exceeding Tandem Control-IQ’s 68% result, influencing endocrinologist prescribing behaviour. Pen-needle makers follow SIMDO guidance favoring 4 mm 32G formats to minimize lipohypertrophy risk. Management innovations thereby cement a higher-growth runway within the Italy diabetes devices market.

By End User: Digital Infrastructure Sustains Homecare Dominance

Italy diabetes devices market size for homecare reached USD 0.74 billion in 2025 and represents 67.12% of total revenue. Seniors benefit from EUR 1.6 billion in digital investments that provide broadband links for real-time data transfer. Community pharmacists, now authorized to interpret CGM trends, enhance adherence counseling during routine refills. Tele-consult volumes grew 58% between 2022 and 2024, yet 66% of clinicians still insist on quarterly in-person reviews for therapy adjustment. Devices engineered with Bluetooth Low Energy simplify data push from rural villages where 4G coverage is patchy.

Hospitals and clinics capture 32.88% of revenue but grow faster at 7.26% CAGR through 2031. The Marche diabetes network pools 15 clinics on a single electronic record, enabling shared analytics that spotlight sub-optimal sensor usage in real time. Non-ICU wards in Milan adopt professional CGM to detect covert nocturnal hypoglycemia, cutting average length of stay by 0.6 days. Closed-loop pumps approved for in-patient use help standardize perioperative glucose control. Hospitals thus act as technology showcases, accelerating subsequent homecare uptake once patients are discharged.

By Patient Type: Type 2 Segment Dominates and Grows Fastest

Type 2 cases held 91.72% share of the market supported by earlier onset and obesity trends. Bariatric programs in Campania now connect discharged patients directly to CGM follow-ups to prevent relapse, broadening sensor penetration. Employers adopt tax-advantaged wellness packages covering Libre readers for staff with impaired glucose tolerance, a tactic expected to save USD 140 million in lost productivity by 2030. Weekly basal insulin simplifies complexity for poorly controlled Type 2 patients and seeds demand for smart pens that log doses automatically.

Type 1 is growing with 7.55% CAGR and benefits from policy and technology tailwinds. National pediatric screening identifies 2,000 new children annually, and 74% of newly diagnosed families opt for CGM within three months. Hybrid closed-loop adoption is also high; 68% of eligible adolescents in Lombardy transitioned to Omnipod 5 during its first six months, aided by school nurse training campaigns . Continuous data streams feed machine-learning algorithms that predict glucose excursions 30 minutes ahead, reducing parental anxiety. As a result, clinical outcomes improve and advocacy for broader reimbursement rises, indirectly benefiting all device segments within the Italy diabetes devices market.

Geography Analysis

Northern regions contribute more than 55% of national revenue, leveraging robust digital health ecosystems and stronger fiscal capacity. Lombardy processes 12 million e-referrals yearly with 99.9% routing accuracy, allowing endocrinologists to free 1.4 million appointment slots for complex cases. Emilia Romagna pilots same-day pharmacy CGM initiation, cutting average sensor start delays to two days from the former three-week wait. Toscana scales remote foot-ulcer monitoring through 120 tele-clinics, reducing complication-related admissions by 11% in 2024. Such integrated pathways make the North a preferred early–launch zone for innovators in the Italy diabetes devices industry.

Central Italy shows mixed performance. Toscana matches Northern metrics, yet Umbria and Marche contend with rural broadband gaps that slow data uploads. The Marche diabetes network nevertheless integrates 15 centers with shared records, achieving a 4.4% prevalence yet superior control metrics compared to national averages. Lazio’s public-private pilot equips municipal pharmacies with CGM download stations, strengthening adherence among city commuters. These initiatives illustrate how mid-tier regions leverage targeted funds to narrow the technology gap.

Southern territories remain challenging. Calabria, Sicily, and Sardegna failed to guarantee all essential health benefits in 2021, leaving CGM waiting lists of six months. Out-of-pocket costs impair uptake; in Campania, mean annual sensor co-pay reaches USD 210, three times the national average. Clinician shortages also limit advanced pump training sessions. Yet telepharmacy pilots in Bari recorded a 9% HbA1c reduction among 600 enrollees by shipping sensors directly to homes, hinting at scalable work-arounds. Over time, differentiated regional autonomy may either fuel tailored innovation or widen inequities depending on fiscal transfers and workforce mobility.

Regulatory Landscape

Italy diabetes devices are regulated under the EU Medical Device Regulation (MDR 2017/745), with the Italian Ministry of Health acting as the national Competent Authority and maintaining the national medical device database (BD/RDM) for device registration and traceability. For drug-device combination products, the regulatory route depends on the principal mode of action. When a device includes an ancillary medicinal substance, a Notified Body conformity assessment is required, typically with consultation to a competent authority for a scientific opinion (commonly AIFA, and in some cases EMA pathways), which can add evidence and timeline requirements for higher-risk systems such as integrated pump-sensor solutions.

A key operational change for market access and post-market compliance is the phased shift to EUDAMED. Under Commission Implementing Decision (EU) 2025/2371, four EUDAMED modules became mandatory from 28 May 2026 (Actors, UDI/Devices, Notified Bodies/Certificates, and Market Surveillance), while Italy keeps BD/RDM active for national registration until 27 November 2027. This dual-system period increases the need for parallel registrations, consistent UDI data, and vigilance reporting alignment for manufacturers selling CGM, SMBG, insulin delivery devices, and related disposables into regional tenders and NHS channels.

Value Chain Analysis

The value chain starts with global manufacturers supplying regulated diabetes monitoring (SMBG meters, strips, lancets, CGM sensors and durables) and management devices (pumps, infusion sets, reservoirs, pens, needles, syringes), supported by EU MDR compliance and Italian registration steps via the Ministry of Health BD/RDM. Market access is shaped by reimbursement classification and coding requirements, including CND classification for inclusion in reimbursed channels, and for combination products with ancillary medicinal substances by scientific consultation inputs involving AIFA as part of the Notified Body assessment.

Downstream, distribution is split between institutional purchasing for public facilities and retail dispensing via pharmacies. Centralized procurement bodies influence supplier selection and logistics cadence, and framework agreements (Accordo Quadro) can qualify multiple vendors under a regional procurement model before clinicians and diabetes centers guide patient-level device choice, training, and follow-up. Tender and HTA dynamics can disrupt supply continuity, and So.Re.Sa. Determination n.17 dated 19 January 2026 cited the annulment and resolution of insulin pump and CGM contracts for Campania and Molise following Consiglio di Stato judgment n.10015/2025, underscoring the need for resilient fulfillment networks, compliant substitutions within framework rules, and strong local service capability for complex devices.

Competitive Landscape

Competition is moderate, with global multinationals and select newcomers converging on integrated ecosystems. Abbott, Medtronic, and Dexcom jointly command more than 60% revenue through complementary sensor and pump portfolios. Their August 2024 interoperability pact merges Libre sensing with Medtronic dosing algorithms, aiming at the 11 million European intensive insulin users. Dexcom’s G7 sensor launch in February 2025 increases wear comfort, while its open API strategy lures Italian start-ups that build decision-support apps. Roche re-enters the sensor space with a July 2024 CE-marked CGM featuring improved lag time, positioning itself as a fourth major monitor supplier.

Insulet broadens the pump arena. Omnipod 5 debuted in January 2025 with dual CGM compatibility, drawing strong pharmacist interest because it ships without durable controllers. Tandem counters by rolling out Control-IQ software upgrades that raise Time-in-Range by 6 percentage points in interim Italian studies. Meanwhile, Senseonics partners with Ascensia to explore reimbursement for its 180-day implantable sensor, targeting needle-averse users.

Strategic M&A reshapes supply chains. Becton Dickinson spins off Embecta, which then signs a Mediterranean distribution deal with Italian wholesaler Comifar in March 2025, cementing pen-needle availability across 30,000 pharmacies. Ypsomed negotiates local production of its insulin pen caps to meet EU sustainability rules on single-use plastics. Start-ups face regulatory headwinds, yet those offering AI analytics such as GlucoMinds close seed rounds backed by hospital incubators in Milan and Naples. Collectively, these moves keep the Italy diabetes devices market on an innovation fast track.

Italy Diabetes Devices Industry Leaders

Abbott Diabetes Care

Roche Diabetes Care

LifeScan Inc.

Medtronic PLC

Dexcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrated in expanding beyond early-adopter cohorts into broader insulin-treated Type 2 populations and in higher-value device-plus-software pathways that match Italy's digital care buildout. Abbott cited Italy-generated clinical evidence at ATTD in March 2026 from an interventional study in adults with Type 2 diabetes on basal insulin using FreeStyle Libre, which supports wider discussion on CGM coverage and tender specifications that account for outcomes beyond Type 1 and pediatrics. Separately, the June 2024 expansion of pharmacy-run services (Farmacie dei Servizi) across approximately 19,000 community pharmacies creates additional touchpoints for onboarding, troubleshooting, and adherence reinforcement, which can be relevant where specialist appointment backlogs delay device initiation.

A second opportunity sits at the intersection of device ecosystems and national reimbursement governance for digital health. In May 2026, the Chamber of Deputies approved legislation to regulate digital therapies and connect them to the National Health Technology Assessment Program (PNHTA-DM) as a route toward reimbursement eligibility, increasing the value of CGM and pump platforms that fit secure data-sharing workflows and the Electronic Health Record (FSE). With procurement and access still managed largely by regions through tariffs and tenders, whitespace remains in harmonizing device availability across North-South funding gaps. Solutions that reduce training burden, such as simplified MDI smart systems and AI-supported decision tools, and that meet HTA evidence requirements can compete for inclusion at regional diabetes centers (Centri Diabetologici) and among purchasing bodies.

Recent Industry Developments

- April 2026: Roche Diagnostics Italy launched the Accu-Chek SmartGuide sensor in Italy, positioning predictive, AI-supported glucose insights as a differentiator within CGM-led monitoring ecosystems. The move increases competitive pressure on incumbent sensor platforms by emphasizing software-led value, which can affect tender requirements and clinician preference for integrated digital features.

- February 2025: Dexcom announced a shift from its distribution partnership model with Roche in Italy to a direct presence approach, including establishing a Milan office and local team. This commercial reconfiguration improves local coverage for diabetes centers and procurement stakeholders and supports faster execution on market access, training, and service for CGM adoption.

- June 2024: Italy implemented reforms that expanded the role of community pharmacies under Farmacie dei Servizi, enabling services such as capillary blood tests and chronic prescription renewals in local settings. This channel expansion increases access points for diabetes device initiation and follow-up, supporting higher-throughput dispensing and patient education outside hospital outpatient pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers diabetes devices sold and used in Italy for monitoring glucose and managing insulin delivery, including the device hardware and the recurring consumables that are needed for regular use. The value is measured in USD at manufacturer selling price levels, net of typical rebates.

Scope exclusions: We exclude veterinary use, general wellness wearables that are not intended for diabetes care, and refurbished or gray market imports.

Segmentation Overview

- By Device Type

- Management Devices

- Insulin Pump

- Insulin Pump Device

- Insulin Pump Reservoir

- Infusion Set

- Insulin Syringes

- Cartridges in Reusable Pens

- Insulin Disposable Pens

- Jet Injectors

- Insulin Pump

- Monitoring Devices

- Self-Monitoring Blood Glucose

- Glucometer Devices

- Blood Glucose Test Strips

- Lancets

- Continuous Glucose Monitoring

- Sensors

- Durables

- Self-Monitoring Blood Glucose

- Management Devices

- By End User

- Hospitals & Clinics

- Home-care Settings

- Specialized Diabetes Centers & Pharmacies

- By Patient Type

- Type-1 Diabetes

- Type-2 Diabetes

- Gestational & Other Specific Types

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on diabetes burden, treatment patterns, and how devices are funded and accessed in Italy. For this, we rely on public sources such as the Italian Ministry of Health publications, ISTAT health statistics, OECD Health data, and WHO and International Diabetes Federation country indicators.

To align the device side, we review sources such as European Commission and Eurostat trade series, public tender and procurement notices, and peer reviewed clinical and health economics papers that discuss adoption of CGM, SMBG testing frequency, and pump therapy. Company annual reports, investor decks, and press releases are used to validate product launch timing, reimbursement changes, and capacity signals. We also use a paid subscription selectively for company financials and patent and filing checks. These examples are illustrative, and many other public documents were also reviewed for data collection, clarification, and cross checks.

Primary Interviews and Surveys

Primary work focuses on Italy specific checks that desk sources cannot fully explain, such as how CGM uptake differs by patient group, how often consumables are actually used, and how procurement and reimbursement influence realized pricing. We speak with a mix of manufacturers, distributors, clinicians, hospital procurement teams, and pharmacy channel participants, and then we re-check assumptions with local experts before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | |

| Mid tier: 51% | Functional/Unit leaders: 40% | |

| Smaller Players: 21% | Managers: 44% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where diagnosed diabetes population, treated cohorts, and device penetration rates are combined to reconstruct annual demand, and then the value is converted using realistic price bands by device type. Results are then corroborated with selective bottom-up approximations, such as sampling unit volumes through channel checks, rolling up consumables per active user, and comparing implied revenues against supplier disclosures.

Key inputs that shape the totals include the split of patients on insulin therapy, CGM versus SMBG adoption, average testing frequency and sensor change cycles, pump penetration for intensive insulin users, and public reimbursement and tender dynamics that influence realized prices. When a bottom-up signal is incomplete, gaps are handled by using conservative ranges from interviews, followed by sensitivity checks so the final number does not rely on a single assumption.

For forecasts, we use scenario analysis supported by simple multivariate relationships between diabetes prevalence, reimbursement coverage, technology adoption trends (for example CGM share), and expected price normalization over time. Assumptions are kept easy to trace, so a client can see how each variable moves the market value year by year.

Data Validation & Update Cycle

Validation is done through multiple checks so the final outputs match real world signals. We compare market totals against independent indicators like diabetes population direction, import and shipment trends for relevant device classes, and procurement and reimbursement changes that can shift volumes or pricing.

If a variance looks unusual, the assumption is reopened and interview notes are revisited, and follow up calls are triggered when a change appears material. Before sign-off, the work is reviewed in steps by analysts who did not build the first draft, and the model is stress tested for currency timing, price erosion, and adoption pace. Reports are refreshed annually, with interim updates when major regulatory, reimbursement, or product events occur, and a final pre-delivery pass is completed so clients receive the latest view.

Mordor Intelligence's Italy Diabetes Devices Market Sizing Compared With Other Published Estimates

Published market sizes for Italy diabetes devices often do not match because the boundaries are drawn differently and the value build is not always done the same way. Differences usually come from whether recurring consumables are counted, how prices are treated after rebates, and which device categories are grouped together.

By tracking device penetration and consumables per active user and refreshing rebate and procurement assumptions, Mordor Intelligence keeps the Italy total tied to manufacturer level selling prices, which can shift the number versus estimates that lean on list prices or broader digital diabetes definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.17 B (2026) | |

| Industry Publisher A | USD 1.09 B (2023) | Uses an earlier base year and a longer horizon, and the category framing is broader under a general diabetes care devices label, which can blend pricing and adoption assumptions across device groups without explicitly netting rebates. |

| Databook Provider B | USD 0.42 B (2024) | Tracks a narrower digital diabetes management scope that includes smart connected solutions and apps, so it does not represent the full diabetes devices pool that includes traditional SMBG consumables and non-connected insulin delivery hardware. |

The spread in values is mainly explained by scope boundaries and price treatment, not by arithmetic errors. When the model is anchored to clear patient usage logic, realistic consumable cycles, and net pricing that reflects how devices are bought in Italy, the final market value becomes easier to reproduce and compare across years for planning.

Key Questions Answered in the Report

How big is the Italy Diabetes Devices Market?

The Italy Diabetes Devices Market size is expected to reach USD 1.17 billion in 2026 and grow at a CAGR of 6.61% to reach USD 1.61 billion by 2031.

Which device segment is expanding the fastest?

Management devices, including pumps and smart pens, are growing at a 6.98% CAGR due to launches such as Omnipod 5 and weekly insulin formulations.

Who are the key players in Italy Diabetes Devices Market?

Abbott Diabetes Care, Roche Diabetes Care, LifeScan Inc., Medtronic PLC and Dexcom Inc. are the major companies operating in the Italy Diabetes Devices Market.

What is driving homecare dominance?

Telemedicine platforms adopted by 72% of facilities, combined with pharmacy-based clinics and digital reimbursement, make at-home monitoring convenient for seniors and working adults.

Page last updated on: