Flexible Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

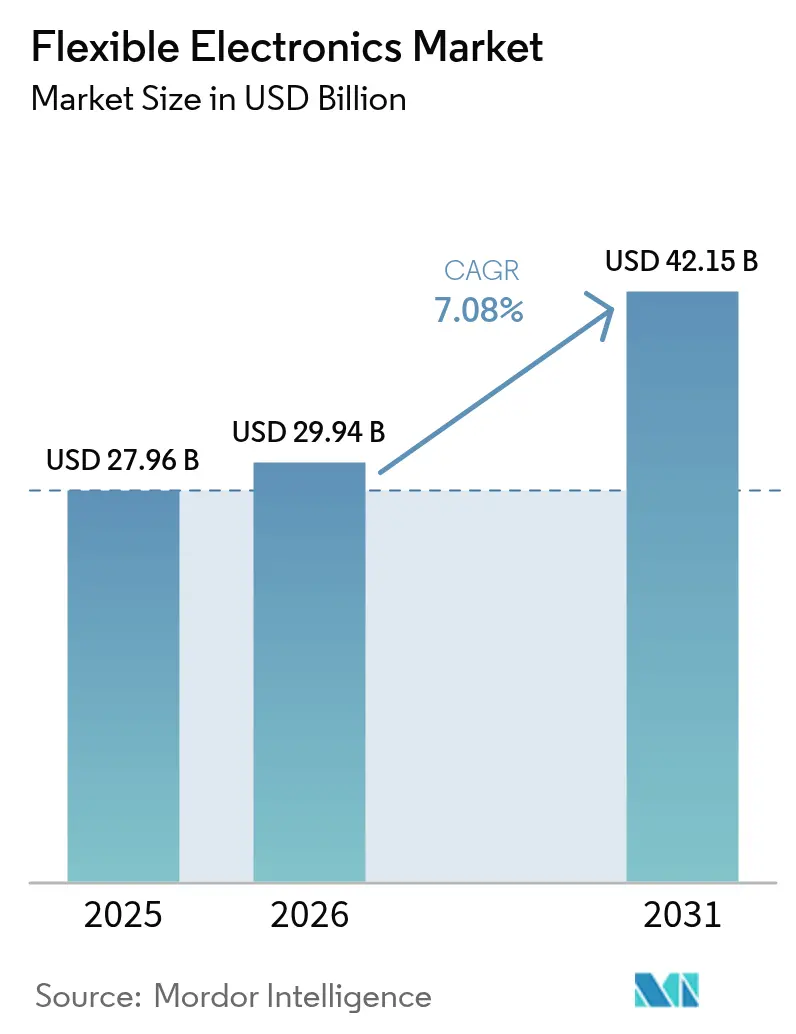

| Market Size (2026) | USD 29.94 Billion |

| Market Size (2031) | USD 42.15 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

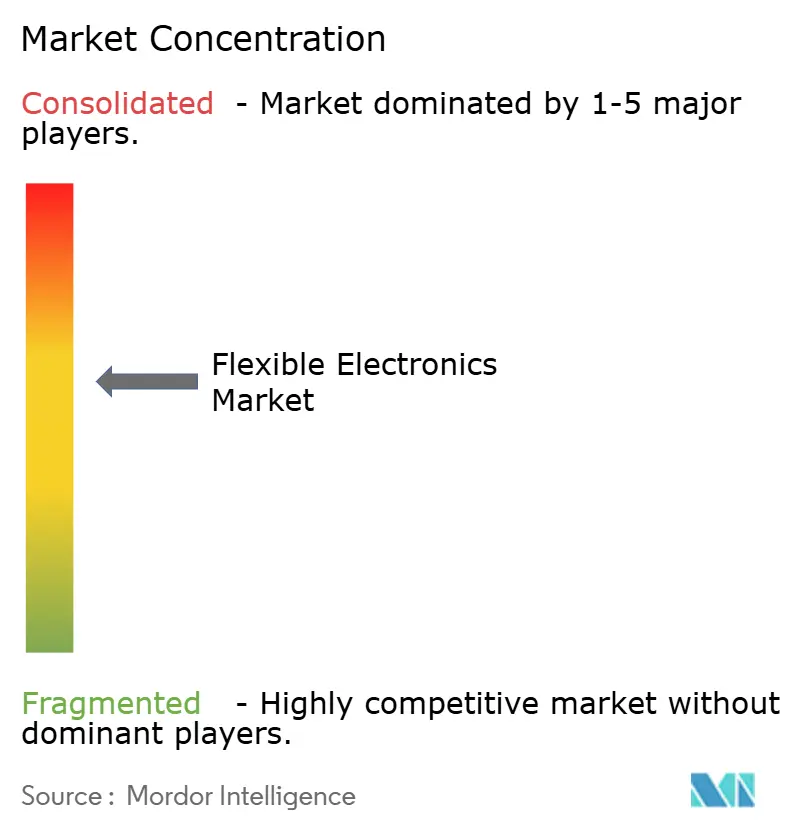

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Electronics Market Analysis by Mordor Intelligence

The flexible electronics market size in 2026 is estimated at USD 29.94 billion, growing from 2025 value of USD 27.96 billion with 2031 projections showing USD 42.15 billion, growing at 7.08% CAGR over 2026-2031. The expansion stems from a shift away from niche prototypes toward mainstream deployments in smartphones, automobiles, and healthcare wearables, supported by ultra-thin OLED stacks, conformal sensor breakthroughs, and roll-to-roll production economics that lower entry costs. Demand accelerates as curved automotive head-up displays (HUDs) reshape cockpit design, while North American healthcare systems validate continuous monitoring patches that rely on stretchable biosensors. Investments from BOE and Samsung in Gen-8.6 AMOLED and ultra-thin OLED lines, coupled with Middle East defense programs prioritizing lightweight conformal antennas, further elevate the flexible electronics market’s momentum. At the same time, supply-chain concentration in high-barrier encapsulation films and the absence of universal reliability standards for stretchable interconnects temper growth prospects by raising qualification hurdles and cost uncertainty.

Key Report Takeaways

- By component, flexible displays led with 54.12% of flexible electronics market share in 2025; flexible sensors post the fastest CAGR at 8.78% through 2031.

- By material, plastic substrates accounted for 61.10% share of the flexible electronics market size in 2025, whereas metal foils are projected to expand at an 8.11% CAGR between 2026-2031.

- By technology, printed electronics held 59.25% share of the flexible electronics market size in 2025, while organic electronics shows the highest 10.12% CAGR forecast to 2031.

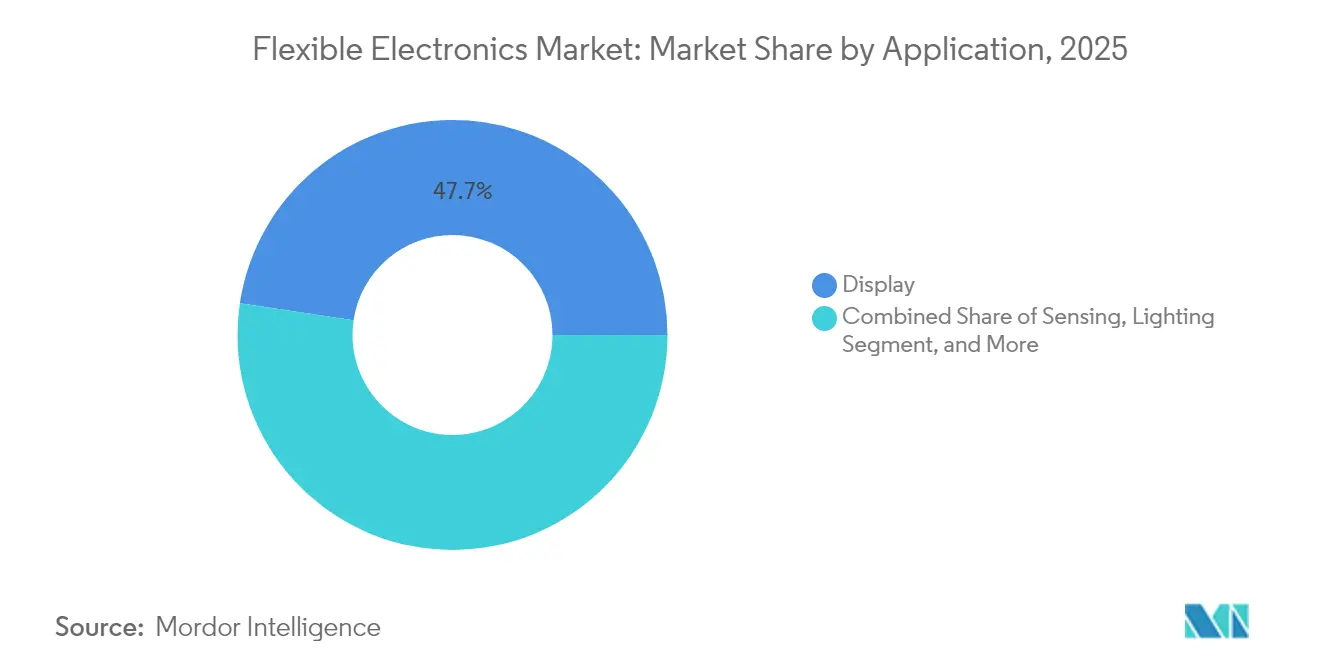

- By application, display solutions captured 47.65% share of the flexible electronics market size in 2025; sensing applications advance at a 7.22% CAGR to 2031.

- By end-user industry, consumer electronics led with 64.20% revenue share in 2025, yet healthcare devices are poised for a 13.18% CAGR through 2031 as regulatory approvals widen clinical use.

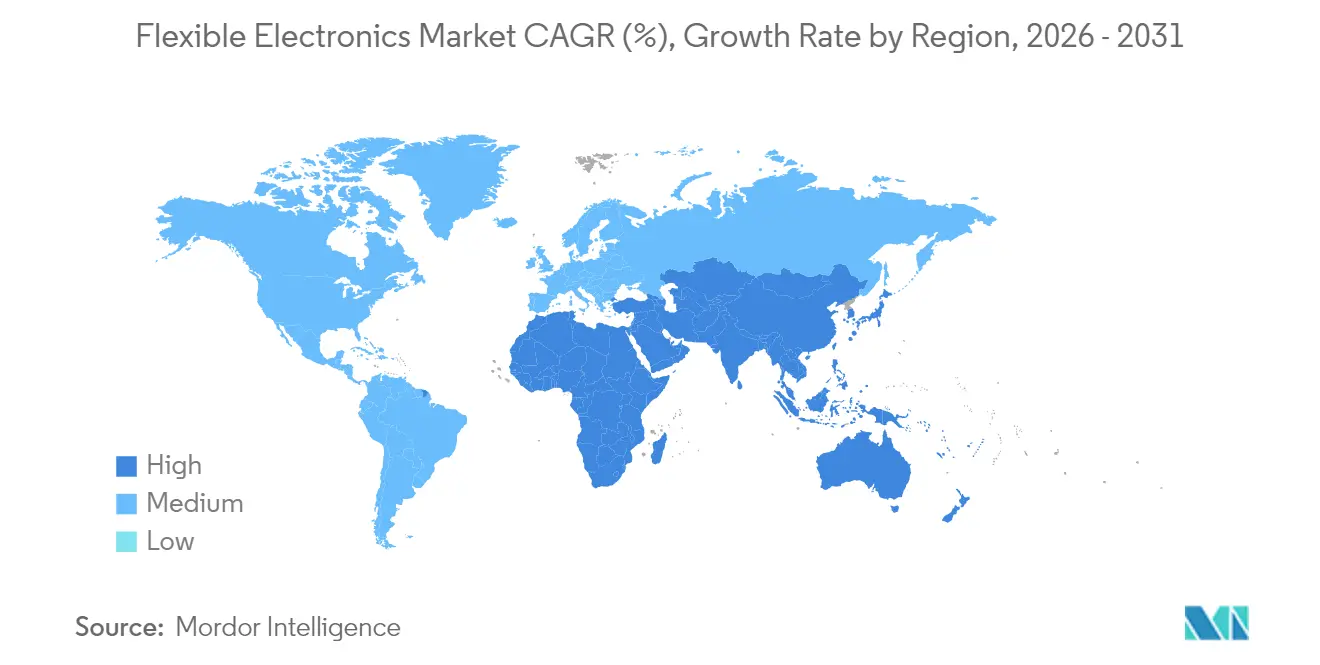

- by geography, Asia-Pacific dominated with 45.30% regional share in 2025; Middle East & Africa exhibits the fastest 11.05% CAGR outlook for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Improved durability of ultra-thin OLED stacks | +1.80% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Demand for conformal sensors in medical patches | +1.20% | North America, expanding to EU | Long term (≥ 4 years) |

| Automotive cockpit digitization with curved HUDs | +0.90% | Europe, spill-over to North America | Medium term (2-4 years) |

| Roll-to-roll cost reduction for printed ICs | +1.40% | Asia-Pacific core, global impact | Long term (≥ 4 years) |

| Defense need for lightweight conformal antennas | +0.70% | Middle East, global defense | Short term (≤ 2 years) |

| ESG push for flexible PV skins on buildings | +0.60% | Global, early EU/NA adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Improved durability of ultra-thin OLED stacks enabling foldable smartphones

Samsung Display’s Flex Magic Pixel demonstrator passed military-grade durability tests, eliminating visible creases and meeting user expectations for robust folding screens. Apple’s 2026 foldable iPhone order for 9-15 million 7.8-inch panels validates commercial readiness and signals mass adoption. Weight reductions of 30% and power savings of 30% in 2026 laptop panels widen the addressable device pool beyond phones. These advances resonate across the flexible electronics market as OEMs migrate tablets and laptops toward bendable formats, reinforcing supply-chain demand for high-barrier encapsulation and ultra-thin glass.

Demand for conformal sensors in wearable medical patches across North America

FDA clearance for X-trodes’ Smart Skin and UC San Diego’s 1,024-channel brain sensor array legitimizes flexible biosensors for continuous monitoring. Health-system reimbursement models pivot toward outcome-based care, favoring devices that capture longitudinal patient data. Flexible substrates reduce motion artifacts, maintaining signal integrity during everyday activities. Device makers tap organic electrochemical transistors for in-sensor computing, minimizing latency and protecting patient privacy. As reimbursement codes codify remote monitoring, the flexible electronics market benefits from recurrent sensor and patch replacements.

Automotive cockpit digitization driving curved HUD adoption in Europe

Zeiss and Hyundai Mobis target 2027 mass production of holographic windshield HUDs, integrating navigation overlays without obstructing driver vision. [1]Optics.org, “Zeiss, Hyundai Mobis hook up on holographic windshield displays,” optics.org AUO’s Smart Cockpit illustrates micro-LED surfaces across dashboards and sunroofs, merging ambient lighting with driver alerts. Infineon and Marelli’s MEMS laser beam scanning eliminates traditional display backplanes, shrinking package depth for curved instruments. European regulations emphasizing driver distraction mitigation push OEMs to adopt intuitive visual cues, boosting demand for bendable displays and integrated sensor layers.

Roll-to-roll manufacturing cost reduction in Asia for printed ICs

VTT’s Printocent Pilot Factory demonstrates continuous printing of fully recyclable ECG patches, merging biomaterials with silver nanowire inks. Scaling from lab to industrial lines extends calibration cycles yet drops unit cost once stabilized. China’s share of global OLED panel output rose to 53.4% in 2024 as local fabs ramped Gen-8.6 capacity, capturing orders from global smartphone brands. These economics anchor Asia-Pacific’s leadership in the flexible electronics market, enabling downstream device makers to launch lower-price foldable gadgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield Losses in Large-area Printing of Metallic Inks | -1.2% | Global, acute in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Limited Standardization of Stretchable Interconnect Reliability Tests | -0.8% | Global, acute in North America and EU | Medium term (2-4 years) |

| Supply-chain Concentration of High-barrier Encapsulation Films | -0.5% | Global, critical for Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Disposal and Recycling Complexities of Poly-imide Substrates | -0.3% | EU and North America regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited standardization of stretchable interconnect reliability tests

Rigid-electronics standards fail to capture simultaneous bending, twisting, and temperature cycling seen in wearable use. IEEE’s draft bladder-inflation method measures multi-axis stretch but remains voluntary, deterring automotive and medical OEMs that require certified lifetime data. Researchers propose polymer interlayer designs to curb substrate cracking under strain, yet without consensus metrics investors hesitate to fund high-volume tooling. The flexible electronics market thus faces slower design-win cycles until unified protocols emerge.

Yield Losses in Large-area Printing of Metallic Inks

Defects in metallic ink printing hinder flexible electronics by causing yield losses, especially in cost-sensitive applications like RFID tags and smart packaging. Achieving consistent ink properties at scale is challenging, as particle size and distribution affect conductivity. Transitioning to industrial-scale printing extends timelines due to recalibrations. While CuMOD inks reduce performance variations, ensuring uniform results across large areas remains difficult. A -1.2% CAGR reflects manufacturers' reluctance to scale production, limiting market growth until process reliability improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Displays Dominate While Sensors Accelerate

Flexible displays accounted for 54.12% of flexible electronics market share in 2025, powered by relentless foldable smartphone launches and curved automotive dashboards. Samsung’s 18.1-inch foldable prototype proves scalability into laptops, while LG’s stretchable micro-LED panel unlocks 3D surfaces in fashion and in-vehicle lighting. Complementing displays, the sensor category yields a 8.78% CAGR over 2026-2031 as hospitals adopt epidermal ECG and EEG patches for chronic care. Quantum-dot display-sensor hybrids that tolerate 1.5× stretching herald multifunctional surfaces that both show and sense data, positioning sensors as the next growth catalyst. Despite progress, flexible batteries and memory lag due to safety and yield hurdles, limiting fully integrated flexible systems today.

The flexible electronics market benefits from panel makers leveraging transparent OLED stacks to embed fingerprint and SpO₂ reading directly under the screen, condensing component count and thinning device profiles. Integrated biosensing displays open new monetization avenues for smartphone vendors seeking differentiation. Energy-harvesting films that convert vibration into micro-watts reduce battery load in wearables and industrial tags, though commercialization awaits stable supply of high-performance piezoelectric polymers. As cross-component synergies mature, device architects can design seamless form factors that merge visual, haptic, and sensing capabilities.

By Material: Plastic Substrates Lead Despite Metal Foil Innovation

Plastic substrates represented 61.10% of flexible electronics market size in 2025, driven by mature polyimide supply chains aligned with display fabs. Their thermal stability up to 400 °C pairs well with copper traces, minimizing delamination in automotive dashboards exposed to wide temperature swings. Metal foils, chiefly copper and stainless steel, post an 8.11% CAGR thanks to innate conductivity and EMI shielding valued in defense radios and high-speed data cables. Graphene-coated copper nanowires offer lower sheet resistance than indium-tin-oxide while retaining flexibility, attracting interest for roll-to-roll touch sensors.

Ultra-thin glass gains traction in premium foldable devices requiring pristine optics and scratch resistance. At just 30 µm, Corning’s latest glass can bend to 5 mm radius without fracture, albeit at a higher price point than polymer. Silver-nanowire ink advances, accelerated by DuPont’s 2024 C3Nano asset purchase, improve transparency and mechanical resilience for smart windows. Carbon-based conductive inks address ESG mandates by eliminating scarce indium and toxic solvents, appealing to builders of flexible photovoltaics integrated into façades. Material selection now balances cost, performance, and recyclability as regulators scrutinize electronic waste.

By Technology: Printed Electronics Foundation Enables Organic Innovation

Printed electronics held 59.25% of flexible electronics market size in 2025, the result of leveraging existing gravure and screen-printing equipment to mass-produce antennas, RFID tags, and basic sensor circuits. Inks formulated with silver flake or carbon nanotubes enable feature sizes adequate for NFC coils and moisture sensors. Organic electronics registers the highest 10.12% CAGR, propelled by breakthroughs in stretchable organic solar cells achieving 19% efficiency with tenfold elongation. Organic semiconductors’ low-temperature processing allows direct deposition onto textiles, expanding design freedom for apparel and medical garments.

Thin-film inorganic electronics defend niches requiring sub-10 nm channel lengths and extreme temperature resilience, such as aerospace radar phased-arrays. Hybrid stacks that co-print organic logic atop oxide TFT backplanes combine the drive current of inorganic layers with the flexibility of organics. Research into self-healing dielectric layers promises longer device lifetimes, addressing a key adoption hurdle. As printer line-width shrinks and registration accuracy improves, printed electronics will transition from simple identifiers to moderately complex logic, trimming BOM costs for disposable health sensors.

By Application: Display Applications Mature While Sensing Accelerates

Display applications captured 47.65% of flexible electronics market size in 2025, underscored by Samsung’s Sensor OLED prototype integrating biometric capture under the panel. Foldable phones and tablets employ hinge geometries previously impossible with rigid glass, while automotive interiors adopt pillar-to-pillar curved screens that merge cluster, infotainment, and passenger displays. Sensing applications grow at 7.22% CAGR as hospitals embrace wearable ultrasound and e-skin patches enabling at-home diagnostics previously bound to clinics. Continuous glucose monitoring moves from invasive probes to optical patches leveraging micro-LED emitters on pliable substrates

Lighting solutions leverage flexible OLED strips for uniform ambient glow along architectural contours, though adoption is limited by lifetime concerns. Energy harvesting films lining building façades generate supplemental power, advancing net-zero objectives in Europe’s retrofit market. RFID and smart labels remain stable, serving retail and logistics where unit cost trumps performance. The application mix indicates a pivot toward functionality as markets look beyond spectacle displays to problem-solving sensors and power skins.

By End-User Industry: Consumer Electronics Dominance Faces Healthcare Disruption

Consumer electronics retained 64.20% revenue share in 2025, fueled by record foldable smartphone shipments and tablet refreshes incorporating bendable hinges. Brands differentiate through screen continuity with minimal crease visibility, capturing premium price points. Yet healthcare devices outpace overall growth, posting a 13.18% CAGR by exploiting FDA pathways for remote diagnostics. Hospitals shift to outcome-based reimbursements that favor continuous patient data, encouraging adoption of disposable EEG caps and wound-healing sensors.

Automotive OEMs embed flexible displays in dashboards and headliners, pairing them with MEMS lidar modules conforming to vehicle curves. Defense contractors adopt antenna arrays printed on aerogel to cut weight in UAV airframes, while industrial IoT players use peel-and-stick vibration sensors for predictive maintenance. The University of Hong Kong’s in-sensor computing array shows how flexible devices can process data locally, shrinking latency and bandwidth needs. Cross-industry diffusion underscores the flexible electronics market’s maturation into a platform technology serving divergent requirements.

Geography Analysis

Asia-Pacific commanded 45.30% of flexible electronics market share in 2025, anchored by China’s manufacturing scale and Korea’s OLED innovation pipeline. BOE’s USD 9 billion Gen-8.6 AMOLED fab in Chengdu-the city’s largest single industrial investment-expands panel capacity for tablets and automotive cockpits. Korean institutes pushed piezoelectric harvester output 280×, underscoring regional leadership across displays, sensors, and energy devices. Japan contributes precision deposition tools and ultra-thin glass that support foldable handset reliability.

North America focuses on high-value healthcare and defense niches, leveraging FDA clearances for flexible biosensors and Pentagon funding for battlefield antenna arrays. Samsung’s USD 240 million Yokohama packaging R&D hub highlights cross-border collaboration, as Asian suppliers co-locate near U.S. system integrators. Silicon Valley startups pioneer flexible IC design automation, shortening tape-out cycles for printed logic that feeds disposable diagnostics.

Europe prioritizes automotive digitization and sustainability. German OEMs mandate holographic HUD integration by 2028, driving demand for bendable displays meeting stringent glare and impact standards. EU directives on building-integrated photovoltaics spur trials of façade-embedded flexible PV skins. Simultaneously, strict e-waste rules push recyclability, accelerating research into biodegradable substrates.

Middle East and Africa posts the highest 11.05% CAGR as defense modernization and smart-city programs embrace conformal electronics for weight-sensitive drones and harsh-climate sensors. Governments fast-track 5G and edge networks, creating pull for flexible antennas resistant to sand and heat. Regional universities partner with European labs on organic PV to power off-grid IoT nodes, broadening application diversity.

Value Chain Analysis

The value chain covers (1) materials and inputs such as polyimide films, ultra-thin glass, metal foils, encapsulation barriers, adhesives, and conductive inks; (2) device fabrication via TFT/OLED deposition and printed-electronics processes (screen, gravure, inkjet) across sheet-to-sheet and roll-to-roll (R2R) lines; (3) assembly and integration, including component attach and lamination onto thermally sensitive flexible substrates; and (4) system-level integration into end products across smartphones, automotive interiors, healthcare patches, smart labels, and building-integrated energy skins. Displays pull the highest-volume upstream demand, while growth in printed sensors, antennas, and smart labels raises requirements for inks, encapsulation films, and converting processes that can maintain registration and electrical performance under bend and stretch.

Bottlenecks show up in high-barrier encapsulation availability and in downstream manufacturing steps that do not transfer cleanly from rigid electronics, particularly high-speed pick-and-place and interconnect reliability validation under multi-axis strain. Recent supplier and manufacturing moves point to efforts to broaden input options and improve scale economics: Covestro partnered with Insulectro to expand access to advanced film materials and technical support for flexible electronics manufacturers, and Henkel partnered with Brilliant Matters to co-develop screen-printable silver inks targeted at higher-throughput organic photovoltaic (OPV) panel manufacturing. On the device side, FlexEnable began shipping a mass-produced consumer product using organic transistor technology (Ledger Stax), and Ynvisible partnered with CCL Design to scale production of printed e-paper displays, indicating a shift from pilot-stage prototypes toward repeatable manufacturing and distribution pathways.

Competitive Landscape

The flexible electronics market exhibits moderate concentration. Samsung Display, LG Display, and BOE Technology collectively deliver the majority of high-volume OLED panels, yet their combined share leaves room for nimble entrants. Samsung’s Dolby tie-up for automotive HDR displays exemplifies incumbents’ strategy to move up the value chain. BOE’s Apple LTPS OLED win demonstrates China’s closing technology gap, intensifying price competition.

Outside displays, the field fragments across components. PragmatIC Semiconductor secured USD 231 million to scale ultra-low-cost flexible ICs, threatening silicon for mass RFID. DuPont’s electronics spin-off and C3Nano nanowire asset purchase signal vertical integration among material suppliers. GE Aerospace’s Sensiworm aircraft-inspection device winning a FLEXI Award shows aerospace incumbents harnessing flexible hybrid electronics for maintenance automation.

Strategic moves include Infineon-Marelli MEMS scanning partnership to unlock curved cockpit architectures, and Flex’s Crown Technical Systems acquisition to bolster power distribution modules in data centers. Energy-harvesting breakthroughs from Korean labs foreshadow start-ups commercializing wearable power sources. Overall, alliances, acquisitions, and government-funded pilots shape competitive dynamics as players jostle for design wins across diverging verticals.

Flexible Electronics Industry Leaders

Samsung Display Co. Ltd

LG Display Co. Ltd

BOE Technology Group Co. Ltd

AU Optronics Corp.

E Ink Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Manufacturing and process innovations are creating whitespace for flexible electronics beyond foldables by easing patterning and lamination constraints that historically raised yield and unit-cost barriers. In Europe, DP Patterning started operations at a new Norrkoping facility with stated capacity of 10 million square metres of flexible electronics using Dry Phase Patterning, supporting local supply for large-area applications where chemical usage and process energy are scrutinized. At the same time, roadmapping is increasingly structured around integration and reliability: NextFlex released its 2025-2026 Public Roadmaps with focus areas including Device Integration and Packaging and Standards, Test and Reliability, and the OE-A published the 10th edition of its Roadmap for Flexible and Printed Electronics, reinforcing practical pathways from prototype builds to qualified production across multiple technology clusters.

On the product and end-market side, opportunities are growing where flexible form factors address integration constraints, especially automotive interiors and clinical-grade wearables that require conformal sensing. Scale-up in displays also widens device categories: BOE initiated mass production at a Gen-8.6 AMOLED facility in Chengdu with a reported total investment of 63 billion yuan, aligning with the market shift toward medium-sized IT panels and cockpit displays referenced in the report context. For higher-density flexible interconnects that enable more complex systems on polymer, American Semiconductor released its Ultraflex Cu-on-Polymer HDI substrate process, citing 1 micron copper features, which expands design options for compact sensor nodes and advanced packaging where rigid boards or coarse-feature flex are less practical. Together, these developments point to near-term opportunity in supply-chain localization (Europe and North America for materials and patterning), reliability and standards work that shortens qualification cycles, and higher-density flexible substrates that increase the amount of electronics that can fit onto bendable form factors.

Recent Industry Developments

- July 2026: American Semiconductor released the Ultraflex Cu-on-Polymer high-density interconnect flexible substrate manufacturing process, citing capability down to 1 micron copper features. The process expands feasible circuit density on polymer, supporting more complex flexible and hybrid electronic modules where traditional flex manufacturing feature sizes and yields become limiting.

- May 2025: NextFlex released its 2025-2026 Public Roadmaps focusing on Device Integration and Packaging and Standards, Test and Reliability. The update shows greater industry focus on bridging prototypes to qualified production and informs roadmap alignment across material, device, and packaging partners.

- September 2024: LG Display unveiled stretchable displays at Seoul Fashion Week, expanding public demonstrations of form-factor adaptability for non-flat surfaces. The milestone supports design-in activity for applications where rigid displays constrain industrial design, including apparel-adjacent wearables and interior surfaces that benefit from conformal lighting and display integration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the flexible electronics market covers electronic devices and components built on bendable, ultra-thin, or stretchable substrates that still operate reliably when flexed in real use. The scope includes functional circuits, sensors, batteries, and displays that are designed for flexible form factors.

Scope exclusions: It excludes conventional rigid electronics built on FR-4 boards or standard glass, as well as crystalline-silicon photovoltaic panels.

Segmentation Overview

- By Component

- Flexible Displays

- OLED

- E-Paper

- Others

- Flexible Sensors

- Biosensors

- Pressure Sensors

- Temperature Sensors

- Others

- Flexible Batteries

- Flexible Memory

- Flexible Photovoltaics

- Others

- Flexible Displays

- By Material

- Plastic Substrate

- Glass (Ultra-thin)

- Metal Foils

- Conductive Inks

- Dielectrics/Encapsulation

- By Technology

- Printed Electronics

- Organic Electronics

- Thin-Film Inorganic Electronics

- Hybrid Systems

- By Application

- Sensing

- Lighting

- Display

- Energy Harvesting

- RFID and Smart Labels

- Others

- By End-User Industry

- Consumer Electronics

- Automotive and Transportation

- Healthcare and Medical Devices

- Military and Defense

- Industrial and IoT

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean fact base using electronics output, trade flows, and adoption signals that link to flexible form factors. We referenced public sources such as the US International Trade Commission data releases, UN Comtrade, the World Bank macro series, and standards and documentation published through bodies such as IEEE.

To make the model practical, the desk phase also uses company annual reports, earnings decks, and product announcements to understand shipment direction and typical price movement for key device categories. Patent databases were used to track intensity of filings in printed electronics, flexible sensors, and flexible displays, which helps confirm when demand is broadening beyond pilot programs. The sources named here are illustrative, and other public references were also consulted for collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to convert desk signals into market-relevant inputs such as adoption timing, realistic pricing curves, and where flexible designs are chosen over rigid alternatives. We spoke with component suppliers, device makers, channel partners, and technical experts across major producing and consuming regions so gaps in secondary information could be closed with real operating context.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 44% |

| Mid tier: 52% | Functional/Unit leaders: 40% | EMEA: 30% |

| Smaller Players: 14% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where electronics demand pools are reconstructed from production, trade, and end-use adoption indicators, then translated into flexible electronics value using penetration assumptions. To keep totals grounded, outputs are cross-checked with selective bottom-up approximations such as sampled average selling price multiplied by plausible volumes for flexible displays, flexible printed circuits, and flexible sensors.

Key inputs that shape the model include shipments of wearables and foldable devices, display area demand trends, use rates of polyimide and other flexible substrates, progress in roll-to-roll manufacturing throughput, and observed price compression in key components. When a bottom-up check cannot be completed for a smaller niche, the gap is handled by using proxy device volumes and conservative attach rates, then reviewed during expert validation.

For forecasting, scenario analysis is used so the outlook stays explainable under different adoption and cost paths, and variables are adjusted using consensus ranges gathered from industry interviews. The final forecast is then smoothed to avoid step changes that are not supported by capacity, qualification timelines, or product-cycle reality.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including demand-side adoption indicators and supply-side capacity and materials movement. If a country or end-use value looks too high or too low against these checks, the assumptions are reopened and, when needed, respondents are re-contacted to confirm what changed.

Before sign-off, the model goes through multi-step analyst review, with variance checks across regions, price levels, and growth rates to catch outliers early. Reports are refreshed annually, and interim updates are made when major events occur that can move pricing, capacity, or end-market demand. Right before delivery, a final pass is completed so clients receive the latest updated view from the model and the newest public signals.

Mordor Intelligence's Flexible Electronics Market Size Compared Against Other Published Estimates

Published market values for flexible electronics often differ because each publisher draws the scope line differently and uses its own timing for price updates and currency conversion. Differences also come from how quickly analysts assume flexible designs replace rigid ones in mainstream devices.

Some published numbers fold in adjacent areas like broader printed electronics revenue and wider device categories that are not always flexible by design. In Mordor Intelligence's model, the value is counted only when the electronic function is delivered on a bendable or ultra-thin substrate, while rigid-board equivalents and crystalline-silicon PV are excluded from the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.94 B (2026) | |

| Global Publisher A | USD 38.08 B (2025) | Uses a different base year and a broader revenue pool that may include adjacent printed electronics categories and faster adoption assumptions, which can lift the near-term total versus a substrate-defined count. |

| Industry Publisher B | USD 32.10 B (2025) | Anchors the market in 2025 and applies a higher forward growth path, and it does not clearly state key exclusions, which can change what gets included when flexible and rigid variants coexist in the same device family. |

Looking at the three figures together, the spread is mainly explained by year selection and what gets treated as in-scope flexible revenue versus adjacent electronics value. By tying the total to observable device demand signals, realistic price movement, and clear inclusion rules, we keep the number traceable and repeatable when the market is re-checked.

Key Questions Answered in the Report

What is the current size of the flexible electronics market?

The flexible electronics market size stands at USD 29.94 billion in 2026, with projections reaching USD 42.15 billion by 2031.

Which component segment leads the market?

Flexible displays lead, holding 54.12% of flexible electronics market share in 2025 due to strong demand in foldable smartphones and automotive dashboards.

Which region is growing the fastest?

Middle East and Africa shows the fastest growth with an 11.05% CAGR forecast for 2026-2031, driven by defense modernization and smart-city projects.

Why are ultra-thin OLED stacks important?

Improved durability and reduced crease visibility from ultra-thin OLED stacks enable mainstream adoption of foldable phones and laptops, adding about 1.8 percentage points to the market’s CAGR.

How are healthcare applications impacting market growth?

FDA approvals for flexible biosensors support a 13.18% CAGR in healthcare devices, shifting monitoring from clinics to continuous wearable platforms and boosting sensor demand.

What challenges hinder wider adoption?

Lack of standardized reliability tests for stretchable interconnects and supply-chain concentration in high-barrier encapsulation films create cautious adoption cycles and cost volatility.

Page last updated on: