Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

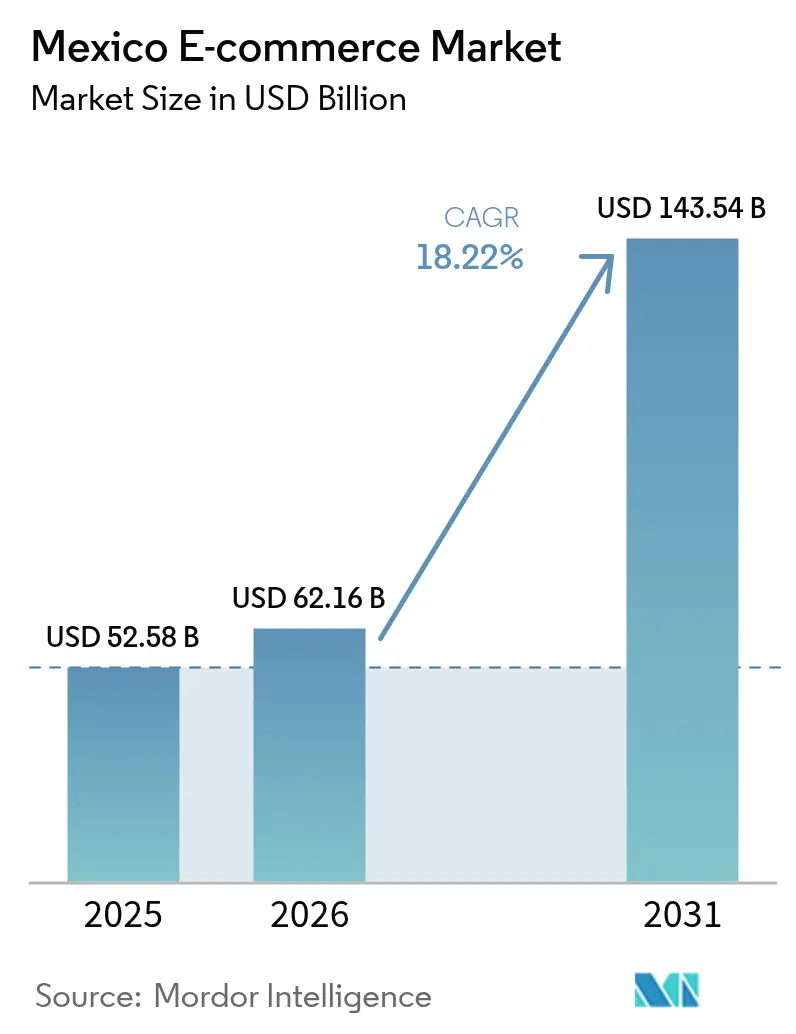

| Base Year Market Size (2025) | USD 52.58 Billion |

| Market Size (2026) | USD 62.16 Billion |

| Market Size (2031) | USD 143.54 Billion |

| Growth Rate (2026 - 2031) | 18.22% CAGR |

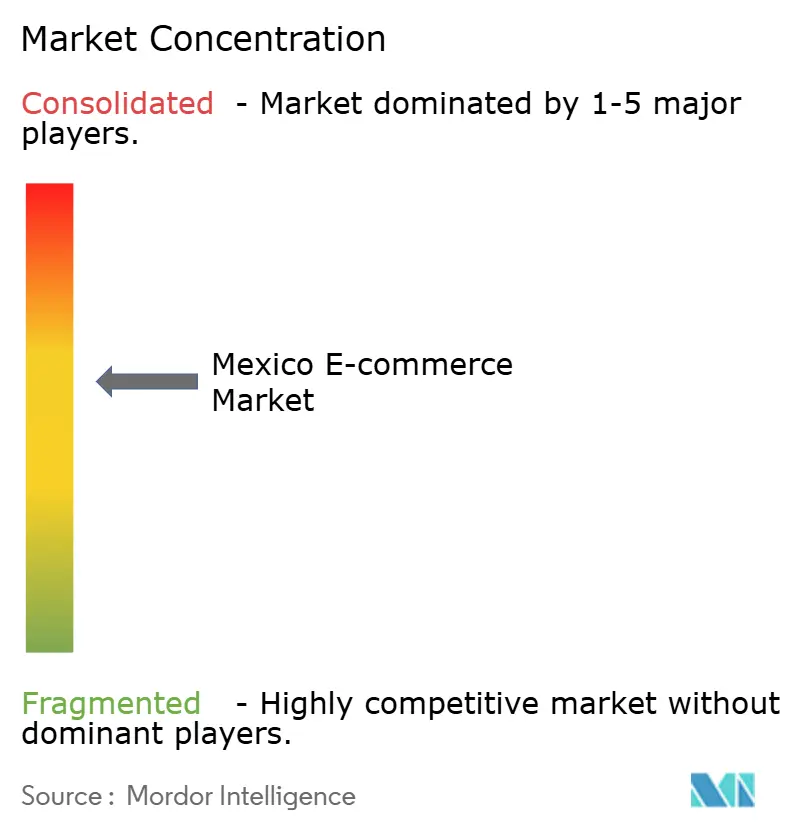

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico E-commerce Market Analysis by Mordor Intelligence

The Mexico e-commerce market size is expected to grow from USD 52.58 billion in 2025 to USD 62.16 billion in 2026 and is forecast to reach USD 143.54 billion by 2031 at 18.22% CAGR over 2026-2031. Mobile phones drove 78.5% of all online purchases in 2024, while internet access covered 83.1% of residents aged 6 or older, underscoring a digital society that increasingly shops from handheld devices.[1]INEGI, “ENDUTIH 2024 RR,” inegi.org.mx New 19% courier tariffs on imports from non-treaty nations reshaped the competitive field, adding compliance costs that primarily hit Chinese sellers. Deep-pocketed retailers responded with capital commitments: Walmart Mexico and Amazon each earmarked USD 6 billion for network expansion, warehousing, and last-mile coverage. Payments kept evolving as digital wallets advanced at a 21.1% CAGR, reflecting consumer appetite for friction-free checkout experiences even while cash still dominated 88% of transactions. In parallel, COFECE disclosed that two marketplaces controlled more than 85% of the vendor base and 61% of shoppers, signaling a concentrated environment with widening regulatory oversight.

Key Report Takeaways

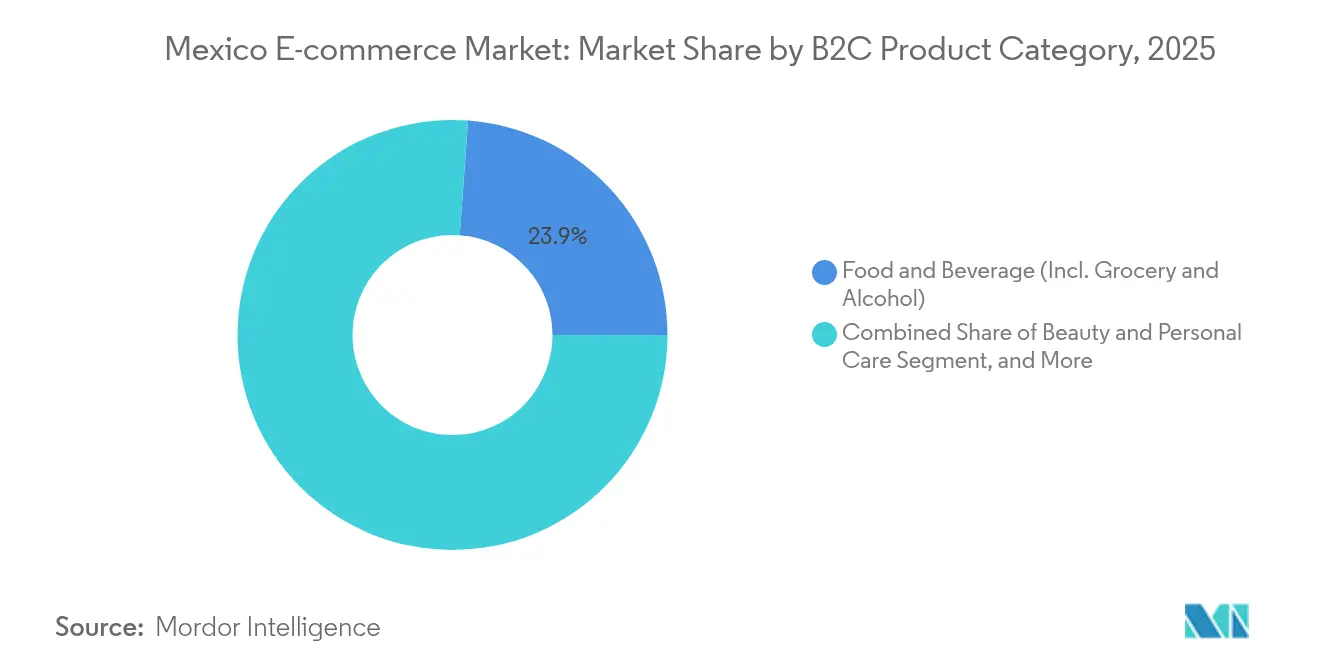

- By product category, Food and Beverage led with 23.85% revenue share in 2025, while Consumer Electronics is poised to grow at 19.45% CAGR through 2031.

- By payment method, credit and debit cards held 45.65% of the Mexico e-commerce market share in 2025, but digital wallets are forecast to expand at 20.65% CAGR over the same horizon.

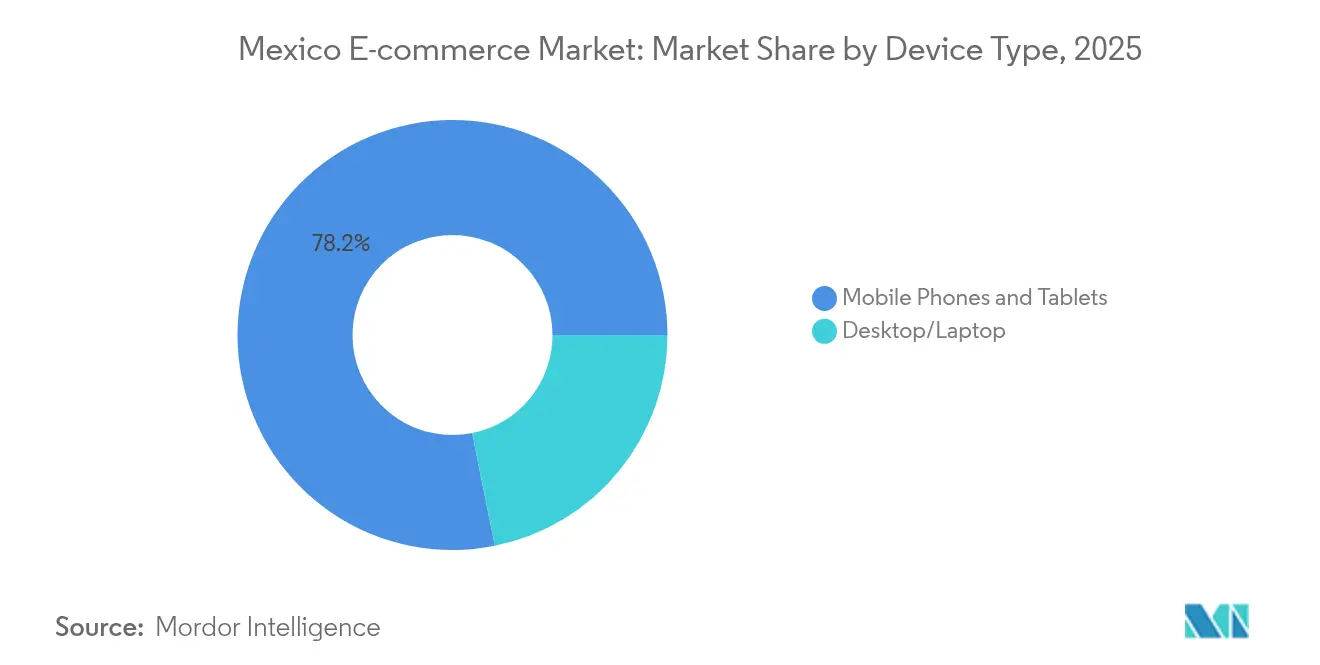

- By device type, mobile phones captured 78.15% of the Mexico e-commerce market share in 2025, advancing at 19.05% CAGR toward 2031.

- By B2B e-commerce, wholesale consumer goods accounted for 40.75% of the Mexico e-commerce market size in 2025, whereas office and IT equipment is projected to rise at 20.08% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of smartphones fuelling mobile commerce among Gen-Z and millennials | +4.2% | Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Increasing adoption of digital wallets and cards | +3.8% | Nationwide urban corridors | Medium term (2-4 years) |

| Acceptance of real-time payment platforms within SMEs | +2.9% | Commercial hubs | Medium term (2-4 years) |

| Omnichannel expansion into tier-2 and tier-3 cities | +2.1% | Puebla, León, Tijuana | Long term (≥ 4 years) |

| Enhanced financial inclusion | +3.4% | Rural and peri-urban areas | Long term (≥ 4 years) |

| Improved digital literacy | +1.8% | Rural localities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising penetration of smartphones fuelling mobile commerce among Gen-Z and millennials

Smartphones accounted for 97.2% of internet connections and powered 78.5% of purchases in 2024, propelling the Mexico e-commerce market toward a mobile-first model. Between 2018 and 2020, Mercado Libre recorded a 352% surge in toy orders placed from mobile devices, illustrating how youthful cohorts have made phones their default shopping channel. Performance gaps persisted; Monterrey clocked 55.17 Mbps 5G speeds while Mexico City lagged at 30 Mbps, shaping divergent user experiences across the Mexico e-commerce market. Fintech apps helped convert browsing into purchasing, evidenced by non-bank product users climbing past 70 million and projected to hit 86 million by 2027. Retailers reacted quickly: Liverpool said active mobile-app users rose 36.6% in 2022, and digital sales contribution increased 23.1% year on year, confirming mobile’s strategic value.

Increasing adoption of digital wallets and cards

Cashless transactions were forecast to jump 80% in 2025 and reach 1.9 trillion annual operations, accelerating the shift toward electronic checkout across the Mexico e-commerce market. MercadoPago launched cash deposit and withdrawal functionality at 20,000 shops to bring cash-first users into the digital loop. The country hosted more than 770 fintech startups in 2024, marking an 18.9% expansion and pushing new wallet experiences deeper into day-to-day commerce.[2]J.P. Morgan Payments, “LATAM’s Payments Landscape Is Evolving Quickly,” jpmorgan.com Partnerships became commonplace; Kueski teamed with BBVA to promote buy-now-pay-later (BNPL) to the 70% of adults lacking credit cards, directly enlarging the customer funnel in the Mexico e-commerce market. Meanwhile, the central bank’s SPEI platform secured mainstream status, used by 6 of every 10 citizens for real-time money movement.

Acceptance of real-time payment platforms within SMEs

SMEs adopting digital payments rose from 500,000 in 2014 to 5 million by 2023, reflecting how immediate settlement tools such as CoDi and SPEI have become indispensable. CoDi’s fee-free QR capability lowered costs and enabled smaller merchants to participate in the Mexico e-commerce market without heavy infrastructure spend. Aggregator terminals proliferated in low-income municipalities, with provider count climbing from 21 to 52 in less than a decade, signaling deeper financial inclusion. OXXO illustrated operational benefits after implementing Prisma’s SaaS data stack, cutting reconciliation costs throughout its 22,000 stores. Collectively, these changes have shortened cash-conversion cycles, raised checkout speed, and shrunk abandonment in the Mexico e-commerce market.

Omnichannel expansion into tier-2 and tier-3 cities

Retailers extended fulfillment networks beyond major metros by rolling out dark stores, pickup lockers, and lightweight distribution nodes in Puebla, León, and Tijuana, drawing fresh cohorts into the Mexico e-commerce market. Walmart Mexico opened 155 new outlets in 2024, mostly Bodega Aurrera banners that blend offline grocery with app-based ordering to reach value-oriented families. Starlink’s alliance with Mercado Libre offered satellite broadband kits costing MX 8,300 (USD 484.43) and monthly fees of MX 1,100 (USD 64.20), making last-mile connectivity viable in remote zones. IKEA’s second store in Guadalajara strengthened regional warehouse coverage, and an e-commerce hub in nearby Puebla was under construction to compress delivery windows. These initiatives have re-stacked logistics maps, allowed localized assortments, and deepened brand stickiness for Mexico e-commerce market leaders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cash-on-Delivery (COD) Dependence Elevating Return-to-Origin (RTO) Costs | -2.8% | National, concentrated in rural and low-income areas | Medium term (2-4 years) |

| High Parcel Theft Rates Along Federal Highways Raising Insurance Premiums | -1.9% | Federal highway corridors, interstate logistics routes | Short term (≤ 2 years) |

| COFECE Antitrust Probes Creating Marketplace Compliance Uncertainty | -1.5% | National, affecting major marketplace operators | Short term (≤ 2 years) |

| Limited Broadband Access in Rural Mexico Capping the Market Growth | -1.2% | Rural Mexico, southern and southeastern states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cash-on-delivery dependence elevating return-to-origin costs

Even in 2024, 88% of online sales were still paid in cash, causing high failure rates, reverse logistics, and added handling fees across the Mexico e-commerce market. Half of adults lacked bank accounts, and 70% had no credit cards, forcing merchants to maintain COD workflows that inflate last-mile risk. Complaints spiked when packages from Chinese platforms were mishandled by third-party carriers, triggering costly return-to-origin claims and friction for the Mexico e-commerce market. Walmart fought back by enabling in-store cash payments for digital baskets across 1,000 on-demand units and 1,400 pickup points, successfully migrating some shoppers into hybrid purchase journeys. Fintech workarounds such as OXXO Pay or MercadoPago cash kiosks provided incremental relief but still increased operating complexity for merchants.

High parcel theft rates along federal highways are raising insurance premiums

Retail theft—largely hijacked trucks and pilfered parcels—costs companies an estimated MX 10-14 billion (USD 580-812 million) per year, with spikes of up to 50% during peak seasons. Electronics and branded fashion ranked as prime targets, feeding informal street markets that siphoned revenue away from legitimate sellers in the Mexico e-commerce market. Carriers raised premiums, rerouted shipments, and invested in escort services, all of which lifted fulfillment costs and elongated delivery promise windows. Jalisco and Veracruz recorded disproportionate incidents, prompting merchants to deploy AI-based inventory tracking and tamper-evident packaging. While these systems improved traceability, they imposed fresh capital outlays that squeezed margins across the Mexico e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By B2C Product Category: Food drives digital grocery revolution

Food and Beverage held 23.85% of 2025 turnover, solidifying grocery’s primacy inside the Mexico e-commerce market, whereas Consumer Electronics targeted 19.45% CAGR from 2026-2031 on the back of manufacturing depth. With more than half of households preferring locally sourced items, online grocers ramped up inventory localization to cut spoilage and enhance freshness perception. Rappi morphed into a super-app, improving internal productivity 25% and onboarding times for restaurants, which kept its catalogue fluid and relevant. Beauty and Personal Care triggered 77.9% of online beauty orders, while household goods were next at 45.8%, cementing the Mexico e-commerce market as a primary channel for routine staples.

Consumer Electronics leveraged Mexico’s export-oriented factories; Liverpool’s digital revenue climbed 20.9% when it deepened electronics assortments, and Home Depot pledged USD 1.3 billion for omnichannel infrastructure that will reinforce large-ticket. Fashion wrestled with 35% import duties on finished apparel, forcing supply-chain pivots and dulling growth expectations. Furniture merchants such as GAIA Design bagged new funding to capitalize on nearshoring, targeting mid-upper consumers seeking rapid delivery. Altogether, shifting baskets and tariff structures demanded agile category management for any operator aiming to expand share within the Mexico e-commerce market.

By Payment Method: Digital wallets accelerate financial inclusion

Cards kept a 45.65% grip on online spending, yet digital wallets raced ahead with 20.65% CAGR, rewriting checkout scripts across the Mexico e-commerce market. Debit accounted for roughly 60% of card-based purchases, while BNPL posted 32% yearly growth as Kueski reached 20 million loans, doubling its book inside 18 months. Amazon embraced the trend, embedding Kueski Pay for installment plans up to 12 bi-weekly payments that bypass traditional credit checks. Cash vouchers redeemed at OXXO and 7-Eleven preserved a bridge between offline and online for the unbanked, while SPEI entrenched itself in B2B settlements.

Digital payment volume was projected to climb from USD 103.37 billion in 2023 to USD 167.85 billion by 2028, cementing electronic rails as the growth backbone for the Mexico e-commerce market. Openpay’s pact with Kueski furnished merchants with broader APIs, and MercadoPago integrated with BBVA for real-time credit scoring, smoothing authentication flows. Collectively, these shifts signaled a declining reliance on cash over the medium term.

By Device Type: Mobile dominance reshapes commerce architecture

Mobile phones and tablets retained 78.15% usage share in 2025 and logged the highest 19.05% CAGR, making responsive design non-negotiable for any Mexico e-commerce market entrant. Desktop remained relevant for high-ticket B2B contracts, yet traffic skew inevitably shifted to handheld screens at all hours. Speed disparities among cities put pressure on CDNs; Monterrey’s 55.17 Mbps 5G contrasted with Mexico City’s 30 Mbps, influencing bounce rates.

Liverpool’s mobile-centric revamp boosted active app users by 36.6% and lifted sales conversion by 20.9%, showing that UI refinements translate directly into revenue leverage. Gig-economy couriers broadened their remit from food to parcel drop-offs for AliExpress and Temu, further embedding smartphones as command centers for on-demand labor. Kueski debuted an offline-capable in-store scanning tool that accepted mobile transfers even without data coverage, helping retailers in connectivity-poor pockets maintain payment continuity.

By B2B E-commerce: Wholesale transformation drives industrial digitization

Wholesale consumer goods captured 40.75% of value, anchoring B2B activity inside the Mexico e-commerce market, while office and IT equipment outpaced with a 20.08% CAGR forecast to 2031. Proximity to US buyers under the USMCA and established production clusters elevated cross-border procurement. Supply-Chain Brain reported that 40% of exported content originated in the United States, dwarfing China’s 4%, which accelerated platform uptake by US distributors sourcing Mexican components.

Grainger scaled Spanish-language catalogues with 63,000 SKUs, while an enlarged Monterrey distribution node shortened lead times for northern factories. Finkargo’s Integra finance allowed importers up to 150 days to pay duties and VAT, slashing the administrative workload by 80% and appealing to mid-market traders. Automotive corridors lured China-based parts makers Minth, Sanhua, and FAWER, each erecting new plants to service Tesla’s forthcoming Gigafactory and the broader tier-1 ecosystem. This wave of industrial spending further legitimized digital procurement channels, driving the Mexico e-commerce market size for B2B higher over the outlook period.

Geography Analysis

Northern industrial states produced the highest online sales per capita, benefiting from 83.8% internet penetration and strong 5G coverage, whereas rural districts remained at 62.3%, generating an uneven digital topography across the Mexico e-commerce market. Monterrey, Tijuana, and other border hubs exploited nearshoring inflows and superior logistics to keep same-day promises viable. Central Mexico yielded the largest absolute GMV but battled slower network speeds of around 30 Mbps that pushed average load times past 2.4 seconds, a hurdle for conversion-driven categories such as fashion. The Bajío—Guadalajara, Querétaro, León—developed into a critical backbone for cloud, fintech, and transport platforms, with IKEA siting its second store in Guadalajara and plotting a Puebla e-commerce center to exploit cross-regional deliveries.

Tier-2 and tier-3 cities became battlegrounds for omnichannel growth; Walmart’s 155 new outlets in 2024 enlarged click-and-collect coverage that funnels rural cash consumers into the Mexico e-commerce market. Southern and southeastern states lagged on infrastructure, but public and private initiatives started to narrow the gap: Starlink–Mercado Libre kits reached remote villages, and community telecenters trialed fintech kiosks to drive inclusion. Ports such as Veracruz and Manzanillo formed strategic nodes, though high cargo theft rates required rerouting and extra security budgets, pressuring cost models for import-heavy merchants.

Regional investment clustered around logistics megaparks: Mercado Libre committed USD 300 million to new Hidalgo and State of Mexico distribution sites, adding 10,000 jobs and processing 400,000 parcels daily. Amazon’s warehouses in Nuevo León and Jalisco complement AWS’s USD 5 billion data campus in Querétaro, creating spill-over demand for last-mile contractors. These geographic bets collectively reinforced the Mexico e-commerce market as the region’s most contested logistics theater.

Competitive Landscape

Two marketplace ecosystems retained over 85% vendor coverage and 61% shopper penetration, signaling a concentrated Mexico e-commerce market that regulators flagged for corrective action.[4]Norton Rose Fulbright, “Lack of competitive conditions in marketplace,” nortonrosefulbright.com Mercado Libre leveraged integrated fintech through MercadoPago to anchor customer wallets, whereas Amazon optimized Prime perks and AWS synergies to strengthen retention. Chinese entrants Temu and Shein carved 40% share within specialty categories, often under-cutting local prices but now absorbing 19% tariff headwinds that could reshape cost advantage.

Strategic playbooks gravitated toward faster fulfillment. Mercado Libre hit 100 million annual buyers and a 28% Mexico GMV uptick by quadrupling distribution nodes and automating sortation. Walmart Mexico adopted Luminate, a proprietary analytics suite, granting suppliers on-shelf availability dashboards that enabled smarter replenishment. Coppel earmarked MX 14.2 billion (USD 690 million) to open 100 stores and overhaul its digital backbone, reflecting growing mid-tier competition.

Regulators proposed remedies such as neutral access to sponsored search, transparent algorithm guidelines and open logistics APIs to foster a more balanced Mexico e-commerce market. Players diversified revenue lines into fintech, streaming and third-party advertising, signaling that future differentiation will hinge on ecosystem depth rather than raw GMV. The battle now encompasses rural penetration, B2B verticals and branded manufacturing partnerships, areas still under-served despite headline scale.

Mexico E-commerce Industry Leaders

Amazon Mexico

Walmart de México y Centroamérica

Grupo Coppel

Costco de México

Mercado Libre Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mercado Libre posted Q4 2024 revenue of USD 6.1 billion (37% YoY) and net income of USD 639 million; Mexico gross merchandise value climbed 28% YoY, reflecting strong cross-border and domestic demand.

- January 2025: Mexico enforced 19% courier tariffs on imports from countries without trade treaties and 35% duties on finished apparel, tightening margins for Chinese sellers and prompting US brands to reroute inventory.

- January 2025: Walmart Mexico confirmed a USD 6 billion capex program for 2025 to build stores and supply-chain hubs, adding around 5,500 jobs.

- January 2025: Coppel announced a MX 14.2 billion (USD 690 million) plan to open 100 outlets and modernize e-commerce fulfillment.

Mexico E-commerce Market Report Scope

E-commerce is the purchasing and selling of products and services over the Internet. It is conducted over computers, mobiles, tablets, and other smart devices. There are primarily two e-commerce types: business-to-consumer (B2C) and business-to-business (B2B).

The Mexican e-commerce market is segmented by B2C e-commerce (beauty and personal care, consumer electronics, fashion and apparel, food and beverage, furniture and home, and others) and B2B e-commerce. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverage (Incl. Grocery and Alcohol) |

| Furniture and Home Décor |

| Toys, Baby and DIY |

| Books, Music and Stationery |

| Auto-parts and Industrial Tools |

By B2B E-commerce

| Industrial Supplies Marketplaces |

| Office and IT Equipment |

| Wholesale Consumer Goods |

By Device Type

| Mobile Phones and Tablets |

| Desktop/Laptop |

By Payment Method

| Credit and Debit Cards |

| Digital Wallets (PayPal, Mercado Pago, Apple Pay) |

| Cash Vouchers (Oxxo, 7-Eleven) |

| Bank Transfer (SPEI) |

| Buy Now Pay Later (Kueski Pay, Aplazo) |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverage (Incl. Grocery and Alcohol) | |

| Furniture and Home Décor | |

| Toys, Baby and DIY | |

| Books, Music and Stationery | |

| Auto-parts and Industrial Tools | |

| By B2B E-commerce | Industrial Supplies Marketplaces |

| Office and IT Equipment | |

| Wholesale Consumer Goods | |

| By Device Type | Mobile Phones and Tablets |

| Desktop/Laptop | |

| By Payment Method | Credit and Debit Cards |

| Digital Wallets (PayPal, Mercado Pago, Apple Pay) | |

| Cash Vouchers (Oxxo, 7-Eleven) | |

| Bank Transfer (SPEI) | |

| Buy Now Pay Later (Kueski Pay, Aplazo) |

Key Questions Answered in the Report

What is the current size of the Mexico e-commerce market?

The market was valued at USD 62.16 billion in 2026 and is forecast to climb to USD 143.54 billion by 2031 after growing at 18.22% annually.

Which product category leads online sales in Mexico?

Food and Beverage held the largest share at 23.85% of online revenue in 2025, supported by rapid digital grocery adoption.

How dominant is mobile shopping in Mexico?

Mobile devices drove 78.15% of all online transactions in 2025, and their share is projected to rise further as 5G coverage expands.

What payment method is growing fastest?

Digital wallets are advancing at a 20.65% CAGR, boosted by fintech partnerships and BNPL plans that reach consumers without credit cards.

How have new tariffs affected the competitive landscape?

Nineteen percent of courier duties and 35% apparel tariffs increased cost pressures on Chinese platforms, prompting fulfillment pivots and regulatory scrutiny of marketplace dominance.

Page last updated on: