Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

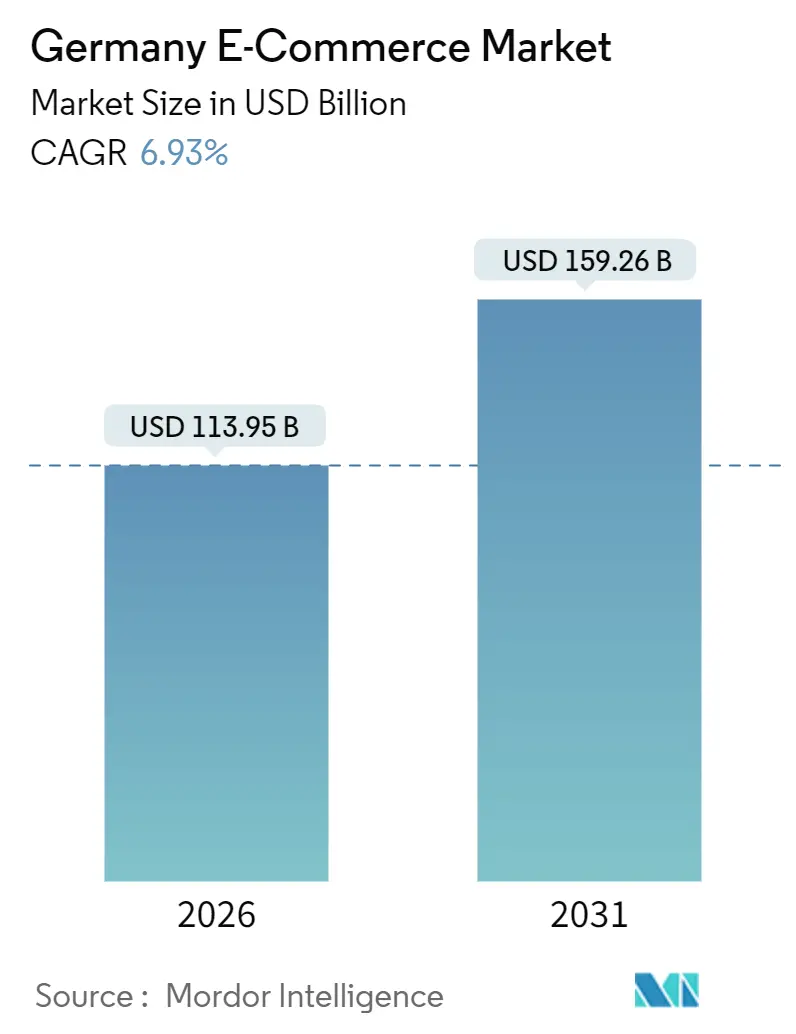

| Market Size (2026) | USD 113.95 Billion |

| Market Size (2031) | USD 159.26 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

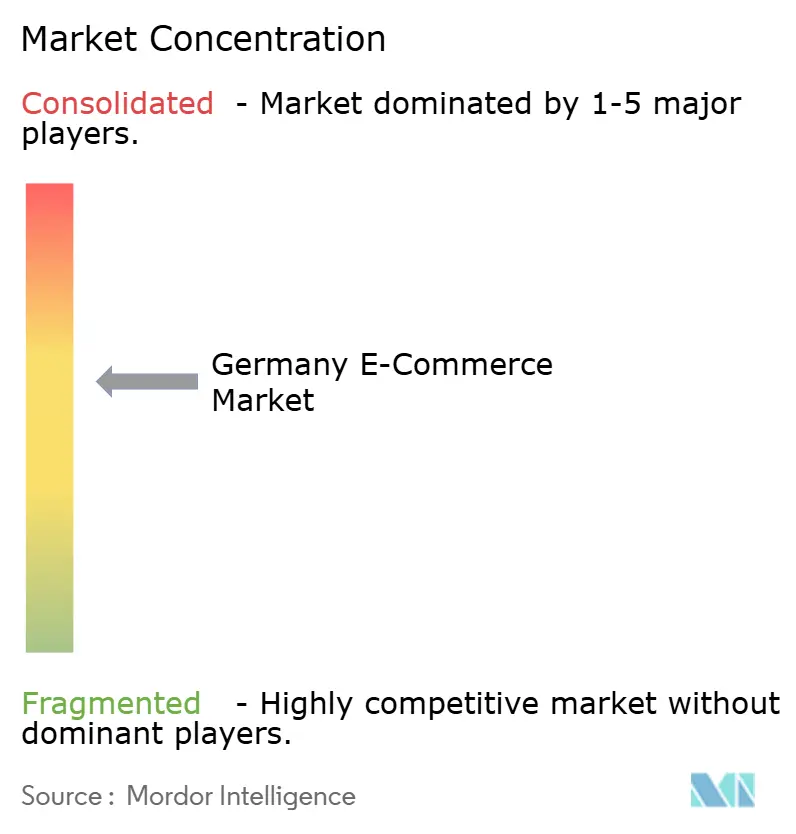

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany E-Commerce Market Analysis by Mordor Intelligence

The Germany e-commerce market size stood at USD 113.95 billion in 2026 and is projected to reach USD 159.26 billion by 2031, translating into a 6.93% CAGR for the period. Robust broadband penetration, instant-payment adoption, and a race toward faster fulfillment underpin steady expansion even as regulatory costs rise and discretionary spending moderates. Merchants are trimming checkout friction through biometric authentication and account-to-account payments, while rural fiber rollouts narrow the digital divide and unlock new postal codes for home delivery. Venture-backed quick-commerce adds urgency to same-day propositions, prompting supermarkets and marketplaces to retrofit real-estate into micro-fulfillment hubs. On the supply side, carbon-neutral shipping commitments accelerate fleet electrification, creating a capital-intensive moat that favors incumbents.

Key Report Takeaways

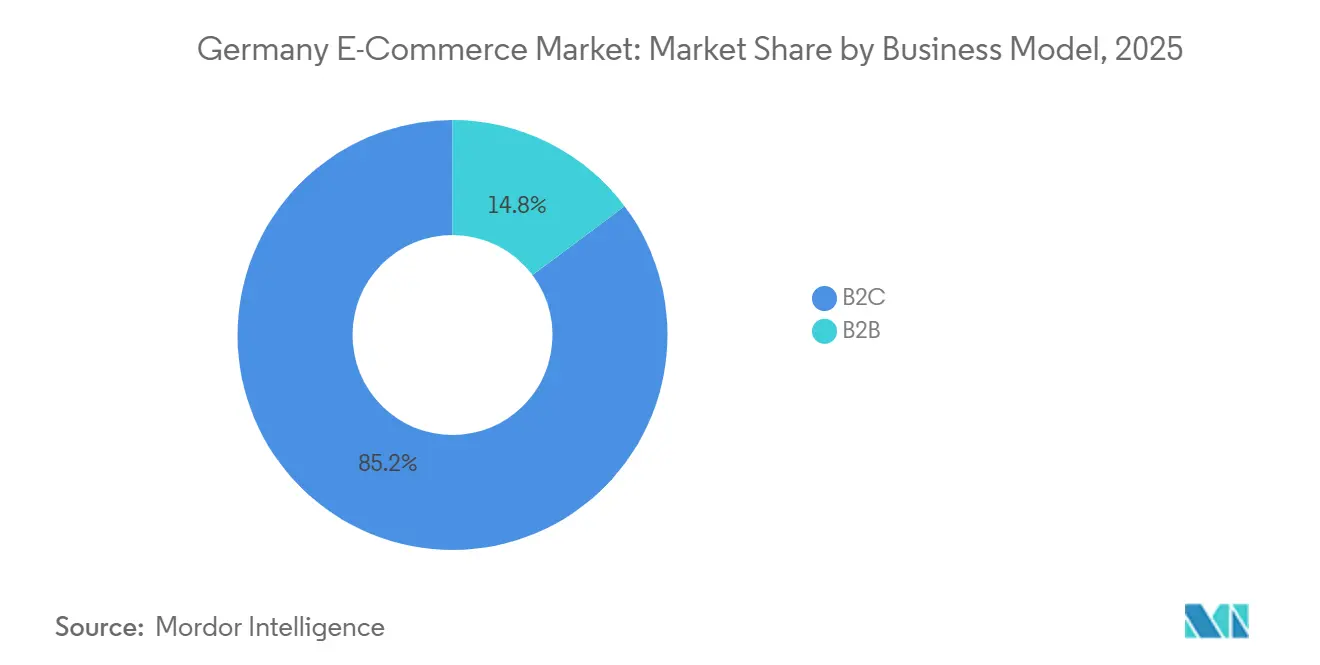

- By business model, business-to-consumer transactions held 85.23% of the Germany e-commerce market in 2025, while business-to-business e-procurement is advancing at a 9.24% CAGR to 2031.

- By device, smartphones captured 63.12% of the Germany e-commerce market in 2025, and mobile commerce is expanding at a 7.01% CAGR through 2031.

- By payment method, digital wallets accounted for 31.09% of the German e-commerce market in 2025, whereas buy-now-pay-later is rising at an annual 11.23% pace to 2031.

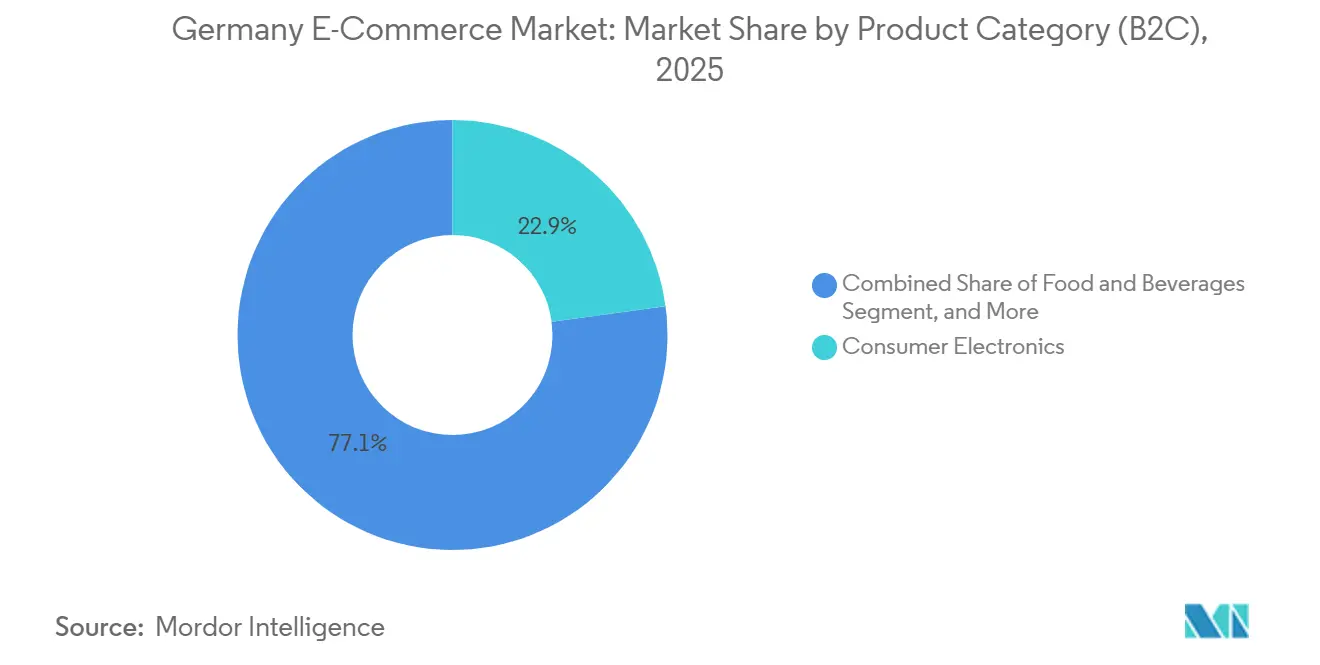

- By product category, consumer electronics led with 22.87% revenue share of the Germany e-commerce market in 2025, while food and beverages are forecast to grow at a 10.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany E-Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of SEPA-Friendly Payment Options Fuels Conversion Rates | +1.2% | Germany with spillover to Austria and Netherlands | Short term (≤ 2 years) |

| Rise of Quick-Commerce Start-ups Drives Same-Day Delivery Demand | +1.5% | Berlin, Munich, Hamburg | Short term (≤ 2 years) |

| Digitalization of Mittelstand Procurement Platforms | +1.1% | Baden-Württemberg, North Rhine-Westphalia | Long term (≥ 4 years) |

| Integration of AI-Powered Personalization Engines | +1.0% | Platform-led adoption nationwide | Short term (≤ 2 years) |

| Federal Gigabit Initiative Widens Rural High-Speed Coverage | +0.9% | Brandenburg, Mecklenburg-Vorpommern, Saxony | Medium term (2–4 years) |

| Sustainability-Driven Preference for Carbon-Neutral Shipping | +0.7% | Urban cores including Frankfurt, Cologne, Stuttgart | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Expansion of SEPA-Friendly Payment Options Fuels Conversion Rates

Universal coverage of SEPA instant payments in October 2025 removed the final clearance bottleneck in German checkout flows, delivering sub-10-second settlement and erasing foreign-exchange opacity for cross-border shoppers.[1]European Central Bank, “SEPA Instant Payment Adoption,” ecb.europa.eu Payment processors documented a 12% drop in cart abandonment for the 25-44 age cohort, while merchants saved 40-60 basis points per transaction compared with card rails. Small businesses now capture incremental margin that subsidizes free returns and loyalty vouchers. The rails also reinforce the cultural preference for direct debit, easing entry for regional sellers and lowering their dependence on global wallet providers. Strong customer-authentication rules embedded in PSD2 ensure biometric security without degrading user experience, keeping fraud below card-network averages.

Rise of Quick-Commerce Start-Ups Drives Same-Day Delivery Demand

Start-ups such as Flink and Gorillas secured EUR 890 million in 2024-2025 funding, deploying 340 micro-fulfillment centers clustered within 2 kilometers of dense neighborhoods. Consulting estimates indicate quick-commerce captured 6% of grocery spend in Germany’s ten largest metros by 2025. Order density above 12 drops per rider per hour keeps unit economics marginally positive, but limits viable expansion to affluent urban cores. Supermarket chains reacted by partnering with or acquiring these ventures to protect share, with REWE investing EUR 50 million to extend 10-minute delivery into 15 additional cities. While growth is explosive, profitability hinges on technology-driven routing and labor availability, making the segment sensitive to wage inflation.

Digitalization Of Mittelstand Procurement Platforms

Germany’s Lieferkettensorgfaltspflichtengesetz obliges mid-sized manufacturers to document human-rights due diligence, accelerating adoption of cloud e-procurement software that embeds compliance metadata. Transaction volume at Mercateo and Wucato jumped by 22% and 19% in 2025 as firms replaced email-based requisitions with API-linked catalogs. The business-to-business channel now shows a sustained 9.24% CAGR outlook, underpinned by average basket sizes above EUR 500 and lower price elasticity. However, interoperability gaps persist because 60% of Mittelstand companies still run on-premises ERP suites lacking modern API layers, forcing middleware integration and delaying full automation. Over the long term, mandated transparency acts as a structural tailwind that narrows the historic B2C-centric skew of the Germany e-commerce market.

Integration Of AI-Powered Personalization Engines Increases Basket Size

Retailers plugging machine-learning recommenders into storefronts recorded 14-19% uplifts in average order value in 2025.[2]Adobe, “AI-Powered Personalization in E-commerce,” adobe.com Zalando’s size-recommendation tool cut fashion returns by 11 percentage points, a major saving in a vertical where reverse logistics can exceed EUR 9 per item. Generative-AI styling assistants at About You lengthened session duration 23% and increased conversion 8%, proving that consultative experiences translate into measurable revenue. Dynamic-pricing modules further add 2-4 percentage-point margin, self-learning from competitor feeds and inventory velocity. The main hurdle is Germany’s strict GDPR enforcement that reduces behavioral-tracking consent rates by roughly 40% compared with markets like Spain, limiting available data for model training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Last-Mile Labor Shortages Amid Aging Workforce | -1.1% | Leipzig, Dortmund, national logistics hubs | Long term (≥ 4 years) |

| Compliance Costs of VerpackG and Recycling Mandates | -0.8% | Nationwide, acute for SMEs | Medium term (2–4 years) |

| Competition from Ultra-Low-Cost Cross-Border Marketplaces | -0.9% | Fashion and home-goods segments | Medium term (2–4 years) |

| Bundeskartellamt Scrutiny on Dominant Marketplaces | -0.5% | Berlin-based platforms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Last-Mile Labor Shortages Amid Aging Workforce Hinder The Market

Germany’s courier workforce contracted 7% year-over-year in 2025 as the under-35 labor pool shrank, compelling carriers to raise wages 11%. The shortage is acute in secondary cities where warehouse jobs with regular schedules lure drivers away. Autonomous sidewalk robots tested by DHL struggle to exceed 6 km/h and remain confined to pedestrian zones, limiting scalability. The labor squeeze delays same-day rollouts beyond metro cores and inflates delivery surcharges paid by rural consumers, nudging some shoppers back to click-and-collect. Proposed visa relaxations for non-EU logistics workers face political opposition, implying structural tightness through at least 2027.

Compliance Costs of VerpackG And Recycling Mandates Hinder The Market

Every seller shipping into Germany must register packaging volumes in the LUCID database and pay dual-system fees ranging from EUR 0.80-2.50 per kilogram, plus stiff fines for non-compliance. A 2025 survey showed that 38% of small online retailers incurred more than EUR 15,000 in unplanned legal and consulting costs, slicing 1.2-1.8 percentage points off operating margins.[3]Handelsblatt, “German E-commerce Market Developments,” handelsblatt.com Recycled-content mandates lifted material costs 12-18% as virgin plastics traded below recycled equivalents, squeezing packaging budgets. Cross-border sellers frequently skirt enforcement, leaving compliant domestic merchants at a cost disadvantage. Unless inspection capacity expands, the uneven playing field will persist and curb the competitiveness of local SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Digitalization Narrows The B2C Lead

The Germany e-commerce market size for business-to-consumer activity amounted to 85.23% of total value in 2025, validating the mature status of consumer platforms. Conversely, business-to-business channels are forecast to expand at a 9.24% CAGR, propelled by legally mandated supply-chain transparency that pushes Mittelstand firms toward cloud procurement. Industrial buyers appreciate higher basket values, often between EUR 500 and EUR 5,000, cushioning fulfillment costs. Marketplace operators leverage compliance modules that auto-populate certificates, turning regulation into a service differentiator. Yet, legacy on-premises ERP still dominates 60% of mid-market manufacturers, forcing temporary middleware bridges. Integration rollouts typically last 12-18 months, slowing immediate conversion but creating a multi-year runway for platform vendors. The convergence implies that B2B may command a markedly larger Germany e-commerce market share by the end of the decade without cannibalizing the consumer side.

B2C continues to add value through mobile-first design, influencer discovery, and subscription commerce, although its growth decelerates as urban penetration reaches saturation. Quick-commerce is cannibalizing supermarket foot traffic, spurring incumbents to embed dark stores into existing networks. Loyalty ecosystems that fuse streaming, payments, and logistics further deepen customer lock-in. Despite this, rising compliance and labor costs erode B2C margins, incentivizing diversification into higher-ticket verticals and cross-border sales. Over time, the dual-engine growth model stabilizes the Germany e-commerce market by balancing steady consumer volumes with faster-growing enterprise procurement.

By Device Type (B2C): Mobile Dominance Reshapes Checkout Flows

Smartphones accounted for 63.12% of B2C orders in 2025, and mobile purchasing volume is rising at a 7.01% CAGR. Progressive web apps remove the friction of native downloads, while biometric authentication trims checkout to a single tap. Retailers optimizing for 5G speeds report 9-percentage-point improvements in mobile conversion. Desktops remain preferred for complex, high-consideration purchases and for business procurement exchanges. Tablet share is marginal, servicing kiosk and couch-commerce use cases. Mobile average basket values trail desktop, at EUR 52 versus EUR 89, reflecting impulse behavior and screen constraints.

Mobile-centric UX delivers 40% higher session-to-purchase ratios thanks to auto-fill payment credentials and geo-triggered promotions. However, device fingerprinting becomes less reliable as privacy-savvy users clear cookies and rotate IP addresses, complicating fraud models. In the Germany e-commerce market, mitigation strategies include behavioral biometrics and carrier-level identity tokens. As 5G rollouts blanket rural districts, mobile will cement its lead, yet desktop retains a niche in enterprise workflows where multi-line orders and spreadsheet uploads demand larger screens.

By Payment Method (B2C): BNPL Gains As Wallets Plateau

Digital wallets processed 31.09% of 2025 transaction value, but their share is flattening as SEPA instant rails lower the relative advantage of stored-value intermediaries. Buy-now-pay-later volume is expanding at 11.23% annually, with Klarna, PayPal Pay Later, and Affirm handling EUR 4.2 billion in Germany last year. Typical BNPL ticket sizes range EUR 180-220 and skew toward fashion and electronics. Wallet incumbents respond by embedding installment features, while card networks push own-brand BNPL add-ons to defend interchange.

BaFin’s 2025 proposal to classify BNPL providers as credit institutions could elevate capital requirements and mandate affordability checks, tempering growth. Instant account-to-account transfers undermine wallet pricing power by saving merchants 40-60 basis points. For lower-margin categories like grocery, that delta can offset logistics inflation. In the Germany e-commerce market, payment diversification is thus reshaping checkout stacks, with merchants adopting orchestration layers that route by cost and approval probability.

By Product Category (B2C): Food Accelerates While Electronics Mature

Consumer electronics captured 22.87% of spend in 2025, underpinned by high smartphone-replacement cycles and lingering home-office demand. Yet growth is cooling as upgrade intervals stretch from 24 to 30 months. By contrast, food and beverages are forecast to expand at a 10.86% CAGR, riding subscription meal kits, algorithmic replenishment, and refrigerated micro-fulfillment. Cold-chain investment of EUR 320 million during 2024-2025 lowered per-order logistics to EUR 3.50-4.20 and boosted profitability above basket values of EUR 45.[4]Roland Berger, “Quick Commerce Market Analysis,” rolandberger.com

Fashion and beauty each claim double-digit shares and lean on AR try-on tools to cut returns. Ultra-low-cost Asian platforms erode domestic fashion margins by exploiting the EUR 150 de-minimis duty threshold. DIY and media remain niche but stable, and pharmaceuticals are constrained by prescription regulations. Over the forecast, the Germany e-commerce market size for food will narrow the gap with electronics as quick-commerce normalizes rapid grocery fulfillment and households shift routine baskets online.

Geography Analysis

Germany ranks first in absolute European e-commerce turnover but lags France and the United Kingdom in per-capita spend because cultural preferences still tilt toward in-store shopping. Cross-border trade contributed 18% of consumer purchases in 2025, enabled by EU VAT harmonization and shared logistics corridors. Fiber build-outs shrank the urban-rural bandwidth gap from 28 to 14 percentage points between 2023 and 2025. Rural conversion rates jumped 18% within six months of a fiber go-live as page-load times improved and video demos streamed without buffering. Nevertheless, Saxony still trails at 67% gigabit coverage, fragmenting national campaign reach.

Regulatory alignment through the Digital Services Act simplifies content compliance across borders, while strict GDPR enforcement limits behavioral tracking by requiring explicit consent, cutting the addressable audience by 40% relative to Spain. Germany’s supply-chain-due-diligence law advantages vertically integrated brands that already control tier-2 suppliers, putting pressure on marketplaces aggregating opaque inventories. SEPA instant payments reduce checkout abandonment for Dutch and Austrian shoppers and lower fees for merchants.

Pan-European fulfillment hubs in Leipzig, Dortmund, and Frankfurt process orders for Poland, Czech Republic, and Austria, reinforcing Germany’s role as a regional logistics nucleus. Yet ultra-cheap Asian marketplaces already capture 8% of domestic fashion and home-goods volume by exploiting duty loopholes. An EU proposal to scrap the de-minimis threshold in 2027 could restore parity, but customs inspection capacities remain a potential bottleneck.

Competitive Landscape

Amazon.de, Otto, and Zalando together hold roughly 40% of gross merchandise value, leaving a long tail of niche specialists and regional players that compete on curation, sustainability, or hyper-local delivery. Bundeskartellamt’s 2024 ban on self-preferencing forced platforms to unbundle logistics, enabling third-party networks to woo sellers with cheaper rural parcel rates. Zalando’s AI recommendation suite lifted basket sizes 19% and lowered returns 11 points, illustrating tech-led margin defense. Quick-commerce insurgents aggregate EUR 890 million in funding, yet their dependence on dense urban clusters leaves suburban markets open for supermarket hybrids.

Ultra-low-cost imports from Asia intensify price pressure, pushing domestic retailers toward service differentiation: same-day delivery, eco-packaging, and localized sourcing. Compliance costs under VerpackG and Lieferkettensorgfaltspflichtengesetz tilt the field toward capital-rich incumbents capable of absorbing documentation overhead. Industrial distributors see white-space in e-procurement, as 60% of Mittelstand firms still operate legacy systems. Platforms bundling catalog content with compliance reporting stand to consolidate share. Over time, AI-driven personalization, sustainability credentials, and payment optionality emerge as table stakes across the Germany e-commerce market.

Germany E-Commerce Industry Leaders

Amazon.de

eBay.de

eBay Kleinanzeigen

Idealo Internet GmbH

Otto GmbH and Co KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Amazon.de unveiled a EUR 1.2 billion expansion adding four fulfillment centers in Leipzig, Dortmund, Erfurt, and Magdeburg, targeting sub-24-hour delivery for 95% of postal codes and creating 3,500 jobs by 2027.

- November 2025: Zalando purchased a 25% stake in About You for EUR 280 million, enabling shared inventory pools and AI-based personalization across both fashion platforms.

- September 2025: Otto Group committed EUR 500 million to achieve net-zero logistics by 2030, deploying 1,200 electric vans and 300 cargo bikes and installing 450 fast-chargers at urban depots.

- July 2025: REWE Digital invested EUR 50 million to expand its partnership with Flink into 15 new cities, integrating micro-fulfillment with REWE’s supplier network.

- May 2025: MediaMarktSaturn merged its MediaMarkt and Saturn sites into a single e-commerce platform, spending EUR 120 million on cloud infrastructure and AI recommendations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the German e-commerce market as all business-to-consumer and business-to-business sales of physical goods and services that are ordered on a public internet site or app and paid through any electronic instrument.

Transactions fulfilled fully in virtual environments, pure in-app micro-payments, and peer-to-peer ticket resales are excluded.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type (B2C)

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method (B2C)

- Credit and Debit Cards

- Digital Wallets

- Buy Now Pay Later (BNPL)

- Other Payment Methods

- By Product Category (B2C)

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed parcel logistics executives, marketplace merchants, and mid-sized brand managers across Berlin, Hamburg, Munich, and two secondary cities. These conversations helped us verify conversion funnels, return rates, and the momentum of wallet-based checkouts, filling gaps that public data leave open.

Desk Research

We began with structured desk work that gathered baseline figures from tier-one public bodies such as the Federal Statistical Office, Bundesnetzagentur traffic reports, and the German Retail Association's Online Monitor. Eurostat trade tables, German customs shipment data, and ECB consumer payments surveys enriched our understanding of cross-border flows and preferred payment rails. Proprietary feeds from D&B Hoovers and Dow Jones Factiva were mined for retailer filings, funding rounds, and parcel carrier disclosures that sharpen average order value and unit-economics assumptions. This list is illustrative; many other open and subscription resources were tapped during validation.

Market-Sizing & Forecasting

We applied a top-down build that starts with national retail turnover, internet penetration, and average online spend per user, which are then adjusted for marketplace share, cross-border leakage, and B2B procurement digitalization. Select bottom-up checks, supplier roll-ups and sampled ASP × parcel volume, ground the totals. Key variables in the model include broadband household coverage, parcel density per capita, mobile share of sessions, digital wallet penetration, and inflation-adjusted basket values. Forecasts are generated through multivariate regression that blends these drivers and the expected policy push for Gigabit infrastructure. Where bottom-up clues were thin, gaps were smoothed using three-year moving averages aligned to primary research sentiment.

Data Validation & Update Cycle

Outputs pass anomaly scans and senior analyst peer review. Any variance wider than five percent versus independent indicators triggers re-checks. The model is refreshed each year, with interim revisions when material events, tax rule changes or major platform M&A, arise.

Why Our Germany E-commerce Baseline Is Dependable

Published estimates often diverge because firms pick different scope boundaries, currencies, or refresh cadences.

Key gap drivers include whether services like travel are folded into totals, how average selling prices are trended, and the cadence at which exchange rates are locked. Mordor's figures rest on a clear goods-only scope, annual FX rebasing, and an openly disclosed update rhythm, which together give decision-makers a dependable midpoint view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 106.23 B (2025) | Mordor Intelligence | |

| USD 100.60 B (2024) | Regional Consultancy A | Omits B2B transactions and applies prior-year FX |

| EUR 92.40 B (2025) | Industry Association B | Retail-only scope, excludes cross-border inflows |

| USD 64.30 B (2024) | Global Consultancy C | GMV limited to platform-to-consumer channel |

These comparisons show that our disciplined scoping and annual refresh cadence deliver a balanced baseline that is transparent, traceable to public variables, and repeatable for future updates.

Key Questions Answered in the Report

How large is online retail spending in Germany today?

The Germany e-commerce market size reached USD 113.95 billion in 2026 and is tracking a 6.93% CAGR toward USD 159.26 billion by 2031.

Which segment is growing fastest within German e-commerce?

Food and beverages lead on growth, expanding at a 10.86% CAGR thanks to quick-commerce groceries and subscription meal kits.

What share of German online sales already occur on mobile devices?

Smartphones generated 63.12% of B2C order volume in 2025, and mobile share is climbing by roughly 7% annually.

How dominant is Amazon in German online retail?

Amazon.de, together with Otto and Zalando, accounts for about 40% of gross merchandise value, indicating a moderately concentrated competitive field.

Why are buy-now-pay-later services under regulatory scrutiny?

BaFin has proposed classifying BNPL providers as credit institutions, which would impose capital and affordability rules that could slow their 11.23% annual growth trajectory.

What regulatory costs most impact German online merchants?

Compliance with the Verpackungsgesetz, requiring packaging registration and recycling fees, can subtract 1.2-1.8 percentage points from SME margins due to legal and material expenses.

Page last updated on: