Medical Robotic Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

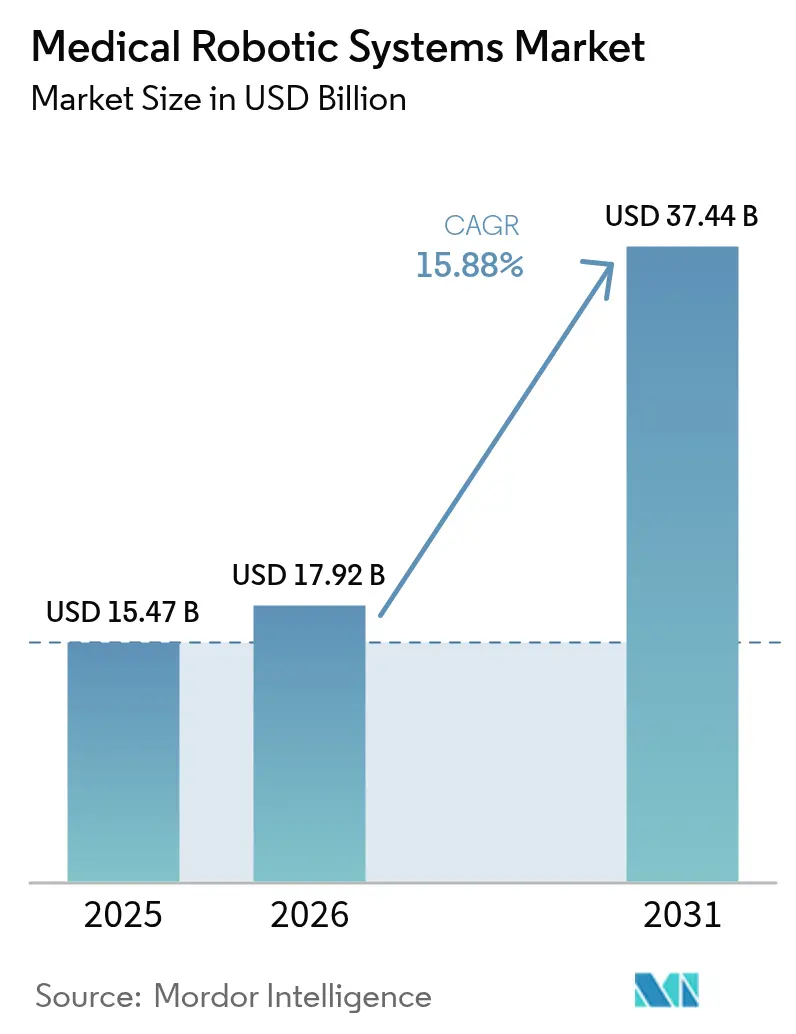

| Market Size (2026) | USD 17.92 Billion |

| Market Size (2031) | USD 37.44 Billion |

| Growth Rate (2026 - 2031) | 15.88% CAGR |

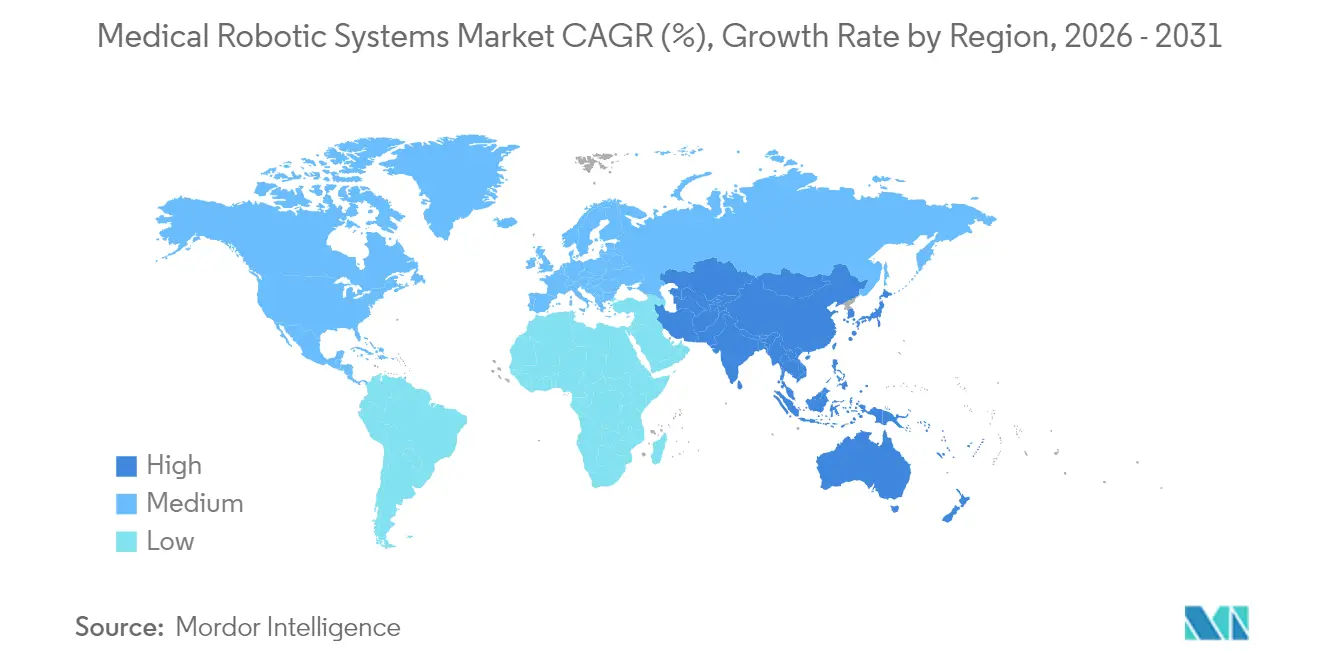

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Robotic Systems Market Analysis by Mordor Intelligence

The medical robotic systems market size is expected to grow from USD 15.47 billion in 2025 to USD 17.92 billion in 2026 and is forecast to reach USD 37.44 billion by 2031 at 15.88% CAGR over 2026-2031. Growing convergence between artificial intelligence and precision engineering, subscription-based financing that removes capital barriers, and regulatory policies that favor automated solutions are key accelerants. Procedure volumes are rising fastest in outpatient surgery centers across the United States and Europe, while China’s tier-3 hospitals deploy oncology-focused platforms to shorten cancer treatment queues. North America maintains its leadership through favorable reimbursement, while the Asia-Pacific region registers the steepest growth curve as government-sponsored rehabilitation programs expand access. Competitive positioning hinges on the installed base, clinical evidence, and the ability to wrap hardware in data-driven service contracts that secure recurring revenue.

Key Report Takeaways

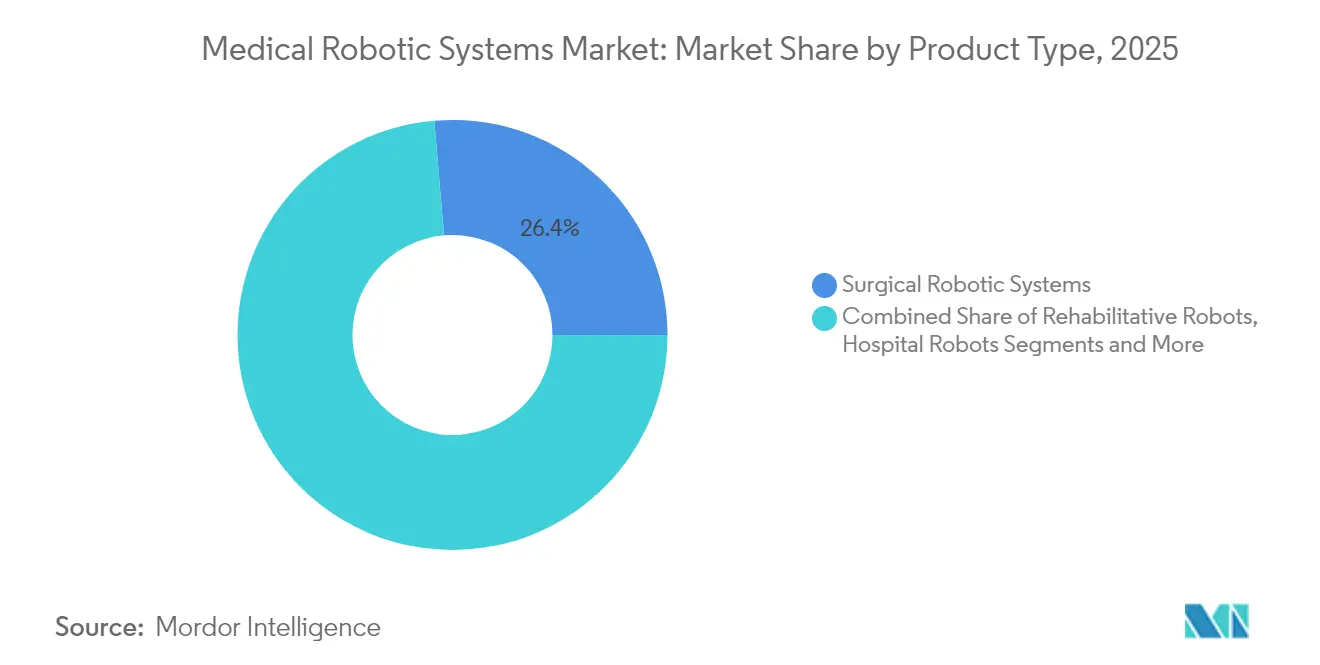

- By product type, surgical robotic systems led the medical robotic systems market with a 26.35% share in 2025; exoskeleton and rehabilitative robots are projected to expand at a 18.48% CAGR through 2031.

- By component, instruments and accessories commanded a 50.35% share of the medical robotic systems market size in 2025, while the services segment is projected to post the fastest 18.3% CAGR through 2031.

- By application, general surgery accounted for a 29.15% share of the medical robotic systems market size in 2025; however, neurology applications are expected to advance at a 18.1% CAGR through 2031.

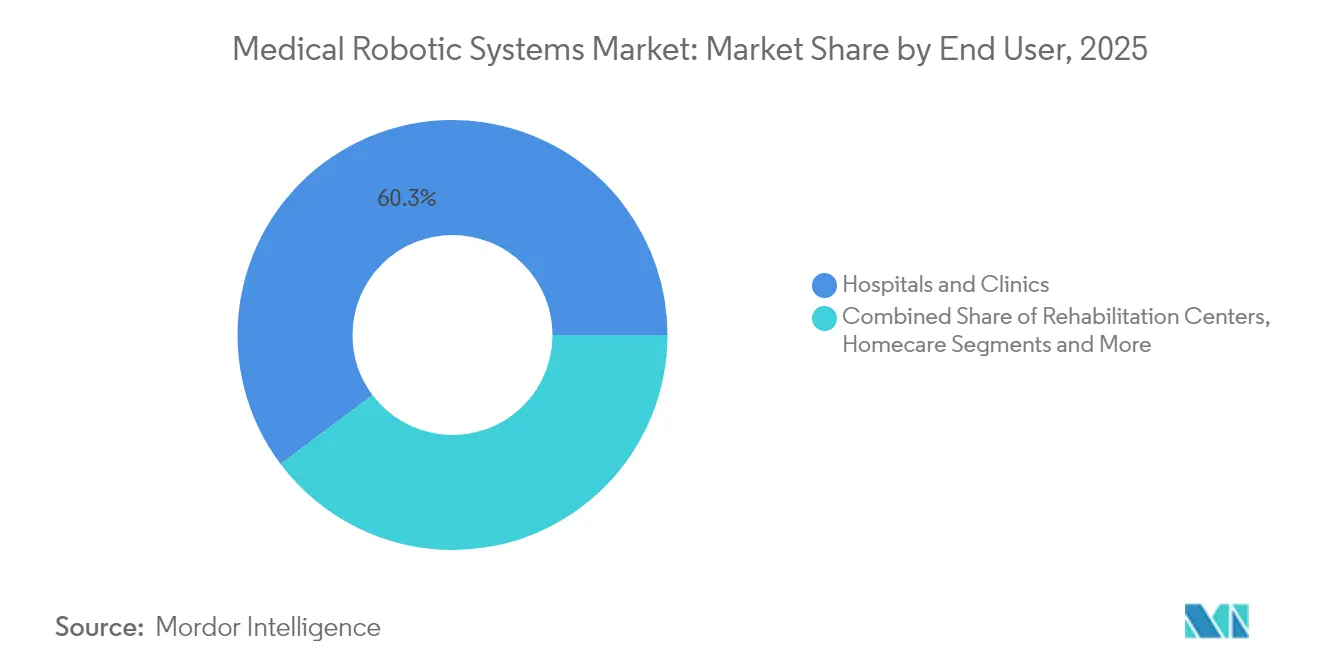

- By end user, hospitals and clinics held 60.25% of the medical robotic systems market share in 2025, whereas ambulatory surgery centers are expected to record the highest 18.05% CAGR through 2031.

- By region, North America is expected to hold a 35.45% revenue share in 2025, while the Asia-Pacific region is forecast to grow at a 17.6% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Robotic Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerating Adoption of Outpatient Robotic Surgery Centers in US and Europe | +2.8% | North America and Europe | Medium term (2-4 years) |

| Rapid Surge in Oncology-Focused Robotic Procedures in China's Tier-3 Hospitals | +2.1% | China, spill-over to Asia Pacific | Short term (≤ 2 years) |

| Mandatory Minimum-Volume Policies in Germany Pushing Hospitals toward Robotic Systems | +1.4% | Germany, expanding to European Union | Long term (≥ 4 years) |

| Emergence of Subscription and Leasing Business Models Reducing Up-front CAPEX | +3.2% | Global, early gains in emerging markets | Medium term (2-4 years) |

| Integration of AI-Powered Intra-operative Imaging Driving Precision Neurosurgery | +2.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Government-Sponsored Rehabilitation Robotics Programs Addressing Stroke Burden | +1.7% | Japan and South Korea, expanding to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Outpatient Robotic Surgery Centers in the United States & Europe

Ambulatory surgery facilities reduce procedure costs by 30-40% relative to inpatient settings while matching clinical outcomes, a differential that compels payers to steer appropriate cases into same-day pathways. Medicare’s payment updates for 2025 continue to expand the ASC-eligible list, and private insurers deploy bundled payments that reward high-throughput centers. European systems follow suit; Germany links hospital funding to procedure-volume thresholds, prompting regional networks to pool robotic assets to keep complex cases local.[1]Intuitive Surgical, “Intuitive Announces Fourth Quarter and Full Year 2024 Financial Results,” investor.intuitive.com

Rapid Surge in Oncology-Focused Robotic Procedures within China’s Tier-3 Hospitals

China’s National Health Commission increasingly references robot-assisted resection in its oncology protocols, spurring procurement among provincial referral centers that traditionally lacked capital budgets. Hospitals leverage robotics to recruit top surgeons from tier-1 cities and to standardize outcomes across sprawling networks. Domestic vendors enter with lower-priced systems, compressing acquisition costs and accelerating penetration beyond state targets.

Mandatory Minimum-Volume Policies in Germany Pushing Hospitals toward Robotic Systems for Complex Surgeries

In Germany, mandatory minimum-volume regulations are driving the surge in robotic systems for intricate surgeries. These regulations require hospitals to perform a specified number of specific surgeries, such as pancreatic and esophageal procedures, annually to maintain their accreditation. By enhancing surgical precision and reducing variability, robotic systems are enabling hospitals to meet these stringent requirements. As a result, hospitals are channeling investments into robotic platforms, not only to centralize specialized surgeries but also to attract and retain top-tier surgeons who favor advanced technology. Furthermore, these robotic systems are aiding multi-site hospital networks by standardising workflows and promoting collaborative surgical initiatives. In response, vendors are highlighting Germany as a pivotal market, introducing innovations such as multi-port, single-port, and imaging-integrated robotic systems. With an emphasis on meeting minimum procedural volumes, hospitals are ramping up robotic training, adopting AI-driven workflows, and enhancing documentation to ensure compliance. Moreover, Germany's regulatory stance is resonating with neighbouring EU nations, many of which are contemplating similar volume-based quality standards, solidifying Germany's role as a frontrunner in Europe's robotic surgery landscape.

Emergence of Subscription & Leasing Business Models Reducing Up-front CAPEX in Middle-Income Markets

Robotics-as-a-Service converts large capital purchases into predictable monthly fees that bundle hardware, instruments, maintenance, and training. Med One Group reports a 40% year-over-year increase in surgical-robot leases, a trend that is especially visible in Latin America and Southeast Asia, where hospital borrowing capacity is limited. Manufacturers gain steady annuity streams while hospitals align costs with utilization.[2]Med One Group, “Medical Equipment Leasing—Surgical Robotics,” medonegroup.comSubscription-based and leasing models are driving the surge in medical robot adoption, especially in middle-income markets. These models convert hefty capital expenditures (CAPEX) into manageable operational expenses (OPEX), making it easier for budget-conscious hospitals to embrace the technology. With options such as predictable monthly payments, pay-per-use, and bundled packages (covering services, consumables, and training), hospitals can expand their robotics programs without the delays associated with lengthy capital-approval processes. Leasing not only provides access to cutting-edge robotic innovations but also sidesteps concerns of depreciation and obsolescence.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Back-log of Post-Warranty Service Costs Deterring Smaller Hospitals | -1.8% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Data-Protection Regulations Limiting Cloud-Connected Robot Analytics | -1.2% | Europe & North America, expanding globally | Long term (≥ 4 years) |

| Shortage of Certified Robotic Surgeons in Latin America Slowing Utilization Rates | -0.9% | Latin America, spill-over to emerging markets | Long term (≥ 4 years) |

| Stringent FDA Cybersecurity Draft Guidance Elevating Compliance Costs for New Entrants | -1.1% | Global, concentrated in US market entry | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Back-log of Post-Warranty Service Costs Deterring Smaller Hospitals

As post-warranty service expenses surge, the medical robots market faces a significant challenge, particularly affecting smaller hospitals. Typically, annual service fees for robotic surgical systems range between 12% and 18% of the system's original cost. This recurring financial burden proves unsustainable for many mid- and low-volume facilities. Consequently, rural and Tier-2 hospitals are experiencing a growing backlog of deferred maintenance, resulting in increased downtime and diminished returns on their robotics investments. The situation is exacerbated by limited access to competitive third-party servicing, inflationary pressures on biomedical services, and sluggish response times from original equipment manufacturers (OEMs). These challenges have prompted some hospitals to adopt a reactive maintenance approach rather than a preventive one. Such a backlog can result in reliance on outdated software, compromised operational safety, and limited surgical options. Without in-house biomedical engineers, smaller hospitals often find themselves heavily reliant on costly OEM technicians, which intensifies their financial challenges. This mounting service backlog not only heightens medico-legal risks but also increases the likelihood of cancelled robotic procedures and hinders the adoption of emerging technologies, such as AI-guided navigation. The repercussions are most pronounced in regions such as Southeast Asia, Eastern Europe, and Latin America, where hospitals operate on thin margins and surgical volumes fall short of justifying the steep service costs.

Data-Protection Regulations (GDPR/HIPAA) Limiting Cloud-Connected Robot Analytics

In Europe, strict data-protection laws, such as GDPR, and HIPAA in the U.S., are increasingly stifling the growth of cloud-connected robotic analytics. Modern medical robots, which rely on cloud processing for tasks such as algorithm training, predictive maintenance, and intraoperative video insights, are facing challenges. The cross-border transfer of surgical data is mired in compliance hurdles. Even anonymised metadata is often classified as high-sensitivity health information. As a result, hospitals face regulatory risks, lengthy approval cycles, and administrative challenges related to BAAs, cybersecurity certifications, and data anonymization. These challenges have prompted many facilities to either turn off connected features or shift to on-premise analytics, thereby compromising the sophistication and accuracy of their predictive models. The restricted sharing of diverse datasets across institutions hampers AI development, slows algorithm refinement, and diminishes benchmarking quality across global installations. Additionally, cloud-edge fusion models encounter challenges due to dual-processing risks, and encrypted real-time streaming can hinder the effectiveness of surgical collaboration tools. Ultimately, these compliance-driven challenges inflate vendor costs, delay product deployment, and limit access to advanced cloud-based robotics, curbing the growth of AI-enhanced surgical robot ecosystems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surgical Dominance Amid Rehabilitation Upswing

Surgical systems retained a 26.35% share of the medical robotic systems market in 2025, buoyed by mature reimbursement codes and extensive training pipelines among surgeons. Utilization spans urology, gynecology, general, and orthopedic procedures, with cumulative da Vinci case volumes surpassing 15 million globally. Oncology applications in radiosurgery, led by platforms such as CyberKnife, demonstrate a 89.3% local tumor control rate, reinforcing clinical acceptance.

Rehabilitative solutions trail in revenue but are scaling quickly on the back of publicly funded stroke programs. Exoskeleton sessions deliver higher therapy intensity, and early health-economic studies show 15% faster functional recovery versus conventional physiotherapy. Combined, these factors push rehabilitation robotics to an 18.48% CAGR, the fastest within the medical robotic systems market.

By Component: Services Propel Recurring Revenue

Consumable instruments and accessories accounted for 50.35% of the medical robotic systems market share in 2025, as every procedure requires single-use items such as staplers, trocars, and energy tips. High-throughput hospitals average seven robotic cases per console per day, a cadence that secures double-digit margins for vendors even after bulk-pricing concessions. To entrench loyalty, suppliers introduce smart inventory cabinets that automatically replenish disposables and book charges directly to patient dossiers, thereby trimming nursing time by 12 minutes per case.

Services, spanning lease, warranty, software, and training, scale even faster at an 18.3% CAGR, as providers favor operating-expense models over capital lock-in. Multi-year “system-as-a-service” packages now bundle unlimited instruments, predictive maintenance, and quarterly software updates that enhance AI guidance without requiring new hardware. Hospitals, such as the University of California health network, report a 2% higher uptime and 9% quicker credentialing of new surgeons after migrating to subscription portals that host virtual reality (VR) rehearsal modules. Vendors increasingly tie fee levels to case volumes, aligning economics with utilization and making renewals almost frictionless.

By Application: Neurology Emerges as Growth Engine

General surgery retained a 29.15% share of the 2025 medical robotic systems market, leveraging high-frequency procedures such as cholecystectomy, bariatric revisions, and ventral hernia repair, which achieve post-complication reductions of up to 40% compared to laparoscopy. Reimbursement authorities in the United States and France approve bundled payments that reimburse robotics when they are cost-equivalent to laparoscopy at a 24-month follow-up, driving sustained demand. Surgeons credit motion scaling and 8K visualization for enabling fine dissection near critical vasculature, a capability that curbs conversion-to-open rates to below 2%.

Neurology, however, is the fastest riser, with a 18.1% CAGR, as stereotactic guidance systems merge with intraoperative MRI to localize deep brain targets with 0.5 mm accuracy. Hospitals performing robot-guided spine fusions report 30% less X-ray exposure and 20 minutes shorter OR time per level fused, savings that translate into an additional daily case on high-volume lists. AI-powered anomaly detection flags microhemorrhages in real-time, enhancing safety in tumor resections. These advantages underpin payer approvals in Germany and South Korea, widening addressable volumes.

By End User: Ambulatory Centers Capture Momentum

Hospitals and integrated delivery networks still commanded a 60.25% market share of the medical robotic systems market in 2025, leveraging critical-care backup and 24/7 imaging to handle multi-quadrant oncology and cardiac cases. Teaching centers embed robotics into residency curricula; a single 1,000-bed academic hospital may operate six to eight consoles across disciplines, solidifying vendor lock-in through credentialing pipelines. Such institutions negotiate tiered-instrument pricing that falls once volume exceeds 1,500 cases annually, preserving margins while expanding the vendor footprint.

Ambulatory surgery centers (ASCs) are growing at a 18.05% CAGR, converting former orthopedic suites into multi-specialty robotic pods where same-day discharge hits 95% of caseload. U.S. Medicare’s 2025 outpatient rule adds colectomy and prostatectomy to the ASC-covered list, a catalyst that opens up seven-figure annual revenue opportunities for early adopters. To accommodate tighter footprints, vendors are rolling out compact carts with boom-mounted arms and integrated smoke evacuation, which save 14 square feet compared to legacy rigs. Rehabilitation clinics, meanwhile, pilot subscription exoskeletons reimbursed under new CPT codes for gait training, signaling further end-user diversification.

By Automation Level: Semi-Autonomous Platforms Prevail

In 2025, tele-operated medical robots commanded a dominant 54.65% share of the medical robotic systems market. This surge is attributed to the increasing adoption of surgical consoles in hospitals, driven by compelling evidence of enhanced precision, reduced complications, and expedited recovery times. The leadership of tele-operated systems is further solidified by rising procedure volumes in urology, gynecology, and general surgery. Major manufacturers are reaping benefits not only from upgrades to their installed base but also from a steady stream of revenue generated through instruments and services. Yet, challenges loom: high capital expenditures, stringent credentialing mandates, and extended training periods hinder wider adoption, particularly in mid-sized hospitals. Additionally, limited interoperability among systems and concerns over procedural costs further dampen penetration rates. Nonetheless, teleoperated platforms remain the cornerstone of surgical robotics on a global scale.

Healthcare systems are increasingly adopting robotic rehabilitation, mobility support, bedside assistance, and logistics automation, resulting in a 18.48% growth rate for assistive and collaborative medical robots during the forecast period. The demand for robotic exoskeletons, therapy robots, and mobile collaborative assistants is being driven by an aging population, a rising burden of chronic diseases, and staffing shortages in hospitals. These robotic systems not only provide operational relief but also standardize therapy sessions and enhance patient engagement. The growth of this sector is bolstered by advancements in AI-driven sensing technologies and safer interactions between humans and robots. Yet, challenges such as reimbursement gaps, a lack of extensive long-term clinical evidence, and difficulties in integrating these technologies into existing hospital workflows pose significant hurdles. Despite these challenges, the versatility of these robots and their comparatively lower entry costs, especially when juxtaposed with surgical robots, position them as the fastest-growing segment in the market.

Geography Analysis

North America captured 35.45% revenue in 2025, supported by clear FDA pathways, strong venture funding, and payer acceptance of robotic codes. U.S. ambulatory centers increasingly integrate multi-specialty robotic suites, and Canada’s provincial tenders shift toward leasing to manage upfront budgets. Mexico’s private hospitals embrace robotics to service inbound medical tourists seeking cost-effective bariatric and orthopedic procedures.

The Asia-Pacific region is the fastest-growing geography, with a 17.6% CAGR to 2031, driven by public funding, demographic pressure, and rising insured populations. China’s tier-3 hospital procurements accelerate oncology robot volumes, while Japan subsidizes exoskeletons for post-stroke therapy under its national insurance scheme. India’s corporate hospital chains adopt robots to differentiate care and draw diaspora patients, with procedural pricing 40-60% lower than Western counterparts.

Europe shows moderate but steady adoption shaped by heterogeneous payer systems. Germany’s volume-based quality rules force robotic investment, especially in visceral and cardiac surgery. The United Kingdom’s NICE incorporates cost-effectiveness thresholds, stretching adoption timelines yet ensuring sustainable utilization. France, Italy, and Spain pool robotic assets across regional clusters, while the Nordics integrate robotic data feeds into national registries for outcome benchmarking.

Competitive Landscape

The medical robotic systems market remains moderately fragmented. Intuitive Surgical leverages its 7,500-plus installed da Vinci systems and extensive surgeon-training curricula to safeguard share, but newer entrants erode price points. CMR Surgical’s modular Versius robot, cleared in more than 80 countries, offers a smaller footprint and flexible financing, appealing to budget-constrained facilities.

Johnson & Johnson’s Ottava prototype performed its first human surgeries in February 2025, marking the company’s bid to integrate AI vision through its Polyphonic digital ecosystem. Siemens Healthineers expands its robotics scope by integrating imaging, navigation, and automated C-arm positioning to create tightly coupled intraoperative workflows. Stryker maintains leadership in ortho robotics, and Smith+Nephew’s CORI knee platform secures new insert clearances, sustaining application depth.

Strategically, vendors tend to focus on recurring revenue. Hardware innovation alone no longer guarantees differentiation; AI analytics for predictive maintenance, integrated training modules, and cloud-delivered upgrades are key to anchoring customer loyalty. Partnerships with semiconductor and cloud providers accelerate algorithm development, while acquisitions in imaging and navigation fill capability gaps.

Medical Robotic Systems Industry Leaders

Intuitive Surgical Inc.

Stryker Corporation

Medtronic plc

Johnson & Johnson Services, Inc.

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zimmer Biomet reported Q1 2025 financial results showing continued growth in robotic solutions, highlighting the Z1 Triple-Taper Femoral Hip System and HAMMR Automated Hip Surgical Impactor System as key innovations. The company's acquisition of Paragon 28 for foot and ankle orthopedic technologies strengthens their robotic portfolio and market position in specialized surgical applications.

- April 2025: Smith+Nephew announced Q1 2025 revenue of USD 1,407 million with strong growth in robotics, particularly their CORI Surgical System for knee surgery. The company received FDA clearance for new LEGION Medial Stabilized inserts designed for use with the CORI system, expanding their robotics-enabled procedure capabilities.

- March 2025: Siemens Healthineers introduced the Ciartic Move, an automated self-driving C-arm system for intraoperative imaging that reduces procedure times by up to 50% during spine and pelvic surgeries. This innovation addresses global medical staff shortages while improving workflow efficiency and reducing radiation exposure for surgical teams.

- February 2025: Johnson & Johnson completed first surgeries with their Ottava surgical robot after receiving FDA Investigational Device Exemption approval, marking a significant milestone in their robotic surgery platform development. The company also announced a collaboration with NVIDIA to advance AI integration in surgical robotics through their Polyphonic digital ecosystem.

Global Medical Robotic Systems Market Report Scope

The Medical Robotic Systems Market Report is Segmented by Product Type (Surgical Robotic Systems, Rehabilitative Robotic Systems, Non-invasive Radiosurgery Robots, Hospital and Pharmacy Automation Robots, and Other Product Types), Component (Robotics Systems, Instruments and Accessories, Services (Maintenance, Training, Subscription), and Software and AI Platforms), Application (General Surgery, Orthopedic Surgery, Neurosurgery, Cardiovascular, Gynecology, Urology, Oncology, aparoscopy and Thoracoscopy, and Other Applications), End User (Hospitals and Clinics, Ambulatory Surgery Centers, Rehabilitation Centers, and Homecare Settings), Automation Level (Tele-operated, Semi-autonomous, Autonomous, and Assistive and Collaborative), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Surgical Robotic Systems |

| Rehabilitative Robotic Systems |

| Non-invasive Radiosurgery Robots |

| Hospital and Pharmacy Automation Robots |

| Other Product Types |

| Robotic Systems |

| Instruments and Accessories |

| Services (Maintenance, Training, Subscription) |

| Software and AI Platforms |

| General Surgery |

| Orthopedic Surgery |

| Neurosurgery |

| Cardiovascular |

| Gynecology |

| Urology |

| Oncology |

| Laparoscopy and Thoracoscopy |

| Other Applications |

| Hospitals and Clinics |

| Ambulatory Surgery Centers |

| Rehabilitation Centers |

| Homecare Settings |

| Tele-operated |

| Semi-autonomous |

| Autonomous |

| Assistive and Collaborative |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Surgical Robotic Systems | |

| Rehabilitative Robotic Systems | ||

| Non-invasive Radiosurgery Robots | ||

| Hospital and Pharmacy Automation Robots | ||

| Other Product Types | ||

| By Component | Robotic Systems | |

| Instruments and Accessories | ||

| Services (Maintenance, Training, Subscription) | ||

| Software and AI Platforms | ||

| By Application | General Surgery | |

| Orthopedic Surgery | ||

| Neurosurgery | ||

| Cardiovascular | ||

| Gynecology | ||

| Urology | ||

| Oncology | ||

| Laparoscopy and Thoracoscopy | ||

| Other Applications | ||

| By End User | Hospitals and Clinics | |

| Ambulatory Surgery Centers | ||

| Rehabilitation Centers | ||

| Homecare Settings | ||

| By Automation Level | Tele-operated | |

| Semi-autonomous | ||

| Autonomous | ||

| Assistive and Collaborative | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical robotic systems market?

The medical robotic systems market is valued at USD 17.92 billion in 2026 and is projected to reach USD 37.44 billion by 2031, reflecting a 15.88% CAGR.

Which product category dominates medical robotics installations?

Surgical robotic systems hold leadership with 26.35% of 2025 revenue, anchored by broad specialty coverage and established reimbursement frameworks.

Why are ambulatory surgery centers important for future growth?

ASCs deliver 30–40% cost savings over inpatient settings and post a 18.05% CAGR through 2031, making them pivotal in expanding robotic procedure volumes.

What regions present the highest growth potential?

Asia-Pacific records the fastest 17.6% CAGR, driven by public funding in China, Japan, and South Korea as well as rising insurance penetration across emerging economies.

How are vendors addressing high capital costs for hospitals?

Manufacturers and finance companies are rolling out subscription and leasing models that convert upfront CAPEX into predictable operating expenses, accelerating adoption in middle-income markets.

What role does artificial intelligence play in medical robotics?

AI enhances intra-operative imaging, guides instrument trajectories, and supports predictive maintenance, collectively improving surgical precision and system uptime while forming a new layer of differentiation for vendors.

Page last updated on: