Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 43.19 Billion |

| Market Size (2031) | USD 68.66 Billion |

| Growth Rate (2026 - 2031) | 9.72% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Diabetes Care Devices Market Analysis by Mordor Intelligence

The Diabetes Care Devices Market size is expected to increase from USD 40.16 billion in 2025 to USD 43.19 billion in 2026 and reach USD 68.66 billion by 2031, growing at a CAGR of 9.72% over 2026-2031.

A closer link between those population dynamics and unit demand emerges as payers, providers and manufacturers increasingly recognize that technology-enabled care lowers lifetime treatment costs. Executives weighing expansion strategies can infer that every incremental percentage point increase in the diagnosed population translates into a disproportionately larger uptick in technology adoption because most newly diagnosed individuals today start their journey with at least one connected device rather than legacy finger-stick meters.

Key Report Takeaways

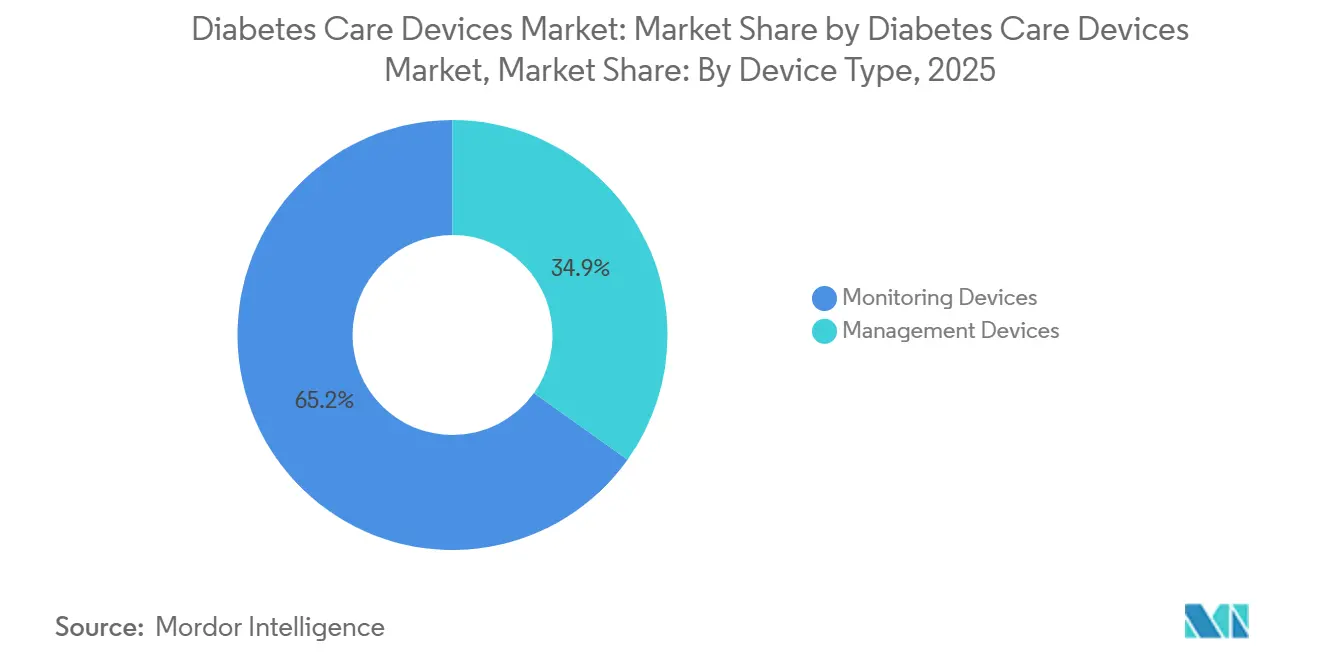

- By device type, Monitoring Devices dominated with 65.15% market share in 2025 and are projected to register a 10.15% CAGR through 2031.

- By patient type, Type-2 Diabetes commanded 85.30% market share in 2025 and is simultaneously the fastest-growing segment with a 9.91% CAGR from 2026-2031.

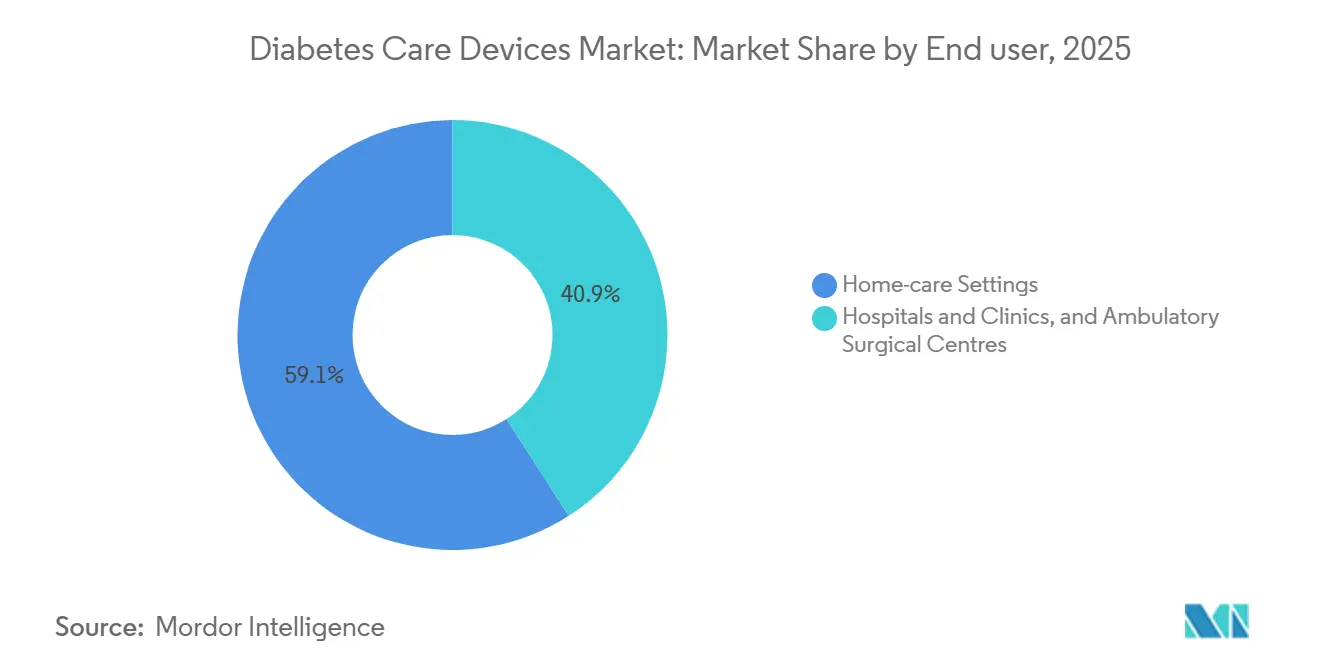

- By end-user, Homecare Settings led with 59.10% market share in 2025 and are expected to expand at a 10.77% CAGR to 2031.

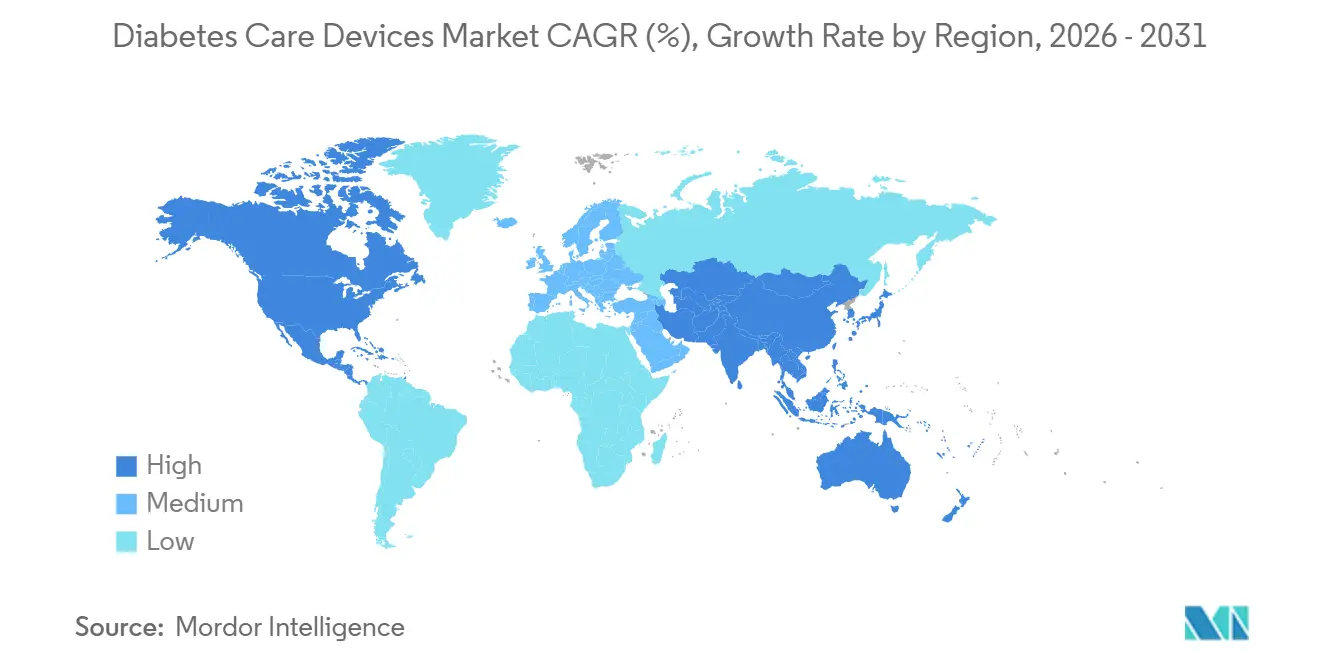

- By region, North America held 41.94% of 2025 revenue; Asia-Pacific is forecast to accelerate at an 12.31% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diabetes Care Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid reimbursement expansion for CGM Worldwide | 1.70% | Global, with significant impact in North America and Europe | Medium term (2-4 years) |

| Increasing Global prevalence of diabetes and associated risk factors | 1.40% | Global, with higher impact in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Advancements in technology | 1.00% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Increased Government and Private Investments | 0.80% | North America, Europe, and emerging Asian markets | Medium term (2-4 years) |

| European paediatric guidelines accelerating hybrid closed-loop pump uptake | 0.70% | Europe, with spillover effects in North America | Short term (≤ 2 years) |

| Off-label GLP-1 surge fuelling home glucose testing demand in North America | 0.60% | North America, with emerging impact in Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Reimbursement Expansion for CGM Worldwide

The expansion of insurance coverage for continuous glucose monitoring (CGM) systems is fundamentally reshaping market dynamics, with a 1.7% contribution to the overall CAGR forecast. In a significant development, New Zealand announced funding for CGMs and expanded access to insulin pumps effective October 2024, with expectations of over 12,000 people accessing funded CGMs in the first year [1]Pharmac. "Decision to fund continuous glucose monitors, insulin pumps and insulin pump consumables." . Similarly, Canada's introduction of Bill C-64 in February 2024 aims to provide universal coverage for diabetes medications and create a dedicated fund for diabetes devices and supplies, addressing the financial burden for approximately 3.7 million Canadians with diabetes Health Canada [2]Health Canada. "Universal Access to Diabetes Medications, and Diabetes Device Fund for Devices and Supplies." . The reimbursement landscape is shifting from covering only high-risk patients to broader populations, with private insurers following government initiatives to expand coverage criteria, creating a virtuous cycle of increased adoption, improved outcomes, and further reimbursement expansion

Increasing Global Prevalence of Diabetes and Associated Risk Factors

The alarming rise in diabetes prevalence is driving market growth with a 1.4% contribution to the overall CAGR forecast. According to a BMJ study, the global age-standardized prevalence of type 1 diabetes increased from 400 to 514 per 100,000 population between 1990 and 2019, while mortality decreased from 4.74 to 3.54 per 100,000, indicating longer lifespans for diabetic patients requiring continuous management. This epidemiological shift is creating sustained demand for diabetes devices across all segments. The Western Sydney Diabetes initiative reported diabetes rates exceeding 13% among adults in the region, with an economic burden of USD 1.8 billion annually, highlighting the financial imperative for effective management solutions. The convergence of aging populations, increasing obesity rates, and sedentary lifestyles is accelerating diabetes incidence worldwide, with particularly rapid growth in emerging economies where changing dietary patterns and urbanization are contributing factors.

Advancements in Technology

Technological innovation is revolutionizing diabetes management, contributing 1.0% to the overall CAGR forecast. The integration of artificial intelligence with continuous glucose monitoring is enabling predictive capabilities, with systems like Roche's Accu-Chek SmartGuide providing glucose level predictions from 30 minutes to two hours ahead, allowing proactive management of potential hypoglycemic events. Non-invasive monitoring technologies are advancing rapidly, with researchers at the University of Waterloo developing a wearable device using miniaturized radar technology that fits inside a smartwatch and tracks glucose levels without skin contact. The emergence of closed-loop artificial pancreas systems is automating insulin delivery, with neural-network artificial pancreas (NAP) technology demonstrating performance comparable to traditional algorithms while requiring significantly less processing time, making it suitable for devices with limited computational resources Healio.

Increased Government and Private Investments

Strategic investments in diabetes technology are accelerating innovation and market expansion, contributing 0.8% to the overall CAGR forecast. The FY 2025 President's Budget for the Indian Health Service (IHS) proposes USD 8.2 billion in total funding, including USD 260 million specifically allocated for the Special Diabetes Program for Indians, aimed at reducing diabetes prevalence among American Indian and Alaska Native populations [3]Tso, Roselyn. "Testimony from Roselyn Tso, Director, Indian Health Service on FY 2025 President's Budget Request." U.S. Department of Health and Human Services. In Canada, the federal government is establishing a long-awaited diabetes device fund to enhance access to innovative diabetes management technologies, responding to growing public support for government investment in research and cures. The European Commission's Horizon Europe Work Programme for 2025 is allocating significant funding for health research and innovation, with specific focus on improving healthcare systems and developing innovative health technologies for non-communicable diseases including diabetes. These investments are not only advancing technological capabilities but also expanding market access by reducing cost barriers and supporting infrastructure development.

Restraint Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Devices | -1.00% | Global, with severe impact in developing regions | Medium term (2-4 years) |

| Less Awareness about Device usage in remote and underdeveloped region | -0.70% | Asia-Pacific, Africa, and rural areas globally | Long term (≥ 4 years) |

| EU-MDR re-certification backlog for legacy lancets | -0.60% | Europe, with supply chain impacts globally | Short term (≤ 2 years) |

| Patch-pump recalls dampening uptake in Oceania | -0.30% | Australia, New Zealand, and neighboring Pacific islands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Devices

Premium CGM annualized costs hover near USD 3,800 for flagship brands before insurance, while lower-priced flash glucose monitors cost closer to USD 2,300. These figures, drawn from publicly available company catalog pricing, create a bifurcated market in which reimbursement status largely dictates adoption. Executives should recognize that in low-income regions even a USD 500 annual out-of-pocket burden can depress uptake, so localized manufacturing or subscription-based financing may prove effective. The takeaway for strategy teams is that pricing elasticity varies not only by per-capita income but also by cultural perceptions of preventive care; for instance, some emerging markets accept higher spending on chronic-disease devices if bundled telehealth support is included.

Less Awareness About Device Usage in Remote and Underdeveloped Regions

Recent surveys indicate that fewer than 15 % of primary care physicians in certain Asia-Pacific districts feel fully confident in prescribing advanced diabetes devices. While that statistic emerges from regional conference proceedings rather than peer-reviewed journals, it still signals a bottleneck in the commercial funnel. Device manufacturers that build clinician-focused e-learning modules can shrink that knowledge gap and create brand loyalty ahead of competitors. A pertinent inference for executives is that educational infrastructure can serve as a market-entry wedge, often yielding a lower customer-acquisition cost than traditional direct-to-consumer advertising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring Technologies Drive Market Evolution

The monitoring devices segment commands a dominant 65.15% market share in 2025 and is expected to grow with a 10.15% CAGR from 2026-2031, reflecting its critical role in diabetes management across all patient populations. Continuous glucose monitoring (CGM) systems are revolutionizing diabetes care through real-time data provision and integration with automated insulin delivery systems, fundamentally changing treatment paradigms. A study published in the Journal of Diabetes Science and Technology demonstrated that CGM use is associated with lower HbA1c levels and improved outcomes, though disparities in access persist based on race and socioeconomic status Liebertpub. The management devices segment, encompassing insulin pumps, pens, and syringes, is projected to grow, driven by innovations in automated insulin delivery systems and smart insulin pens.

Technological convergence is reshaping the competitive landscape, with integration between monitoring and management devices creating comprehensive diabetes management ecosystems. The emergence of hybrid closed-loop systems that combine CGM data with automated insulin delivery represents a significant advancement, with studies showing improvements in time-in-range metrics and quality of life for users. A clinical trial of the Omnipod 5 automated insulin delivery system in adults with type 2 diabetes demonstrated a significant reduction in hemoglobin A1c levels from 8.2% to 7.4% after 13 weeks, indicating improved glycemic control JAMA Network Open. The development of non-invasive glucose monitoring technologies, including optical and electromagnetic sensors, promises to further transform the market by addressing patient discomfort associated with traditional monitoring methods.

By Patient Type: Type-2 Diabetes Dominates and Drives Growth

Type-2 diabetes represents the largest patient segment with an overwhelming 85.30% market share in 2025, while simultaneously exhibiting the fastest growth trajectory at 9.91% CAGR through 2031. This dual dominance reflects the global epidemic of type-2 diabetes, driven by increasing obesity rates, sedentary lifestyles, and aging populations. The management of type-2 diabetes is evolving beyond traditional approaches, with continuous glucose monitoring (CGM) increasingly recognized as valuable for this patient population. Stanford Medicine researchers have developed an AI-based algorithm that utilizes data from continuous blood glucose monitors to identify subtypes of Type 2 diabetes with approximately 90% accuracy, enabling more personalized treatment approaches.

The rise of GLP-1 receptor agonists is creating new dynamics in the type-2 diabetes devices market, with increased demand for glucose monitoring among patients using these medications. A study published in the Journal of Shoulder and Elbow Surgery found that GLP-1 users have a higher likelihood of developing adhesive capsulitis (odds ratio = 1.28), highlighting the need for comprehensive monitoring during treatment Science Direct. Type-1 diabetes and gestational diabetes segments, though smaller, are driving innovation in specialized devices tailored to their unique needs. The development of hybrid closed-loop systems for pediatric type-1 diabetes patients has shown significant improvements in glycemic control, with a study reporting a 0.4% reduction in HbA1c and an 8.4 percentage point increase in time spent in the target glucose range compared to sensor-augmented pump therapy.

By End-user: Home-care Settings Gain Momentum

Hospitals & Clinics benefit from established infrastructure and specialized diabetes care teams. However, Home-care Settings had a market share of 59.10% in 2025 and are experiencing faster growth at 10.77% CAGR from 2026 to 2031, reflecting the paradigm shift toward patient-centered, remote diabetes management. This transition is accelerated by advancements in telehealth and connected diabetes devices that enable effective remote monitoring and intervention. A Stanford Medicine study implemented an AI-powered dashboard to help diabetes educators identify patients needing assistance by analyzing CGM data efficiently, resulting in 64% of patients achieving optimal A1c levels after one year, compared to 28% in previous cohorts .

The integration of artificial intelligence with home diabetes management is creating new possibilities for personalized care. AI algorithms can predict glucose levels up to 30 minutes in advance, enabling proactive management and reducing the risk of severe glycemic events. Ambulatory Surgical Centers represent a smaller but growing segment, particularly for procedures related to insulin pump implantation and management of diabetes complications. The COVID-19 pandemic accelerated the shift toward home-based care, with patients and providers recognizing the benefits of remote monitoring and telehealth consultations for routine diabetes management. This trend is likely to persist and expand as technologies improve and reimbursement policies adapt to support home-based care models, fundamentally reshaping the end-user landscape for diabetes devices.

Geography Analysis

North America maintains a 41.94% share in 2025, partially owing to Medicare reimbursement and a high density of device-trained endocrinologists. In that same year, the CDC recorded 29.7 million diagnosed and 8.7 million undiagnosed cases of diabetes in the United States (same CDC citation). This sizable undiagnosed cohort provides a latent expansion pool that device makers can target via screening initiatives tied to retail pharmacies. Yet mounting pressure from employers and government payers to reduce healthcare spending suggests future price compression for premium platforms, nudging manufacturers toward value-based-care contracts.

Asia-Pacific posts the fastest growth at 12.31% CAGR through 2031, driven by urbanization and the world’s highest absolute number of diabetes cases. International Diabetes Federation estimates place the region’s share above 60% of global prevalence. Manufacturing executives often overlook that Asia-Pacific also boasts some of the world’s most digitally engaged populations, so smartphone-tethered CGM models may leapfrog earlier Bluetooth-only variants. Consequently, suppliers that embed local language AI coaching into their apps stand to win disproportionately high market share.

Europe sustains a stable presence thanks to universal health systems and aging demographics. The region’s regulatory environment, guided by the European Medicines Agency, traditionally demands longer trial follow-ups than the FDA, which can delay commercialization. The recent Abbott–Dexcom patent truce removes a legal overhang that previously cast uncertainty on procurement timelines, giving hospital buyers clearer visibility into multi-year supply contracts. An astute reading of the situation suggests that European buyers will now leverage the presence of two legally unencumbered suppliers to negotiate bulk-purchase discounts, compressing average selling prices but potentially boosting unit volumes.

Competitive Landscape

Market concentration is moderate, with three multinational corporations capturing a majority share yet facing nimble startups in sensor miniaturization and algorithm design. The Abbott–Dexcom ten-year cross-license agreement exemplifies a new era of “coopetition,” wherein rivals share foundational intellectual property to accelerate overall market expansion. Medtronic’s partnership with Abbott on an integrated CGM-pump portfolio further evidences the pivot to interoperable ecosystems. Strategists may recognize that partnerships of this nature often presage joint ventures in manufacturing or cloud data analytics, areas where scale provides tangible cost advantages.

White-space opportunities are emerging at the intersection of diabetes care and obesity pharmacotherapy. GLP-1 receptor agonists reduce glucose excursions, potentially lowering device usage frequency, yet they also heighten the need for periodic titration. Companies integrating weight-management metrics into insulin-dosing algorithms could command premium pricing among endocrinology clinics that treat metabolic syndrome holistically.

Diabetes Care Devices Industry Leaders

-

Abbott Diabetes Care

-

Medtronic (Diabetes)

-

Dexcom

-

Roche Diabetes Care

-

Insulet Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Medtronic received FDA clearance to pair its Simplera Sync sensor with selected insulin pumps, reinforcing its integrated-system roadmap.

- April 2025: Dexcom secured FDA authorization for the G7 15 Day CGM, extending its sensor life and improving inventory turns.

- February 2025: Tandem’s Control-IQ+ algorithm gained FDA clearance for Type 2 diabetes, opening a substantial new revenue stream for the company.

- December 2024: Abbott and Dexcom signed a ten-year cross-license accord, removing litigation costs and accelerating product innovation.

- November 2024: Medtronic launched an upgraded InPen app, setting the stage for a Simplera CGM-enhanced smart-MDI ecosystem.

- October 2024: Senseonics received FDA clearance for the Eversense 365, the first implantable sensor approved for annual wear.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global diabetes care devices market as all purpose-built hardware that measures blood glucose or delivers insulin, including glucometers, test strips, lancets, continuous glucose monitoring (CGM) sensors, insulin pens, pumps, syringes, and jet injectors, sold to healthcare facilities and home users worldwide. We treat disposables that are intrinsically paired with each device (for example, CGM transmitters and infusion sets) as part of the same revenue pool.

Scope Exclusion: Standalone mobile apps or cloud analytics that do not ship with a physical measuring or dosing component are outside this market.

Segmentation Overview

-

By Device Type

-

Monitoring Devices

-

Self-Monitoring

- Glucometer Devices

- Test Strips

- Lancets

-

Continuous Glucose Monitoring

- Sensors

- Durables

-

Self-Monitoring

-

Management Devices

-

Insulin Pumps

- Insulin Pump Device

- Insulin Pump Reservoir

- Infusion Set

- Insulin Syringes

- Insulin Pens

- Jet Injectors

-

Insulin Pumps

-

Monitoring Devices

-

By Patient Type

- Type-1 Diabetes

- Type-2 Diabetes

- Gestational & Others

-

By End-user

- Hospitals & Clinics

- Home-care Settings

- Ambulatory Surgical Centres

-

Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- France

- Italy

- Spain

- United Kingdom

- Rest of Europe

-

Asia-Pacific

- Japan

- South Korea

- China

- India

- Australia

- Rest of Asia-Pacific

-

South America

- Mexico

- Brazil

- Rest of South America

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed endocrinologists, diabetes educators, hospital procurement leads, and retail pharmacy buyers across North America, Europe, Asia-Pacific, and the Middle East. Their insight refined sensor replacement rates, typical pump wear times, and reimbursement triggers, allowing us to bridge data gaps and stress-test early findings.

Desk Research

We began with open datasets from bodies such as the International Diabetes Federation, WHO, and the World Bank, which anchor prevalence, treatment coverage, and spending patterns across 40 major countries. Trade associations, including the Advanced Medical Technology Association and the European Diabetes Forum, provided shipment audits and regulatory timelines. Company 10-Ks, investor decks, and customs shipment records added price and channel color, while paid access to D&B Hoovers and Dow Jones Factiva let Mordor analysts verify manufacturer revenue splits and product launch cadence. These and many other sources supplied the factual spine; the list above is illustrative, not exhaustive.

A second sweep mined clinical journals for device accuracy studies and adoption barriers, and we tracked procurement portals for hospital tenders to gauge institutional demand shifts. This layered desk work established realistic average selling prices (ASP) and unit volumes before we spoke with the market.

Market-Sizing & Forecasting

We employ a top-down prevalence-to-treated cohort build, multiplying diagnosed diabetics by device penetration rates and validated ASPs. Selective bottom-up checks, such as supplier roll-ups and sampled retail scans, are then used to tune totals. Key variables include diagnosed diabetes population, CGM adoption curve, insulin pump installed base, average testing frequency, reimbursement coverage ratios, and disposable-per-device multipliers. A multivariate regression model projects each variable forward, with scenario analysis layering in guideline changes or disruptive technology uptake where flagged by experts.

Data Validation & Update Cycle

Outputs pass three analyst reviews, anomaly screens, and a final variance check against independent shipment or revenue signals. Mordor refreshes every twelve months, with interim updates if material events, such as major recalls or reimbursement shifts, warrant a rerun.

Why Our Diabetes Care Devices Baseline Remains Dependable

Published estimates often diverge because firms slice the market by different device families, pricing bases, or refresh cadences. Our disciplined scope selection and annual data sweep keep the baseline clear and current.

Major gaps typically stem from partial inclusion of consumables, unvetted ASP assumptions, or outdated prevalence numbers; this is where Mordor Intelligence applies its treated-cohort logic and live ASP tracking, which many others bypass.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 65.74 B | Mordor Intelligence | - |

| USD 34.30 B | Global Consultancy A | Excludes insulin delivery devices and related disposables |

| USD 59.20 B | Industry Research Firm B | Relies on manufacturer revenue only, omits retail mark-ups |

| USD 68.57 B | Trade Journal C | Uses aggregated company filings, limited geographic breakout |

In sum, the side-by-side review shows that our prevalence-anchored model, refreshed annually and triangulated through primary checks, offers decision-makers a balanced, transparent starting point they can readily audit and replicate.

Key Questions Answered in the Report

What is the current global diabetes care devices market size?

The Diabetes Care Devices Market is valued at USD 43.19 billion in 2026.

How fast is the diabetes care devices market expected to grow?

Market size is forecast to expand at a 9.72% CAGR from 2026 to 2031, reaching USD 68.66 billion.

Which region will register the highest growth?

The Asia-Pacific market size is projected to rise at an 12.31% CAGR between 2026 and 2031.

What device category is growing fastest?

Monitoring devices, especially continuous glucose monitoring devices, will grow around 10.15% per year through 2031.

Why are CGM reimbursement policies critical to market share?

Expanded coverage increases patient affordability, accelerating uptake and boosting manufacturer revenue.

How are interoperability regulations affecting competition?

FDA interoperability pathways allow pumps, CGMs and algorithms from different brands to work together, shifting competitive focus from closed hardware ecosystems to software and data integration.

Page last updated on: