Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

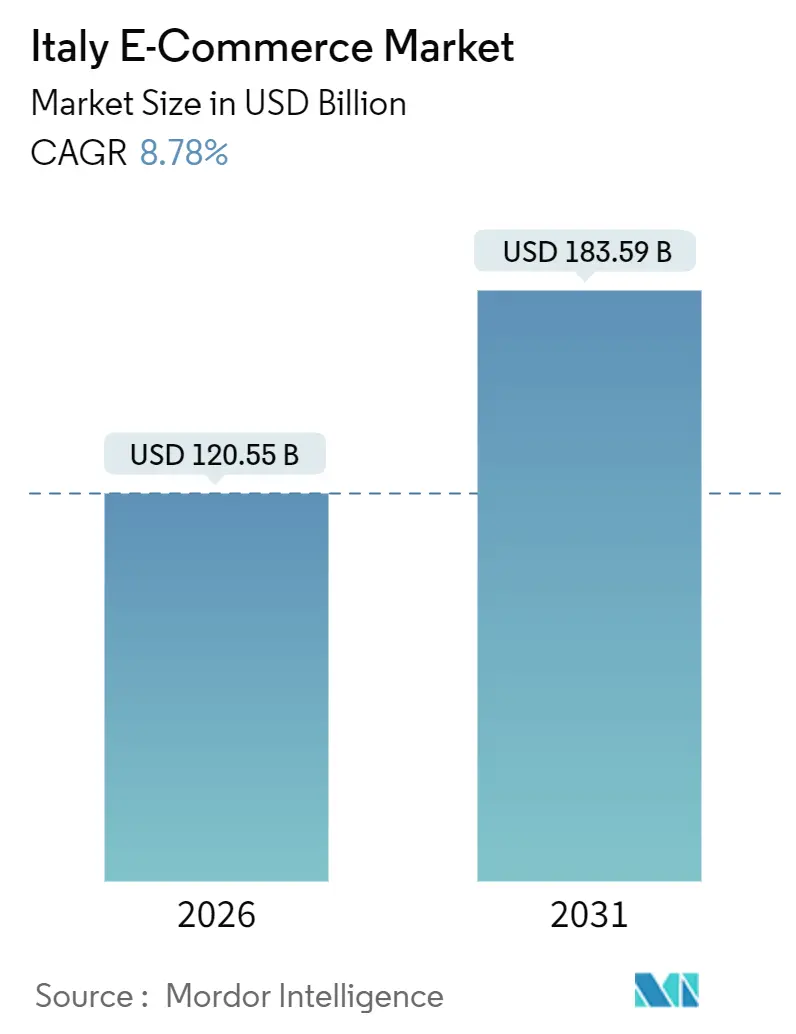

| Market Size (2026) | USD 120.55 Billion |

| Market Size (2031) | USD 183.59 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

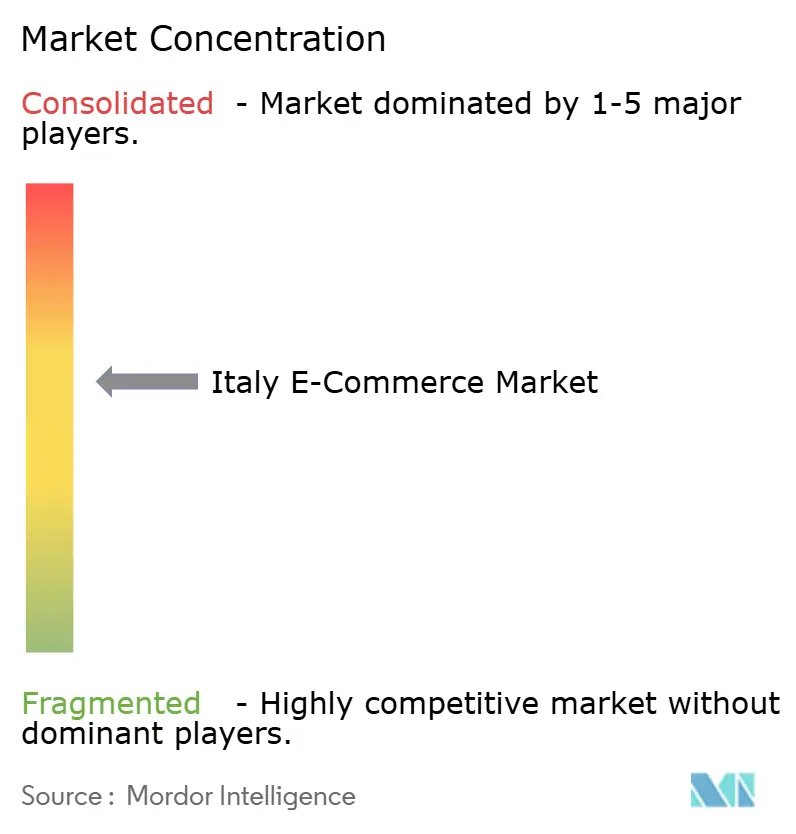

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy E-commerce Market Analysis by Mordor Intelligence

The Italy E-commerce Market size reached USD 120.55 billion in 2026 and is projected to climb to USD 183.59 billion by 2031, reflecting an 8.78% CAGR. Digital payments overtook cash in 2024, the first time this occurred nationwide, and the mandatory rollout of SEPA Instant Credit Transfer in 2025 removed interchange fees that previously discouraged low-margin online sales. Smartphone checkouts now anchor most consumer journeys, while the country’s compulsory B2B e-invoicing network processes 2 billion electronic invoices each year, lowering reconciliation costs and widening the addressable pool of digital buyers. Same-day delivery capacity in the north, government tax credits for SME digitalization, and a 46% jump in buy-now-pay-later (BNPL) volume during 2024 all reinforce the market’s structural growth path. Competitive intensity is rising as vertical specialists gain share from broad marketplaces and as fintechs push real-time account-to-account payment rails into everyday retail.

Key Report Takeaways

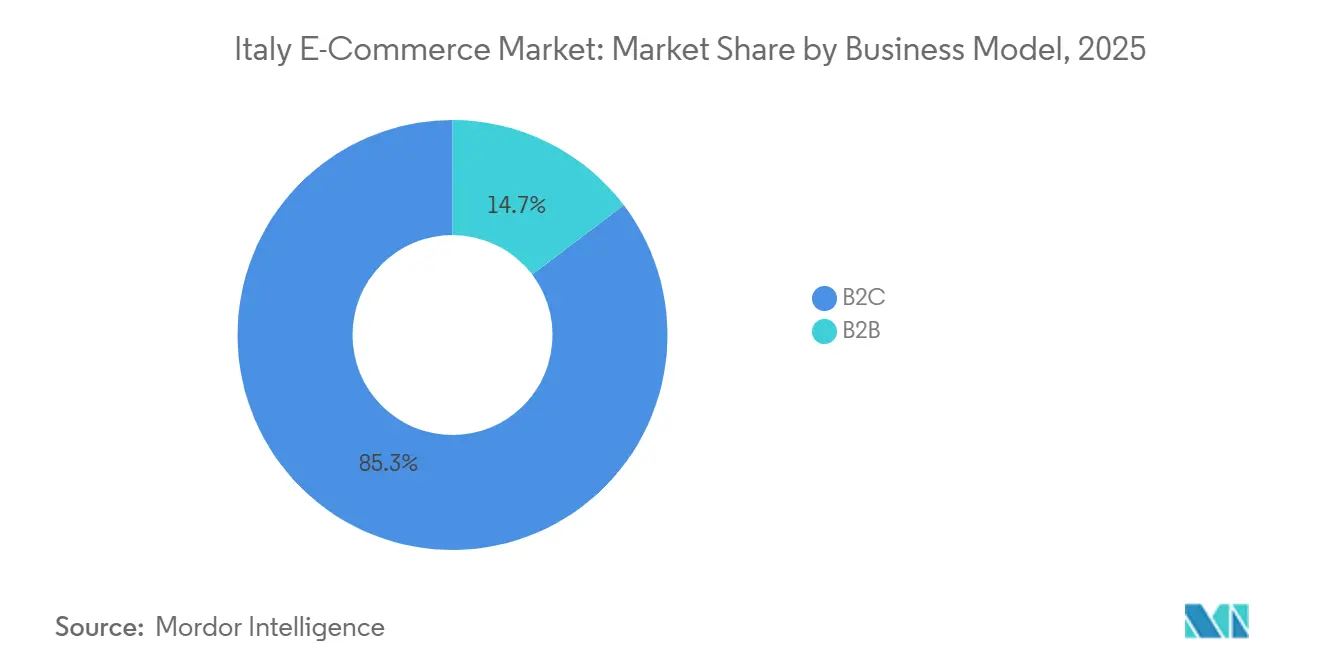

- By business model, consumer transactions held 85.34% of the Italy E-commerce Market share in 2025, while B2B sales are forecast to expand at an 11.87% CAGR to 2031.

- By device type, smartphones accounted for 56.42% of the Italy E-commerce Market in 2025, and the segment is advancing at a 9.21% CAGR through 2031.

- By payment method, credit and debit cards led with 31.68% of the Italy E-commerce Market in 2025, whereas BNPL solutions are projected to grow at a 13.16% CAGR to 2031.

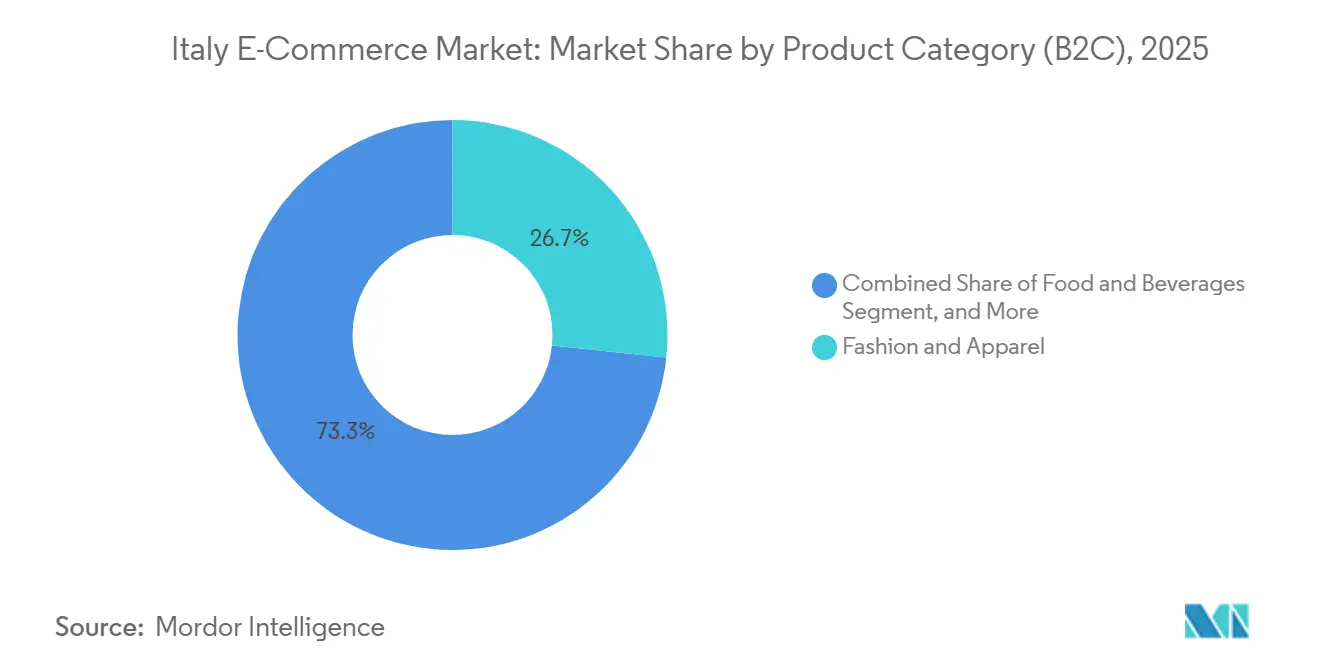

- By product category, fashion and apparel delivered 26.67% of the Italy E-commerce Market 2025 revenue, yet food and beverages are the fastest-growing line, set to expand at a 12.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of Account-to-Account Instant Payments | +1.8% | Nationwide, strongest in Lombardy, Emilia-Romagna | Short term (≤ 2 years) |

| Rising Mobile-Commerce Adoption | +1.5% | Urban centers across the country | Medium term (2-4 years) |

| Surge in Same-Day Delivery Infrastructure | +1.3% | Northern regions with spillover to central provinces | Medium term (2-4 years) |

| Government Spinta Digitale Tax Credits | +1.1% | Nationwide, highest uptake in Veneto and Lombardy | Long term (≥ 4 years) |

| Rapid Penetration of Ultra-Fast Grocery Delivery | +0.9% | Tier-2 cities, expanding south | Short term (≤ 2 years) |

| Cross-Border Marketplace Access via EU Single-VAT | +0.7% | Export-oriented SMEs nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption Of Account-To-Account Instant Payments

Real-time SEPA Instant rails became mandatory for all Italian banks in 2025, eliminating two-day settlement delays and interchange fees that averaged 1.5% of order value. Merchants in Lombardy and Emilia-Romagna adopted instant-payment modules 35% faster than peers elsewhere, improving margins on low-ticket grocery and electronics orders. Domestic fintech Satispay embedded the rails into its wallet, giving 380,000 merchants sub-10-second settlement and raising its user base to 5 million. Instant transfers also meet strong customer authentication rules without one-time passwords, trimming checkout abandonment rates. Together, these factors position instant payments as the default tender type for repeat transactions nationwide.[1]Banca d'Italia, “Payment Systems and Financial Market Infrastructures,” BANCA D’ITALIA, bancaditalia.it

Rising Mobile-Commerce Adoption Among 25-34-Year-Olds

Smartphones generated 56.42% of online transaction value in 2025, propelled by contactless software POS terminals that jumped from 40,000 units in 2023 to 152,000 in 2024. Short-form video commerce, spearheaded by TikTok Shop, now redirects traffic straight into one-tap checkout pipelines handled by Zalando’s ZEOS network. Wearable devices added EUR 2.5 billion in 2024 volume, widening the definition of mobile commerce beyond phones. Biometric logins satisfy PSD2 authentication with minimal friction, an advantage that amplifies conversion among younger cohorts. As a result, median purchase time on smartphones fell to 2.8 minutes in 2025, down from 4.2 minutes two years earlier.[2]Politecnico di Milano, “Osservatori Digital Innovation,” POLITECNICO DI MILANO, osservatori.net

Surge In Same-Day Delivery Infrastructure

Zalando’s 80,000 m² hub in Verona, operational since late 2024, now fulfills 70% of northern orders within 24 hours. Poste Italiane handled 308 million parcels in 2024 and is fielding 10,000 automated lockers with DHL by 2027, reducing failed deliveries significantly. Locker operator InPost surpassed 3,000 boxes by mid-2025, clustering them around Milan, Turin, and Bologna railway stations. Same-day capability also lowers apparel return costs by compressing try-and-return cycles. Although delivery density in Calabria and Sicily remains 30% below the northern average, new hubs in Naples and Palermo are narrowing the gap.

Government Spinta Digitale Tax Credits For SME Digitalization

Italy earmarked EUR 24 billion in Transition 4.0 credits through 2025, reimbursing up to 50% of SME spend on e-commerce platforms, cloud ERP, and cybersecurity. Invitalia logged 12,000 grant applications in the first half of 2025, with a median project size of EUR 80,000. The program also funds workforce training, addressing a digital-skills deficit that affects 54.2% of Italians. Veneto, Lombardy, and Emilia-Romagna captured nearly half of the approved projects, reflecting the concentration of export-oriented manufacturers integrating web-based procurement portals.[3]Ministero delle Imprese e del Made in Italy, “Transition 4.0 Program Details,” MINISTERO DELLE IMPRESE E DEL MADE IN ITALY, mise.gov.it

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent PSD2 Strong Customer Authentication Friction | -0.8% | Nationwide, harsher for older users | Short term (≤ 2 years) |

| Fragmented Last-Mile Logistics In Southern Regions | -0.6% | Southern mainland and islands | Medium term (2-4 years) |

| Cyber-Fraud Spike in Digital Wallets | -0.5% | Large urban centers | Short term (≤ 2 years) |

| Persistent Digital-Skills Gap In SME Ownership | -0.4% | Mostly rural south and center | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent PSD2 Strong Customer Authentication Friction

Italian regulators apply PSD2 rules so strictly that two-factor checks trigger even on sub-EUR 30 orders if merchants lack transaction-risk-analysis waivers. Banca d’Italia data show 18% of online payments failed authentication in H1 2025, up from 14% a year earlier. Shoppers older than 55, already under-represented online, abandon carts at a 28% rate when redirected to banking apps. Fashion and electronics sellers, where average tickets exceed EUR 50, lose up to one-quarter of sessions when strong customer authentication steps in. Any regulatory relief is unlikely before 2027, compelling retailers to fine-tune exemption logic to reclaim conversions.[4]European Banking Authority, “PSD2 Regulatory Technical Standards,” EUROPEAN BANKING AUTHORITY, eba.europa.eu

Fragmented Last-Mile Logistics In Southern Regions

Calabria, Sicily, and Sardinia together house 18% of the population but just 11% of parcel flows, a gap driven by sparse road networks and higher per-stop costs. Carriers levy EUR 3-EUR 8 surcharges per parcel to Basilicata, Molise, and rural Apulia. Longer lead times discourage online grocery orders that depend on freshness, holding back category growth. Parcel lockers slated for nationwide rollout will reach southern provinces only after 2028, delaying relief. Low return rates in the south mask consumer frustration because initiating pick-ups is cumbersome, inflating perceived satisfaction levels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Compliance-Led Digitization Recasts B2B Economics

B2C transactions controlled 85.34% of the Italy E-commerce Market share in 2025, yet the Italy E-commerce Market size for B2B orders is projected to outpace consumer growth at an 11.87% CAGR, lifted by compulsory e-invoicing that removed turnover thresholds in 2024. Mandatory use of the national Sistema di Interscambio automates three-way matching and speeds cash application, which reduces working-capital drag for manufacturers in Veneto, Lombardy, and Emilia-Romagna.

Repeat purchasing and bulk baskets give B2B sellers stronger margin profiles than fashion or grocery sites, even as mobile procurement apps mirror consumer-grade usability. Transition 4.0 credits, covering half of the cloud-ERP investment, align directly with the EUR 80,000 median project cost logged by Invitalia, accelerating platform deployments that sync to the EU one-stop VAT regime.

By Device Type (B2C): Phones And Wearables Compress Checkout Time

Smartphones captured 56.42% of 2025 basket value and will widen their lead as software POS installations pass 200,000 units by 2027. Desktop sessions still yield order values 18% higher than mobile, reflecting their role in big-ticket electronics and furniture, but their share is slipping two percentage points each year.

Wearables added EUR 2.5 billion in 2024 volume, indicating that the Italy E-commerce Market is extending to any connected device with biometric login. The Italy E-commerce Market size tied to desktops is shrinking, yet the channel remains critical for older buyers and corporate procurement teams that need spreadsheet-style interfaces.

By Payment Method (B2C): Installments Chip Away At Card Dominance

Cards held a 31.68% slice of 2025 spending, but BNPL volume grew 46% in 2024 and is forecast to post a 13.16% CAGR through 2031. Digital wallets already handle 28% of online outlays and are set to climb as SEPA Instant rails remove interchange costs. The Italy E-commerce Market size associated with cards is therefore likely to plateau, while BNPL penetration deepens in fashion and electronics baskets averaging EUR 50-EUR 150.

Scalapay’s dual licensing model satisfies fragmented regional credit rules, and card networks have responded by embedding installment logic directly into plastics, though uptake remains modest. Wallet players such as Satispay blur the BNPL boundary by allowing deferred settlement inside a standard account-to-account flow.

By Product Category (B2C): Grocery Outruns A Maturing Fashion Segment

Fashion and apparel delivered 26.67% of 2025 receipts, yet same-store growth is tapering as urban saturation nears 80% shopper penetration. Food and beverages, in contrast, will grow 12.43% annually as dark-store operators guarantee sub-30-minute fulfillment in Bologna, Verona, and Bari.

Electronics remain a core revenue pillar but face cross-border price pressure, leading domestic chains to leverage omnichannel pick-up and warranty add-ons. The Italy E-commerce Market size linked to grocery will expand rapidly as ultra-fast delivery converts habitual in-store top-ups into multiple weekly app purchases, offsetting lower basket values.

Geography Analysis

Northern Italy commands the densest logistics grid, anchored by Zalando’s Verona megahub and a high locker concentration that significantly reduces failed-delivery costs. Smartphone penetration is among the highest in Lombardy, driving contactless payments to lead nationally. Robust industrial clusters in the region also channel B2B traffic into web portals optimized for the EU single-VAT scheme.

Central regions, including Lazio, Tuscany, and Umbria, contribute a substantial share of national online spending relative to their population. Tax incentives encourage Rome-based SMEs to upgrade digital systems, and new BRT hubs in Perugia and Latina have improved delivery times. Tourism adds another demand driver as hotels and museums adopt online booking for foreign visitors, who have significantly boosted the economy.

Southern mainland and island provinces face challenges, with delivery density considerably lower than in the north and higher surcharges per parcel. Despite these obstacles, wallet adoption is growing rapidly, with a notable portion of Satispay’s new merchants coming from Campania, Puglia, and Sicily. Quick-commerce firms are targeting youth clusters in Bari and Catania, banking on speed to compensate for infrastructure gaps, even as locker rollouts lag behind other regions.

Competitive Landscape

No single platform dominates the Italy E-commerce Market, which remains moderately fragmented. Recent consolidation is reshaping the field: NewPrinces acquired Carrefour Italia, forming a significant grocery group, while Zalando secured a majority stake in ABOUT YOU to pool logistics and marketing resources. OVS expanded its click-and-collect reach by acquiring Goldenpoint, and fintech Satispay significantly increased its merchant base after a successful funding round.

Technology continues to be a critical factor. Esselunga’s route-optimization software has significantly reduced delivery costs, and its cashless Milan Lab is piloting advanced technologies like RFID and computer-vision checkout. Zalando’s partnership with TikTok Shop positions it to capitalize on social-commerce flows from a substantial base of Italian users. However, SME adoption of artificial intelligence in B2B portals remains limited, indicating opportunities for vendors offering solutions that combine e-invoicing compliance with predictive reordering.

Regulatory expertise is becoming a key differentiator. Merchants implementing transaction-risk analysis gain exemptions under PSD2 regulations, reducing cart abandonment rates, while slower adopters face challenges due to higher conversion penalties. Additionally, adherence to GDPR data-protection standards and investments in cybersecurity are increasingly important as wallet fraud incidents rise in urban areas.

Italy E-commerce Industry Leaders

Shein

Esselungaa

Zalando

Amazon.it

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: NewPrinces completed the USD 1.13 billion acquisition of Carrefour Italia, rolling out an everyday-low-pricing strategy across 1,027 stores.

- June 2025: Satispay introduced an in-app investment service with Amundi, offering a 2.24% return to its 5 million users.

- June 2025: Esselunga launched a USD 73.5 digital voucher program to spur first-time orders on its Esselunga a Casa platform.

- March 2024: Satispay partnered with myPOS, adding 50,000 merchants and targeting USD 565 million in 2026 corporate-welfare volume.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italy e-commerce market as the total gross merchandise value generated when Italian residents or firms purchase goods or services over the internet through computers, smartphones, tablets, voice assistants, or connected TVs. Sales flowing through retailer websites, native apps, marketplaces, travel portals, food-delivery aggregators, and B2B procurement platforms are included because they all settle through standard digital payment rails.

Scope exclusions include informal social-media barters, crypto-only transactions, and government e-procurement portals, which are outside the frame.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type (B2C)

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method (B2C)

- Credit and Debit Cards

- Digital Wallets

- BNPL

- Other Payment Methods

- By Product Category (B2C)

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Italian e-tailers, logistics integrators, payment processors, and digital-policy specialists across Lombardy, Lazio, Campania, and Emilia-Romagna. These conversations validated assumptions on smartphone conversion, BNPL adoption, and regional delivery costs, and they supplied real-time sentiment that balanced the historical desk data.

Desk Research

We started with publicly available macroeconomic series from sources such as the Bank of Italy, ISTAT, Eurostat, and the OECD, then layered in sector-specific material from Netcomm, Ecommerce Europe, and AGCOM to benchmark user penetration, average spend, and mobile-checkout shares. Company filings, investor presentations, and press releases helped anchor merchant revenues, while customs and VAT shipment data clarified cross-border flows. Subscription databases, notably D&B Hoovers for merchant financials and Dow Jones Factiva for deal news, provided further color. The sources listed illustrate our desktop base; many additional references were consulted to validate figures and close data gaps.

Market-Sizing & Forecasting

A top-down reconstruction begins with national private-consumption outlays, which are then split by online penetration, basket composition, and cross-border share; selective bottom-up checks, including merchant roll-ups and sampled ASP × order volumes, calibrate category totals. Key variables in the model include (1) smartphone share of checkout, (2) credit-card and wallet transaction mix, (3) BNPL uptake, (4) parcel-delivery density by province, and (5) PNRR digital-investment disbursements. Multivariate regression with an ARIMA overlay projects each driver and produces the 2025-2030 path, while scenario analysis tests sensitivity to GDP swings and logistics costs.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, analyst peer checks, and a senior sign-off. Figures are reconciled with independent metrics such as postal-parcel counts and VAT e-invoice volumes. We refresh every twelve months, triggering interim updates when material policy or macro shocks occur. Before delivery, an analyst reruns the model so clients receive the freshest view.

Why Mordor's Italy E-commerce Baseline Commands Reliability

Published estimates often diverge because firms choose different scopes, price bases, and refresh cadences.

Key gap drivers include whether services like travel and food delivery are counted, the treatment of cross-border receipts, exchange-rate translation, and how aggressively future digital-wallet usage is ramped. Mordor's definition captures the full GMV universe and applies province-level smartphone, payment, and logistics factors, whereas many studies rely on merchant revenue or limited retail baskets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 110.35 B (2025) | Mordor Intelligence | - |

| USD 93.52 B (2024) | Global Consultancy A | Excludes travel and on-demand food; lower cross-border attribution |

| USD 55.10 B (2024) | Regional Consultancy B | Counts only B2C physical products and uses constant 2022 FX rates |

| USD 0.45 B (2023) | Trade Journal C | Measures platform revenue not GMV; omits marketplace third-party sales |

In sum, our disciplined scope selection, variable-level transparency, and annual refresh cycle deliver a balanced, repeatable baseline that decision-makers can trust for strategic planning.

Key Questions Answered in the Report

What was the value of online retail sales in Italy in 2026?

The Italy E-commerce Market size stood at USD 120.55 billion in 2026.

How fast is Italian B2B e-commerce expanding?

B2B online sales are growing at an 11.87% CAGR through 2031, outpacing consumer growth.

Which device drives most online purchases in Italy?

Smartphones accounted for 56.42% of transaction value in 2025 and continue to gain share.

Why is BNPL important to Italian shoppers?

BNPL volume jumped 46% in 2024 and is forecast to rise at a 13.16% CAGR, offering interest-free installments that appeal to fashion and electronics buyers.

What limits e-commerce growth in southern Italy?

Fragmented last-mile logistics and delivery surcharges of up to EUR 8 per parcel lengthen lead times and reduce adoption.

How do SEPA Instant transfers benefit merchants?

Real-time account-to-account payments bypass card fees and settle funds in seconds, improving margins on low-ticket orders.

Page last updated on: