Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.6 Billion |

| Market Size (2026) | USD 9.04 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Bottled Water Market Analysis by Mordor Intelligence

The Italy bottled water market size is expected to grow from USD 8.6 billion in 2025 to USD 9.04 billion in 2026 and is forecast to reach USD 11.58 billion by 2031 at 5.08% CAGR over 2026-2031. Consumer demand remains resilient even though 99.1% of the country’s tap water complies with health standards[1]Italian National Institute of Health, “Water Quality Compliance Rates in Italy,” pyllola.com. Solid brand heritage, entrenched drinking habits, and the perceived purity of regional sources keep volumes high despite mounting environmental criticism. Tourism revival, premiumization through functional and flavored varieties, and fast-moving sustainability regulations also shape growth trajectories. Producers strengthen competitive positions through recycled-content bottles, blockchain traceability, and product extension into low-calorie or vitamin-fortified lines, all of which reinforce price premiums. Supply-side investments in circular economy infrastructure and digital monitoring support operational efficiency while aligning with upcoming recycled-content mandates.

Key Report Takeaways

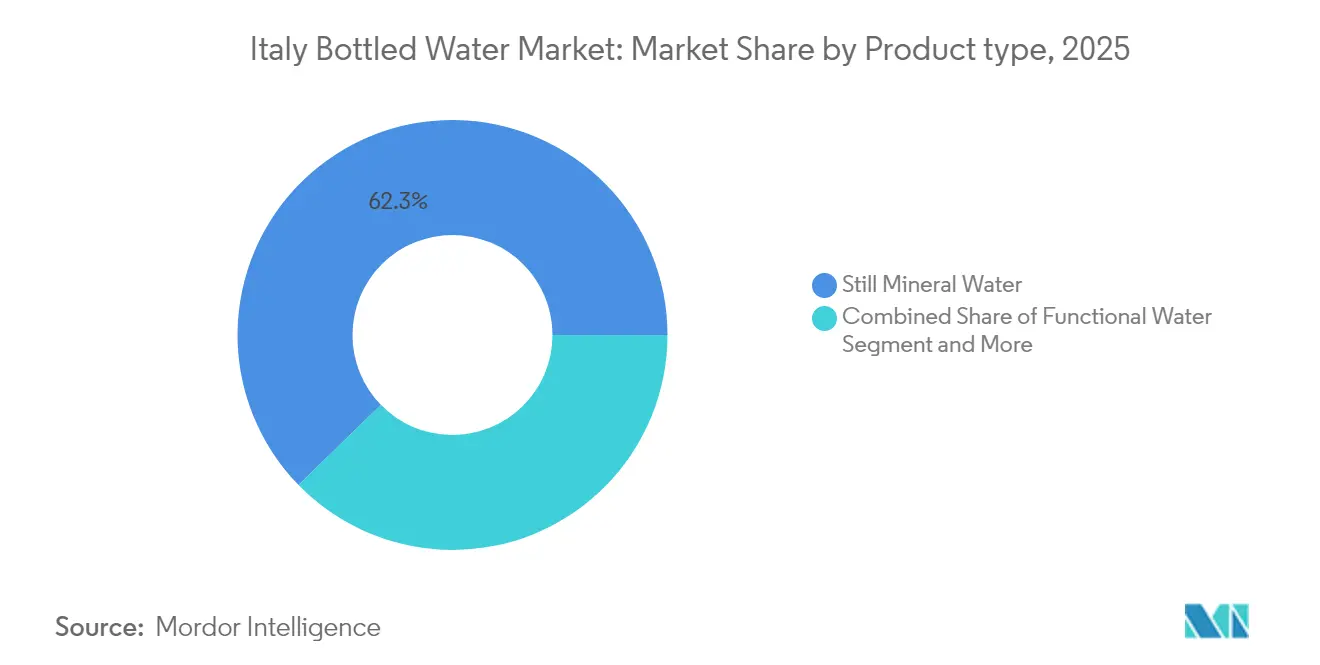

- By product type, still mineral water held 62.30% of the Italy bottled water market share in 2025, whereas functional bottled water is advancing at a 7.27% CAGR through 2031.

- By distribution channel, the off-trade segment accounted for 74.35% of the Italy bottled water market size in 2025, while the on-trade channel is projected to expand at a 5.69% CAGR between 2026 and 2031.

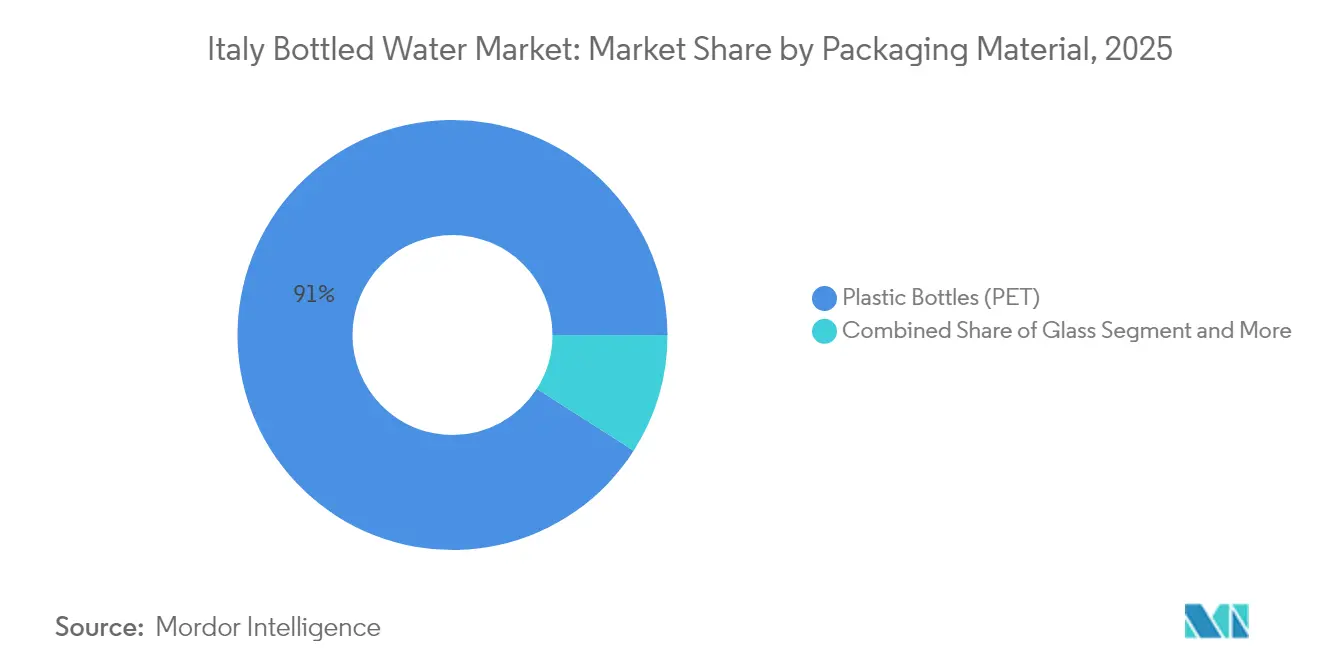

- By packaging material, plastic bottles commanded 90.95% of the Italy bottled water market size in 2025, but alternative formats are rising at an 8.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Bottled Water Market Trends and Insights

Growth in Foodservice Expenditure & Tourism Sector

Italy's hospitality sector recovery post-COVID drives substantial demand for bottled water across restaurants, hotels, and bars, with the on-trade channel demonstrating 5.79% CAGR through 2030. Tourism's resurgence particularly benefits premium water brands positioned in high-end establishments, as international visitors expect consistent quality standards. The sector's expansion creates multiplier effects throughout the value chain, from distribution logistics to packaging requirements. MARR S.p.A., a leading foodservice distributor, reported EUR 1,610.5 million in consolidated revenues for the first nine months of 2024[2]Sistema Distribuzione Informativa Regolamentata, “Interim Report 30 September 2024,” emarketstorage.it, though it noted challenges in the commercial catering segment due to evolving product mix dynamics. The foodservice channel's recovery trajectory suggests sustained momentum as Italy's tourism infrastructure continues to modernize and expand capacity.

Premiumization Through Fortified & Flavored Water

Consumer willingness to pay premium prices for enhanced water products drives the functional bottled water demand, outpacing traditional mineral water growth. This trend reflects broader health consciousness and the desire for products delivering specific wellness benefits beyond basic hydration. Sanpellegrino's launch of the Ciao line of flavored sparkling waters in 2025, featuring four flavors with 10 calories or fewer and no added sugars, exemplifies this premiumization strategy[3]Danielle Oster, “Sanpellegrino Launches Ciao Line,” mediapost.com. The segment's growth potential remains substantial as manufacturers develop increasingly sophisticated formulations targeting specific health outcomes. Regulatory frameworks governing functional claims create barriers to entry that protect established players while rewarding innovation investments.

Rising Health Consciousness & Sugar-Reduction Initiatives

Government health policies, including Italy's sugar tax implementation from July 2025, accelerate consumer migration toward zero-calorie bottled water options. This regulatory intervention complements organic health consciousness trends, creating a dual-catalyst environment for market expansion. Sanpellegrino's proactive reformulation efforts, achieving 40% sugar reduction through stevia substitution, demonstrate industry adaptation to evolving consumer preferences and regulatory requirements. The trend extends beyond product reformulation to encompass broader wellness positioning, with brands emphasizing natural sourcing, mineral content, and functional benefits. Health-conscious consumers increasingly scrutinize ingredient lists and nutritional profiles, rewarding transparency and authenticity in brand communications.

Blockchain-Enabled Source Transparency Adoption

Supply chain transparency emerges as a competitive differentiator, particularly for premium brands targeting health-conscious consumers demanding verifiable quality claims. Blockchain technology enables end-to-end traceability from source to shelf, addressing consumer concerns about water purity and environmental impact. This technological adoption supports premium pricing strategies while building consumer trust through verifiable authenticity. The trend aligns with broader food industry movements toward transparency and traceability, creating opportunities for early adopters to establish competitive moats. Implementation costs remain significant, limiting adoption primarily to larger players with substantial technology investment capabilities.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-waste backlash & shift toward tap water | -0.9% | Italy nationwide, urban areas leading | Short term (≤ 2 years) |

| Stricter EU single-use-plastic regulations | -0.7% | Italy nationwide, EU compliance mandatory | Medium term (2-4 years) |

| Margin pressure from private-label expansion | -0.5% | Italy nationwide, retail channel focus | Medium term (2-4 years) |

| Rapid uptake of domestic micro-filtered dispensers | -0.4% | Urban Italy, affluent households | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Waste Backlash & Shift Toward Tap Water

Environmental consciousness drives increasing consumer resistance to single-use plastic bottles, with Milan's municipal government actively promoting tap water consumption through extensive public fountain networks and educational campaigns. Despite Italy's tap water achieving 99.1% compliance rates for safety parameters, cultural preferences for bottled water persist, though younger demographics show greater willingness to embrace alternatives. The backlash intensifies as environmental awareness campaigns highlight the contradiction between Italy's excellent tap water quality and excessive bottled water consumption. Companies respond through accelerated sustainability initiatives, including increased recycled content and alternative packaging formats, though these solutions require substantial capital investments and may not fully address consumer concerns.

Stricter EU Single-Use-Plastic Regulations

The European Union's comprehensive packaging regulations, including mandatory 25% recycled plastic content and lifecycle sustainability requirements under EU Regulation 2025/40, create significant compliance costs and operational complexity. Italy's additional plastic tax of EUR 0.45 per kilogram of virgin plastic compounds these pressures, forcing manufacturers to accelerate circular economy investments or face margin compression. Regulatory compliance requires substantial capital expenditure for production line modifications, supply chain reconfiguration, and quality assurance systems. The regulatory framework favors larger players with resources to navigate compliance complexity while potentially creating barriers for smaller regional producers. Long-term implications include industry consolidation and accelerated innovation in sustainable packaging alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Waters Drive Innovation

Still mineral water contributed 62.30% of 2025 category revenues, underlining the cultural affinity for minimally processed spring sources anchoring the Italian bottled water market. Leading brands accentuate terroir narratives and low-sodium claims to protect positions even as growth moderates. Functional products, by contrast, are forecast to post the fastest gains at 7.27% CAGR. These fortified lines elevate perceived value by delivering vitamins, collagen, or electrolyte blends, widening price gaps and sustaining premium shelf placement. Ferrarelle’s Vitasnella campaigns underscore detox benefits and sparkling variants that attract image-conscious consumers [ENGAGE.IT]. The Italy bottled water industry exploits this wellness wave by investing in scientific validation and targeted advertising across social media platforms.

Volume acceleration also reflects regulatory tailwinds because fortified waters remain exempt from the forthcoming sugar levy, encouraging retailers to allocate prime space. As formulations grow more sophisticated, makers emphasize natural extracts and clean labels to satisfy EU health-claim rules. Blockchain authentication tools further bolster credibility, ensuring that the Italy bottled water market maintains consumer confidence while charging premium margins.

By Distribution Channel: On-Trade Recovery Accelerates

The off-trade network retained a 74.35% share in 2025 thanks to supermarket multipacks that serve household consumption habits. Private-label penetration deepened as retailers leveraged bargaining power, compressing margins for branded suppliers. Nevertheless, on-trade sales are projected to outpace off-trade through 2031, growing at a 5.69% CAGR on the back of tourism rebound and foodservice modernization. USDA assessments show non-alcoholic beverage exports to Italy climbing 14% in 2023 in anticipation of hospitality demand. Restaurateurs prefer premium glass formats that carry storytelling value, enabling price points substantially above retail. This momentum widens exposure for terroir-focused labels and innovative functional waters positioned as healthier meal accompaniments, thereby refreshing the Italy bottled water market narrative for international visitors.

Digital ordering solutions and QR-code menus further elevate visibility, while experiential dining concepts integrate bespoke water pairings. Supply logistics adapt through specialized distributors focused on maintaining mineral integrity via temperature-controlled fleets. In parallel, convenience-store operators refine assortment strategies by mixing premium singles with value multipacks, preserving the Italy bottled water market relevance across income brackets.

By Packaging Material: Alternative Formats Gain Traction

PET bottles still dominate the Italy bottled water market with 90.95% share because they balance cost, weight, and durability. Producers progressively substitute virgin resin with recycled PET to comply with EU thresholds and company sustainability pledges. Sanpellegrino averages 30% recycled plastic and aims for higher ratios, underscoring long-term investment in closed-loop systems. When sharing sustainability progress, firms leverage lifecycle assessments to illustrate carbon improvements, reinforcing brand equity among eco-minded buyers.

Alternative formats record an 8.49% CAGR as glass, aluminum, and paper-based cartons secure incremental shelf space. Carton water—made up to 83% plant-based materials—satisfies on-the-go consumption while addressing plastic anxiety. Gable-top technology reaches 6,500 cartons per hour, enabling scale economies that shrink price gaps with PET. Premium sparkling varieties retain glass for sensory and prestige advantages, whereas slim aluminum cans resonate with active consumers seeking lightweight and fully recyclable options. Collectively, these shifts help diversify the Italy bottled water market portfolio while supporting national circular-economy targets.

Geography Analysis

Regional consumption patterns mirror economic disparities, tourism flows, and source availability. Northern Italy shows higher uptake of functional and flavored lines due to greater disposable incomes and wellness awareness, driving value growth in Lombardy, Veneto, and Emilia-Romagna. Affluent urban dwellers gravitate toward glass bottlings from Alpine springs, reinforcing price premiums. Southern regions, traditionally loyal to heritage still waters, are gradually experimenting with flavored offerings as retailers expand cold-chain distribution.

Tourism hotspots in Tuscany, Lazio, and along the Amalfi Coast significantly influence on-trade demand peaks during summer. Seasonal inflows elevate sales of premium sparkling formats paired with regional cuisine, ensuring the Italy bottled water market remains intertwined with hospitality fortunes. The national recovery and resilience plan dedicates EUR 20 billion to water infrastructure upgrades, potentially reducing leakage and improving tap-water perception, yet cultural inertia sustains bottled preferences. Municipal campaigns, such as Milan’s fountain network that touts EUR 0.80 savings per 1,000 liters compared with bottled alternatives, encourage refill behavior among students and young professionals, hinting at gradual long-term erosion in PET volumes. Rural areas maintain stronger adherence to local springs, sustaining volumes even where tap water quality matches national standards. Overall, geography-driven nuances reinforce the importance of tailored marketing, distribution flexibility, and region-specific storytelling across the Italy bottled water market.

Competitive Landscape

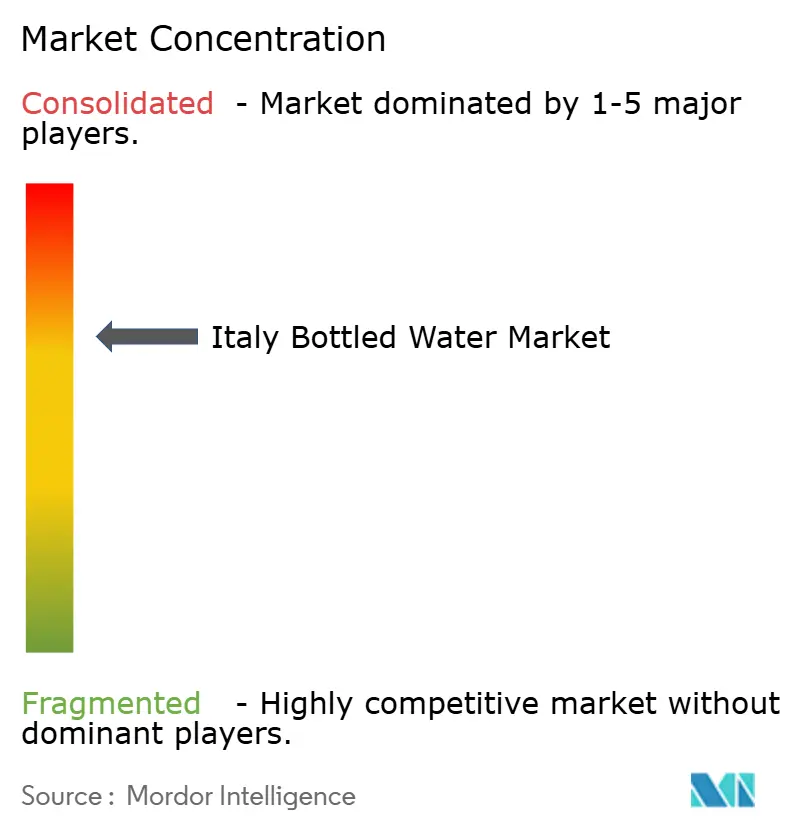

The Italy bottled water market is concentrated, with the top five brands collectively holding about 70%, resulting in a concentration score of 7. Nestlé’s decision to carve out its global waters division, including Sanpellegrino and Acqua Panna, into a standalone entity effective 2025 is designed to enhance category focus and accelerate sustainability investment. Ferrarelle strengthens its share through constant innovation in functional extensions and high-profile endorsements, while San Benedetto expands direct-to-consumer offerings to capture younger audiences.

Quality concerns surfaced in 2024 when Altroconsumo detected TFA contaminants in several labels, prompting Mineracqua to defend existing protocols. The episode underscores reputation vulnerability and motivates firms to adopt advanced testing and blockchain traceability. Meanwhile, environmental scrutiny pushes bottlers to adopt recycled plastic, explore aluminum, and engage in large-scale tree-planting partnerships such as Blupura’s Greenwood pledge to offset 630 tons of CO₂. Ecolab’s acquisition of Barclay Water Management for USD 50 million introduces sophisticated water-safety platforms, likely to raise industry benchmarks for hygiene and compliance.

Strategic whitespace lies in e-commerce subscription models, smart dispensers, and export growth into the broader Mediterranean area where Italian sourcing enjoys premium cachet. Early investments in logistics digitization and circular economy partnerships will separate long-term winners from laggards in the Italy bottled water industry.

Italy Bottled Water Industry Leaders

Nestlé S.P.A

Acqua Minerale San Benedetto

Ferrarelle S.p.A

Fonti di Vinadio

CoGeDi (Uliveto & Rocchetta)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sanpellegrino introduced Ciao flavored sparkling water in four varieties with ≤ 10 calories and no added sugar, starting on Amazon and Publix.

- January 2025: Nestlé finalized the spin-off of its waters portfolio, creating a dedicated company under CEO Muriel Lienau.

- November 2024: Ecolab acquired Barclay Water Management for USD 50 million, integrating proprietary water safety and digital monitoring solutions that could impact bottled water quality assurance standards. The acquisition enhances water safety technologies relevant to bottled water production and distribution.

Italy Bottled Water Market Report Scope

Purified, contaminant-free drinking water packed in bottles is known as bottled water. It is the most practical means for the body to meet its hydration demands and is offered in plastic and glass water bottles. The Italian bottled water market is segmented by type and distribution channel. By type, the market studied is segmented into carbonated bottled water, still bottled water, and flavored/functional bottled water. By distribution channel, the market learned is segmented into on-trade and off-trade channels. under the off-trade channels, the market is segmented into supermarkets/hypermarkets, convenience stores, home and office delivery, and other off-trade channels. For each segment, the market sizing and forecasting have been done in value terms of USD million.

By Product Type

| Still Mineral Water |

| Carbonated/Sparkling Water |

| Flavoured Bottled water |

| Functional Bottled Water |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

By packaging Material

| Plastic Bottles (PET) |

| Glass Bottles |

| Cans |

| Others (Pouches, Cartons) |

| By Product Type | Still Mineral Water | |

| Carbonated/Sparkling Water | ||

| Flavoured Bottled water | ||

| Functional Bottled Water | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By packaging Material | Plastic Bottles (PET) | |

| Glass Bottles | ||

| Cans | ||

| Others (Pouches, Cartons) | ||

Key Questions Answered in the Report

How large is the Italy bottled water market in 2026?

The Italy bottled water market size stands at USD 9.04 billion in 2026.

What is the forecast growth rate for bottled water demand in Italy to 2031?

Sales are projected to expand at a 5.08% CAGR, reaching USD 11.58 billion by 2031.

Which product segment is growing fastest within Italian bottled water?

Functional bottled water is forecast to rise at a 7.27% CAGR through 2031, driven by health and wellness trends.

How will Italy’s plastic tax impact bottled water packaging?

The EUR 0.45 per kilogram levy on virgin plastic raises costs and accelerates the shift toward recycled PET and alternative formats.

Page last updated on: