Polyurea Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

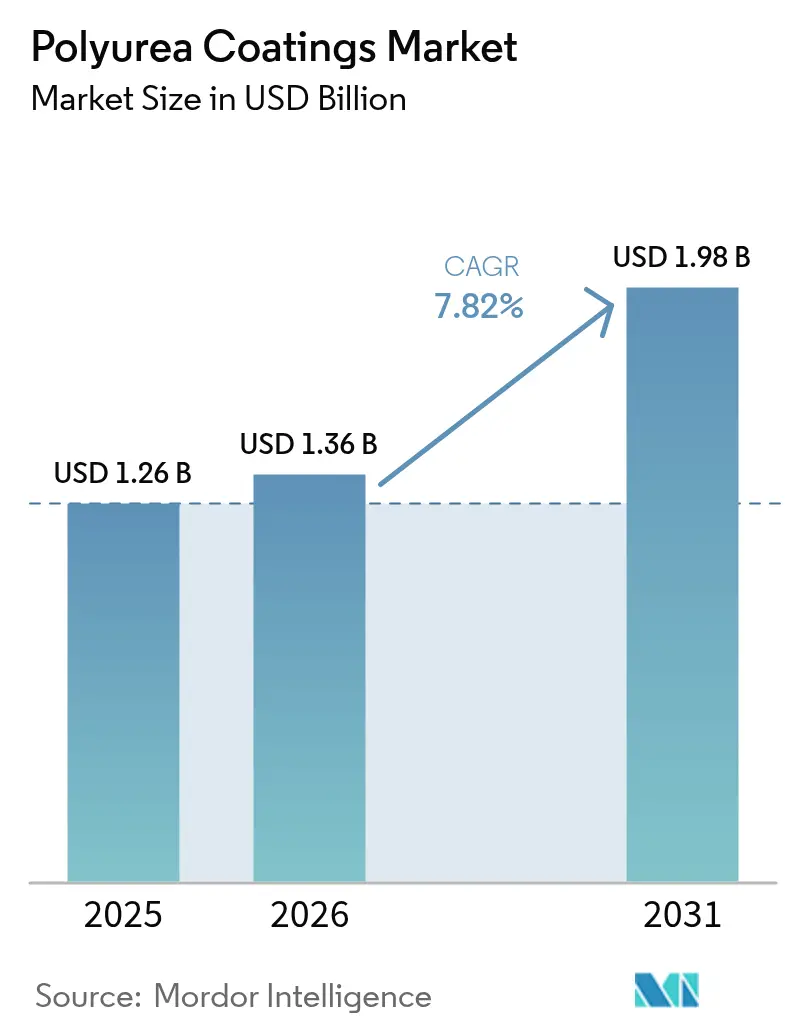

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

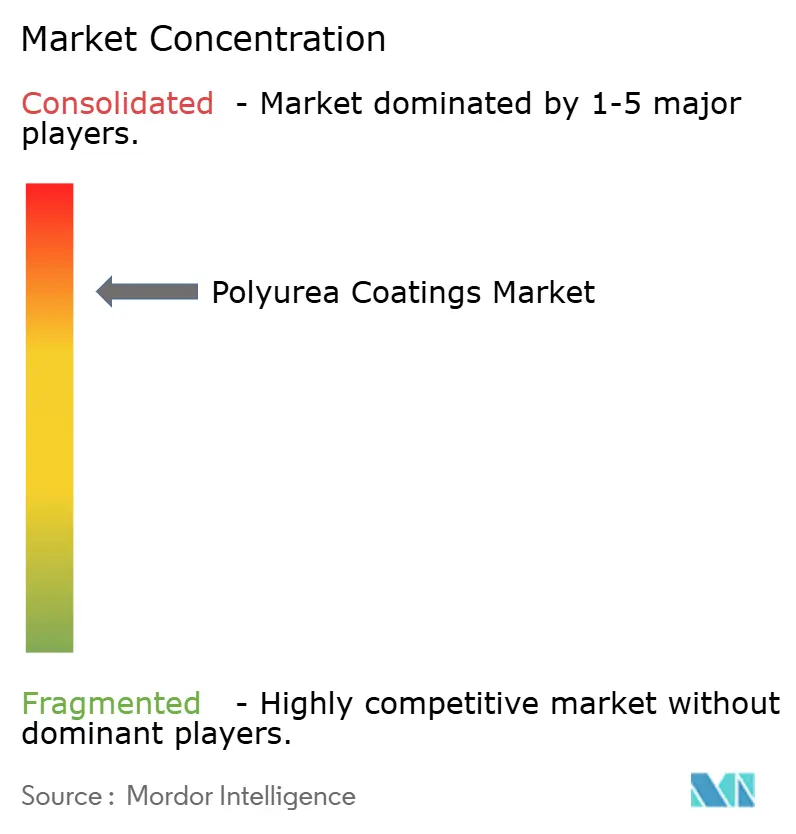

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyurea Coatings Market Analysis by Mordor Intelligence

Polyurea Coatings Market size in 2026 is estimated at USD 1.36 billion, growing from 2025 value of USD 1.26 billion with 2031 projections showing USD 1.98 billion, growing at 7.82% CAGR over 2026-2031. Infrastructure upgrades, industrial-flooring refurbishments, and transportation OEM specifications are widening the application base, while equipment innovations and hybrid formulations are lowering adoption barriers. Competitive dynamics are shifting as leading producers rationalize portfolios and channel investment toward sustainability, positioning advanced polyurea systems as preferred substitutes for epoxy and polyurethane in high-performance settings.

Key Report Takeaways

- By type, pure formulations captured 66.12% of the polyurea coatings market share in 2025, while hybrid variants are forecast to grow at 9.07% CAGR through 2031.

- By technology, spraying led with 69.68% revenue share in 2025, whereas hand-mixing is progressing at 9.46% CAGR to 2031.

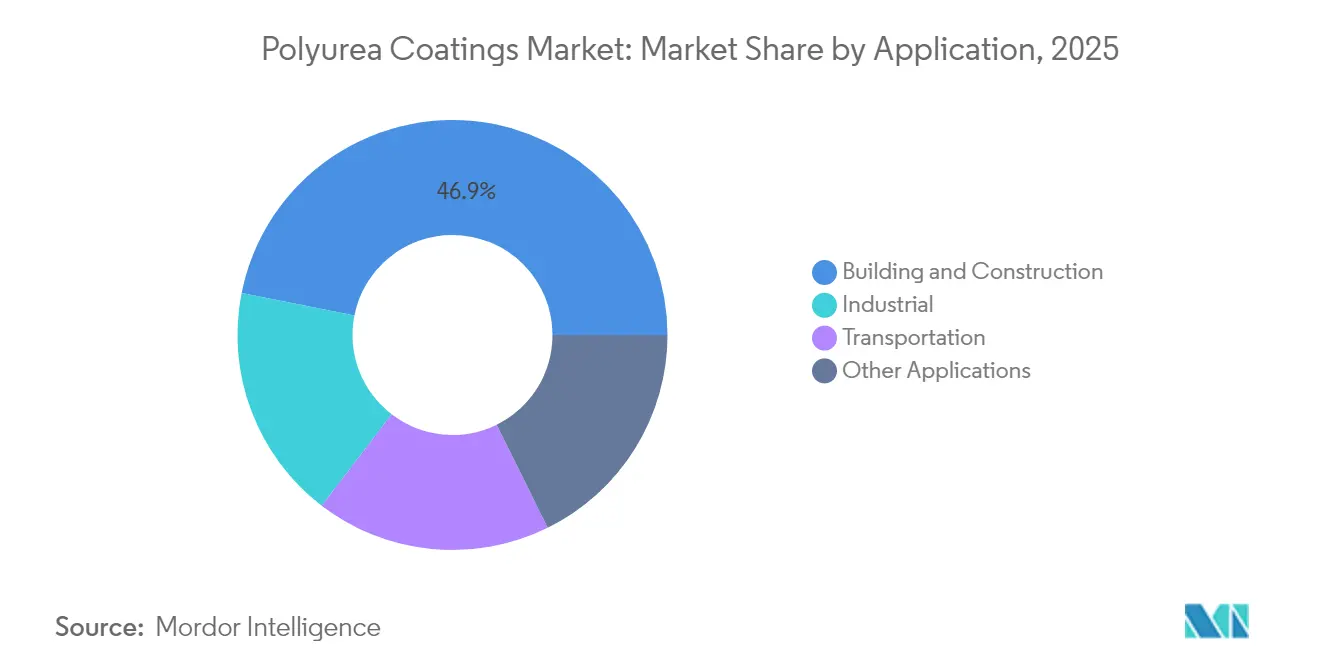

- By application, building and construction accounted for 46.88% of the polyurea coatings market size in 2025, and transportation applications are rising at a 9.18% CAGR through 2031.

- By geography, Asia Pacific commanded 40.85% of the polyurea coatings market share in 2025 and is expanding at 9.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Polyurea Coatings Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding building and construction activities | +2.5% | Global, with APAC core and spillover to MEA | Medium term (2-4 years) |

| Stricter VOC and HAP emission regulations | +1.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Shift from epoxy/PU to higher performance polyurea systems | +1.2% | Global, led by developed markets | Medium term (2-4 years) |

| Industrial flooring upgrades in food and beverage and pharma | +0.9% | North America, EU, and developed APAC markets | Short term (≤ 2 years) |

| Rapid-cure aliphatic polyurea for emergency infrastructure repairs | +0.6% | Global, with focus on aging infrastructure regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Construction Activity

Real-estate spending, infrastructure megaprojects, and urbanization are accelerating polyurea consumption as contractors prioritize coatings that cure within minutes and tolerate wide temperature ranges. Roof restoration, podium waterproofing, and joint sealing benefit from 400% elongation that mitigates crack propagation in seismic and thermal-cycling zones. Prefabricated modules now receive factory-applied polyurea layers, arriving on-site fully cured and reducing labor requirements. Asia Pacific dominates volume because China’s transport corridors and India’s smart-city schemes specify durable membranes, while Middle East mixed-use complexes adopt polyurea for rapid turnaround on tight construction schedules.

Stricter VOC and HAP Emission Regulations

The US National VOC Emission Standards cap industrial-maintenance coatings at 450 g/L, with California enforcing 100–250 g/L, pressuring formulators toward 100%-solids polyurea technologies. EPA’s proposed amendments to polyether-polyol NESHAP are poised to trim hazardous air pollutants by 157 tons annually, tightening upstream supply quality. Similar directives in the EU and South Korea create region-specific compliance hurdles that reward suppliers with robust regulatory affairs capacity. Large enterprises are leveraging green-energy transitions, such as BASF’s full renewable-electricity adoption at key North American sites, to present lower-carbon footprints and win VOC-constrained bids.

Shift from Epoxy/PU to Higher-Performance Polyurea Systems

Asset owners are phasing out epoxy and polyurethane where rapid return-to-service, chemical resistance, or elongation is critical. Automotive OEMs employing 142 million lb of polyurethane in 2023 are testing aliphatic polyurea for underbody exposure and color retention. Wastewater utilities specify pure polyurea linings that bridge active cracks and resist hydrogen-sulfide attack, extending concrete life by multiples[1]Association for Materials Protection and Performance, “Polyurea for Wastewater Infrastructure,” ampp.org. Material-science advances such as optimized 7:3 TDI/MDI blends delivering 52.9 MPa tensile strength are cementing polyurea’s performance edge.

Rapid-Cure Aliphatic Polyurea for Emergency Infrastructure Repairs

Departments of transportation deploy aliphatic formulations for bridge-deck overlays that reopen lanes within hours, preserving traffic flow. Winter work becomes viable because polyurea sprays at –40°F and remains UV-stable in exposed settings. These attributes underpin contingency-repair strategies for pipelines, spill-containment berms, and airport runways pending full reconstruction.

Restraints Impact Analysis of Polyurea Coatings Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High raw-material cost volatility | -1.5% | Global, with acute impact in price-sensitive markets | Short term (≤ 2 years) |

| Requirement for specialized plural-component spray equipment and skills | -0.8% | Developing markets and small contractor segments | Medium term (2-4 years) |

| Poor Color Stability on Exposure to UV Light | -0.7% | Global, particularly in architectural and transportation applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material Cost Volatility

Isocyanate and polyamine feedstocks track oil-price swings, compressing margins when supply tightens. Bio-based polyTHF and recycled-PET polyols promise eventual relief, yet currently command premiums that smaller contractors cannot absorb. Emerging markets such as Indonesia are particularly sensitive to price spikes that stall project awards.

Requirement for Specialized Plural-Component Spray Equipment and Skills

Plural-component rigs exceeding USD 50,000 and requiring precise ratio control limit market access for small applicators. Maintenance and training further raise the entry bar. OEM and association training programs are easing the learning curve, but equipment complexity remains a drag on growth in contractor-dominated regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Polyurea Coatings Market Segment Analysis

By Type:

Performance Leadership of Pure FormulationsPure systems dominated 2025 revenue, claiming 66.12% of demand on the strength of rapid gel times and best-in-class tensile properties. Asset owners in wastewater, chemical processing, and marine sectors increasingly specify pure polyurea to secure 400% elongation and multi-decade service life. Research optimizing isocyanate ratios continues to push performance ceilings, reinforcing customer preference for pure grades in mission-critical environments.

Hybrid grades, while lagging in mechanical attributes, offer compelling economics by incorporating polyol segments and are therefore penetrating residential waterproofing and light industrial flooring at 9.07% CAGR. Suppliers emphasize balanced formulations that meet ASTM C836 waterproofing standards while trimming raw-material spend. This pragmatic approach broadens addressable demand among cost-constrained users without cannibalizing pure-system strongholds.

By Technology:

Spray Dominance with Emerging Hand-Mixing AlternativesSpray application controlled 69.68% revenue in 2025, owing to unmatched productivity on tanks, bridge decks, and large roofs where uniform 1-to-3 mm membranes are essential. Recent plural-pump designs handle 1:1 to 6:1 ratios at 100% solids, permitting jobsite tuning for viscosity and cure speed.

Conversely, hand-mixing’s 9.46% CAGR stems from demand in confined spaces, remote sites, and small-budget projects. Manufacturers introduced cartridge or pail kits that combine extended pot life with safer exotherm control, letting general-contractor crews apply polyurea using rollers or notched squeegees. While thickness uniformity may vary, the approach democratizes access and seeds future conversion to spray once volume scales.

By Application:

Construction Dominance and Accelerating Transportation UptakeConstruction uses captured 46.88% of the 2025 spend as building envelopes, plaza decks, and sub-grade structures employed polyurea to combat water ingress and shorten project cycles. Strict building codes in seismic and hurricane regions now recognize the value of high-elongation membranes that sustain structural movement without cracking.

Transportation, rising at 9.18% CAGR, reflects automotive OEM deployment of aliphatic coatings for underbody abrasion, railcar refurbishment programs, and marine hull protection in saltwater theatres. The adoption curve accelerates as OEMs seek thin-film, solvent-free technologies that align with life-cycle-assessment targets and expedite production-line throughput.

Geography Analysis

APAC Polyurea Coatings Market

Asia Pacific held a 40.85% share in 2025 and records the fastest 9.31% CAGR to 2031. China’s Belt-and-Road corridors and India’s metro-rail extensions specify polyurea for waterproofing tunnels and viaducts, while Japan deploys the material for marine terminals vulnerable to salt-fog corrosion. Indonesia’s coatings market advancing at 6.47% annually underscores regional momentum.

North America Polyurea Coatings Market

North America shows a mature yet resilient appetite anchored in bridge-deck rehabilitation, industrial flooring, and stringent VOC legislation. California’s 100–250 g/L VOC limits and upcoming aerosol-coatings compliance deadline of January 2027 intensify migration toward 100%-solids systems.

EMEA and South America Polyurea Coatings Market

Europe balances stable renovation cycles with advanced environmental compliance demands. Asset owners invest in polyurea overlays for parking structures and potable-water reservoirs to extend service life under EN 1504 guidelines. South America, and the Middle East and Africa collectively advance from a low base; government-led housing and desalination projects create opportunities, but limited contractor training and volatile foreign-exchange conditions temper immediate scaling.

Regulatory Landscape

Polyurea coatings adoption is closely tied to tightening air-emissions rules and evolving coatings standards. In the United States, VOC compliance is anchored in EPA requirements under 40 CFR Part 59, while the EU framework includes Directive 2004/42/EC, reinforcing the shift toward 100%-solids, low-VOC systems that reduce solvent emissions in maintenance and construction coatings.

Across end uses, compliance also spans application and performance standards that influence specifications and contractor practices. AMPP guidance such as SSPC-PA 14-2021 (thick-film polyurea and polyurethane coatings applied with plural-component equipment) is commonly referenced for quality control in field application, while testing and qualification frequently rely on ASTM methods, including ASTM D412 tensile testing and ASTM D4060 abrasion resistance. For potable water contact and hygiene-sensitive environments, projects may require formulations aligned with NSF/ANSI 61, and in China, the rollout of GB 30981.2-2025 (implemented in 2026) adds a new anchor standard for harmful-substance limits in industrial coatings and auxiliary materials used on concrete and metal substrates.

Value Chain Analysis

The polyurea coatings value chain begins with upstream feedstocks and intermediates, led by isocyanates (notably MDI and TDI) and amine-terminated resins and chain extenders, followed by additives for color, UV stability, flame resistance, and processing control. Major upstream chemical producers supply these building blocks into systems houses and formulators that design pure and hybrid polyurea systems. The market then runs through equipment manufacturers (plural-component, high-pressure proportioners and spray guns) and into certified applicators and contractors that execute projects across building and construction, industrial flooring, and transportation.

Constraints and value capture typically concentrate at two points: raw-material availability and pricing, and application capability. Early-2026 actions by key MDI suppliers highlighted upstream sensitivity, including announced MDI price increases during March 2026 (reported for Covestro, Huntsman, and BASF, with BASF also citing East Asia increases for MDI and TDI), which can quickly flow into formulated system pricing and project bid recalibration. On the downstream side, rapid set time elevates the importance of correct mixing ratios and trained labor, so contractor certification programs (via industry bodies and supplier-led training) and distributor technical support function as key enablers, especially in spray-dominant installation workflows.

Competitive Landscape

Market structure is consolidated in nature. Front-runner strategies revolve around vertical integration and end-use specialization. Sherwin-Williams’ purchase of Dur-A-Flex strengthens resinous-floor offerings for food and pharma clients. Innovation pipelines are pivoting toward bio-based, self-healing, and low-temperature-cure platforms. Collaborations with raw-material suppliers ensure backward integration and secure supply of next-generation isocyanates and chain extenders. Distributors such as Univar capture value by bundling technical support, logistics, and regulatory guidance, enabling smaller formulators to reach global OEMs.

Polyurea Coatings Industry Leaders

BASF

Huntsman International LLC

PPG Industries, Inc.

Sika AG

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Polyurea Coatings Market Companies Covered in this Report

- Armorthane

- BASF

- Chemline

- DELTA Coatings International

- Graco Inc.

- Huntsman International LLC

- KUKDO Chemical Co., Ltd.

- Line-X LLC

- MARVEL COATINGS

- Nukote Coating Systems

- Polycoat Products

- PPG Industries Inc.

- Rhino Linings

- Rhino Linings

- Sika AG

- Specialty Products Inc.

- Teknos Group

- The Sherwin-Williams Company

- Ultimate Linings

- VIP Coatings Europe GmbH

Market Opportunities and Future Outlook

White-space is forming around regulatory-driven solvent reduction and specification-led infrastructure protection where fast return-to-service is valued. In North America and Europe, VOC frameworks (including EPA 40 CFR Part 59 and EU Directive 2004/42/EC) align with the technical advantage of 100%-solids polyurea, supporting substitution in industrial maintenance, flooring refurbishment, and waterproofing where downtime costs are high. China also adds a compliance-driven avenue as GB 30981.2-2025 (implemented in 2026) introduces a clearer benchmark for harmful-substance limits in industrial coatings used on concrete and metal, increasing the need for localized formulation documentation and compliant product lines.

Application-led opportunities are also expanding in high-consequence protection and large-scale refurbishment, where owners prioritize durability and rapid cure over traditional membrane systems. For example, defense and critical-infrastructure blast mitigation has become a visible niche, and ArmorThane reported securing more than a dozen blast mitigation contracts across eight countries in April 2026, reflecting active procurement for hardened infrastructure that uses high-performance polyurea systems. Execution capacity remains a near-term gap as industry organizations point to increased emphasis on specialty endorsements and ongoing training needs for plural-component spray technicians, which creates room for suppliers, distributors, and equipment makers to bundle certification, jobsite QA/QC, and application support into their offerings.

Recent Industry Developments in Polyurea Coatings Market

- July 2026: IDI, Insulation Distributors Inc. acquired MCC Equipment & Service Center, expanding its Midwestern footprint for spray foam and polyurea distribution and adding rig-building and service capabilities. The deal strengthens downstream availability of plural-component application equipment and support, which can shorten contractor lead times and improve execution consistency for spray-applied polyurea jobs.

- May 2026: Kimpur announced a strategic partnership with Kobe Polyurethane to collaborate on polyurethane and polyurea system developments. The collaboration targets faster system development and broader formulation options, supporting suppliers and applicators that need tailored performance profiles for waterproofing, industrial maintenance, and specialty protection.

- March 2026: DELTA Coatings International announced global availability of its DELTAShield High Impact Protection (HIP) polyurea systems positioned for blast mitigation in defense infrastructure. The launch broadens commercial access to higher-impact protection systems and signals continued product specialization toward critical infrastructure and security-focused end uses.

Polyurea Coatings Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers revenue generated from polyurea coating materials sold for protective and functional surface coating use, across industrial, construction, and transportation environments, and counted at the point of sale in the value chain.

Scope exclusions: Excludes polyurethane and polyaspartic coating systems that are marketed and sold as non-polyurea solutions, even if they compete in similar protective coating jobs.

Segments Covered in This Report

- By Type

- Pure

- Hybrid

- By Technology

- Spraying

- Pouring

- Hand Mixing

- By Application

- Building and Construction

- Industrial

- Transportation

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping where polyurea coatings are used and which end-use drivers move demand, then translating that into an addressable spend. We rely on public sources such as US Census construction spending, Bureau of Labor Statistics price series for chemicals and construction inputs, UN Comtrade trade flows for relevant chemical categories, and trade bodies that publish protective coatings guidance and related standards context.

We also review company annual reports, investor presentations, product technical data sheets, and trusted press coverage to understand application mix, channel structure, and the specification language used when fast return-to-service is required. Where available, we use paid subscriptions for company financials and intelligence, patent databases to track technology direction, and shipment-level import and export data to sanity-check regional supply availability. These examples are not exhaustive, and many other public and internal reference sources were used to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work was used to pressure-test the demand pool and the pricing logic through interviews and surveys with applicators, distributors, raw material participants, and end users that specify coatings for floors, roofs, tanks, and infrastructure repairs. We also checked regional differences in adoption, with inputs balanced across APAC, EMEA, and the Americas, so the assumptions did not over-rely on one construction cycle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 48% |

| Mid tier: 47% | Functional/Unit leaders: 26% | EMEA: 29% |

| Smaller Players: 14% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand reconstruction, where construction activity, industrial maintenance intensity, and protective coating penetration are translated into an addressable coating spend for polyurea. After forming the demand pool, we convert it into market value using application-level price ranges and mix assumptions that are checked through interviews.

To keep totals realistic, we corroborate the result with selective bottom-up approximations, such as sampled volume by end-use, typical square meters coated per project type, and distributor and applicator channel checks, then adjust when the two views do not align. Key inputs used in the model include infrastructure repair spending trends, industrial flooring refurbishment cycles, corrosion protection requirements in tanks and secondary containment, technology mix between spray and hand-mix application, and the split between pure and hybrid polyurea in mainstream specifications.

For forecasting, we run scenario analysis around construction and industrial capex cycles, then refine the path using a regression check on leading indicators such as construction output and manufacturing activity. When bottom-up proxies are missing for smaller countries, we fill gaps using regional intensity ratios (coated area per unit of construction output) and re-check the implied pricing against interview ranges.

Data Validation & Update Cycle

Outputs are validated through triangulation between the model, independent signals from trade flows and chemical pricing direction, and feedback from primary respondents who sit close to ordering and application activity. Outliers are investigated, and if a country or application category shows an unexpected jump, we review the underlying drivers and assumptions before sign-off.

Each report is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as sharp feedstock price moves, major regulatory changes, or unusual shifts in construction activity. Before delivery, we run a final update pass so clients get the latest consistent view of market size and outlook.

Mordor Intelligence's Polyurea Coatings Market Size Compared With Other Published Estimates

Published market values for polyurea coatings do not always match, and the spread typically comes from different product boundaries, year selection, and the way pricing is projected across applications. Some sources also mix volume and value logic without clearly stating what is being counted, which can move the number materially.

Polyurethane and polyaspartic protective coatings sit outside Mordor Intelligence's scope for this market, which is one reason the 2026 value can look lower than estimates that group adjacent fast-cure coating chemistries together. Another common gap is the base year itself, since some publications anchor on 2024 or 2025 and then extrapolate using a single CAGR, while our build uses application mix shifts such as spray adoption and pure versus hybrid usage to shape the price and volume paths.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.36 B (2026) | |

| Global Research Publisher A | USD 0.94 B (2024) | Uses an earlier base year and a shorter forecast window, and the published view does not clearly show how application mix and technology split are carried into pricing over time. |

| Business Insights Group B | USD 1.02 B (2025) | Positions the market with a 2025 base year and a longer horizon, and it appears to include adjacent coating and sealant framing that can shift what is counted as polyurea coatings revenue. |

Looking across the table, most of the difference can be traced back to what chemistries are bundled together, and which year is treated as the starting point for the forecast. By keeping the scope tied to polyurea coating revenue and by checking assumptions against real adoption signals and interview pricing ranges, we get a practical number that can be re-created and re-checked as conditions change.

Key Questions Answered in the Report

What is the current polyurea coatings market size and growth outlook?

The polyurea coatings market is worth USD 1.36 billion in 2026 and is projected to expand at an 7.82% CAGR to reach USD 1.98 billion by 2031.

Why are companies switching from epoxy or polyurethane to polyurea systems?

Polyurea cures in minutes, resists chemicals, and stretches up to 400%, cutting downtime and extending asset life in demanding environments.

Which region leads demand for polyurea coatings?

Asia Pacific holds 40.85% of global revenue and is growing the fastest at 9.31% CAGR thanks to large-scale infrastructure and construction investment in China and India.

How do VOC regulations influence the polyurea coatings industry?

Strict federal and state VOC limits favor 100% solids polyurea, giving compliant suppliers a competitive edge and accelerating market penetration in North America and the EU.

What key factors are driving market growth through 2031?

Rapid urbanization, stricter emission rules, industrial-flooring upgrades in food and pharma plants, and the need for speedy infrastructure repairs are boosting demand.

Page last updated on: