Conductive Ink Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

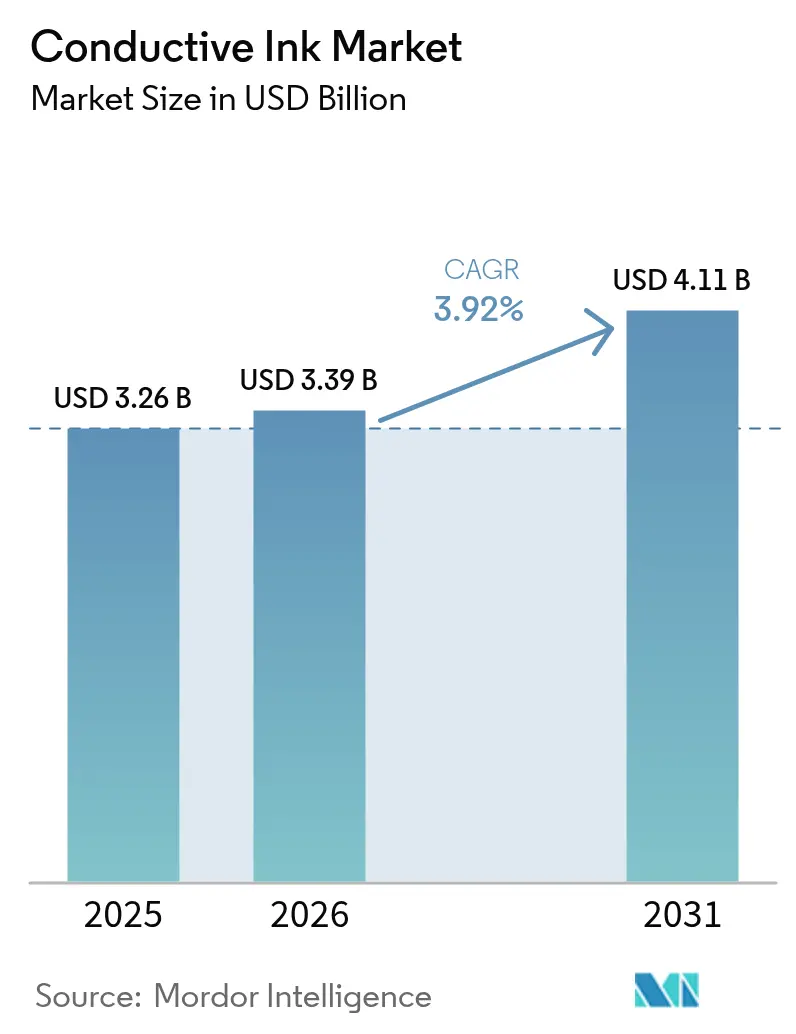

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 4.11 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

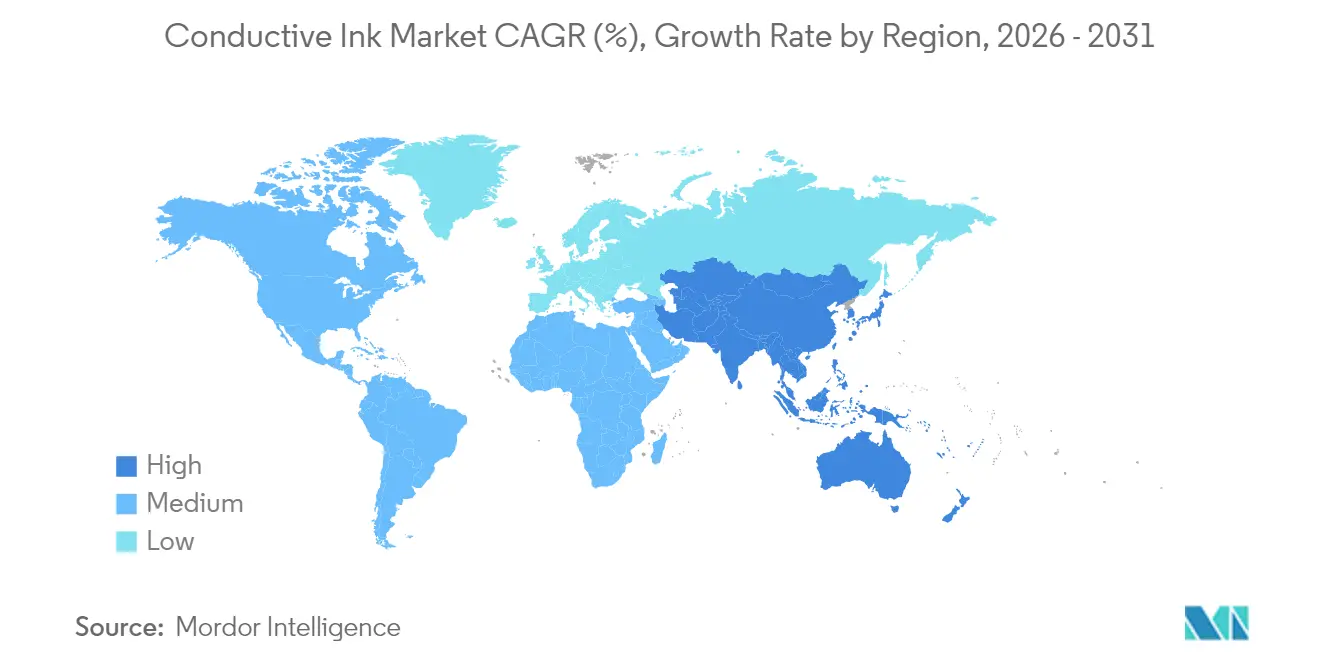

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conductive Ink Market Analysis by Mordor Intelligence

The Conductive Ink Market size in 2026 is estimated at USD 3.39 billion, growing from 2025 value of USD 3.26 billion with 2031 projections showing USD 4.11 billion, growing at 3.92% CAGR over 2026-2031. Steady photovoltaic demand, expanding semiconductor volumes, and the rise of flexible electronics sustain this moderate growth path. Graphene-based formulations open new opportunities by lowering silver use while adding flexibility advantages. Asia-Pacific’s integrated supply chains and renewable-energy policies keep the region at the center of global demand. Meanwhile, cost volatility for silver and copper nudges producers toward hybrid or alternative materials that still meet reliability targets.

Key Report Takeaways

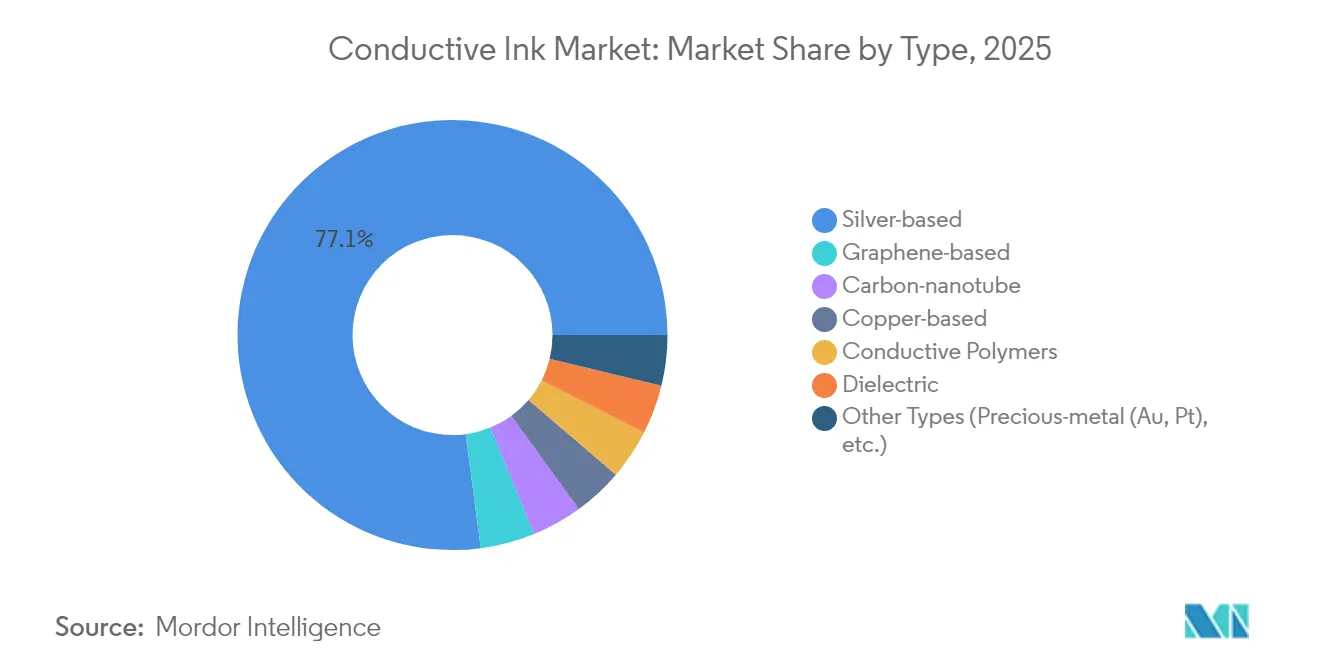

- By type, silver-based inks led with 77.10% of the conductive inks market share in 2025; graphene-based inks record the fastest 4.88% CAGR through 2031.

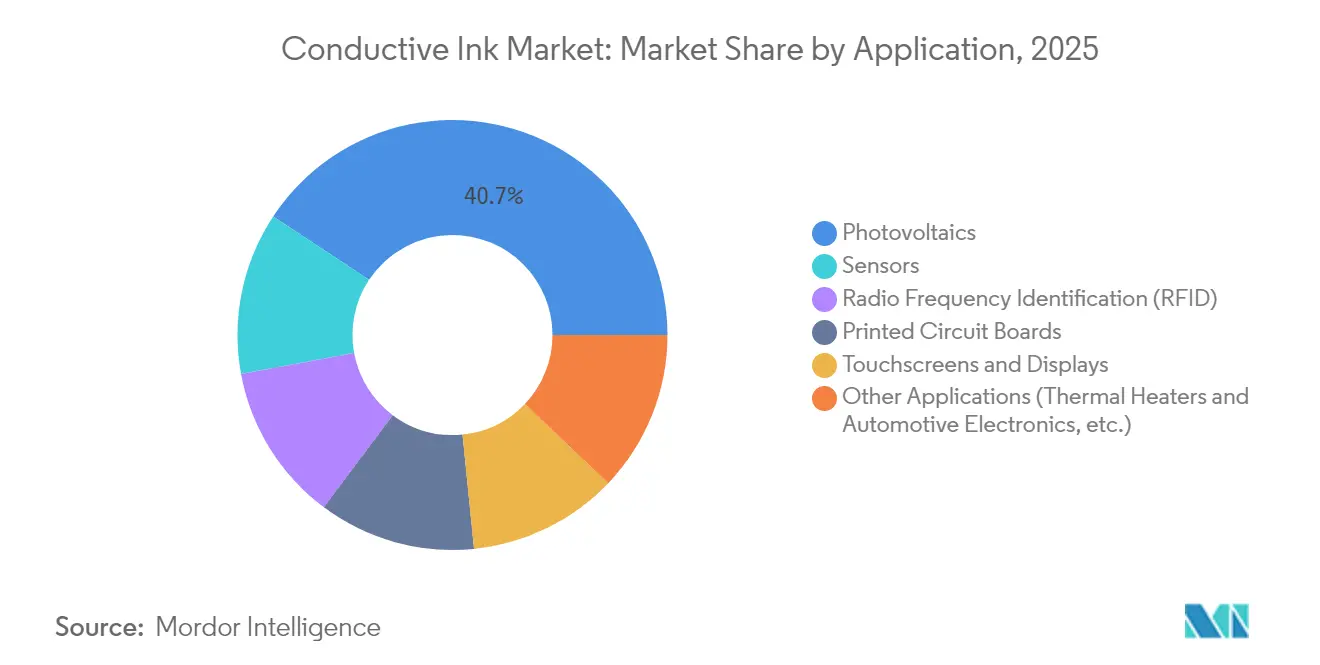

- By application, photovoltaics generated 40.70% revenue in 2025, while sensors exhibit the strongest 4.63% CAGR to 2031.

- By geography, Asia-Pacific held 45.20% of the conductive inks market size in 2025 and remains the fastest-growing region at 4.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Conductive Ink Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing installation of solar panels | +1.20% | China, India, Middle East | Medium term (2-4 years) |

| Rising demand for printed circuit boards | +0.90% | Asia-Pacific, North America, Europe | Short term (≤2 years) |

| Expansion of flexible & wearable electronics | +0.80% | North America, Asia-Pacific | Long term (≥4 years) |

| Automaker shift to silver-nanowire transparent heaters | +0.60% | North America, Europe, China | Medium term (2-4 years) |

| Commercialisation of graphene/silver hybrid low-Ag inks | +0.40% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Installation of Solar Panels

Global solar build-outs keep silver paste consumption rising, with 700 million oz used in 2024, a 7% year-on-year jump. Higher-efficiency N-type cells rely on thicker silver fingers, lifting per-panel ink usage. Chinese and Indian policies that mandate large-scale solar arrays extend the demand pipeline through 2030. The International Energy Agency states that solar will add over 60% of renewable capacity this decade[1]International Energy Agency, “Renewables 2024,” iea.org . Each incremental gigawatt, therefore, translates into heightened conductive inks market demand, reinforcing long-run growth.

Rising Demand for Printed Circuit Boards

High-density interconnect boards need fine-line printing that silver inks deliver, and North American PCB shipments were up 11.3% in February 2025 with a 1.33 book-to-bill ratio. Capacity re-shoring from China to Thailand and Vietnam broadens the Asia-Pacific manufacturing base. HDI expansion aligns with the conductive inks market goal of lowering resistive losses on smaller traces. Quick-turn production cycles also benefit from screen-printed circuits that cut etching steps. As demand keeps exceeding supply, ink suppliers secure multi-year contracts with board fabricators.

Expansion of Flexible & Wearable Electronics

Wearables require inks that stretch yet retain conductivity. Scientific studies report conductive polymers that keep electrical paths intact under repeated flexing[2]MDPI, “Conductive Polymers for Flexible Electronics,” mdpi.com . Printing methods such as inkjet and screen printing reduce fabrication cost for smart textiles and flexible supercapacitors. AI-enabled health trackers connect through these circuits, adding volume to the conductive inks market. The trend moves beyond consumer electronics into soft robotics and biomedical patches, each spawning bespoke ink chemistries.

Automaker Shift to Silver-Nanowire Transparent Heaters

Automotive original equipment makers replace opaque grids with transparent heaters that meet EV efficiency and styling goals. DuPont’s Activegrid ink achieves 93% transmittance while staying under 20 Ω/sq after durability testing. Qualification timelines of three to five years mean programs already initiated will reach mass production before 2030. Transparent heaters also appear in advanced driver-assistance sensors, multiplying unit demand. The automotive vessel thus grows from a niche to a sizable slice of the conductive inks market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in silver and copper prices | -0.80% | Global | Short term (≤2 years) |

| Oxidation & reliability issues in copper-based inks | -0.50% | Global | Medium term (2-4 years) |

| Throughput limits of roll-to-roll graphene ink processes | -0.30% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Oxidation & Reliability Issues in Copper-Based Inks

Copper nanoparticles oxidize quickly, adding resistive layers that undercut circuit performance. Polymer capping reduces oxidation but increases viscosity and print complexity. Advanced binders can hit 158 µΩ·cm resistivity yet require inert reflow ovens that raise capital cost. These processing burdens limit copper’s penetration in high-reliability products such as medical sensors or aerospace circuits, keeping silver ahead despite its premium.

Throughput Limits of Roll-to-Roll Graphene Ink Processes

Current CVD lines top out near 1 m/min before graphene quality degrades[3]Materials Research Society, “Roll-to-Roll CVD Graphene,” mrs.org . Faster runs create smaller crystal domains, cutting sheet mobility. The GRAFOL program invested EUR 10.5 million to close this gap, but commercial high-throughput remains years away. The bottleneck restricts graphene uptake to high-value niches where price tolerates slower output. Until production scales, most of the conductive inks market will stay anchored to metal-based systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Silver Dominance Faces Graphene Innovation

Silver compositions supplied 77.10% of the conductive inks market in 2025, underscoring their unmatched conductivity for photovoltaics and circuit boards. Graphene-based inks, although smaller today, grow at a 4.88% CAGR by offering cost relief and flexibility benefits. Hybrid graphene-silver blends bridge the performance gap, easing the transition away from full-silver pastes. Copper tracks remain limited to low-cost electronics because oxidation needs protective chemistries that raise process steps. Carbon nanotubes and conductive polymer classes serve stretchable, chemical-resistant niches such as e-textiles and bio-patches.

The commercialization push elevates dielectric inks too, which enable multilayer architectures by insulating adjacent traces. Water-based graphene formulations nearing 1.5 × 10⁴ S/m conductivity threaten silver in sensors that can tolerate modest resistance. Precious-metal formulations using gold and platinum stay reserved for aerospace or implantable devices where cost recedes behind mission-critical reliability. Overall, performance, not price alone, dictates selections, securing silver’s lead even as alternatives enlarge the broader conductive inks market.

By Application: Photovoltaics Leadership Drives Sensor Innovation

Photovoltaics accounted for 40.70% of the conductive inks market size in 2025 because each N-type wafer now carries thicker silver fingers to obtain higher cell efficiencies. IoT rollout makes sensors the quickest-rising use case, advancing at 4.63% CAGR through 2031 as health patches and industrial monitors shrink and flex. RFID tags sustain incremental demand from logistics digitization, while touchscreens plateau with smartphone saturation.

AI inference at the edge compels robust thermal pathways, nudging designers toward inks with improved heat dissipation. Biocompatible graphene systems open fresh lanes in wearable medical electronics where metal allergies restrict silver usage. Automakers explore in-mold electronics for cockpit controls, another channel that favors printable circuits. As each emerging use arrives, it enlarges the conductive inks market, creating a rolling wave of opportunities rather than a single dominant growth spike.

Geography Analysis

Asia-Pacific commanded 45.20% of 2025 revenue and posts a 4.58% CAGR through 2031. China’s renewable mandates, India’s giga-factory buildout, and South Korea’s chip packaging boom form a self-reinforcing ecosystem. Japan supplies specialty pastes and printer heads that tune performance. Thailand and Vietnam absorb capacity as brands mitigate geopolitical risk, yet remain within the regional value network. Such clustering compresses logistics costs and accelerates product iteration, advantages difficult for other regions to replicate.

North America follows, supported by policy incentives that favor domestic EV supply chains and defense electronics. The CHIPS Act allocates capital for new fabs, bringing printed interposer demand in-house. Automotive suppliers adopt transparent heaters and battery management circuits that rely on silver and graphene inks. Regulations emphasize critical material security, pushing ink firms to source regionally or recycle metals as Henkel now demonstrates. Europe prioritizes sustainability, valuing water-based chemistries that comply with REACH and RoHS. OEMs develop circular design guidelines that specify recyclable pastes. Electric vehicles lead adoption of advanced battery current collectors that need low-resistance printable materials. Meanwhile, South America and the Middle East & Africa see rising solar farm investments, but limited local converting means many inks still arrive from Asia-Pacific or Europe. These emerging markets extend the geographic footprint of the conductive inks market yet do not displace existing regional leaders.

Competitive Landscape

The conductive inks market remains moderately fragmented. Barriers include deep materials science know-how, pilot-line validation capacity, and global service networks. DuPont, Henkel, Sun Chemical, and Heraeus leverage vertical integration from powder metallurgy to application engineering, giving them an edge in turnkey support. Patent estates fortify positions by limiting rivals’ formulation windows.

Innovation now centers on cost reduction and environmental compliance. Henkel’s 2025 launch of recycled-silver inks shows how incumbents pivot to greener inputs while protecting performance. DuPont prepares to spin off its electronics unit as Qnity, sharpening its focus on advanced materials for displays and automotive glazing. Start-ups such as Haydale push plasma-functionalized graphene that drops silver loadings without performance loss. Partnerships between printhead makers and ink formulators quicken adoption because co-development slashes line-qualification times.

Supply-chain resilience has become strategic. Large players multisource silver and invest in regional paste manufacturing to cushion logistics disruptions. Smaller firms differentiate by quick customization for niche IoT or biomedical projects, slipping under the radar of larger competitors. M&A activity is poised to rise as established vendors acquire technology boutiques to fill capability gaps. The shift toward hybrid chemistries suggests the next competitive frontier is tuning metal-carbon synergies rather than an outright switch away from precious metals.

Conductive Ink Industry Leaders

DuPont

Henkel AG & Co. KGaA

Heraeus Holding

NovaCentrix

Sun Chemical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Henkel unveiled the industry's first silver inks utilizing recycled silver at LOPEC 2025, enabling the production of highly conductive printed circuits for smart surfaces. This breakthrough is poised to enhance sustainability and innovation within the conductive inks market, fostering the adoption of environmentally friendly technologies.

- September 2024: DuPont introduced its silver nanowire technologies at SID Vehicle Displays and Interfaces 2024, expanding its portfolio into transparent conductive materials for automotive and consumer electronics. Key innovations include Activegrid ink for transparent heaters and OLED displays, and Activegrid ink LT for low-temperature curing on sensitive substrates.

Global Conductive Ink Market Report Scope

Conductive ink is an ink that results in a printed object which conducts electricity. These are produced by infusing graphite or other conducting materials into ink. These find application in photovoltaics, sensors, PCBs, and Radio Frequency Identification (RFID), among others.

The conductive ink market is segmented by type, application, and geography. By type, the market is segmented into silver-based, copper-based, graphene-based, carbon nanotubes, dielectric, conductive polymers, and other types (gold and platinum-based, etc). By application, the market is segmented into photovoltaics, radio frequency identification (RFID), sensors, touchscreen and displays, printed circuit boards, and other applications (digital printing, aerospace, etc). The report also covers the market size and forecasts for the conductive inks market in 15 countries across major regions.

For each segment, the market sizing and forecasts have been done based on value (USD).

| Silver-based |

| Copper-based |

| Graphene-based |

| Carbon-nanotube |

| Conductive Polymers |

| Dielectric |

| Other Types (Precious-metal (Au, Pt), etc.) |

| Photovoltaics |

| Radio Frequency Identification (RFID) |

| Sensors |

| Touchscreens and Displays |

| Printed Circuit Boards |

| Other Applications (Thermal Heaters and Automotive Electronics, etc.) |

| Asia-Pacifc | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Silver-based | |

| Copper-based | ||

| Graphene-based | ||

| Carbon-nanotube | ||

| Conductive Polymers | ||

| Dielectric | ||

| Other Types (Precious-metal (Au, Pt), etc.) | ||

| By Application | Photovoltaics | |

| Radio Frequency Identification (RFID) | ||

| Sensors | ||

| Touchscreens and Displays | ||

| Printed Circuit Boards | ||

| Other Applications (Thermal Heaters and Automotive Electronics, etc.) | ||

| By Geography | Asia-Pacifc | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the conductive inks market?

The conductive inks market is valued at USD 3.39 billion in 2026 and is projected to reach USD 4.11 billion by 2031.

Which segment holds the largest conductive inks market share?

Silver-based inks lead with a 77.10% share in 2025, largely due to their use in photovoltaic cells.

Which application is growing fastest within the conductive inks market?

Sensor applications grow at a 4.63% CAGR through 2031 as IoT and wearable devices proliferate.

Why is Asia-Pacific dominant in the conductive inks market?

The region hosts integrated electronics supply chains, strong renewable-energy targets, and supportive government policies, resulting in 45.20% revenue share in 2025.

How are raw material price swings affecting the conductive inks industry?

Volatile silver and copper prices pressure margins, pushing suppliers to adopt hybrid or recycled materials and dynamic pricing models.

Page last updated on: