Market Overview

| Study Period | 2020 - 2031 |

|---|---|

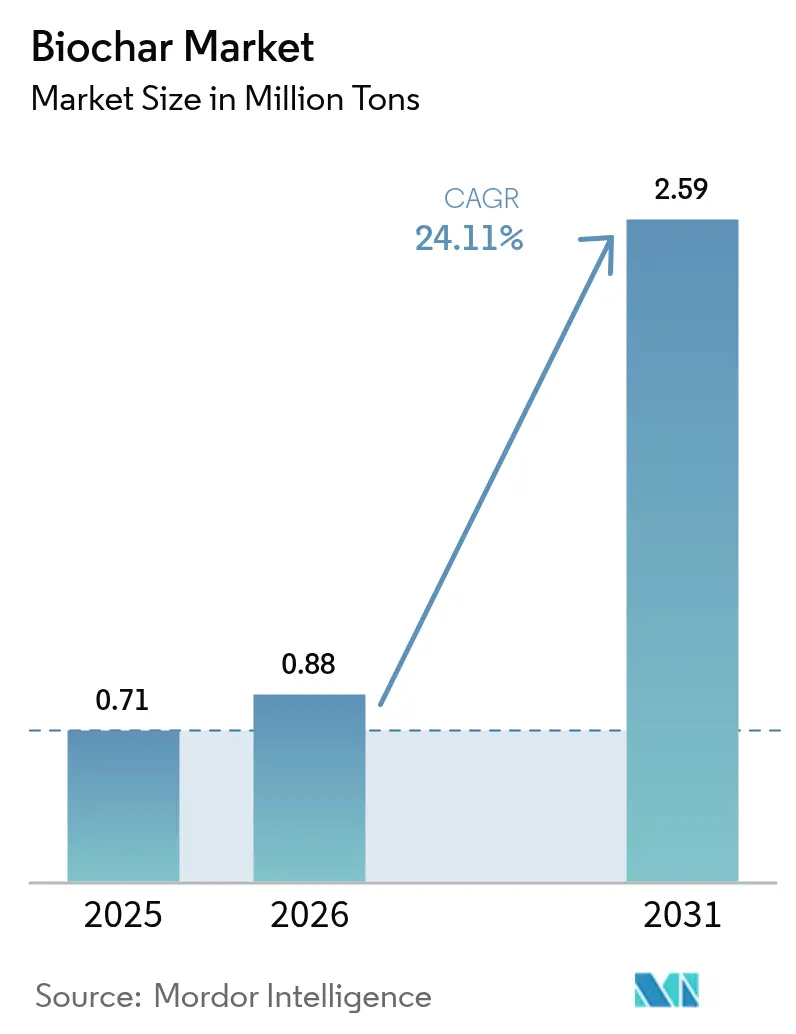

| Market Volume (2026) | 0.88 Million tons |

| Market Volume (2031) | 2.59 Million tons |

| Growth Rate (2026 - 2031) | 24.11% CAGR |

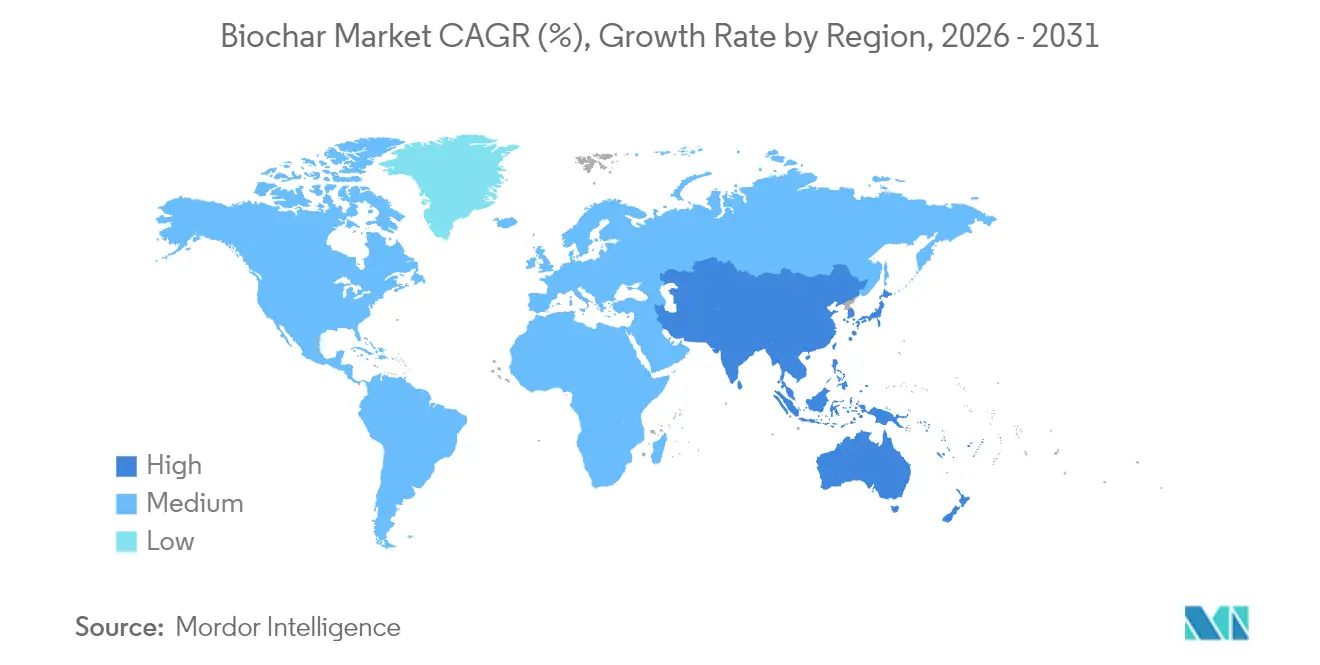

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biochar Market Analysis by Mordor Intelligence

Biochar market size in 2026 is estimated at 0.88 Million tons, growing from 2025 value of 0.71 Million tons with 2031 projections showing 2.59 Million tons, growing at 24.11% CAGR over 2026-2031. Rapid scale-up is tied to supportive climate policies, the need for negative-emission technologies, and mounting pressure on agriculture to restore soil health. Premium carbon-credit pricing, a widening set of industrial use-cases, and technology advances that cut unit costs are expanding revenue streams and improving project bankability, especially in regions with clear carbon-removal protocols. Asia-Pacific leads today’s biochar market with an estimated 40.26% volume share, while robust government incentives in North America and the European Union encourage new capacity additions. Feedstock diversification away from high-cost woody biomass toward agricultural residues is easing long-standing supply constraints. At the same time, distributed pyrolysis units are shrinking logistics distances and lowering scope-3 emissions, reinforcing biochar’s climate credentials.

Key Report Takeaways

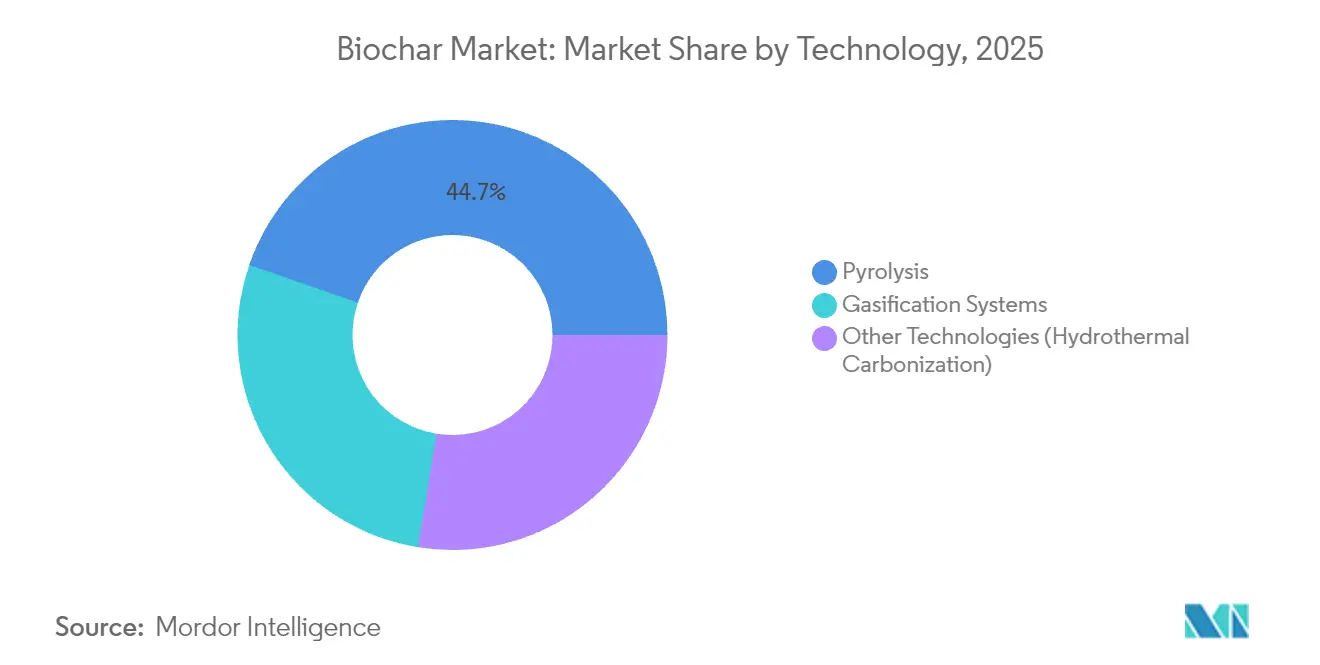

- By technology, pyrolysis accounted for 44.72% of biochar market share in 2025, whereas other technologies are forecast to expand at a 24.63% CAGR to 2031.

- By feedstock, woody biomass led with 61.15% share of the biochar market size in 2025, while agricultural residues are projected to grow at 25.05% CAGR through 2031.

- By form, powder products dominated with 43.25% share of the biochar market in 2025; liquid suspensions are set to register a 24.21% CAGR to 2031.

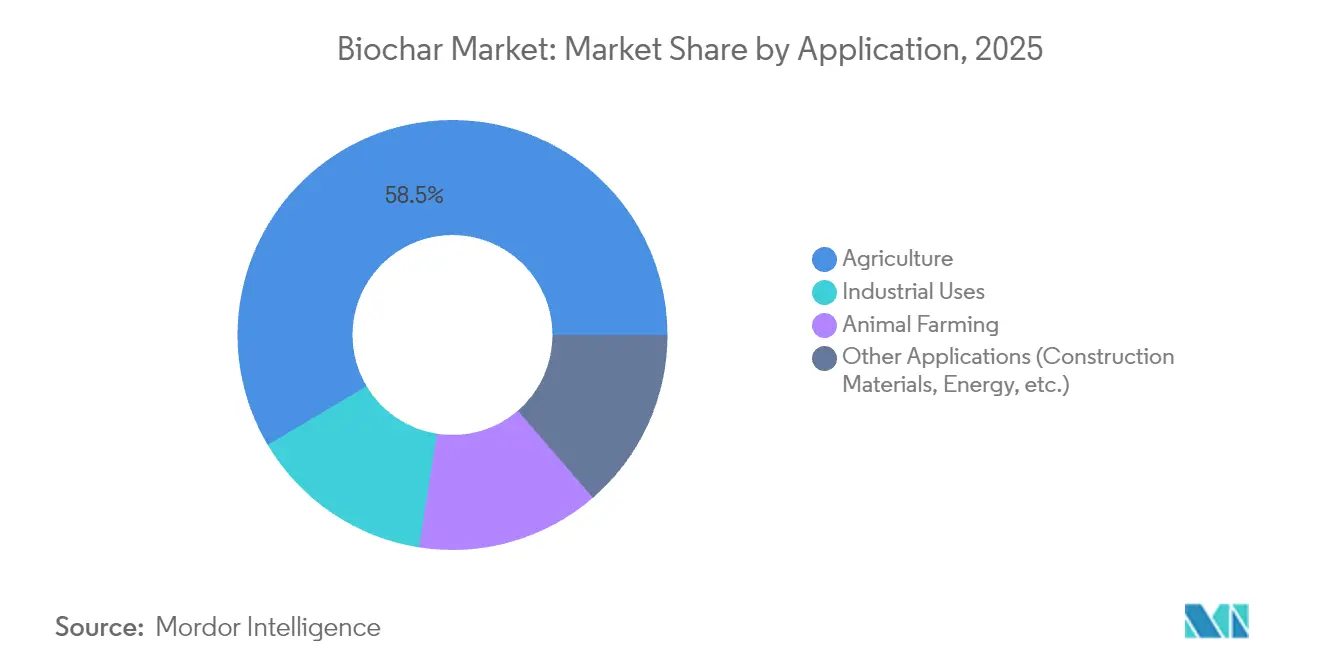

- By application, agriculture held 58.54% share of the biochar market in 2025, yet industrial uses are on track for the fastest 25.1% CAGR over the same period.

- By geography, Asia-Pacific captured 39.88% of global volume in 2025 and is also expected to log the quickest 24.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biochar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand from Organic and Regenerative Farming | +6.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Government Incentives for Negative-Carbon Materials and Waste Valorization | +7.8% | North America, EU, China | Short term (≤ 2 years) |

| Carbon-Credit Monetisation for Soil Sequestration Projects | +5.4% | Global, led by North America and EU | Medium term (2-4 years) |

| Expanding Horticulture and Greenhouse Adoption | +3.1% | North America, EU, Japan | Long term (≥ 4 years) |

| Biochar-Enhanced Asphalt and Concrete for Green Construction | +2.1% | Global, early adoption in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Organic and Regenerative Farming

Organic farmers are replacing synthetic inputs with biochar as they chase higher soil-organic-carbon scores required for premium certification. Twenty US states have already activated the NRCS Soil Carbon Amendment 808 standard, which reimburses growers for verified biochar applications[1]Natural Resources Conservation Service, “Soil Carbon Amendment 808 Practice Standard,” usda.gov . Yield trials show first-year productivity gains near 9% and cumulative boosts that exceed 20% after six seasons, especially in nutrient-poor soils. Biochar qualifies for use in USDA-certified organic systems when sourced from untreated biomass, a rule that removes a major market barrier and supports premium pricing. The cascading-use concept—deploying biochar first in filtration or livestock bedding and later reincorporating it into fields—multiplies income streams and aligns with circular-economy mandates. As input prices remain volatile, growers view biochar as a hedge that locks in stable nutrient supply and long-term carbon credits.

Government Incentives for Negative-Carbon Materials and Waste Valorization

Policy levers are accelerating demand. The Inflation Reduction Act broadened Section 45Q and 45V tax credits to include carbon-utilisation pathways, letting qualified biochar facilities claim monetisable certificates once lifecycle analyses are filed with the IRS. In parallel, the European Commission’s Carbon Removal Certification Framework is drafting biochar-specific quantification rules that should standardise permanence proofs and attract institutional capital. Several US states, notably Washington, have legalised flame-cap kilns under updated clean-air codes, clearing the way for distributed production models that shorten feedstock haulage. These incentives lower compliance risk and improve debt-service coverage ratios, nudging private investors toward large-scale projects.

Carbon-Credit Monetisation for Soil Sequestration Projects

Durable-removal buyers prefer biochar credits because independent studies peg carbon-storage horizons at well over 100 years, outlasting most forestry offsets. In 2024, biochar accounted for 94% of verified durable-removal tonnes delivered into the voluntary market. Corporate purchasers such as Microsoft and JPMorgan continue to sign multi-year forward contracts priced above USD 100 per tonne CO₂e, providing revenue certainty that supports construction-phase financing. New registry protocols in the United States and Canada cut transaction costs by streamlining monitoring, reporting, and verification procedures. As price transparency improves, originators can bundle credits with physical product sales, raising margins without sacrificing liquidity.

Expanding Horticulture and Greenhouse Adoption

Peat-free mandates in the European Union and proposed restrictions in several US states push commercial growers toward sustainable substrates. Scientific trials confirm that biochar can displace up to 80% of peat in nursery mixes while maintaining—or even enhancing—root development across multiple ornamental species. Because peatland drainage releases substantial CO₂ and threatens biodiversity, regulators view biochar as an immediate substitute that carries a negative-emission profile. Greenhouse operators also benefit from local sourcing that cuts freight bills on bulky growing media. Industry surveys show that substrate cost savings can reach 15-20% when biochar replaces imported peat, a differential that scales with greenhouse acreage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Logistics Costs | -4.7% | Global, particularly acute in remote areas | Short term (≤ 2 years) |

| Availability of Low-Cost Substitutes | -2.8% | Global, varying by application | Medium term (2-4 years) |

| Regulatory Ambiguity on Fertiliser Registration | -1.9% | North America, EU, emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production and Logistics Costs

Unit economics remain challenging because feedstock, preprocessing, and thermal conversion each add sizeable cost blocks. Academic cost curves place fully-loaded production between USD 106 and USD 170 per ton depending on moisture content, plant scale, and regional energy tariffs[2]College of Food, Agricultural, and Environmental Sciences, “Techno-Economic Assessment of Biochar Production,” osu.edu . Low bulk density means a 40-foot container carries far fewer tonnes of biochar than of synthetic fertiliser, inflating per-tonne freight costs on long-haul routes. Producers either adopt mobile pyrolysis units that follow feedstock sources or build rail-linked hubs to capture logistics efficiencies, yet both strategies demand capital outlays that small operators struggle to finance. Until automated, high-throughput plants gain traction, scale economies will arrive slowly.

Availability of Low-Cost Substitutes

Compost, manure, and peat remain entrenched in agronomy and horticulture because they deliver familiar performance at lower purchase prices. Activated carbon dominates water-treatment tenders owing to precise specification standards and global supply chains that guarantee availability. In concrete, fly ash and ground-granulated blast-furnace slag already serve as supplementary cementitious materials, offering well-documented performance data that engineers trust. Each substitute erodes potential demand where biochar’s co-benefits lack explicit monetary value, forcing producers to compete on delivered-price parity or to bundle carbon-credit upside into sales contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Pyrolysis Retains an Economic Edge but Faces Rapid Diversification

Slow and intermediate pyrolysis systems held 44.72% of biochar market share in 2025 thanks to reliable throughput, flexible feedstock windows, and a coproduct slate that includes bio-oil and syngas. These attributes let operators layer electricity or heat revenue onto core biochar sales, raising overall project internal-rate-of-return figures. Capital-intensive rotary-kiln designs dominate high-volume installations, while smaller retort units serve on-farm programmes that target regenerative agriculture. The wider diffusion of continuous-feed reactors has triggered process-control improvements, enabling better yield consistency and tighter emissions control, an aspect that simplifies permitting in air-quality-sensitive regions.

Alternative routes are gaining mindshare because they process high-moisture substrates without costly pre-drying. Hydrothermal carbonisation runs at 180–260 °C and converts sewage sludge into carbon-rich hydrochar suitable for soil amendment or energy applications. Gasification systems, though producing lower char yields, integrate readily with combined-heat-and-power modules, allowing municipal waste managers to transform refuse into baseload electricity and char by-products. R&D consortia in Japan and Germany are piloting microwave-assisted pyrolysis that promises higher energy efficiency and reduced residence times, innovations that could narrow cost gaps against incumbent thermochemical options. Over the forecast window, these emerging systems are anticipated to grow at a 24.63% CAGR, gradually diluting pyrolysis dominance yet collectively lifting the biochar market size as new feedstock classes come online.

By Feedstock: Agricultural Residues Claim Momentum amid Stable Woody Supply Chains

Woody biomass provided 61.15% of total volume in 2025 due to reliable forestry residues, uniform particle sizes, and chemical compositions that yield predictable char quality. Timber-rich geographies such as British Columbia and Scandinavia run dedicated thinning programmes to mitigate wildfire risk, generating a continuous stream of low-value residues that biochar plants can secure on multi-year contracts. High lignin content in conifer fractions also enhances fixed-carbon percentages, a metric prized by carbon-credit auditors for permanence calculations.

The competitive landscape is shifting as corn stover, rice husks, and sugarcane bagasse enter commercial supply agreements. Mobile torrefaction and pyrolysis rigs have demonstrated the logistical viability of converting loose residues where they are generated, bypassing costly bale transport. Agricultural residues are forecast to expand at 25.05% CAGR to 2031, helped by waste-burn bans and landfill taxes that tilt economics toward valorisation. Sewage sludge and animal manure offer nutrient-enriched end-products but must clear tighter contaminant hurdles under European fertiliser regulations. Large urban centres in Brazil and India are exploring public-private partnerships that marry wastewater treatment, renewable power, and biochar credit sales, pointing to an eventual broadening of feedstock portfolios across the biochar market.

By Form: Liquid Suspensions Rise as Precision-Application Demands Intensify

Powder biochar retained leadership with 43.25% share in 2025, a status owed to conventional spreading equipment compatibility and relative ease of bulk handling in grain-belt economies. Particle-size optimisation around the 1–5 mm range strikes a balance between surface area and wind-loss risk, which is critical for side-dress operations. Pelletised formats, though higher in manufacturing cost, suit horticulture blends where uniformity and low dust are paramount.

Liquid suspensions, forecast to clock a 24.21% CAGR, promise new efficiencies. Producers micronise char to sub-100-micron particles, emulsify them with organic binders, and supply growers who already rely on drip-line fertigation. Field trials show faster infiltration and better root-zone distribution compared with granular products, which translates into lower per-hectare dosage rates. The format mitigates occupational dust exposure and allows co-formulation with micronutrients or microbial inoculants, sharpening competitive differentiation. As irrigation-water availability tightens in arid zones, the ability to deliver soil amendments through existing drip infrastructure will likely cement liquid biochar as a mainstream option, gradually lifting its share of the broader biochar market.

By Application: Agriculture Anchors Demand, while Industrial Use-Cases Accelerate

Agriculture accounted for 58.54% of deployed volumes in 2025, reflecting decades of academic field trials that document yield boosts, moisture retention, and microbial-activity gains on marginal soils. Public cost-share programmes further buttress uptake by underwriting the initial treatment expense for growers who validate soil-organic-carbon increases. Precision-ag platforms now bundle variable-rate biochar prescriptions into digital agronomy services, thereby lowering application costs and offering data-rich verification packages for carbon-credit issuances.

Beyond the farmgate, industrial applications are set to grow at 25.1% CAGR, pushing the biochar market into new revenue verticals. Water-utility pilots report heavy-metal and PFAS removal efficiencies above 90%, a performance that competes favorably with virgin activated carbon at lower embodied-carbon scores. Construction companies have co-designed mix designs where 4-10% by weight of cement is replaced with biochar, achieving compressive-strength parity alongside embodied-carbon cuts approaching 25% per cubic metre of concrete. Steelmakers in South Korea and Austria are evaluating injection-grade biochar that partially offsets pulverised coal in blast-furnace operations, a pathway that supports scope-1 decarbonisation targets in a hard-to-abate sector. Collectively, these industrial proofs-of-concept expand total addressable volume and diversify revenue streams beyond cyclical agricultural demand.

Geography Analysis

Asia-Pacific captured 39.88% of global shipments in 2025, reflecting an abundant biomass resource base, emerging carbon-removal targets, and generous public R&D funding. China alone publishes over 200 peer-reviewed biochar papers each year, underpinning its leadership in reactor design, agronomic testing, and carbon-credit protocol development. Provincial subsidies lower the capital cost of rural pyrolysis units, enabling small municipalities to turn crop residues into products that meet national soil-restoration goals.

North America ranks second in volume but leads in commercial carbon-credit transactions. High-profile corporate offtake agreements, including Microsoft’s multi-year procurement of 95,000 tCO₂e from Pacific-Northwest facilities, provide predictable revenue tails that derisk debt financing. Federal incentives—ranging from production tax credits to USDA cost-share grants—further catalyse plant-level investment. Although the region’s mature regulatory framework accelerates deployment, growth rates will moderate compared with emerging Asia because early movers have already secured a large share of easily accessible feedstocks.

Europe clusters around quality standards and policy alignment. Draft EU rules governing carbon-removal verification encourage member states to harmonise methodologies, facilitating cross-border trade in removal credits. Scandinavian countries, confronted with stringent national net-zero deadlines, are testing district-heating link-ups where waste-wood pyrolysis supplies both thermal energy and high-carbon biochar. Meanwhile, Latin America and Sub-Saharan Africa present long-term upside tied to abundant agricultural residues yet lag on financing and infrastructure. Development-finance institutions are piloting blended-capital funds that could unlock these frontier markets, potentially adding significant incremental tonnage to the global biochar market after 2028.

Regulatory Landscape

Policy and certification rules are increasingly shaping biochar market access through carbon-removal accounting and land-application controls. In the European Union, the Carbon Removal and Carbon Farming framework moved into implementation in 2026, with the European Commission adopting Delegated Regulation (EU) 2026/285 in February 2026 to set certification methodologies for permanent biochar carbon removal (BCR) activities, and the CRCF framework entering into force in May 2026. These steps create a formal, government-led route for BCR quantification and sustainability requirements, which helps standardize eligibility and documentation for projects that monetize carbon removal.

In the United Kingdom, the Environment Agency re-issued Regulatory Position Statement (RPS) 366 in February 2026 for storing and spreading biochar to benefit land (waste code 19 01 18), with effectiveness extending until review by March 1, 2029. This reinforces an operational compliance pathway for land application. In the United States, state-level activity is emerging alongside federal incentives, with Maryland Senate Bill 625 taking effect in July 2026 and requiring the Department of the Environment to adopt regulations for carbon removal projects utilizing biochar, signaling more explicit permitting and oversight structures at the sub-national level.

Value Chain Analysis

The biochar value chain runs from feedstock sourcing (forestry residues, agricultural residues, manure, sewage sludge, and organic waste) through preprocessing (drying, sizing, contamination control), thermochemical conversion (predominantly pyrolysis, plus gasification and hydrothermal carbonization), and downstream finishing (screening, pelletizing, or suspension formulation) before distribution to farms, horticulture blenders, water-treatment users, and construction and industrial buyers. The chain is fragmented because low bulk density and variable feedstock moisture shift a large share of delivered cost toward logistics and preprocessing. This dynamic encourages regional sourcing, co-location near residue generators (sawmills, mills, wastewater plants), and modular or distributed production assets.

Verification and market-enablement layers increasingly sit alongside the physical chain, including standards and carbon-credit monitoring, reporting, and verification needed for durable carbon-removal monetization. Capacity announcements and commissioning activity also point to a shift toward industrial-scale, locally anchored hubs: Pure DC opened the PureBiochar facility in Royal Wootton Bassett, United Kingdom (11,500 tonnes per year) in April 2026, and Jain Irrigation commissioned a 20,000-tonne-per-year facility in Jalgaon, India in June 2026 using agricultural and fruit-processing residues. On the certification side, Carbon Standards International published the Global Biochar C-Sink standard in June 2024, and Mission Innovation reported in March 2026 that 33 BCR-dedicated plants had been commissioned with 46 additional projects under construction in the European Union and Switzerland, highlighting the growing role of standardized methodologies and project pipelines in scaling supply.

Competitive Landscape

The global biochar market remains higly fragmented, with the top five producers accounting for well under 30% of installed capacity. Fragmentation stems from local feedstock realities; trucking low-density biomass more than 80 km erodes margins, so most facilities stay regional. Consequently, small and mid-sized firms using kiln capacities below 10,000 tons per year dominate rural supply. Large incumbents are beginning to integrate vertically—securing forestry rights, investing in mobile harvesters, and forming offtake pacts with concrete makers—to lock in both inputs and high-value outputs.

Process innovation is an active battleground. Firms in the United States and Germany commercialised continuous-flow, auger-fed reactors that improve yield predictability while trimming labour costs. Others concentrate on modular skids that can be dropped beside sawmills or municipal-waste sites, slashing feedstock transport expense. Quality differentiation is sharpening as well; manufacturers now market application-specific grades that vary in pH, ash content, and surface area to suit plantation crops, water-filtration beds, or construction mixes.

Strategic financing shapes market share trajectories. Venture-backed start-ups often rely on forward carbon-credit sales to large multinationals, converting future cashflows into upfront capital. In contrast, publicly listed biochar firms tap green bonds or sustainability-linked loans that reward production milestones tied to verified carbon removal. Cross-industry alliances—cement majors taking equity stakes in char producers, for instance—signal the emergence of captive supply models aimed at securing low-carbon feedstocks for hard-to-abate sectors.

Biochar Industry Leaders

Airex Energy

Pyreg GmbH

Carbon Gold Ltd

Phoenix Energy

Biochar Now LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace in the market is scaling biochar production through infrastructure-adjacent feedstock integration, where waste owners can secure consistent inputs and capture co-benefits from avoided disposal while supplying verified carbon removal and physical product. This shows up in municipal and industrial partnerships that embed biochar into existing waste systems, such as AMP Robotics partnering with the Southeastern Public Service Authority (SPSA) in April 2026 to integrate biochar production into municipal solid waste infrastructure in Portsmouth, Virginia (initially handling 108,000 tons of waste annually). Similar integration is also advancing in agro-industrial settings where residue streams are concentrated, illustrated by Cold Steppe commissioning a USD 15 million rice-hull biochar facility in Stuttgart, Arkansas in July 2026 (processing 20,000 tons of rice hulls to produce 10,000 tons of biochar annually).

Another opportunity area is large-scale capacity build-out in regions with abundant biomass residues and carbon-removal monetization pathways, using multi-line deployments and technology partnerships to reduce unit costs and improve supply reliability for long-term offtakes. Exomad Green expanded its Riberalta site in Bolivia in January 2026 from three to six pyrolysis lines, doubling annual production to 50,000 tonnes of biochar, and in April 2026 commenced a second phase with Beston Group to deploy additional industrial units in Bolivia. At the same time, maturing certification frameworks and protocols (including government-led approaches in Europe and registry approaches cited across voluntary markets) are tightening requirements around permanence and sustainability, which raises the premium for traceable, consistently specified material and pushes producers toward standardized quality, documented feedstock chains, and audited measurement systems.

Recent Industry Developments

- February 2026: SUEZ and PYREG GmbH announced a partnership to develop Pyrolis S2B, an integrated pyrocarbonisation solution designed for energy-autonomous sewage sludge treatment with biochar output. The collaboration broadens biochar feedstock pathways into wastewater and positions integrated sludge-to-biochar systems as a route to combine waste compliance with carbon-removal product supply.

- September 2025: Airex Energy received Puro.earth certification for its Carbonity biochar project, enabling issuance of carbon removal credits. Certification strengthens bankability for project expansions and supports long-term offtake structures by tying biochar output to a recognized carbon-removal issuance pathway.

- July 2024: Carbon Gold announced a partnership with Westland Horticulture to launch carbon-neutral biochar-enriched compost targeted at home gardeners. The move expanded downstream channels in horticulture and consumer-facing soil products, supporting volume pull-through beyond farm applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as biochar supplied as a carbon-rich solid made from biomass conversion and then sold for end use, mainly in soil improvement and other industrial uses, tracked as market volume in tons.

Scope exclusions: We exclude raw biomass feedstock trade, activated carbon, and general charcoal used mainly as fuel when it is not sold and specified as biochar.

Segmentation Overview

- By Technology

- Pyrolysis

- Gasification Systems

- Other Technologies (Hydrothermal Carbonization)

- By Feedstock

- Woody Biomass

- Agricultural Residues

- Animal Manure

- Sewage Sludge and Organic Waste

- By Form

- Powder

- Pellets/Granules

- Liquid Suspension

- By Application

- Agriculture

- Animal Farming

- Industrial Uses

- Other Applications (Construction Materials, Energy, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public facts that help us map supply, demand, and policy signals that influence biochar output. We typically refer to sources such as USDA and FAO agriculture and residue statistics, US EPA information on waste and emissions, European Commission and national environment agencies for soil and climate programs, and customs statistics for biomass-related trade where relevant.

To convert signals into a usable model, we also review company filings and investor presentations, plant announcements captured through news and financials subscriptions, and patent databases to understand technology scaling (pyrolysis and related systems). Academic journals and association publications are used to sense-check application rates and agronomy outcomes, before assumptions are carried forward to forecasting. This desk source list is illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered from producers, technology providers, distributors, agronomy experts, and large end users, so that conversion yields, operating rates, and application demand could be checked against the desk assumptions. We also tested our view across APAC, EMEA, and the Americas because supply build-outs and soil-use adoption can move differently by region, and we needed the same definitions applied consistently.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 43% |

| Mid tier: 42% | Functional/Unit leaders: 26% | EMEA: 33% |

| Smaller Players: 22% | Managers: 60% | Americas: 24% |

Market-Sizing & Forecasting

Our sizing starts from a top-down build where biomass availability, conversion yields, and regional operating activity are used to reconstruct feasible biochar output, then this is aligned to demand signals in key end uses. To keep the totals grounded, we run selective bottom-up checks using sampled producer capacity and utilization, channel checks on shipped volumes, and observed ranges for application rates in agriculture.

A few practical model inputs are tracked and updated as the forecast runs, such as installed and announced production capacity, typical yield by feedstock and technology pathway, average plant utilization, and the share of output going into soil amendment versus other uses. Where needed, we also factor in policy pull like carbon removal program activity and soil health incentives, because they can change purchasing behavior faster than agronomy alone.

For forecasting, scenario analysis is applied around capacity ramp-ups and adoption speed, followed by time-series smoothing on near-term volumes to avoid overreacting to one-off plant starts or pauses. When gaps appear in bottom-up approximations, they are handled through regional normalization and re-contact with knowledgeable respondents so we do not over-count the same volume through multiple channels.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including observed capacity additions, regional production feasibility, and reported biochar usage trends in agriculture programs, and then exceptions are reviewed before sign-off. If a variance is large, the underlying assumption is revisited, and follow-up calls are triggered to confirm whether the issue is definition, timing, or a real market shift.

The work goes through multi-step analyst reviews where calculation logic, units, and year alignment are re-checked. Reports are refreshed annually, and interim updates are made when material events occur, such as major plant commissioning delays, policy shifts, or a clear change in adoption rates. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Biochar Market Size Compared With Other Published Estimates

Published market sizes for biochar can differ more than buyers expect because sources do not always use the same unit, the same definition of what counts as biochar, or the same timing for capacity ramp-ups. Some studies also mix revenue and volume in how they talk about size, which creates confusion when the market is still scaling.

Capacity commissioning announcements and producer shipment checks are the evidence used to keep the Mordor Intelligence estimate tied to a volume-based supply reality, which is why the estimate can look different from value-based figures that move with pricing assumptions and category inclusions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.88 M (2026) | |

| Global Consultancy A | USD 0.70 B (2025) | Reported in revenue terms, so results depend heavily on assumed average selling price and product mix, and adjacent categories can be folded in without a clear boundary to biochar-only volume. |

| Industry Association B | USD 0.61 B (2023) | Uses a survey-led revenue total that can include equipment and related value chain activity, and it is anchored to an earlier year that may not reflect later capacity additions and utilization changes. |

The table shows that the widest spread is explained by unit choice and what is counted inside the boundary, not just by math. By sticking to a clear volume definition and then cross-checking it with real-world operating signals, our view stays traceable to practical drivers that can be re-tested as new capacity and demand information becomes available.

Key Questions Answered in the Report

What is the current size of the biochar market?

The biochar market size reached 0.88 million tons in 2026 and is projected to rise to 2.59 million tons by 2031 at a 24.11% CAGR.

Which region leads global demand?

Asia-Pacific held 39.88% of global volume in 2025 and is expected to maintain leadership thanks to abundant biomass and supportive policy measures.

What technology is most widely used to produce biochar?

Slow and intermediate pyrolysis dominate, capturing 44.72% of 2025 production because they balance high char yields with valuable syngas and bio-oil coproducts.

Why are carbon credits important for the biochar market?

Credits priced above USD 100 per tonne CO₂e add a second revenue stream, improving project economics and attracting institutional finance for new capacity.

Which application is growing fastest outside agriculture?

Industrial uses—including water treatment, concrete, and metals processing—are forecast to expand at 25.1% CAGR to 2031, outpacing agricultural growth rates.

Page last updated on: