Marine Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

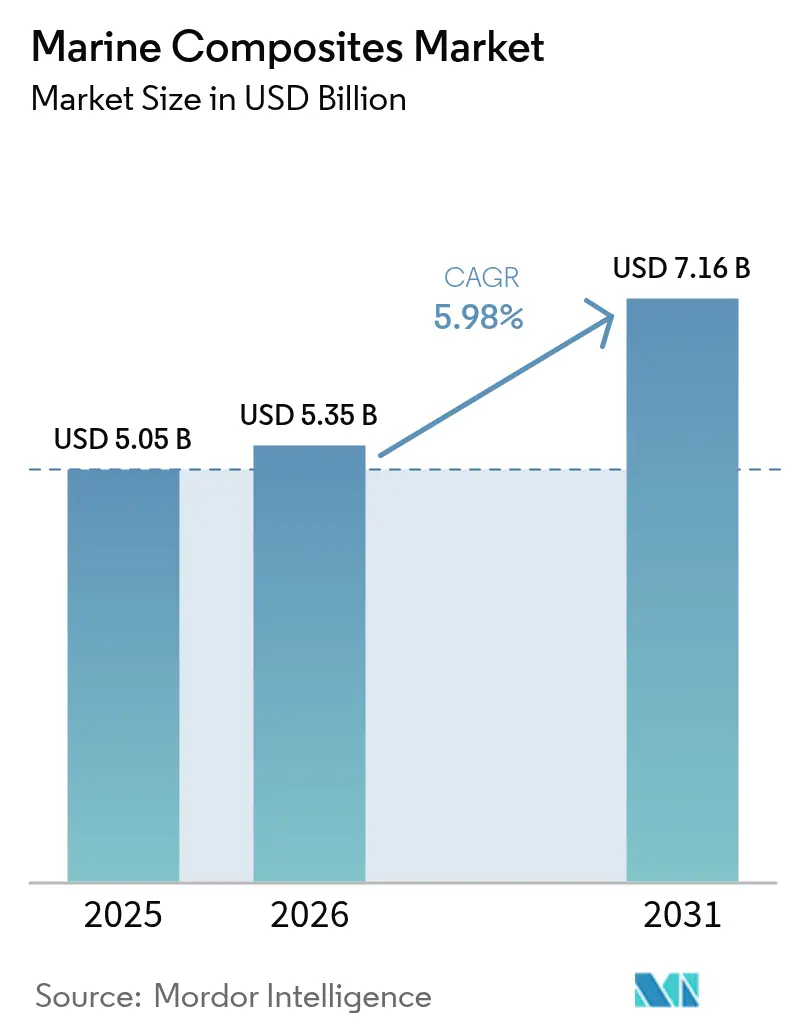

| Market Size (2026) | USD 5.35 Billion |

| Market Size (2031) | USD 7.16 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

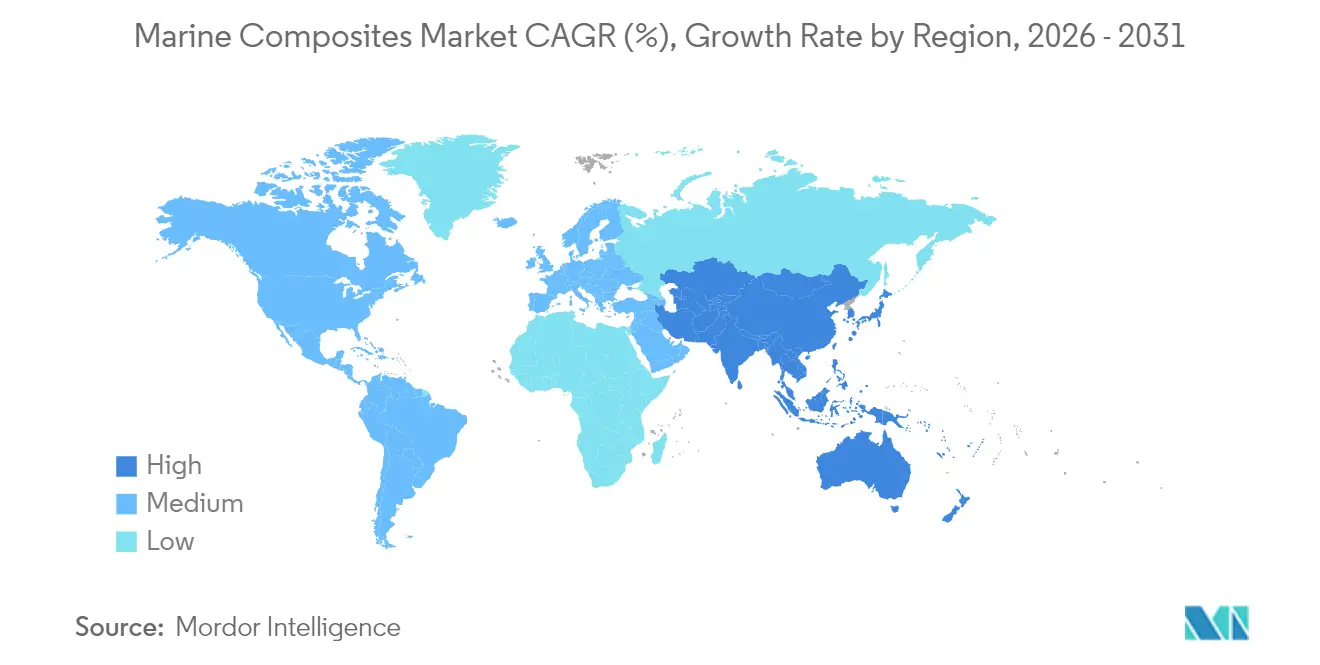

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

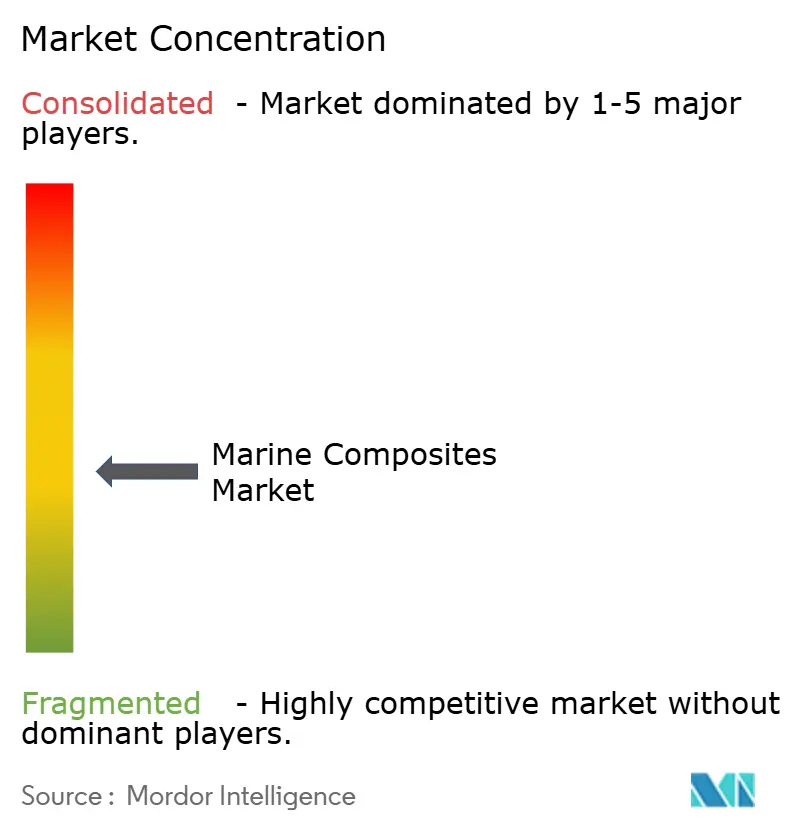

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Composites Market Analysis by Mordor Intelligence

The Marine Composites Market size was valued at USD 5.05 billion in 2025 and estimated to grow from USD 5.35 billion in 2026 to reach USD 7.16 billion by 2031, at a CAGR of 5.98% during the forecast period (2026-2031). The growth outlook reflects an industry‐wide shift from traditional steel and aluminum toward lighter, corrosion-proof composite structures that help vessel builders satisfy tightening emission regulations, extend cruising range, and lower lifetime operating costs. Sustained defense spending, especially the United States Navy’s annual USD 40.1 Billion shipbuilding plan, keeps orderbooks healthy for composite-intensive patrol craft, unmanned systems, and auxiliary platforms. Parallel investments in 3D printing, automated fiber placement, and closed-mold infusion lines reduce cycle times and unlock new design freedom, allowing builders to integrate complex geometries while meeting class-society quality standards. Regional demand patterns diverge: North America enjoys resilient aftermarket revenues in wake-sports boats and personal watercraft, whereas Asia-Pacific accelerates on the back of large-scale naval modernization programs. Supply dynamics remain fluid; aramid fiber lead times and certification bottlenecks for novel resins invite vertically integrated players to forward-secure raw materials or co-develop formulations with chemical partners.

Key Report Takeaways

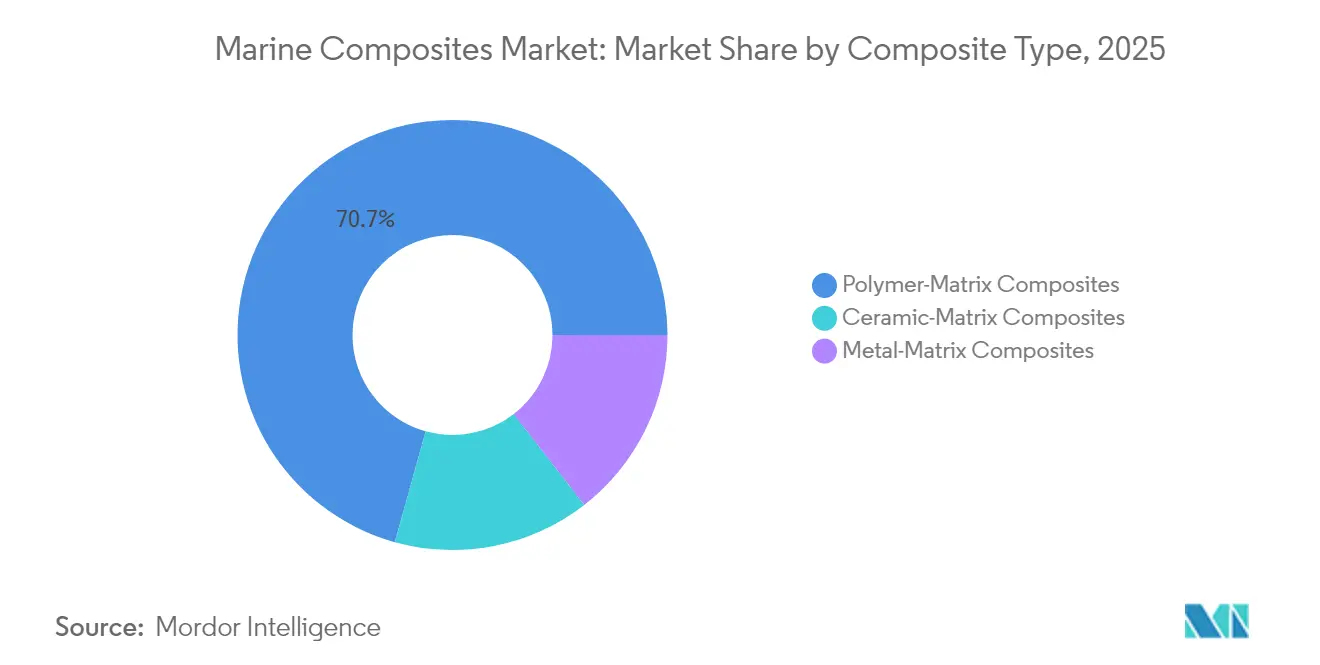

- By composite type, polymer-matrix systems captured 70.68% revenue share in 2025; ceramic-matrix composites are forecast to post a 6.55% CAGR to 2031.

- By resin type, epoxy dominated with a 31.02% share in 2025, while polyester is projected to expand at a 6.62% CAGR through 2031.

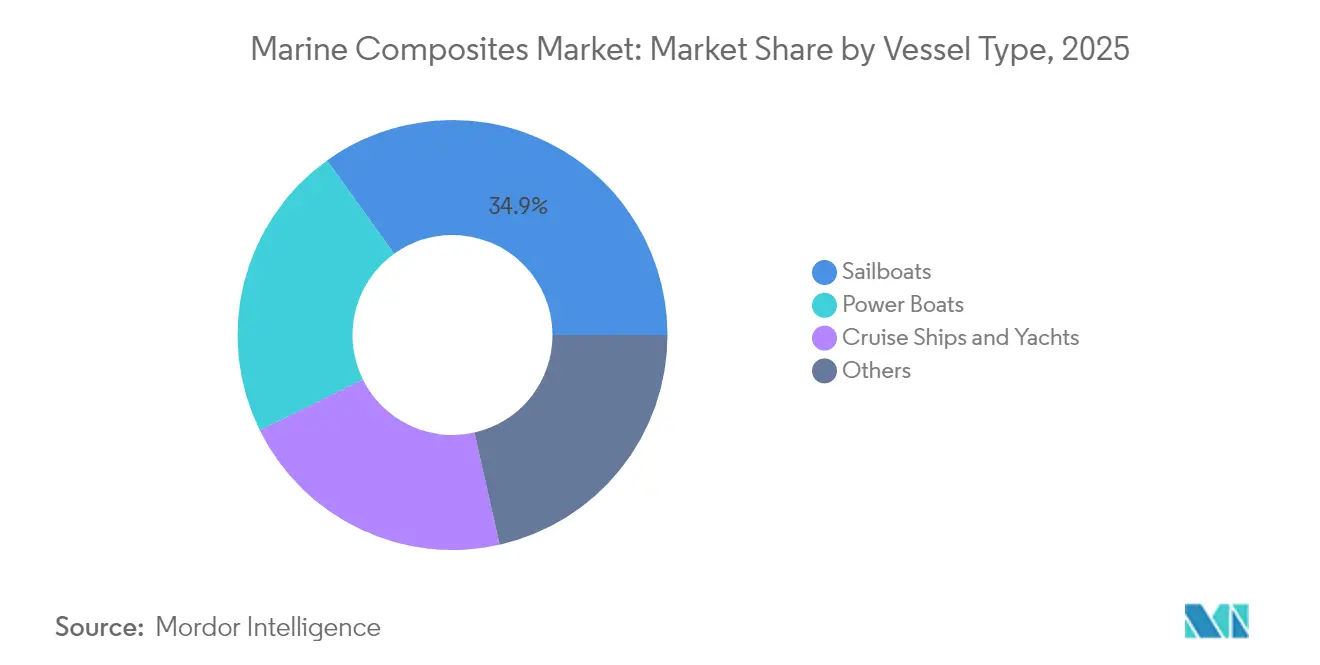

- By vessel type, sailboats accounted for 34.92% of the Marine Composites market share in 2025, and power boats are advancing at a 6.74% CAGR to 2031.

- By geography, North America led with 40.05% of the Marine Composites market size in 2025; Asia-Pacific is projected to register the fastest 6.93% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marine Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Production of Leisure Boats and Cruise Ships | + 1.8% | North America & Europe, spill-over to APAC | Medium term (2-4 years) |

| Stringent Emission Norms Drive Lightweighting | + 2.1% | Global, with early adoption in EU and North America | Long term (≥ 4 years) |

| Recreational Boating Boom in North America and Europe | + 1.2% | North America & Europe core markets | Short term (≤ 2 years) |

| Naval Modernization Budgets | + 1.0% | Global, concentrated in APAC and North America | Long term (≥ 4 years) |

| 3D Printed Composite Parts for Rapid Builds | + 0.3% | Global, with technology hubs in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Production of Leisure Boats and Cruise Ships

Luxury and performance-oriented builders are setting the tone for broader adoption of high-end composites. Carbon fiber catamarans such as the 55-ft model launched by Cure Marine in late 2024 demonstrate full-hull infusion, integrated solar arrays, and all-electric hotel loads that depend on aggressive weight targets. Major original equipment manufacturers (OEMs) have installed five-axis Computer Numerical Control (CNC) routers and large-scale molds to execute ever-larger single-piece deck structures, reducing secondary bonding work and improving cosmetic quality. Associations such as the International Council of Marine Industry Associations note that electrification strategies vary by vessel size but converge on one requirement: mass reduction to preserve range. High-profile proof points in the premium segment reassure mid-tier builders about durability and resale value, accelerating technology diffusion as tooling amortizes. As marinas upgrade shore-power infrastructure, aftermarket retrofits of composite hardtops and swim platforms are also gaining pace, further lifting demand.

Stringent Emission Norms Drive Lightweighting

The European Union’s “Fit for 55” package and the International Maritime Organization’s Carbon Intensity Indicator compel shipyards to chase every kilogram saved. Composite superstructures on cruise ships cut top weight, lowering the center-of-gravity and permitting smaller engines or larger battery packs. Germany’s maritime cluster, worth USD 93 Billion annually, invests in digital twins and Industry 4.0 work cells that pair bio-based matrices with robotized lay-up to meet life-cycle-assessment thresholds [1]U.S. Department of Commerce, “Germany – Marine Technology,” commerce.gov. Research centers like Austria’s Wood K plus have pushed the envelope by converting wood polymer composites into bio-based silicon-carbide ceramics that tolerate 1,400°C, hinting at future exhaust or hot-section components that sidestep metal corrosion issues. The regulatory bar effectively converts lightweighting from a cost premium into a compliance necessity, positioning advanced composites as the pragmatic route to multi-criteria wins, fuel burn, maintenance, and recyclability.

Recreational Boating Boom in North America and Europe

While the National Marine Manufacturers Association expects a dip in new power-boat registrations during 2024 because of high interest rates, personal watercraft and entry-level runabouts remain bright spots. These categories lean heavily on sheet-molding compounds, chopped-strand-mat laminates, and growing volumes of natural fiber cores to hit aggressive price points. European yards participating in the European Union (EU)-funded FIBRE4YARDS program already report 77% composite penetration, and shared design libraries allow smaller builders to download class-approved scantlings that shorten engineering cycles. Foiling day-boats have emerged as halo products demonstrating the stiffness-to-weight benefit of carbon prepregs, nudging consumer expectations upward. Price sensitivity is forcing innovation in hybrid ply schedules, combining glass, basalt, and bio-resins without sacrificing durability, thereby keeping the marine composites market relevant across discretionary-spend brackets.

Naval Modernization Budgets

Government defense planners continue to bankroll composite research because mission envelopes are extending. The United States House of Representatives earmarked USD 5 Billion for naval shipbuilding in FY-2025, carving out USD 500 Million for additive manufacturing pilot lines and USD 750 Million for domestic supplier development. Japan’s 22,000-ton ship Nihonbare exemplifies the region’s pivot to lightweight topside structures that increase helicopter sortie rates without lengthening hulls. The Office of Naval Research still funds polymer-matrix studies to boost out-of-plane toughness through carbon nanotube doping, signaling that even after 50 years, composites can evolve. Because defense budgets are less price-elastic, technologies such as ceramic-matrix exhaust ducts and radar-absorbent laminates can reach production readiness before costs decline enough for commercial fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Material and Processing Costs | -1.4% | Global, particularly impacting price-sensitive segments | Short term (≤ 2 years) |

| Volatile Aramid/Specialty Fiber Supply | -0.8% | Global supply chains, concentrated impact in North America and Europe | Medium term (2-4 years) |

| Certification Bottlenecks for Novel Resins | -0.5% | Global, with regulatory variations by region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Material and Processing Costs

Marine laminates rarely achieve the volume economies of wind blades or automotive body panels, increasing per-kilo carbon prices. Even though worldwide carbon fiber capacity is set to triple to 450,000 tonnes by 2030, aerospace and wind still command priority allocations, leaving yards exposed to spot-market spikes. McClarin Composites’ alliance with ExxonMobil to industrialize resin transfer molding using the Proxxima polyolefin system shows suppliers automating infusion to bring takt times closer to automotive levels. Yet upfront mold investment and the learning curve deter small shops. Hybrid glass-carbon stacks and low-temperature curing epoxies are interim answers, but sticker shock remains a gating factor for fishermen and charter operators evaluating new builds.

Volatile Aramid/Specialty Fiber Supply

Ballistic-grade aramids enhance slamming resistance and offer inherent flame retardancy, making them popular in patrol craft and catamaran bows. Their supply chain, however, is concentrated among a handful of Asian producers whose plasma-oxidation surface treatments are capital-intensive. Any outage swiftly tightens global availability and extends lead times for European and North American finishers. Teijin’s decision to divest its USD 1 Billion North American automotive composites unit underscores strategic refocusing that may ripple into marine allocations [2]JEC Composites, “Teijin Sells Automotive Composites Business,” jeccomposites.com. Builders are experimenting with basalt and Ultra-High Molecular Weight Polyethylene (UHMWPE) fibers as partial substitutes, but qualification campaigns take time, and class-society acceptance is cautious. Until dual-sourcing or regional plants come online, procurement risk persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Composite Type: Polymer-Matrix Dominance Drives Innovation

Polymer-matrix systems generated 70.68% of 2025 revenues, underscoring deep process know-how and broad raw-material availability. The segment continues to receive research dollars aimed at improving interlaminar shear and fatigue life, with the marine composites market size for polymer-matrix laminates expected to expand steadily as vacuum infusion and press-molding lines proliferate. Ceramic-matrix composites, though presently niche, are the clear growth story and should post a 6.55% CAGR to 2031 on the strength of engine-room and exhaust applications where polymers soften. The Marine Composites market share of ceramic-matrix grades will remain modest through the midpoint of the decade, but volume ramp-ups in naval unmanned underwater vehicles and gas-turbine housings illustrate rising confidence in their thermal stability.

Efforts at the National Energy Technology Laboratory to qualify SiC/SiC (Silicon Carbide) joints for hydrogen combustion, combined with Germany’s Ceramic Composites network plan to double oxide fiber output, suggest supply barriers are slowly eroding. Polymer matrices are responding with nanotube and graphene additives that lift through-thickness modulus by double-digit percentages, prolonging their reign in hull and deck structures. Metal-matrix formulations hold on to specialty roles such as propeller hubs and shaft sleeves where heat dissipation trumps weight savings. Overall, cross-pollination between sectors keeps the development pipeline full, ensuring competitive tension among the three composite categories.

By Resin Type: Epoxy Leadership Faces Polyester Challenge

Epoxy retained a commanding 31.02% slice of resin demand in 2025 thanks to superior adhesion, low water uptake, and chemical resistance. However, unsaturated polyester resins are accelerating on a cost-per-performance basis and are poised to register the fastest 6.62% CAGR through 2031. Builders targeting sub-15-meter boats now mix rapid-gel polyester with closed-mold techniques, meeting price targets without sacrificing blister protection. Vinyl ester bridges the gap; it offers higher toughness at mid-market prices and finds favor in transoms and stringers that endure repeated impact loading.

The marine industry's exploration of plant-based alternatives and non-toxic curing methods addresses environmental concerns while maintaining performance characteristics. Other resin systems, including thermoplastic matrices, gain attention for recyclability advantages, with NLcomp's EcoRacer30 sailboat demonstrating 95% recyclable composite construction using thermoplastic resins combined with virgin and recycled carbon fibers.

By Vessel Type: Power Boats Accelerate Past Sailboats

Sailboats generated 34.92% of segment revenues in 2025 because even entry-level cruisers rely on glass/foam sandwiches for stiffness. The Marine Composites market size for sailboats will grow steadily, yet power boats, especially personal watercraft and wake-surf categories, will outpace at a 6.74% CAGR. Volume OEMs have streamlined assembly using large, single-skin glass molds and robot-drilled inserts, slashing touch labor. Therefore, the marine composites market share held by power boats is expected to climb as builders release affordable 16- to 24-ft models sporting composite swim platforms and transom extensions.

Meanwhile, premium yachts and cruise ships serve as technology demonstrators for carbon fiber superstructures and composite exhaust stacks that shave tons of weight. Class approvals for composite propellers, such as QinetiQ’s 2-meter prototype, pave the way for broader adoption in displacement craft where cavitation and corrosion have been perennial headaches. Foiling electric day-boats capture headlines but also stress-test resin toughness and hydro-impact resistance, knowledge that migrates down into mainstream hulls as cost curves fall.

Geography Analysis

North America accounted for 40.05% of 2025 global revenues, anchored by the United States recreational fleet and steady federal appropriations for littoral combat ships, unmanned surface vessels, and auxiliary craft. Canada’s niche in high-latitude expedition yachts and Mexico’s growing aftermarket refurbishment sector raise regional demand. The marine composites market size in North America will expand at a healthy clip as yards upgrade to digital twins and automated infusion to offset skilled-labor shortages.

Asia-Pacific's demand for marine composites is expected to grow at a 6.93% CAGR through 2031. China’s 6,000-m-rated underwater drone featuring an ultra-strong carbon hull illustrates how state-run institutes can leapfrog traditional material limits. Japan’s USD 1.2 Trillion defense modernization roadmap includes composite-rich amphibious assets that address island-chain security. India’s USD 1.07 Billion contract for 14 coast-guard patrol vessels embeds composite superstructures to keep draft shallow and fuel burn low, aligning with its “Atmanirbhar Bharat” self-reliance push. Southeast Asian nations from Indonesia to Vietnam are exploring composite river ferries to serve archipelagic routes, suggesting that local laminate shops will sprout in parallel with demand. Europe retains a strong innovation footprint, with the FIBRE4YARDS consortium proving 77% composite content across participating shipyards and Germany’s Industry 4.0 roll-outs linking CNC kitting, RFID (Radio Frequency Identification) cloth tracking, and real-time resin viscosity monitoring. Strict EU emission rules double as a demand catalyst; yards modernize to stay compliant, and suppliers benefit from early-stage grants and tax credits. Niche markets in the Middle East and South America are leveraging composites for crew boats and offshore wind support vessels, though infrastructure gaps and financing hurdles temper acceleration.

Mordor Intelligence provides coverage of the marine composites market across other key regional markets. Detailed country-level analysis extends to Japan incorporating local coverage and market participation, as required.

Competitive Landscape

The Marine Composites Market is moderately consolidated with major players, such as Hexcel Corporation, Gurit Services AG, DuPont, Owens Corning, and TORAY INDUSTRIES, INC. Gurit and Toray focus on advancing low-toxicity epoxy hardeners and rapid-curing prepregs, respectively, while smaller innovators like NLcomp trial thermoplastic matrices that eliminate styrene emissions at lay-up. Technology differentiation is narrowing as vacuum infusion and 3D-printed core inserts become standard. Competitive edge is now tilting toward supply-chain resilience and sustainability. Asian navies want domestic content, so Western suppliers are pondering joint ventures in India and Japan. Composite recyclers capable of depolymerizing epoxy into reusable oligomers or reclaiming continuous fibers could become king-makers by mid-decade.

Marine Composites Industry Leaders

DuPont

Hexcel Corporation

TORAY INDUSTRIES, INC.

Gurit Services AG

Owens Corning

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: Hypetex Limited announced its expansion into the marine sector with materials that exhibit high stress tolerance, enhancing marine products' durability and longevity while reducing maintenance costs. Through these materials, boatbuilders can achieve their desired aesthetics without compromising performance.

- July 2023: Northern Light Composites (nlcomp) launched its recyclable production boat at the Ocean Race Grand Finale in Spain. The Ecoracer30 is a composite-intensive sailing boat that uses rComposite, the company’s patented sustainable composite solution.

Global Marine Composites Market Report Scope

The Marine Composites Market report includes:

| Metal-Matrix Composites |

| Polymer-Matrix Composites |

| Ceramic-Matrix Composites |

| Epoxy |

| Polyester |

| Others |

| Sailboats |

| Cruise Ships & Yachts |

| Power Boats |

| Others (Commercial Workboats and Defense vessels) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Composite Type | Metal-Matrix Composites | |

| Polymer-Matrix Composites | ||

| Ceramic-Matrix Composites | ||

| By Resin Type | Epoxy | |

| Polyester | ||

| Others | ||

| By Vessel Type | Sailboats | |

| Cruise Ships & Yachts | ||

| Power Boats | ||

| Others (Commercial Workboats and Defense vessels) | ||

| By Geograhy | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Marine Composites Market size?

The Marine Composites market size is valued at USD 5.35 Billion in 2026 and is forecast to grow to USD 7.16 Billion by 2031.

Which composite type holds the largest share of demand?

Polymer-matrix composites lead with 70.68% revenue share in 2025, owing to cost-effective processing options and versatile performance characteristics

Which region is expanding the fastest?

Asia-Pacific exhibits the fastest growth, projected at a 6.93% CAGR through 2031 on the back of naval modernization and rising domestic boat ownership.

What is the biggest growth constraint for composite adoption in marine applications?

High material and processing costs remain the top restraint, reducing affordability for price-sensitive vessel classes until automated manufacturing scales further.

How are sustainability goals influencing material selection?

Builders are trialing bio-based epoxies and recyclable thermoplastic matrices, with recent launches such as the EcoRacer30 demonstrating near-circular manufacturing possibilities.

Page last updated on: