Blue Hydrogen Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

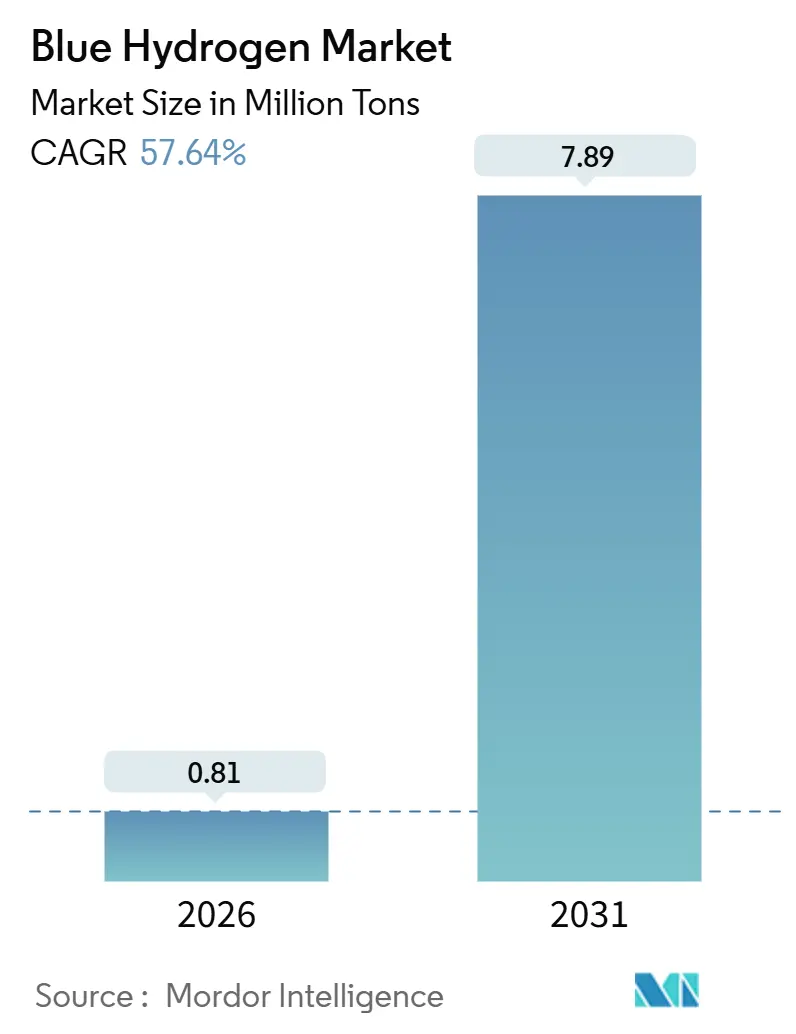

| Market Volume (2026) | 0.81 Million tons |

| Market Volume (2031) | 7.89 Million tons |

| Growth Rate (2026 - 2031) | 57.64% CAGR |

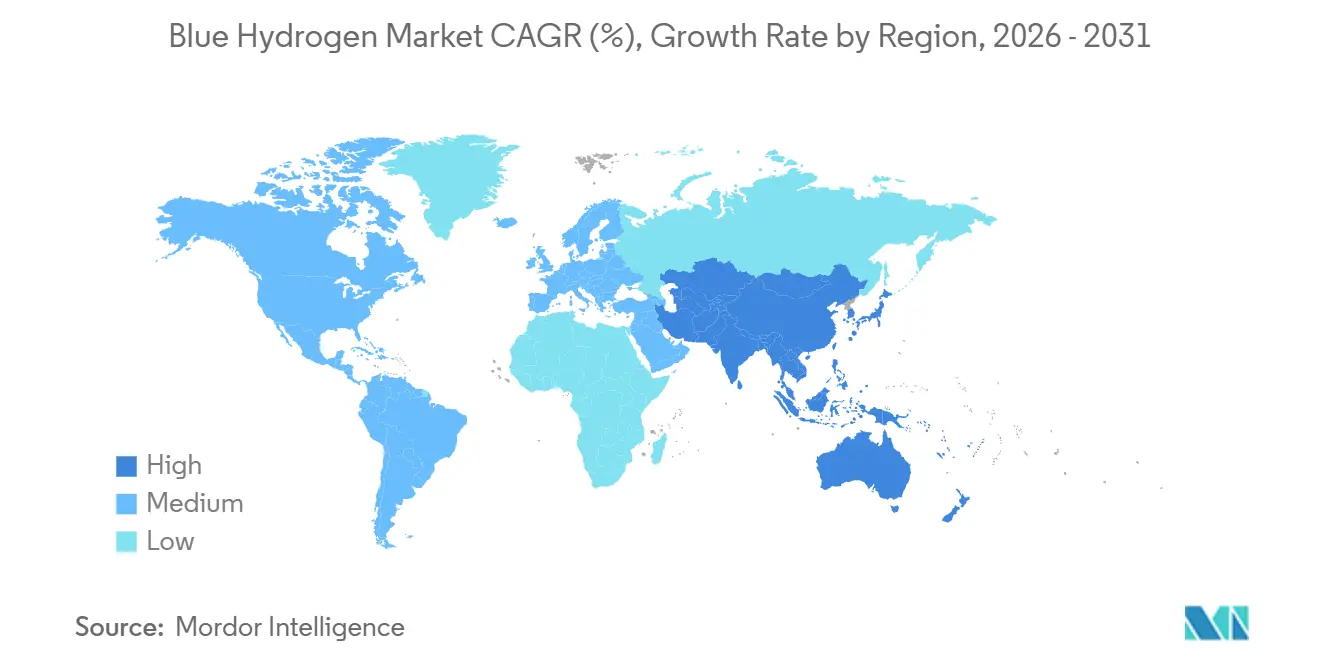

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blue Hydrogen Market Analysis by Mordor Intelligence

The Blue Hydrogen Market size is estimated at 0.81 Million tons in 2026, and is expected to reach 7.89 Million tons by 2031, at a CAGR of 57.64% during the forecast period (2026-2031). The narrowing cost gap with grey hydrogen, accelerated by the United States’ IRA 45V tax credit and the European Union’s RFNBO mandate, is the central force behind this growth. Developers are prioritizing autothermal-reforming (ATR) plants with carbon capture because their 95-plus % capture rates qualify for the most lucrative subsidies, while shared CCS hubs in the US Gulf Coast, the North Sea, and Alberta are trimming project capital outlays by 25-35%. Regional momentum is strongest in Asia-Pacific, where blue-ammonia back-haul corridors from Saudi Arabia and Australia to Japan and South Korea create long-term offtake visibility. Heavy-duty trucking and maritime bunkering trials in California, Rotterdam, and Singapore move transportation from the demonstration phase to commercial scale, signaling a clear policy-driven demand pivot.

Key Report Takeaways

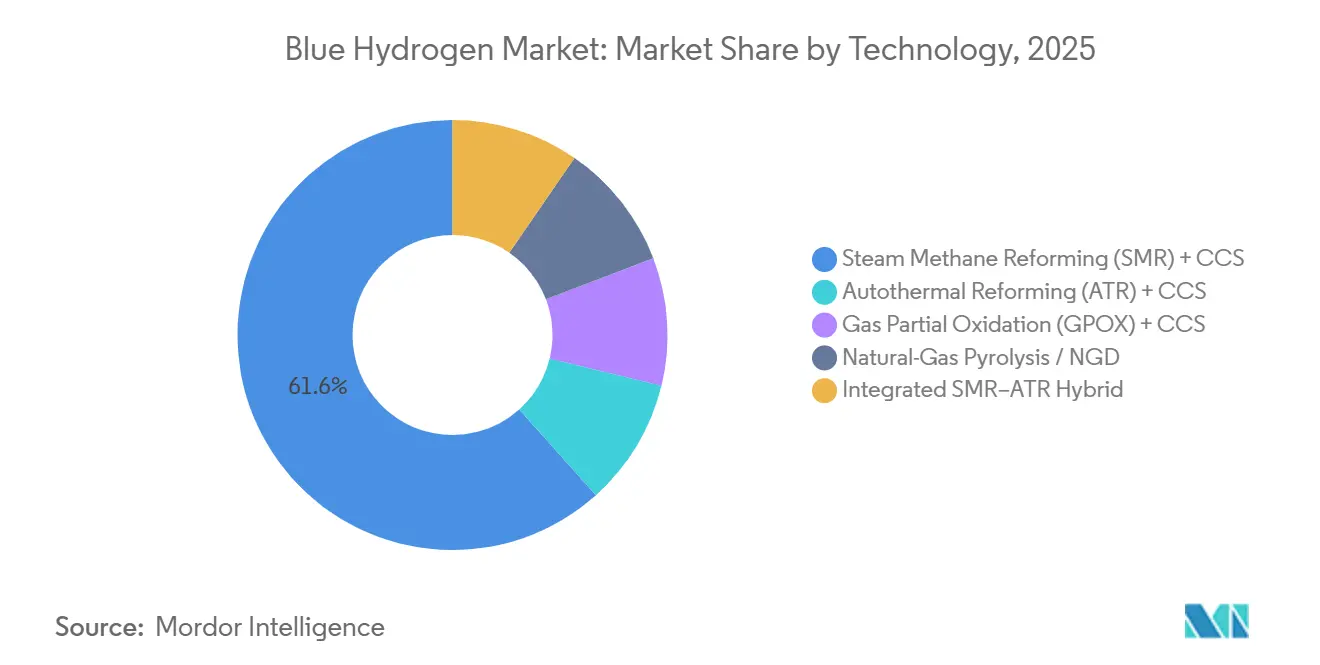

- By technology, Steam Methane Reforming (SMR) + CCS held 61.62% of the blue hydrogen market share in 2025, while Autothermal Reforming (ATR) + CCS is poised to grow at a 62.25% CAGR through 2031.

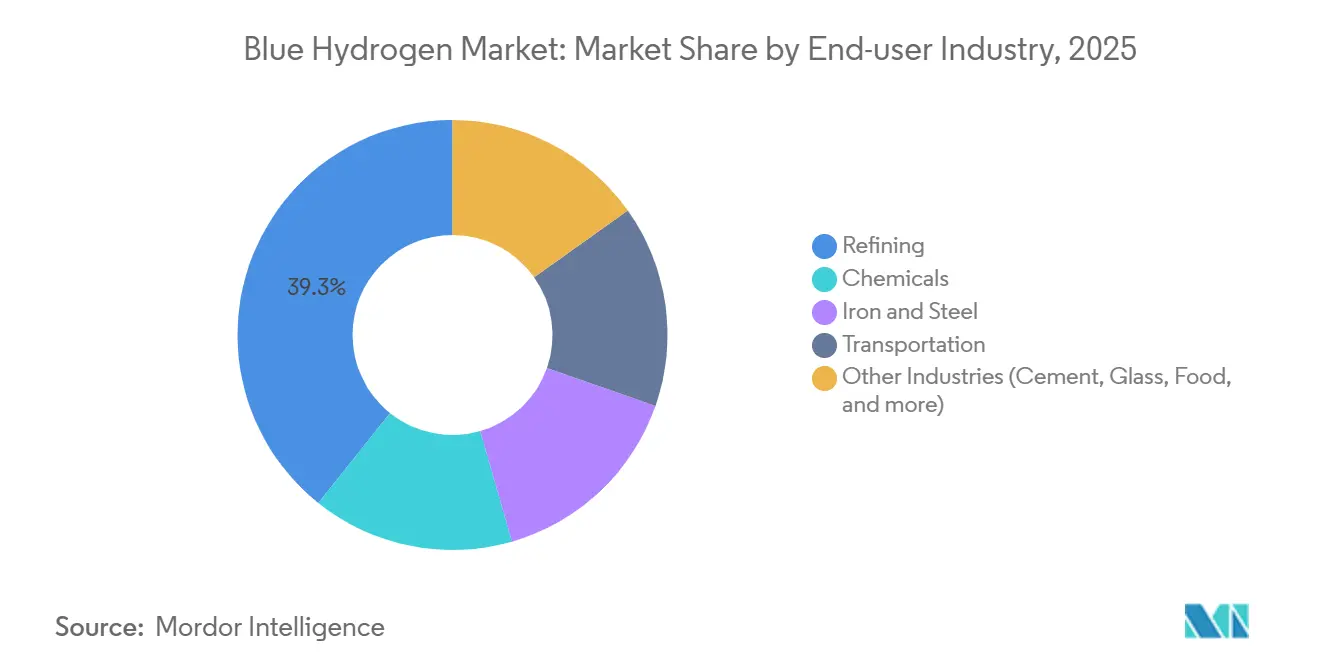

- By end-user industry, the refining sector led with 39.27% revenue share in 2025; transportation is projected to post the fastest 58.06% CAGR to 2031.

- By geography, Asia-Pacific accounted for 38.24% of the blue hydrogen market size in 2025 and is advancing at a 59.42% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blue Hydrogen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel-cell electric-vehicle adoption | +11.2% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Blue-ammonia export corridors | +11.8% | Asia-Pacific core, spillover to Middle East | Long term (≥ 4 years) |

| Low-carbon chemical feedstocks | +11.5% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| IRA 45V and EU RFNBO incentives | +12.1% | North America and Europe | Short term (≤ 2 years) |

| Rapid CCS-hub build-out | +11.3% | North America, Europe, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Application in Fuel-Cell Electric Vehicles

Heavy-duty trucking is moving beyond pilots. Nikola delivered 72 Class 8 fuel-cell trucks in 1H 2025, and Hyundai committed to 1,600 XCIENT units across California and Switzerland by 2027. California’s Low Carbon Fuel Standard credits give blue hydrogen with 90% capture a competitive total cost of ownership, and early fleet operators lock in multi-year supply contracts. Maritime interest is rising as Maersk and TotalEnergies complete bunkering trials in Rotterdam, aiming for 2028 route commercialization. These adopters value immediate emissions compliance without waiting for renewable overbuild, pushing the blue hydrogen market toward transportation inflection.

Growing Blue-Ammonia Back-Haul Corridors in Asia

A first shipment of 40 tons of blue ammonia from Saudi Aramco to JERA in 2024 proved the commercial case for long-distance hydrogen carriage in ammonia form. South Korea’s POSCO earmarked USD 1.2 billion in 2025 for cracking facilities targeting 200,000 tons of hydrogen by 2028. Middle-Eastern producers deliver blue hydrogen at USD 1.20 kg and sell into Northeast Asia near USD 2.50 kg, a 40% price advantage over domestic green supply. The corridor satisfies Japan and South Korea’s 2030 hydrogen targets despite renewable-land constraints, embedding long-term trade lanes in the blue hydrogen market.

Rising Demand from Chemical Feedstocks (Ammonia, Methanol)

BASF’s Ludwigshafen site began taking blue hydrogen from Air Liquide’s Normandy plant in 2025, cutting ammonia-unit emissions 65% and qualifying for EU Green Deal tenders. OCI Global’s Texas methanol complex followed in 2024 to tap California’s renewable-fuel premium. Capturing 1 million tons of CO₂ secures USD 50-80 million annually in EU ETS allowances or IRA 45Q credits, offsetting 40-60% of CCS capex. Blue variants therefore meet certification thresholds for low-carbon fertilizers and marine fuels, underpinning multi-year supply agreements.

IRA 45V and EU RFNBO Incentives Compress Levelized Cost

The IRA offers USD 0.60 kg for blue hydrogen under the 2.5-kg CO₂-eq threshold, slicing U.S. Gulf Coast costs from USD 2.00 kg to USD 1.40 kg[1]U.S. Department of Energy, “Inflation Reduction Act Section 45V Guidance,” energy.gov. Europe’s RFNBO rule compels 42% low-carbon hydrogen in industry by 2030, guaranteeing local demand. ExxonMobil sanctioned the 1-bcf/d Baytown project in 2025 at a 12% IRR thanks to 45V inflows. Conversely, most Asian markets lack equivalent subsidies, limiting domestic offtake and reinforcing the region’s export orientation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost versus grey hydrogen | -6.4% | Global, most acute in Asia-Pacific and South America | Short term (≤ 2 years) |

| Energy-intensity and efficiency losses | -4.8% | Global | Medium term (2-4 years) |

| Methane-slip measurement and certification | -3.6% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost vs. Grey Hydrogen

Unsubsidized blue hydrogen ranges USD 1.80-2.50 kg versus USD 1.00-1.30 kg for grey in gas-rich regions, sustaining a 40-90% premium. EU carbon prices above EUR 80 t narrow the gap to 10-20%, but Asian buyers remain price-sensitive. SMR-CCS capex of USD 2.5-3.0 kg yr capacity is double conventional SMR, mainly from capture equipment. Small industrial users cannot amortize these costs, limiting early adoption to refineries, ammonia, and steel complexes and slowing penetration of the blue hydrogen market.

Energy-Intensity and Efficiency Losses

CCS lowers plant efficiency to 65-72%, pushing feedstock use 15% higher than grey hydrogen. ATR recovers some efficiency at 68-74% but needs oxygen plants that add USD 0.20-0.30 kg to capital costs. High European gas prices lift feedstock cost to USD 2.10 kg before capture, squeezing margins, while emerging pyrolysis remains pilot-scale until 2029. The efficiency drag confines blue hydrogen’s role in peaking power, favoring long-duration storage niches instead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: ATR Gains on Capture-Rate Superiority

Steam-methane reforming with CCS retains the bulk 61.62% share in 2025 because refineries can retrofit existing reformers at 40-50% lower capital cost than greenfield ATR. Gas partial oxidation remains confined to petrochemical sites needing high-CO heat, while natural-gas pyrolysis is pre-commercial. Linde’s planned hybrid SMR-ATR plant in Texas signals a pragmatic middle ground, balancing capture efficiency and cost. Autothermal reforming with CCS is on track for a 62.25% CAGR, the quickest among production pathways. ATR achieves 95-98% CO₂ capture by combining oxygen-blown partial oxidation with high-pressure reforming, producing a near-pure CO₂ stream that slashes solvent-regeneration energy. Air Products’ USD 7 billion Louisiana complex will use ATR to deliver 750,000 t yr hydrogen and sequester 5 million t CO₂, targeting Tier 4 IRA credits[2]Air Products, “Louisiana Clean Energy Complex Fact Sheet,” airproducts.com.

Project economics increasingly hinge on subsidy structures. Where maximum carbon credits are available, ATR dominates; where brownfield integration advantages count more, SMR retrofits prevail. Technology licensors are locked in a competitive race, Topsoe captured eight ATR awards in 2025 thanks to modular SynCOR units that cut construction time 30%, while Johnson Matthey recorded three for its LCH, underscoring a technology shake-out that will reshape the blue hydrogen market.

By End-User Industry: Transportation Outpaces Refining Growth

Transportation is set for a 58.06% CAGR through 2031, making it the fastest-expanding consumer cluster even as refining retains 39.27% of 2025 demand. California’s Advanced Clean Fleets rule drives the conversion of drayage fleets serving Los Angeles and Long Beach ports, creating a secured pull for 120,000-150,000 t yr of hydrogen. Maritime interest compounds growth: the Port of Rotterdam intends to handle 20% low-carbon fuels by 2030, a target underpinned by early blue-hydrogen bunkering trials. In contrast, refining demand scales linearly with renewable-diesel capacity, keeping the segment’s volume steady but growth modest.

Chemicals absorb 25-30% of demand, mainly ammonia that feeds fertilizers and shipping fuel. Yara’s Sluiskil plant switched to blue hydrogen in 2025, cutting product carbon intensity by 60%. Steel is emerging with pilot direct-reduced-iron lines in Germany and Sweden, consuming 8,000-10,000 t of hydrogen annually and showing 75% emissions abatement. Other industrial uses remain marginal until process-equipment retrofits mature. The diverging trajectories confirm that policy-aligned transport applications will be the principal upside lever for the blue hydrogen market through 2031.

Geography Analysis

Asia-Pacific commanded 38.24% of the 2025 blue hydrogen market and is forecast to grow 59.42% CAGR, the strongest regional pace. China commissioned three Inner Mongolia and Shaanxi facilities totaling 180,000 t yr hydrogen in 2025 and paired them with 1.2 million t yr CO₂ sequestration. South Korea’s first commercial cracking terminals come online in 2026, positioning Busan and Gwangyang as regional import hubs. Japan’s updated hydrogen strategy targets 3 million t yr imports by 2030, 60% from blue ammonia, using legacy LNG terminals for offloading. India pilots blue hydrogen at Mathura but awaits a national carbon price before scaling beyond 2028. Competitive delivered-cost baselines of USD 1.20-1.50 kg, plus ample CCS geology, anchor Asia-Pacific’s cost leadership even as certification lags restrict export access to European RFNBO markets.

North America leverages IRA 45V credits to secure most of the regional capacity within the United States. ExxonMobil’s Baytown and Air Products’ Louisiana projects together add 1.5 million t yr by 2028. Canada’s Edmonton region hosts four operating facilities and plans to triple output by 2030 through the Pathways Alliance, capitalizing on proven saline aquifer storage. Mexico’s participation is exploratory only. Post-2032 sunset clauses for 45V create long-term policy risk that could strand 40-50% of un-sanctioned plans, making subsidy durability the critical variable.

Europe presents a mixed picture. RFNBO mandates guarantee demand, yet high gas prices and methane-certification delays slow new FIDs. Germany’s EUR 3 billion fund backed only Linde’s Leuna and Uniper’s Wilhelmshaven projects to date. United Kingdom clusters HyNet and East Coast supply 80,000 t yr hydrogen under GBP 1.50 kg contracts-for-difference, but broader uptake hinges on resolving liability for CO₂ storage. France and Italy focus on green hydrogen, leaving blue to refinery retrofits. Middle East-Africa and South America are early-stage exporters: Saudi Aramco’s Jafurah rises to 1.5 million t yr blue ammonia by 2025, while Petrobras pilots CCS-enabled hydrogen in Brazil, both targeting premium Northeast Asian demand.

Competitive Landscape

The Blue Hydrogen market is moderately consolidated. White-space opportunities lie in mid-scale plants (30-80 kt yr) serving regional chemical clusters. Engineering contractors such as Technip Energies aim to fill this gap with modular ATR-CCS packages. Disruptive entrants pursue methane pyrolysis; BASF and Monolith bet on premium carbon-black sales above USD 800 t to co-fund hydrogen output, though market depth is uncertain. The looming decline in electrolyzer capex could squeeze blue hydrogen’s cost cushion to under USD 0.30 kg by 2030 in renewable-rich regions, intensifying competitive pressure and making early asset monetization critical.

Blue Hydrogen Industry Leaders

Air Liquide

Air Products and Chemicals, Inc.

Linde PLC

Shell plc

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Exxon Mobil paused plans to build blue hydrogen production facilities in Baytown, United States, due to weak customer demand. The company and its partners, including Abu Dhabi National Oil Company (ADNOC), had invested about USD 500 million into the project so far.

- March 2025: Saudi Aramco, in partnership with Air Products Qudra, acquired a 50% stake in Blue Hydrogen Industrial Gases Company (BHIG) to enhance the production and supply of blue hydrogen in Saudi Arabia's Eastern Province.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the blue hydrogen market as all hydrogen that is generated from natural-gas reforming routes, principally Steam Methane Reforming and Autothermal Reforming, where at least 90 % of the process CO₂ is captured and permanently stored or utilized.

Scope Exclusion: Production routes without carbon capture (gray hydrogen) and renewable electrolysis routes (green hydrogen) are excluded.

Segmentation Overview

- By Technology

- Steam Methane Reforming (SMR) + CCS

- Autothermal Reforming (ATR) + CCS

- Gas Partial Oxidation (GPOX) + CCS

- Natural-Gas Pyrolysis / NGD

- Integrated SMR–ATR Hybrid

- By End-user Industry

- Refining

- Chemicals

- Iron and Steel

- Transportation

- Other Industries (Cement, Glass, Food, and more)

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Discussions were held with reformer licensors, carbon-transport operators, and procurement leads at refineries and chemical complexes across North America, Europe, the Gulf, and East Asia. These conversations clarified current capture rates, realistic capacity factors, and price pass-throughs, helping us reconcile desk findings and calibrate regional assumptions.

Desk Research

Mordor analysts began with public datasets such as the IEA Hydrogen Projects Database, US EIA natural-gas balances, Eurostat emission registries, and CCUS capacity ledgers published by the Global CCS Institute, followed by trade-group digests from the Hydrogen Council and the Asia Natural Gas and Energy Association. Company 10-Ks, refinery turnaround reports, and government tender portals added facility-level context. Subscription resources, including D&B Hoovers for company financials and Dow Jones Factiva for deal flow, were consulted to validate ownership structures and commissioning timelines. The sources listed illustrate the evidence base; many additional documents were consulted during data collection and cross-checks.

Market-Sizing and Forecasting

A top-down build triangulated national natural-gas reforming capacity, blue-conversion ratios, and weighted capacity utilization. Selective bottom-up checks, announced project roll-ups and sampled contract ASP × volume, were used to fine-tune totals. Key variables driving the model include reformer nameplate capacity, average capture efficiency, regional natural-gas spreads, 45V/ETS incentive values, and industrial hydrogen off-take growth. Forecasts to 2030 employ multivariate regression that links the variables above to expected blue-hydrogen output, with scenario bounds vetted by interviewees.

Data Validation and Update Cycle

Outputs pass three layers of variance testing before sign-off. We compare modeled volumes with pipeline-grade CO₂ injection data and ammonia refinery hydrogen demand, re-querying experts where deviations exceed thresholds. Reports refresh annually and are re-checked for material project or policy shifts before dispatch.

Why Our Blue Hydrogen Baseline Commands Reliability

Published estimates often diverge because firms mix production routes, apply contrasting price decks, or freeze project lists for long periods.

Key Gap Drivers here stem from (i) Mordor's volume-first scope that strips out gray and by-product hydrogen, (ii) our real-time project ledger that is updated each quarter, and (iii) currency neutrality which avoids volatile ASP multipliers that can swing revenue values by double digits year on year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 4.11 million tons (2025) | Mordor Intelligence | - |

| USD 18.2 billion (2022) | Global Consultancy A | Blends gray and blue volumes and applies average spot hydrogen prices without CCS cost adders |

| USD 7.0 billion (2025) | Industry Journal B | Focuses on OECD regions only and counts captive refinery output at historical utilization rates |

| USD 2.51 billion (2025) | Trade Publication C | Uses conservative project pipeline, excludes transportation end-use, and applies 2023 currency rates |

In summary, differing scopes, price assumptions, and refresh cadences explain the wide spread of published figures. By anchoring our baseline to verified capacity, capture efficiency, and contemporaneous policy signals, Mordor Intelligence delivers a transparent, repeatable benchmark that decision-makers can trust.

Key Questions Answered in the Report

How large is the blue hydrogen market in 2026 and how fast will it grow?

How large is the blue hydrogen market in 2026 and how fast will it grow?

Which region is growing the fastest in blue hydrogen demand?

Asia-Pacific leads with a 59.42% CAGR through 2031, underpinned by Japan and South Korea’s import programs and China’s coal-with-CCS projects.

What technology will dominate future blue hydrogen projects?

Autothermal reforming with CCS is scaling the quickest thanks to 95-plus % capture rates that unlock the highest policy incentives.

Why is transportation the fastest-growing end-user segment?

Heavy-duty fuel-cell trucks and maritime bunkering receive strong regulatory support, driving a 58.06% CAGR for transport demand.

How do IRA 45V tax credits affect project economics?

The credit can lower U.S. Gulf Coast production costs from USD 2.00 kg to roughly USD 1.40 kg, converting marginal projects into bankable investments.

Page last updated on: