Aerospace Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

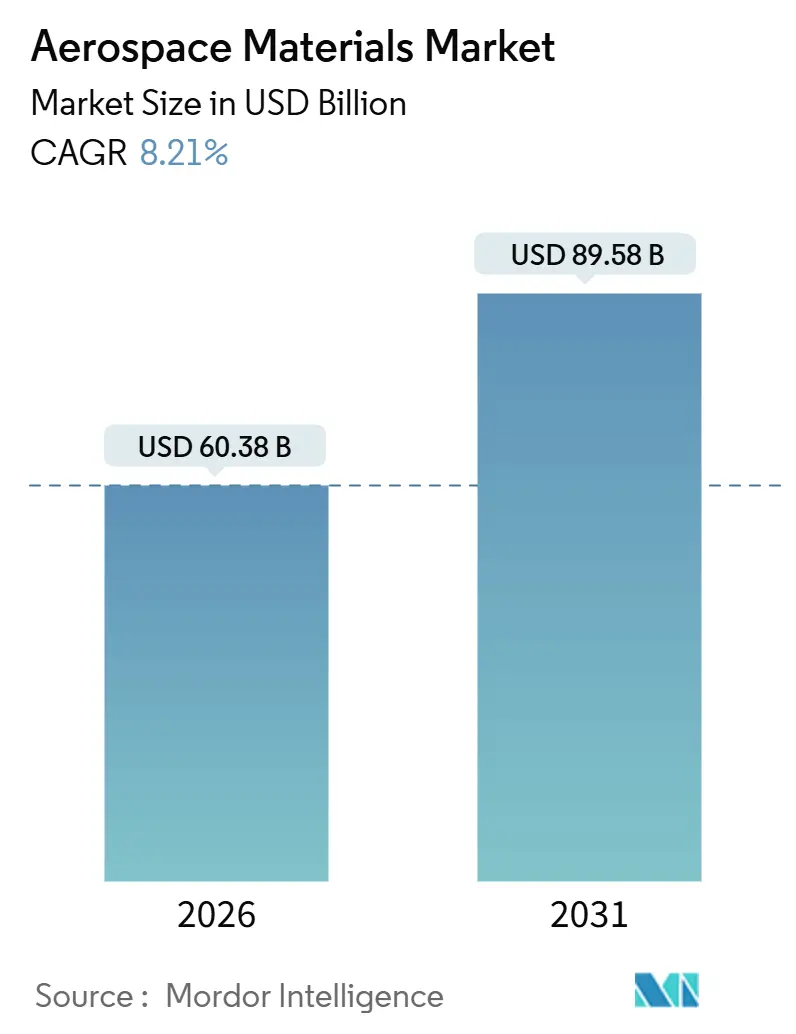

| Market Size (2026) | USD 60.38 Billion |

| Market Size (2031) | USD 89.58 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Materials Market Analysis by Mordor Intelligence

The Aerospace Materials Market size is estimated at USD 60.38 billion in 2026, and is expected to reach USD 89.58 billion by 2031, at a CAGR of 8.21% during the forecast period (2026-2031). Accelerated composite penetration, rising launch cadence in the space sector, and corporate carbon-neutral roadmaps are the principal vectors of growth for the aerospace materials market. Airlines favor lighter airframes to curb fuel burn, while launch providers increasingly specify superalloys and thermal-protection systems that boost material spend per kilogram of payload. OEMs are localizing supply chains to hedge tariff risk, thereby tilting regional demand toward Asia-Pacific even as North America and Europe retain their innovation edge. Simultaneously, additive manufacturing is shrinking lead times for certified parts, enhancing design freedom, and keeping incumbent suppliers under price pressure.

Key Report Takeaways

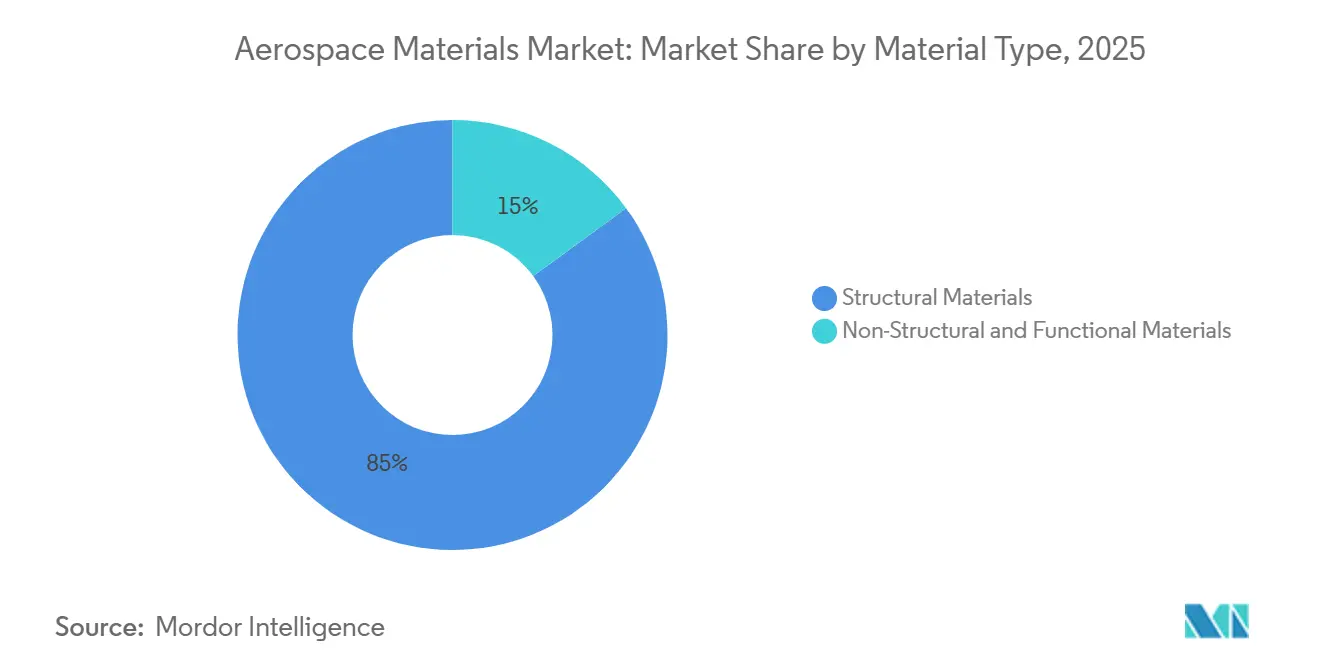

- By material type, structural materials had the largest market share of of the aerospace materials market 85.04% in 2025 and are also forecasted to grow with a CAGR of 8.42% during the forecast period (2026-2031).

- By aircraft type, general and commercial had the most market share of 55.82% in 2025, and the demand for space vehicles is expected to grow with a CAGR of 11.08% during the forecast period (2026-2031).

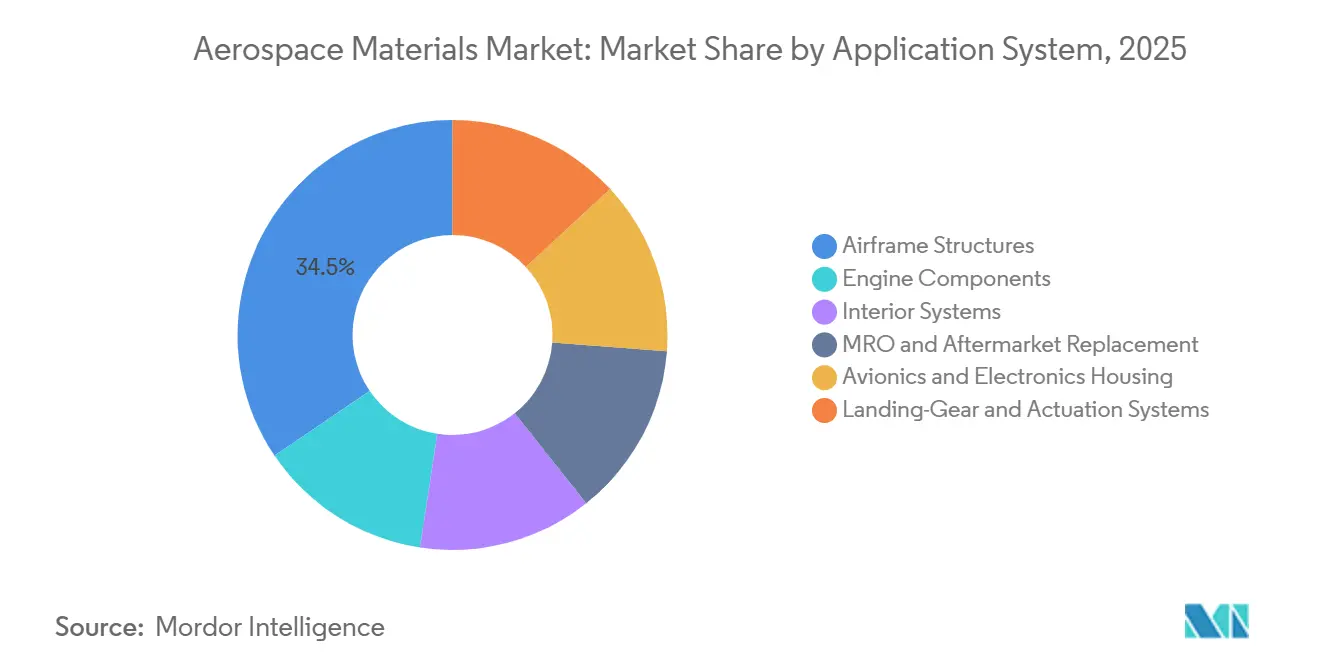

- By application system, airframe structures had the largest market share of 34.47% in 2025, and the market share of MRO (maintenance, repair, and operations) and aftermarket replacement is expected to grow with a CAGR of 10.86% during the forecast period (2026-2031).

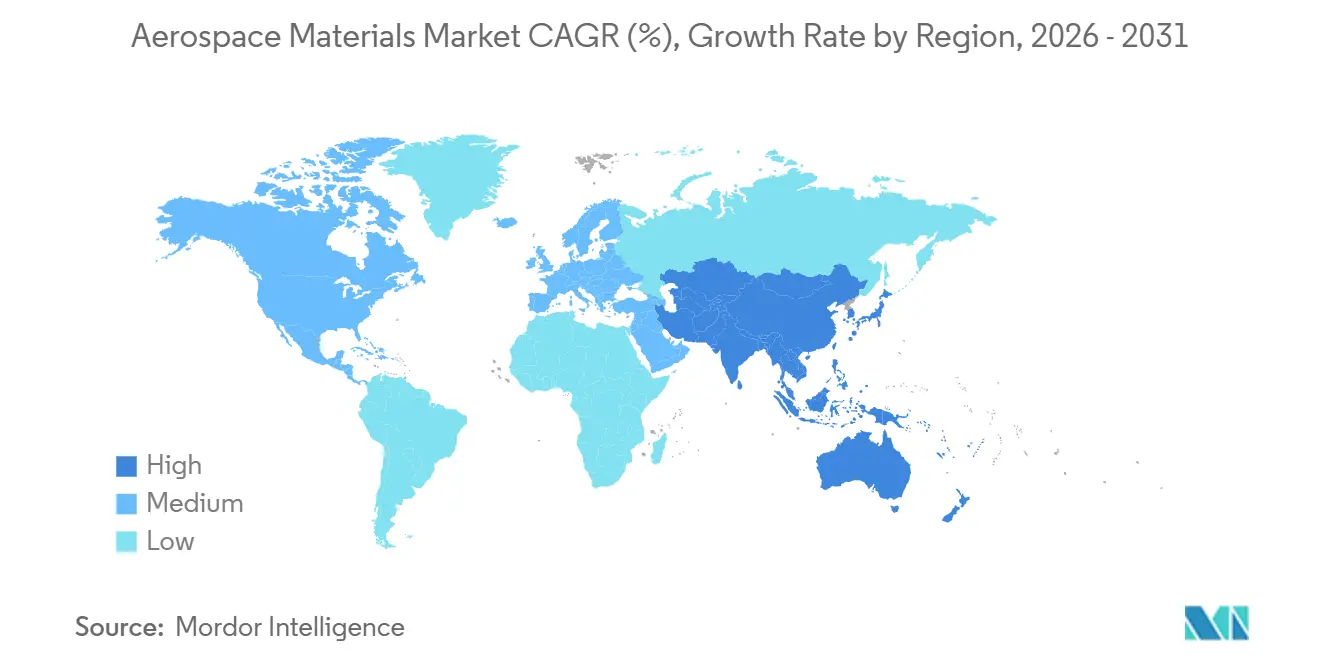

- By geography, Asia-Pacific accounted for 53.65% of the aerospace materials market shareof the market in 2025, and the region is expected to grow at a CAGR of 9.24% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerospace Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight-driven surge in structural composites | +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rapid expansion of space-launch ecosystems | +1.8% | North America, Asia-Pacific, Middle East | Long term (≥ 4 years) |

| OEM carbon-neutral roadmaps | +1.5% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Additive-manufactured certified alloys | +1.3% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Circular-economy mandates | +0.9% | Europe, North America, limited Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweight-Driven Surge in Structural Composites

Composite content surpassed 50% by structural weight in leading twin-aisle programs by 2025, unlocking a 20% reduction in operating weight that translates to 15% lower fuel consumption over a 20-year life cycle[1]Airbus, “A350 XWB Technology Facts,” airbus.com. Even cost-sensitive narrowbody programs are raising composite ratios, with China’s C919 targeting 25% in its next block upgrade. Hexcel and Toray each announced multi-billion-dollar capacity additions to meet this trajectory, leveraging advanced fiber-placement lines that cut labor hours by 35%. Yet regional-jet and turboprop platforms remain predominantly aluminum, preserving a bifurcated material landscape through 2031. Supply-chain bottlenecks, notably in aerospace-grade polyacrylonitrile precursor, still temper the pace of substitution.

Rapid Expansion of Space-Launch Ecosystems

Annual orbital launches tripled between 2020 and 2025, with reusable-rocket providers such as SpaceX flying up to 15 cycles per first stage, a duty profile that demands alloys capable of surviving 1,650°C re-entry temperatures[2]. Blue Origin, ISRO, and emerging Middle Eastern programs have adopted aluminum-lithium, ceramic-matrix composites, and carbon-carbon nose-cone structures to squeeze payload margins. Material qualification cycles are compressing as launch operators iterate hardware every 18-24 months, catalyzing supplier investment in rapid-test infrastructure. Satellite constellations add volume by embedding high-frequency antenna substrates and radiation-hardened panels that raise material intensity per kilogram of spacecraft. Altogether, space-vehicle demand is expected to contribute over USD 15 billion in incremental opportunity for the aerospace materials market by 2031.

OEM Carbon-Neutral Roadmaps Accelerating Material Substitution

Hydrogen propulsion concepts under study at Airbus require cryogenic tanks that operate at -253°C, disqualifying legacy aluminum alloys and steering development toward composite overwrapped pressure vessels. Boeing’s plan for 100% sustainable aviation fuel compatibility by 2030 compels the reformulation of resins and elastomers resistant to higher aromatic content. Turbine makers have introduced ceramic-matrix composites in shrouds and combustors, winning a 1% fuel-burn advantage that compounds across thousands of engines scheduled for delivery by 2031. Regulatory levers such as the EU Carbon Border Adjustment Mechanism heighten the cost of carbon-intensive metals, accelerating composite substitution in Europe and spill-over regions. Collectively, these initiatives underpin a 1.5% uplift in the aerospace materials market CAGR through 2031.

Additive-Manufactured Certified Alloys Enabling Design Freedom

FAA certification of laser-sintered fuel nozzles and EASA approval of 3D-printed landing-gear fittings confirmed additive manufacturing’s suitability for safety-critical hardware in the aerospace materials market. Buy-to-fly ratios plummet from 20:1 in machined titanium to near parity, while lead times shrink from one year to six weeks, freeing working capital for OEMs. Safran, Honeywell, and Rolls-Royce are scaling powder-bed fusion lines that support hundreds of parts per engine, anchoring a market that topped USD 1 billion in 2025. The FAA Advisory Circular 33.15-3, issued in 2025, streamlines process validation, trimming certification cycles for established alloys to three years. Even so, build-size limits and surface-finish constraints confine current adoption mostly to engines and secondary structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & energy intensity of carbon fiber | -1.4% | Global; acute in Asia-Pacific | Short term (≤ 2 years) |

| Strategic-metal supply-chain exposure | -1.1% | Europe, North America | Medium term (2-4 years) |

| Lengthy certification & qualification cycles | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost & Energy Intensity of Aerospace-Grade Carbon Fiber

Producing 1 kg of aerospace-grade carbon fiber consumes 286 MJ of energy and emits 31 kg of CO₂e, quadrupling the carbon footprint of aluminum on a weight basis. Energy price spikes in 2024 raised precursor costs by more than 20%, squeezing margins for integrated producers such as SGL Carbon and Teijin. Small-tow fiber prices remain USD 30–40 per kilogram, twice the cost of industrial large-tow grades. Western firms are co-locating new lines near renewable energy sources in Morocco and Spain to mitigate volatility, while Chinese challengers undercut on price but still lack AS9100 certification for primary structures. Commercial-scale lignin-based precursors promise a 30% energy reduction, but commercialization sits three to five years out.

Strategic-Metal Supply-Chain Exposure

Sanctions on Russian titanium in 2024 severed 35% of global aerospace supply, elevating 6Al-4V billet prices to USD 35 per kilogram and delaying A350 deliveries by 8–12 weeks. Alternative sources from RTI, ATI, and Mishra Dhatu Nigam require 24–36 months of qualification, constraining near-term availability. Substitution is limited; titanium’s 900 MPa tensile strength and 4.5 g/cm³ density remain unmatched for engine mounts and landing gear. Japan and India are expanding sponge capacity, but market balance is unlikely before 2029. Until then, strategic-metal exposure shaves 1.1 percentage points off the aerospace materials market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Structural Dominance Anchors Growth

Structural materials commanded 85.04% of 2025 revenue, reflecting their primacy in fuselage barrels, wing boxes, and empennage assemblies, where weight savings directly impact mission economics. Carbon-fiber-reinforced polymers capture the lion’s share, with Toray and Hexcel together supplying 60% of prepreg consumed in commercial programs. Aluminum-lithium alloys still hold a significant portion of spend inside the structural envelope, leveraging drop-in compatibility with legacy jigs to deliver 7–10% weight reductions without wholesale redesign. Titanium, despite representing just 5% of structural weight, absorbs 12% of value because of its USD 35–40 per kilogram price point. The aerospace materials market size for structural categories is projected to grow at an 8.42% CAGR, outstripping non-structural materials that serve coatings, sealants, and foams.

Non-structural and functional materials underpin mission-critical functions such as corrosion resistance, acoustic damping, and fuel-tank sealing. PPG’s chromate-free primers gained traction as constraints tightened, lifting the firm’s aerospace coatings revenue by 12% in 2025. Henkel’s epoxy adhesives eliminated tens of thousands of fasteners per twin-aisle airframe, cutting assembly hours by 30%. Polyurethane and silicone sealants from 3M and Dow secure pressure boundaries across –55°C to 120°C thermal cycles. Collectively, functional segments defend margins above 20% because of stringent qualification barriers, even as structural materials bear price compression from OEM bargaining power.

By Aircraft Type: Space Vehicles Outpace Legacy Segments

General and commercial aviation retained a 55.82% share in 2025, consuming 50–80 metric tons of materials per aircraft, yet recorded a mid-single-digit CAGR as fleet additions normalized. Narrowbody programs prioritize cost and production cadence, favoring aluminum fuselages paired with composite wings, whereas composite-intensive widebodies invert that mix to shave operating weight. Business-jet OEMs like Gulfstream justify 40% material-cost premiums by extending range beyond 8,000 nautical miles. In contrast, space-vehicle demand is climbing at an 11.08% CAGR, raising the aerospace materials market share for launch systems and satellites.

Defense platforms, though lower in unit count, contribute 30% of value given their appetite for radar-absorbent laminates, single-crystal turbine blades, and boron-fiber composites. The aerospace materials market size for unmanned systems is also expanding fast, as attractive drone concepts adopt cost-optimized glass-fiber composites. Overall, space vehicles remain the fastest-growing segment because reusable hardware multiplies per-unit material content in heat shields, propellant tanks, and engine chambers.

By Application System: MRO Aftermarket Capitalizes on Fleet Aging

Airframe structures represented 34.47% of 2025 spend, driven by composite-rich wings like Boeing’s 71.8-meter 777X span employing T1100G carbon fiber for stiffness. Engine systems incorporate ceramic-matrix composites that endure temperatures surpassing 1,500°C, allowing a 10% reduction in cooling-air bleed that enhances fuel efficiency. Interior systems are adopting thermoplastic laminates that pare 200–300 kg from cabin weight while meeting flammability codes. Landing-gear assemblies, though small in share, remain titanium-intensive and are beginning to integrate additive-manufactured topology-optimized components, achieving 30% weight reductions in the latest A320neo certification.

Maintenance, repair, and overhaul plus aftermarket replacement are the fastest-growing slice at 10.86% CAGR, buoyed by an 11.5-year average fleet age and supply-chain bottlenecks that extend OEM lead times. The aerospace materials market size for MRO applications will exceed USD 20 billion by 2031, driven by parts-manufacturer-approval alternatives that save operators up to 50% versus OEM list prices. Composite repair stations are proliferating, with GKN Aerospace expanding Dutch capacity to process 737 MAX and A320neo panels after a 40% jump in reported damage incidents in 2024-2025.

Geography Analysis

Asia-Pacific dominated the aerospace materials market with a 53.65% share in 2025 and is on track for a 9.24% CAGR to 2031. COMAC delivered 39 C919s in 2025 and plans annual output of 150 units by 2028, each airplane absorbing 45 t of aluminum, 8 t of titanium, and 12 t of composites, mostly sourced from domestic suppliers. India logged 1,200 heavy maintenance events in 2025 as Air India and IndiGo repatriated work, lifting demand for structural adhesives and replacement panels. Japan exports USD 2.8 billion in carbon-fiber prepreg annually, with Toray’s Nagoya site feeding 40% of global supply, while South Korea’s KF-21 fighter requires 25% composites by weight. ASEAN members attracted USD 1.2 billion in aerostructures foreign direct investment between 2024 and 2025, broadening the regional supplier base.

North America is anchored by Boeing, Lockheed Martin, and SpaceX production hubs in the aerospace materials market. SpaceX alone consumed 25 t of aluminum-lithium and 8 t of composites per Falcon 9, flying 96 missions in 2024 and 72 more by mid-2025. Policy support via the CHIPS and Science Act earmarks USD 500 million for advanced material plants, aiming to rebalance import dependence for carbon fiber and titanium. Canada’s Quebec cluster supplies 15% of global landing-gear forgings, while Mexico’s aerospace exports hit USD 9.2 billion in 2025 as tier-2 machining capacity scaled in Queretaro and Chihuahua.

Europe is supported by Airbus’s multi-site assembly network requiring constant feeds of composites, aluminum alloys, and titanium. Production delays in the A320neo narrowed regional volume 3% in 2025, but widebody throughput remained steady as A350 deliveries reached 80 units. Germany’s Premium Aerotec, France’s Safran, and the U.K.’s GKN Aerospace jointly processed more than 11,500 t of titanium and nickel superalloys in 2025. Post-Brexit customs friction added 5–8% to U.K. logistics costs, prompting suppliers to shift machining lines toward Poland and Czechia.

South America and Middle East & Africa combined for a smaller market share in the aerospace materials market but exhibit pockets of growth, notably in Embraer’s E2 series and Saudi Arabia’s localization push.

Competitive Landscape

The Aerospace Materials market is moderately consolidated. Toray and Hexcel dominate carbon-fiber prepreg, leveraging end-to-end control from PAN precursor to autoclave curing, which shields gross margins at roughly 20%. Howmet’s USD 400 million acquisition of Arconic’s extrusion unit in 2025 consolidated 60% of North American capacity, lowering billet conversion costs via integrated ingot casting. Solvay and BASF are racing to commercialize recyclable thermoplastic matrices that promise 30% lower embedded carbon. As of 2026, additive manufacturing penetrated 12% of engine-component spend but less than 2% of primary airframe structures, leaving incumbents’ composite lay-up franchises intact for the medium term.

Aerospace Materials Industry Leaders

Toray Industries Inc.

Hexcel Corporation

Solvay

ATI

Corporation VSMPO-AVISMA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: SeAH Aerospace & Defense Materials, a subsidiary of SeAH Besteel Holdings, secured a pivotal partnership with Boeing. Under this long-term supply agreement (LTA), SeAH will provide high-strength aluminum alloy materials. Beginning in 2026, these aluminum materials will be integral to the fuselage and wings of Boeing's aircraft.

- October 2025: At PTC Industries' Strategic Materials Technology Complex in Lucknow, Uttar Pradesh, India, the Defence Minister inaugurated one of the nation's pioneering Titanium and Superalloy Materials Plants. Additionally, PTC Industries Limited and Bharat Dynamics Limited (BDL) inked an MoU, establishing a joint venture focused on the production of propulsion systems, aero-engines, and more.

Global Aerospace Materials Market Report Scope

Aerospace materials are critical in aircraft manufacturing and must possess various characteristics such as strength and high heat resistance. The materials should be durable and have a high tolerance to damage, which is essential for fuselages. These materials are also chosen for their long lifespan and reliability, especially for fatigue resistance.

The aerospace materials market is segmented by material type, aircraft type, application system, and geography. By type, the market is segmented into structural and non-structural and functional materials. By aircraft type, the market is segmented into general and commercial, military and defense, and space vehicles. By application system, the market is segmented into airframe structures, engine components, interior systems, MRO and aftermarket replacement, avionics and electronics housing, and landing-gear and actuation systems. The report also covers the market size and forecasts for the aerospace materials market in 16 countries across the region. For each segment, the market sizing and forecasts are done based on revenue (USD).

| Structural Materials | Composites | Glass Fiber |

| Carbon Fiber | ||

| Aramid Fiber | ||

| Other Composites (Ceramic-Matrix Composites, etc.) | ||

| Plastics | ||

| Alloys | Aluminum and Al-Li Alloys | |

| Titanium Alloys | ||

| Steel Alloys | ||

| Superalloys (Ni, Co) | ||

| Magnesium Alloys | ||

| Other Alloys | ||

| Non-Structural and Functional Materials | Coatings | |

| Adhesives and Sealants | Epoxy | |

| Polyurethane | ||

| Silicone | ||

| Other Adhesives and Sealants (Bio-based Adhesives, etc.) | ||

| Foams | Polyethylene | |

| Polyurethane | ||

| Other Foams (Thermoplastic Foams, etc.) | ||

| Seals | ||

| General and Commercial |

| Military and Defense Aircraft |

| Space Vehicles |

| Airframe Structures |

| Engine Components |

| Interior Systems |

| MRO and Aftermarket Replacement |

| Avionics and Electronics Housing |

| Landing-Gear and Actuation Systems |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Structural Materials | Composites | Glass Fiber |

| Carbon Fiber | |||

| Aramid Fiber | |||

| Other Composites (Ceramic-Matrix Composites, etc.) | |||

| Plastics | |||

| Alloys | Aluminum and Al-Li Alloys | ||

| Titanium Alloys | |||

| Steel Alloys | |||

| Superalloys (Ni, Co) | |||

| Magnesium Alloys | |||

| Other Alloys | |||

| Non-Structural and Functional Materials | Coatings | ||

| Adhesives and Sealants | Epoxy | ||

| Polyurethane | |||

| Silicone | |||

| Other Adhesives and Sealants (Bio-based Adhesives, etc.) | |||

| Foams | Polyethylene | ||

| Polyurethane | |||

| Other Foams (Thermoplastic Foams, etc.) | |||

| Seals | |||

| By Aircraft Type | General and Commercial | ||

| Military and Defense Aircraft | |||

| Space Vehicles | |||

| By Application System | Airframe Structures | ||

| Engine Components | |||

| Interior Systems | |||

| MRO and Aftermarket Replacement | |||

| Avionics and Electronics Housing | |||

| Landing-Gear and Actuation Systems | |||

| By Geography | Asia-Pacifc | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the projected value of the aerospace materials market in 2031?

The aerospace materials market is forecast to reach USD 89.58 billion by 2031, growing at an 8.21% CAGR.

Which region leads demand growth through 2031?

Which region leads demand growth through 2031?

Which material category holds the largest revenue share in the aerospace materials industry?

Which material category holds the largest revenue share?

Why are space vehicles the fastest-growing aircraft segment?

Why are space vehicles the fastest-growing aircraft segment?

How does additive manufacturing affect supply chains?

How does additive manufacturing affect supply chains?

Page last updated on: