Isoprene Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.36 Billion |

| Market Size (2031) | USD 5.58 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

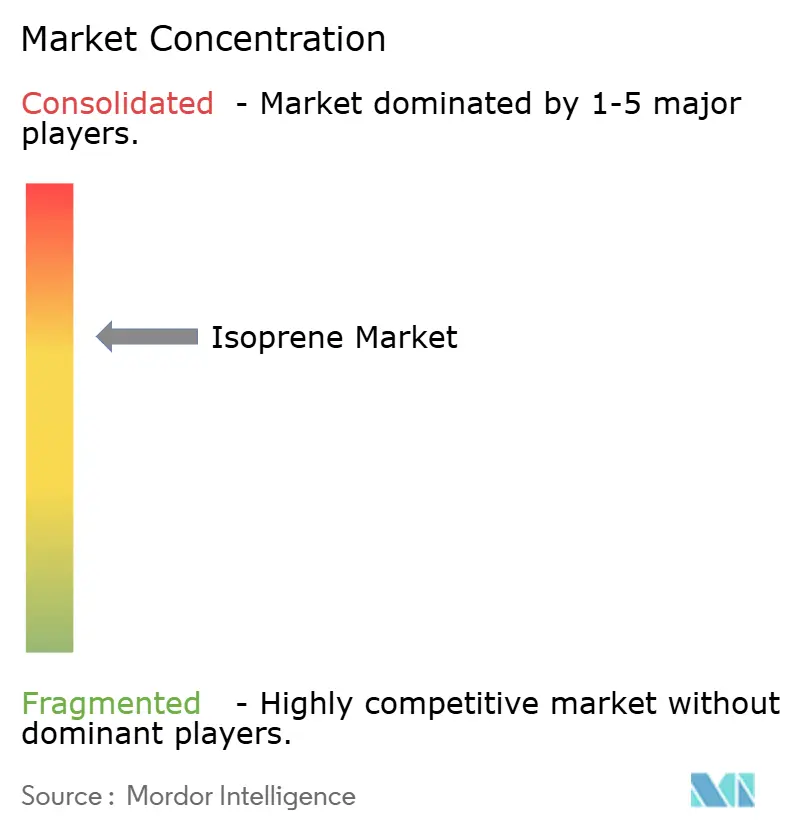

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Isoprene Market Analysis by Mordor Intelligence

The isoprene market size is expected to grow from USD 4.15 billion in 2025 to USD 4.36 billion in 2026 and is forecast to reach USD 5.58 billion by 2031 at 5.06% CAGR over 2026-2031. Growth is propelled by automakers’ shift toward high-performance synthetic elastomers for electric-vehicle (EV) tires, expanding bio-based feedstock trials, and Asia-Pacific’s dominance in manufacturing that supplies over half of global volumes. Polymer-grade materials retain a premium as tire manufacturers prioritize consistent cure rates, while healthcare demand for ultra-pure polyisoprene accelerates on the back of medical-device innovation. Bio-fermentation routes gain strategic importance as petrochemical producers hedge crude-oil volatility through renewable integration, supported by recent capital flows into fermentation start-ups. Competitive intensity rises as fermentation specialists and alternative-rubber innovators challenge conventional C5-cracking economics, nudging incumbents toward joint ventures and feedstock diversification.

Key Report Takeaways

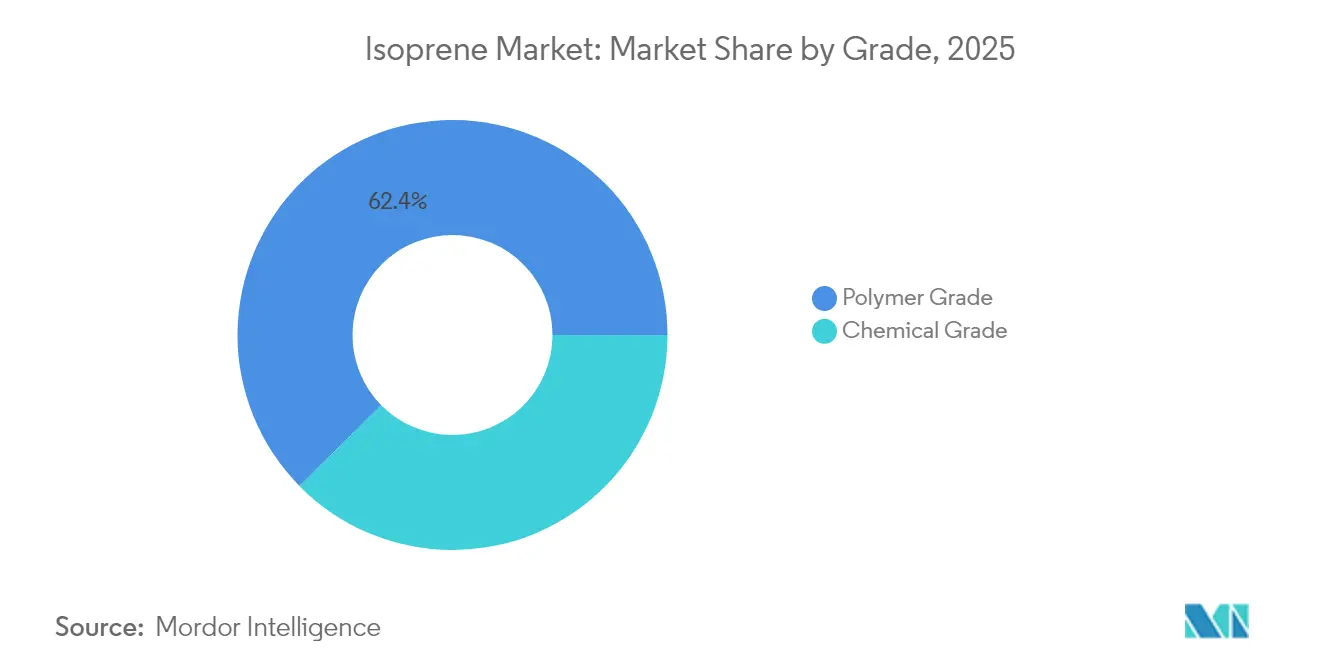

- By grade, polymer grade led with 62.38% revenue share in 2025; chemical grade is forecast to expand at 6.02% CAGR through 2031.

- By production route, petrochemical C5 cracking held 69.98% of isoprene market share in 2025, whereas fermentation routes are projected to record a 6.55% CAGR through 2031.

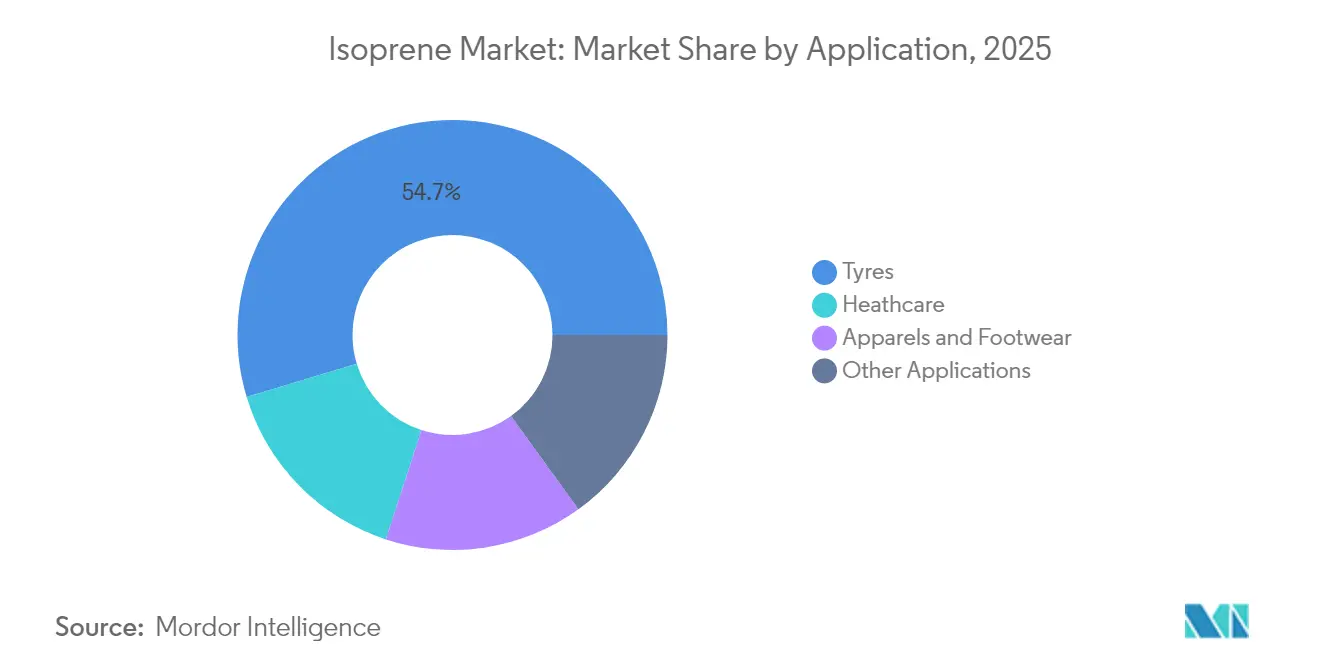

- By application, tires retained 54.66% of the isoprene market size in 2025 and healthcare applications are advancing at 6.27% CAGR to 2031.

- By geography, Asia-Pacific captured 51.12% of the isoprene market size in 2025 and is growing at 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Isoprene Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-led surge in synthetic-rubber demand for high-performance tyres | +1.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Investments in bio-based isoprene routes to cut petro-feedstock risk | +0.8% | North America & EU regulatory push, APAC production | Long term (≥ 4 years) |

| Rising healthcare demand for ultra-pure polyisoprene medical devices | +0.6% | North America & EU markets, APAC manufacturing | Medium term (2-4 years) |

| Asia-Pacific automotive capacity expansion boosting C5 extraction | +0.9% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| 3-D-printed footwear adopting isoprene-based thermoplastic elastomers | +0.4% | Global, with North America & EU early adoption | Medium term (2-4 years) |

| Low-VOC interior adhesives shifting towards low-odor polyisoprene | +0.3% | North America & EU regulatory markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Led Surge in Synthetic-Rubber Demand for High-Performance Tires

Higher torque loads in EVs mandate polymers with superior tensile strength and reduced rolling resistance, directing tire makers toward consistent isoprene formulations that natural rubber cannot guarantee. The US EPA notes over 3 billion tires produced annually, with EV-specific compounds requiring enhanced durability for battery-range preservation[1]United States Environmental Protection Agency, “Tire Pollution Study,” epa.gov. Michelin’s exploration of bio-based synthetic rubber underscores the redesign imperative facing tire compounds. Asia-Pacific’s EV manufacturing concentration magnifies regional pull for isoprene, thereby sustaining a structural uplift in demand beyond the typical replacement cycle.

Investments in Bio-Based Isoprene Routes to Cut Petro-Feedstock Risk

Fermentation technologies such as IFPEN’s Atol and the BioButterfly project confirm the technical feasibility of converting renewable ethanol into polymer-grade isoprene. Global Bioenergies’ industrial isobutene output and Insempra’s USD 20 million funding round highlight the growing investor appetite for renewable C5 chemistry. Cost-parity forecasts indicate fermentation will approach petro-routes within the forecast window, particularly in regions with surplus bio-ethanol.

Rising Healthcare Demand for Ultra-Pure Polyisoprene Medical Devices

Medical-device producers specify latex-free, biocompatible elastomers such as Kraiburg TPE’s expanded medical-grade line offering 30-50 Shore 00 hardness for prosthetic components. Molecular-dynamics studies on cis-1,4-polyisoprene show precise glass-transition control, enabling custom therapeutic performance. Regulatory certification hurdles favor established suppliers with validated supply chains, reinforcing high-value healthcare growth.

Asia-Pacific Automotive Capacity Expansion Boosting C5 Extraction

India’s chemical sector is on track to reach USD 300 billion by 2025, supporting specialty elastomer consumption. Chinese research on bio-coagulated latex pursues elastomer self-sufficiency, complementing synthetic isoprene uptake. Braskem’s joint venture with SCG Chemicals in Thailand offers regional bio-ethylene integration that shortens supply chains for auto manufacturers.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil feedstock price volatility widening producer margins | -0.7% | Global, with higher impact on non-integrated producers | Short term (≤ 2 years) |

| Stricter workplace exposure limits for isoprene monomer (carcinogen) | -0.4% | North America & EU regulatory enforcement | Medium term (2-4 years) |

| Fermentation scale-up bottlenecks delaying commercial BioIsoprene | -0.5% | Global, with focus on bio-based production regions | Medium term (2-4 years) |

| Competition from guayule & dandelion natural-rubber alternatives | -0.3% | North America domestic production, global impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Feedstock Price Volatility Widening Producer Margins

Refinery utilization swings alter C5 fraction availability, pushing input costs higher for non-integrated processors and squeezing margins during crude-price spikes. Although bio-based routes offer price stability, current sugarcane-derived options command premiums between 280% and 752% over fossil routes, challenging near-term competitiveness.

Stricter Workplace Exposure Limits for Isoprene Monomer (Carcinogen)

Health Canada classifies isoprene as a potential carcinogen, banning its use in cosmetics and mandating pollution-prevention plans in synthetic-rubber facilities[2]Government of Canada, “Isoprene Risk Management Document,” canada.ca. Jurisdictions draw on OSHA frameworks for related monomers, signaling potential for lower permissible exposure limits that require advanced engineering controls and medical surveillance. Larger integrated producers can absorb compliance costs while smaller players may delay capacity upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Polymer Dominance Drives Consistency Premium

Polymer grade commanded 62.38% of 2025 revenue and is forecast to advance at 4.98% CAGR to 2031, mirroring demand for uniform cure rates in EV tires. Producers deploy advanced polymerization to achieve lower branching and higher molecular weights that curb heat build-up, benefiting tire longevity. Chemical grade continues serving niche intermediates but faces gradual share erosion as automotive and healthcare sectors value polymer consistency. Elevated purity requirements for surgical devices sustain premium pricing and insulate supply contracts from cyclical auto demand.

By Production Route: Petrochemical Dominance Faces Bio-Based Challenge

Petrochemical C5 cracking accounted for 69.98% share in 2025, benefiting from integrated refinery economics and sunk infrastructure. Capital investment in bio-based fermentation, however, is climbing as firms such as Braskem commit USD 87 million to expand bio-polymer capacity, a move that boosts project draw for renewable isoprene ventures.

Fermentation processes are expanding at a 6.55% CAGR, reflecting technology maturation and policy incentives that reward lower life-cycle emissions. Catalytic conversion of bio-ethanol merges established chemical engineering with renewable feedstocks to deliver a hybrid pathway that could accelerate cost parity. The isoprene market remains anchored in petro-routes, yet the production-route mix is set to diversify as early adopters lock in offtake pacts with tire and medical-device majors.

By Application: Healthcare Growth Challenges Tire Supremacy

Tires dominated with 54.66% market share in 2025, fueled by global vehicle production and short replacement cycles. Rising EV penetration intensifies requirements for polymers that resist instant torque, sustaining tire-application scale. Yet healthcare is projected to climb at 6.27% CAGR through 2031 as polyisoprene enables latex-free alternatives for surgical gloves, catheter tubing, and implantable devices.

The isoprene market size for tire usage reached USD 2.27 billion in 2025 while healthcare logged USD 0.64 billion, with regulatory approvals and biocompatibility standards elevating entry barriers for challengers. Apparel, footwear, and adhesive segments diversify demand, leveraging new 3D-printable elastomers with tensile strength near 94.6 MPa that open design freedoms for mass-customized products.

Geography Analysis

Asia-Pacific’s isoprene market size hit USD 2.12 billion in 2025, and proximity to automotive OEMs offers freight savings that strengthen regional supply stability. China invests in elastomer self-sufficiency through processing advancements that bridge natural and synthetic rubber capability gaps. India’s chemical-industrial growth broadens downstream demand, while Thailand’s bio-ethylene hub creates a springboard for renewable C5 integration.

North American producers expand bio-polymer capacity to 260 kt per year, reflecting corporate attention to consumer pressure for sustainable tires and medical devices. The European Union’s decarbonization policies steer investment toward fermentation and catalytic conversion platforms. Health Canada’s carcinogen classification influences procurement, prompting OEMs to favor suppliers with robust safety protocols. South America’s sugarcane value chain presents a strategic opportunity once cost premiums shrink. Middle Eastern complexes bundle inexpensive Naphtha feed with export logistics that reach Africa’s emerging automotive hubs, while African demand growth hinges on vehicle assembly expansion and infrastructure improvement.

Competitive Landscape

The isoprene market exhibits moderate consolidation. The competitive field consists of integrated petrochemical majors, fermentation start-ups, and agricultural innovators working on guayule and dandelion latex. Braskem’s USD 87 million expansion and its Thailand joint venture signal incumbents’ willingness to scale renewables within petro-portfolios. IFPEN’s Atol technology and Global Bioenergies’ demonstration plant illustrate how intellectual-property holding firms leverage R&D partnerships to accelerate commercialization.

Traditional players focus on operational efficiency and downstream partnerships, whereas disruptors stress carbon-footprint reduction and speed to market. Ohio State University trials with Taraxacum kok-saghyz dandelion improve latex extraction yields, hinting at longer-term displacement risk for monomer-based polymers.

Competitive maneuvering includes supply-chain tie-ups with tire OEMs, medical OEM material approvals, and regional investment in fermentation capacity lined with ethanol corridors. Continuous R&D around catalytic throughput improvements and enzyme-engineering breakthroughs targets lower capex and opex for bio-routes, heightening rivalry across all firm types.

Isoprene Industry Leaders

Shell plc

PJSC SIBUR Holding

LyondellBasell Industries Holdings B.V.

Exxon Mobil Corporation

China Petrochemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2023: The Goodyear Tire & Rubber Company and Visolis announced a collaboration project between the two companies to produce isoprene by upcycling biobased materials. This collaboration is supported by a Small Business Innovation Research (SBIR) grant awarded to Visolis.

- February 2023: Kuraray constructed a new isoprene-related plant in Map Ta Phut, Thailand, under Kuraray GC Advanced Materials and Kuraray Advanced Chemicals, readying staged startup.

Global Isoprene Market Report Scope

Isoprene is an important C5 diolefin that can be polymerized to synthesize rubber, plastics, and other synthetic materials, as well as terpenes compounds. It is highly reactive, and its complex atmospheric reactions have diverse climatic consequences. The majority of industrially manufactured isoprene is used to make polyisoprene, a synthetic equivalent of natural rubber.

The market is segmented by application and geography. By application, the market is segmented into tires, healthcare, apparel and footwear, and other applications. The report also covers the market size and forecasts for the isoprene market in 15 countries across major regions.

For each segment, the market sizing and forecasts have been done based on value (USD million).

| Polymer Grade |

| Chemical Grade |

| Petrochemical C5 Cracking |

| Bio-based Fermentation |

| Catalytic Conversion of Bio-Ethanol |

| Tyres |

| Heathcare |

| Apparels and Footwear |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Grade | Polymer Grade | |

| Chemical Grade | ||

| By Production Route | Petrochemical C5 Cracking | |

| Bio-based Fermentation | ||

| Catalytic Conversion of Bio-Ethanol | ||

| By Application | Tyres | |

| Heathcare | ||

| Apparels and Footwear | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Isoprene Market size?

The isoprene market size stands at USD 4.36 billion in 2026 and is forecast to reach USD 5.58 billion in 2031.

Which segment leads the isoprene market by application?

Tire manufacturing accounts for 54.66% of value in 2025, retaining leadership due to ongoing vehicle production and rising EV tire specifications.

How fast is the healthcare segment growing within the isoprene market?

Healthcare applications are projected to grow at 6.27% CAGR through 2031, outpacing overall market expansion as medical-device makers adopt ultra-pure polyisoprene.

Why are bio-based production routes gaining interest in the isoprene industry?

Bio-based routes reduce exposure to crude-oil volatility and align with decarbonization mandates, with fermentation pathways forecast to achieve cost parity during the outlook period.

Page last updated on: