Vinyl Ester Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

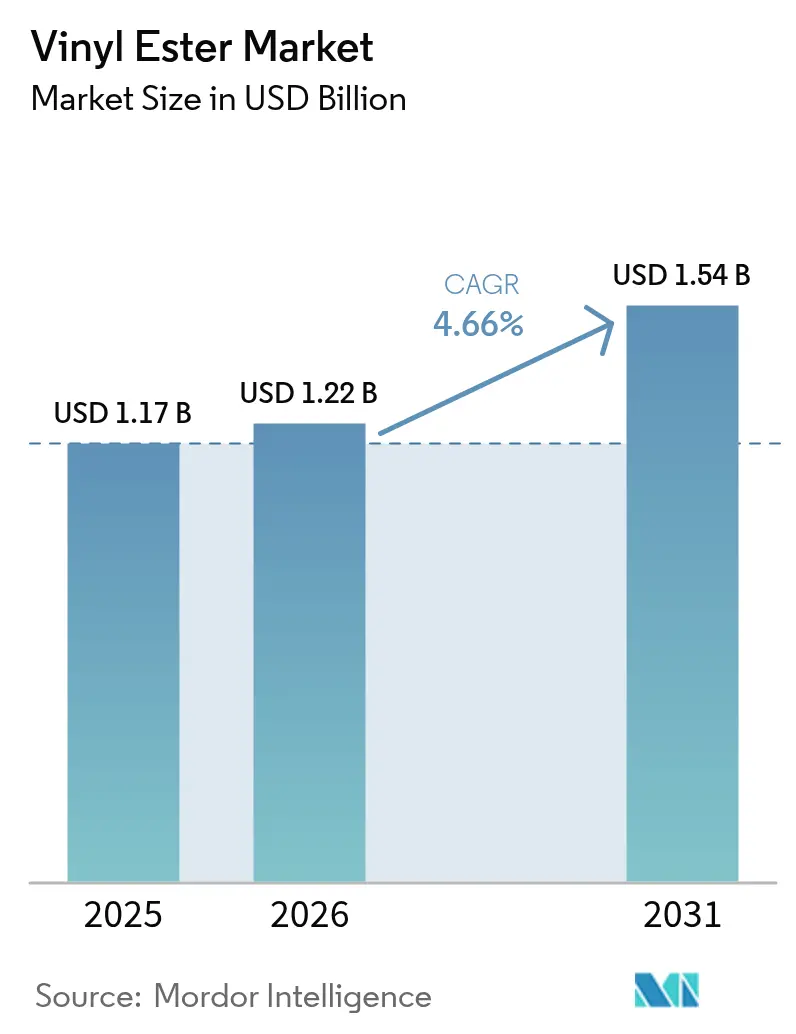

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vinyl Ester Market Analysis by Mordor Intelligence

Vinyl ester market size in 2026 is estimated at USD 1.22 billion, growing from 2025 value of USD 1.17 billion with 2031 projections showing USD 1.54 billion, growing at 4.66% CAGR over 2026-2031. Growth is fueled by demand for corrosion-resistant composites in pipes, tanks, marine structures, and renewable-energy equipment. Continued industrialization in Asia-Pacific, rising refurbishment of chemical plants in North America, and infrastructure upgrades across Europe support steady volume uptake. Competitive activity is marked by portfolio realignment and targeted capacity additions, helping suppliers balance feedstock volatility and tight delivery schedules.

Key Report Takeaways

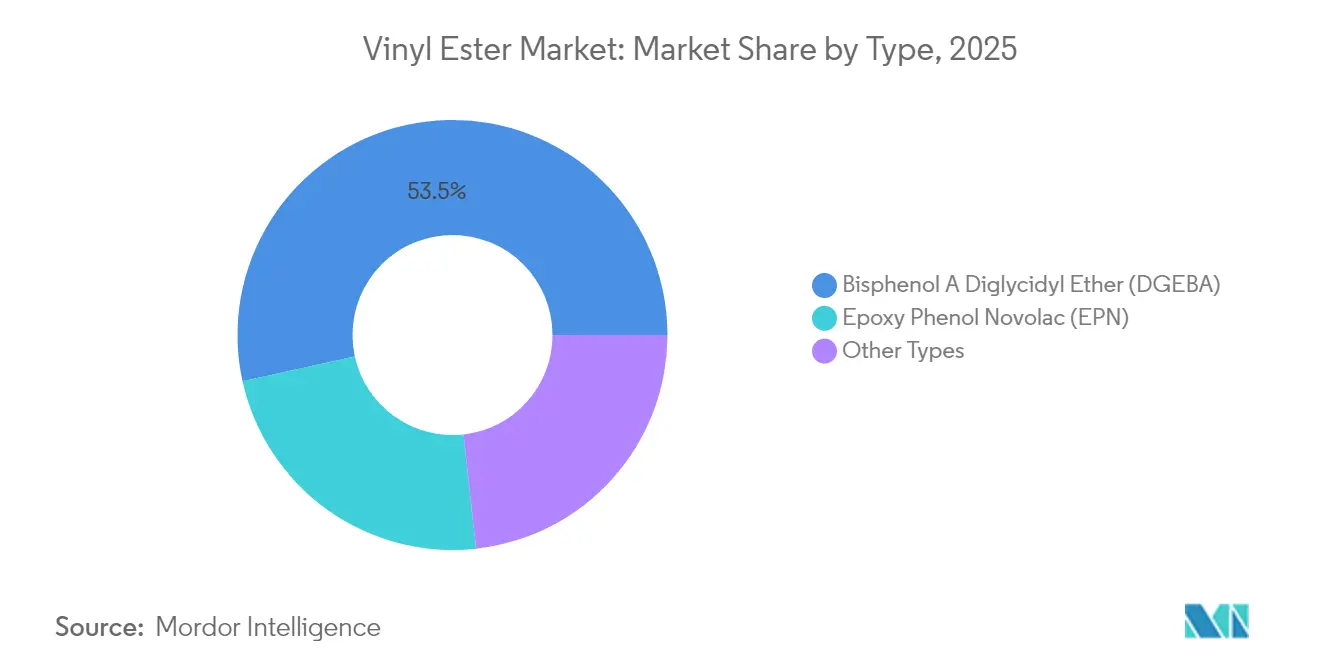

- By type, DGEBA resins led with 53.45% vinyl ester market share in 2025 and is projected to post the fastest CAGR at 4.74% to 2031.

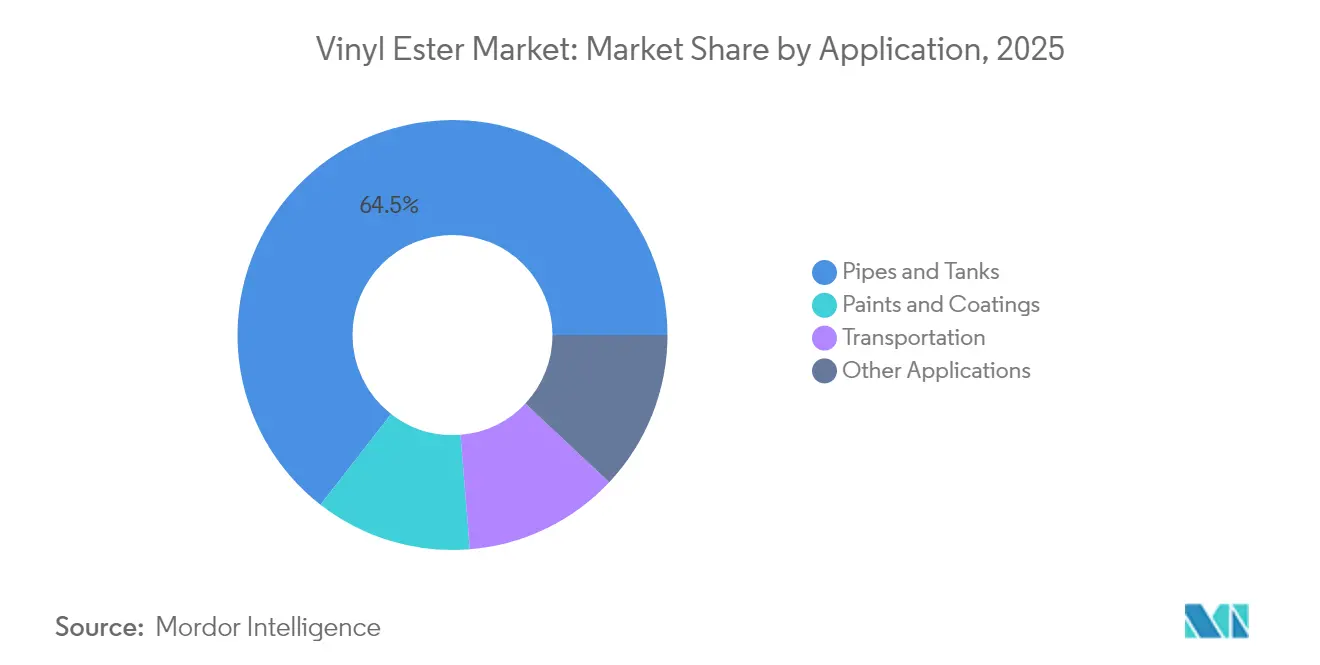

- By application, pipes and tanks captured 64.48% of the vinyl ester market size in 2025 and are expanding at a 4.80% CAGR.

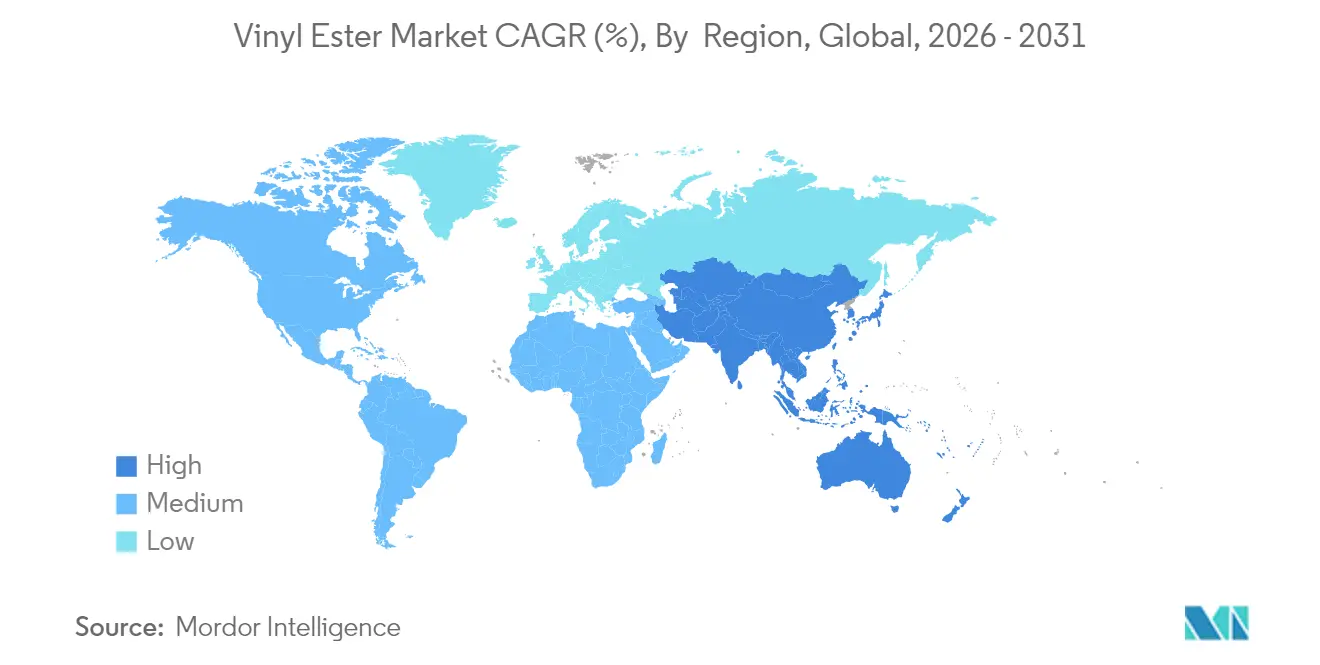

- By geography, Asia-Pacific held 55.60% revenue share of the vinyl ester market in 2025, while the region also records the quickest 4.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Vinyl Ester Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Superior Chemical and Corrosion Resistance | +1.7% | Global, with emphasis on Asia-Pacific and North America | Long term (≥ 4 years) |

| Growing Application in the Manufacture of Fiber Reinforced Plastic Tanks and Vessels | +1.2% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Expansion of Renewable Energy Sector | +0.9% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Growing Demand in Infrastructure and Industrial Applications | +0.7% | Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Advancements in Composite Manufacturing | +0.5% | Global, with emphasis on North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Superior Chemical and Corrosion Resistance

Vinyl ester resins resist acids, alkalis, and solvents better than steel, concrete, or polyester composites, enabling longer service life for chemical processing gear, wastewater assets, and marine platforms. Fewer ester linkages limit hydrolysis, cutting material failures, and shutdown costs. New grades containing silicon-carbide particles boost abrasion resistance for agitators and pump housings. End users increasingly weigh full lifecycle economics, favoring vinyl ester when downtime penalties exceed initial outlay.

Expansion of Renewable Energy Sector

Wind-turbine blades rely on vinyl ester composites for superior fatigue resistance and moisture tolerance. Capacity additions in onshore and offshore parks drive multi-year pull-through for spar caps and nacelle covers[1]International Energy Agency, “Renewables 2024,” iea.org. Hydrogen-storage vessel builders use high-modulus vinyl ester wraps on Type 3 cylinders to meet burst-strength codes. Tin-treated glass/vinyl-ester reflectors achieving 95% solar reflectivity unlock scope in concentrated-solar plants.

Growing Demand in Infrastructure and Industrial Applications

Bridge decks, flue-gas ducts, and polymer-concrete floors benefit from vinyl ester’s combined chemical and mechanical endurance. Formulations reinforced with basalt or carbon fabrics extend spans and resist chloride ingress, lessening repair cycles for coastal highways. Industrial flooring blends using vinyl ester binders exhibit compressive strengths above 90 MPa, supporting heavy process equipment without cracking.

Advancements in Composite Manufacturing

Reuse-capable silicone bagging allows 400–1,000 molding cycles, cutting consumable waste and set-up time. Energy-efficient induction and microwave curing trim composite line power needs are reduced by up to 90%[2]JEC Composites, “Modern Composite Manufacturing with Reusable Silicone Technology,” jeccomposites.com. Direct-ink-written vinyl ester lattices achieve 3.7 GPa modulus, opening additive-manufacturing routes for customized medical and defense parts.

Restraints Impact Analysis of Vinyl Ester Market*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Styrene/Epoxy Feedstock Price Volatility Pressuring Margins | -0.7% | Global, with higher impact in Europe and North America | Medium term (2-4 years) |

| Availability of Substitutes | -0.5% | Global | Medium term (2-4 years) |

| Limited Shelf Life | -0.2% | Global, with higher impact in regions with challenging logistics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Styrene/Epoxy Feedstock Price Volatility Pressuring Margins

Styrene and epoxide monomers faced sharp price spikes in 2024, prompting resin makers to raise list prices for vinyl-ester formulations. Margin protection now hinges on long-term supply deals, hedging, and formula-based pass-through clauses. Research into lower-styrene or styrene-free blends is also accelerating.

Availability of Substitutes

Polyurethane and recyclable thermoplastic composites are winning trial orders thanks to faster cure cycles and lower volatile-organic-compound emissions. Cardanol-based biopolymer epoxies further challenge commodity vinyl ester in green-label projects. Suppliers counter by promoting higher heat-deflection grades and extended-service-life warranties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Vinyl Ester Market Segment Analysis

By Type:

DGEBA Consolidates LeadershipDGEBA resins accounted for 53.45% vinyl ester market share in 2025, underpinned by a cost-to-performance balance suited to marine, chemical, and infrastructure laminates. The segment records a 4.74% CAGR, supported by the ongoing development of low-styrene mixes that ease workplace emission caps. Manufacturers are also pursuing styrene-free DGEBA variants to gain acceptance in tight-ventilation production halls.

Epoxy-phenol-novolac (EPN) resins, though smaller, secure orders for high-temperature scrubbers and acid plants. Brominated grades address flame-spread codes in rail interiors, while elastomer-modified resins supply hull sections needing impact damping. Recent UL 94 V0-compliant compounds maintain tensile strength above 80 MPa, reflecting formulation progress without halogen overuse.

By Application:

Pipes and Tanks Drive VolumePipes and tanks commanded 64.48% vinyl ester market share in 2025 and progress at a 4.80% CAGR. Advances in automated filament winding enable pipe diameters exceeding 3 m while holding dimensional tolerances within ±1 mm.

Coating systems leverage rapid-cure vinyl-ester linings for flue-gas desulfurization ducts and pulp-mill bleaching towers. Transportation uses lighter, tougher panels to shave fuel burn in high-speed ferries and electric bus shells. Self-healing microcapsule technology extends coating life in salt-spray environments beyond 50 days with zero blistering, broadening adoption in coastal infrastructure.

Geography Analysis

APAC Vinyl Ester Market

Asia-Pacific retained a 55.60% revenue share in 2025 and grows fastest at 4.85% through 2031. State-backed rail corridors, desalination projects, and onshore wind farms in China and India underpin the resin offtake. Regional producers benefit from localized supply chains that sidestep transocean freight risks.

North America Vinyl Ester Market

North America is buoyed by refinery overhauls along the Gulf Coast and government incentives for offshore wind arrays. The vinyl ester market size in the United States is also lifted by bridge-deck replacement programs that specify corrosion-resistant composites to extend asset life beyond 75 years.

Europe Vinyl Ester Market

Europe emphasizes recycling and low-styrene emissions, prompting the adoption of next-generation formulations. Grants for hydrogen-demo hubs in Germany and the Netherlands accelerate demand for Type 3 vessels with vinyl-ester liners.

South America and MEA Vinyl Ester Market

South America sees strong orders in Brazil’s water-treatment build-outs and petrochemical capacity additions, while the Middle East applies vinyl-ester composites in desalination piping and chemical handling at new refining complexes. Africa’s mining sector is trialing vinyl-ester lined leach tanks to improve acid resistance in copper extraction circuits.

Competitive Landscape

The vinyl ester market is highly consolidated: the top five suppliers control roughly 60% of global turnover. AOC, Polynt-Reichhold Group, and Ashland concentrate on proprietary binder platforms that cut cure shrinkage and ease pultrusion run rates.

R&D pipelines prioritize bio-content, styrene elimination, and extended pot life. Oxalic-acid stabilization technology lengthens shelf life to six months without latent curing loss, aiding distributors in hot climates[3]U.S. Patent, “Oxalic Acid Stabilized Thermosettable Vinyl Ester Resins,” patents.google.com . Suppliers are also integrating additive manufacturing toolkits to bundle resin and printing filament solutions, creating pull-through for design-for-function components.

Strategic capacity projects cluster near feedstock hubs; for example, expansions in the U.S. Gulf help offset epoxy cost swings while ensuring just-in-time deliveries to wind-blade fabricators. Vertical integration into gelcoats and downstream molding services strengthens switching costs and shields core resin margins.

Vinyl Ester Industry Leaders

AOC

Polynt-Reichhold Group

Ashland Inc.

Interplastic Corporation

ALTA Performance Materials

- *Disclaimer: Major Players sorted in no particular order

Vinyl Ester Market Companies Covered in this Report

- AOC

- Allnex GmbH

- ALTA Performance Materials

- Ashland Inc.

- Changzhou Tianma Group

- DIC Corporation

- Hexion Inc.

- Huntsman Corporation

- Interplastic Corporation

- Nan Ya Plastics

- Poliya Composite Resins

- Polynt-Reichhold Group

- Reichhold LLC2

- Resoltech

- Resonac Holdings Corporation

- Royal DSM

- Scott Bader Co. Ltd

- Sino Polymer Co. Ltd

- Sir Industriale

- Swancor Holding

Recent Industry Developments in Vinyl Ester Market

- February 2025: Allnex GMBH unveiled its latest VIAPAL vinyl ester grades, meticulously designed for superior chemical resistance, which is expected to enhance product offerings and drive growth in the vinyl ester market.

- December 2024: Sir Industriale launched its high-reactivity SIRESTER VE 64-M-140 epoxy-novolac vinyl ester resin, a development expected to positively influence the growth and innovation within the vinyl ester market.

Vinyl Ester Market Report Scope and Research Methodology

Market Definition and Coverage

Mordor Intelligence defines the vinyl ester market as the aggregate revenue generated from neat vinyl-ester resins that are formulated from epoxy precursors and cured with reactive diluents for use in corrosion-resistant composites, coatings, tanks, pipes, marine structures, and renewable-energy components. Measurement covers only virgin resin sales in bulk or pre-accelerated form, expressed in USD at the manufacturer level.

(Scope exclusion) This study does not count unsaturated polyester resins, blended systems containing less than fifty percent vinyl-ester content, or post-consumer recycling streams.

Segments Covered in This Report

- By Type

- Bisphenol A Diglycidyl Ether (DGEBA)

- Epoxy Phenol Novolac (EPN)

- Other Types

- By Application

- Pipes and Tanks

- Paints and Coatings

- Transportation

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Primary Research

Structured interviews with resin formulators, composite fabricators, chemical distributors, and regional trade consultants across North America, Europe, and Asia-Pacific helped verify demand pools, typical selling prices, and upcoming capacity additions. Survey feedback from end users in marine, wind, and chemical processing applications refined adoption-rate assumptions and tested preliminary growth drivers.

Desk Research

Our analysts pulled multi-country production, trade, and consumption data from publicly available customs statistics, the American Composites Manufacturers Association, the European Chemical Industry Council, and the National Bureau of Statistics of China, which outline resin and composite output trends. Price indices and feedstock cost curves were gathered from the US Energy Information Administration, PlasticsEurope, and ICIS Chemical price assessments. Corporate 10-Ks, investor decks, and patent filings supplied company-level revenue and capacity clues, while paid tools such as D&B Hoovers and Dow Jones Factiva enriched competitive intelligence. This list is illustrative; many additional open-source and subscription references supported baseline development, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction started with country-level epoxy and styrene derivative output, adjusted for vinyl-ester penetration and net trade to reach apparent consumption, which was then checked against sampled average selling prices multiplied by indicative volumes from leading suppliers. Key variables like including corrosion-resistant composite demand, flue-gas desulfurization installations, wind-turbine blade additions, refinery turnaround schedules, resin ASP movements, and regional industrial output fed the model. Multivariate regression combined with scenario analysis generated the 2025-2030 trajectory, and bottom-up roll-ups of sampled supplier revenues served as a reasonableness cross-check. Data gaps where supplier disclosure was thin were bridged through channel-partner interviews and regional import records.

Data Validation & Update Cycle

Mordor analysts run variance and consistency checks, benchmark outputs against independent production statistics, and escalate anomalies for senior review. The model is refreshed annually, with interim updates triggered by raw-material price shocks, sizable capacity announcements, or regulatory shifts. Each release undergoes a final analyst pass to ensure clients receive the freshest view.

How Mordor Intelligence's Vinyl Ester Market Size Compares to Other Published Estimates

Published values differ because consultancies select dissimilar functional scopes, forecasting horizons, and currency bases. Volume-to-value conversions, price escalation logic, and refresh cadence further widen gaps.

Key gap drivers here include whether paints and coatings are in scope, how rapidly average selling prices escalate, and how primary research is weighted when supplier disclosures are scarce. Mordor Intelligence keeps a balanced scope, applies moderated ASP curves, and refreshes annually, whereas some peers rely on capacity roll-ups or outdated base years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.17 B (2025) | Mordor Intelligence | - |

| USD 1.04 B (2024) | Global Consultancy A | Excludes paints and coatings; uses 2023 exchange rates without adjustment |

| USD 1.30 B (2023) | Industry Research Firm B | Derives totals from supplier capacity and assumes higher ASP inflation |

The comparison shows estimates can swing by almost USD 0.25 B. Because Mordor links resin demand to clearly tracked industrial indicators and validates every assumption through direct market sounding, clients gain a transparent, repeatable baseline they can rely on for planning and investment discussions.

Key Questions Answered in the Report

What is the current size of the vinyl ester market?

The vinyl ester market size was USD 1.22 billion in 2026 and is projected to reach USD 1.54 billion by 2031.

Which segment leads the vinyl ester market by application?

Pipes and tanks hold 64.48% of 2025 revenue, benefiting from high corrosion-resistance needs in chemical and water-treatment plants.

Why is Asia-Pacific the largest regional market?

The region’s industrial build-out, infrastructure expansion, and wind-energy projects collectively consume the largest volume of vinyl ester composites.

How are manufacturers tackling styrene emissions?

Suppliers are developing low-styrene and styrene-free vinyl ester grades and pairing them with energy-efficient curing to meet stricter workplace and environmental standards.

Page last updated on: