Synthetic Latex Polymers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

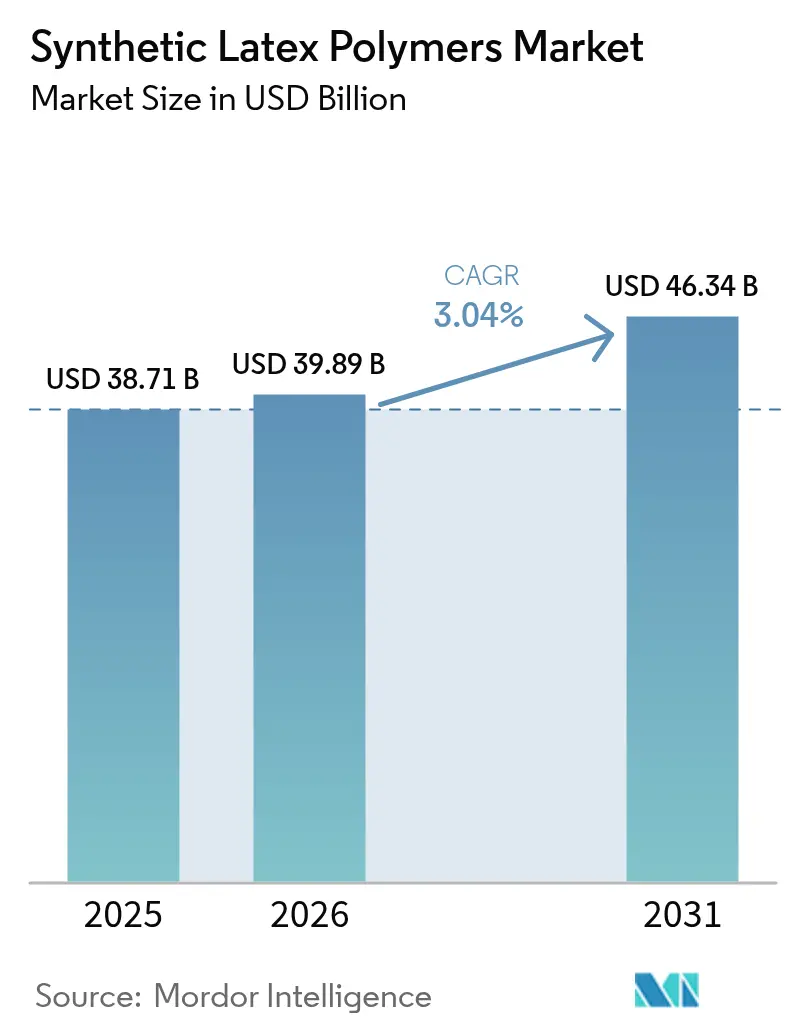

| Market Size (2026) | USD 39.89 Billion |

| Market Size (2031) | USD 46.34 Billion |

| Growth Rate (2026 - 2031) | 3.04% CAGR |

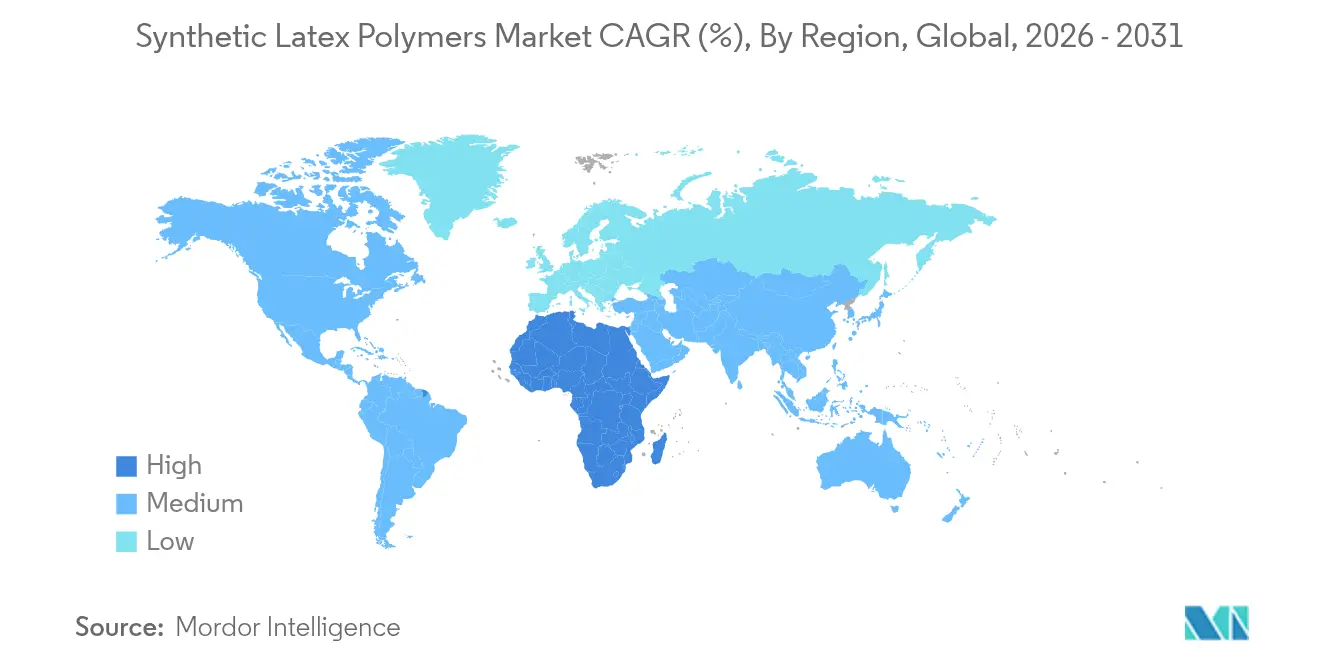

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

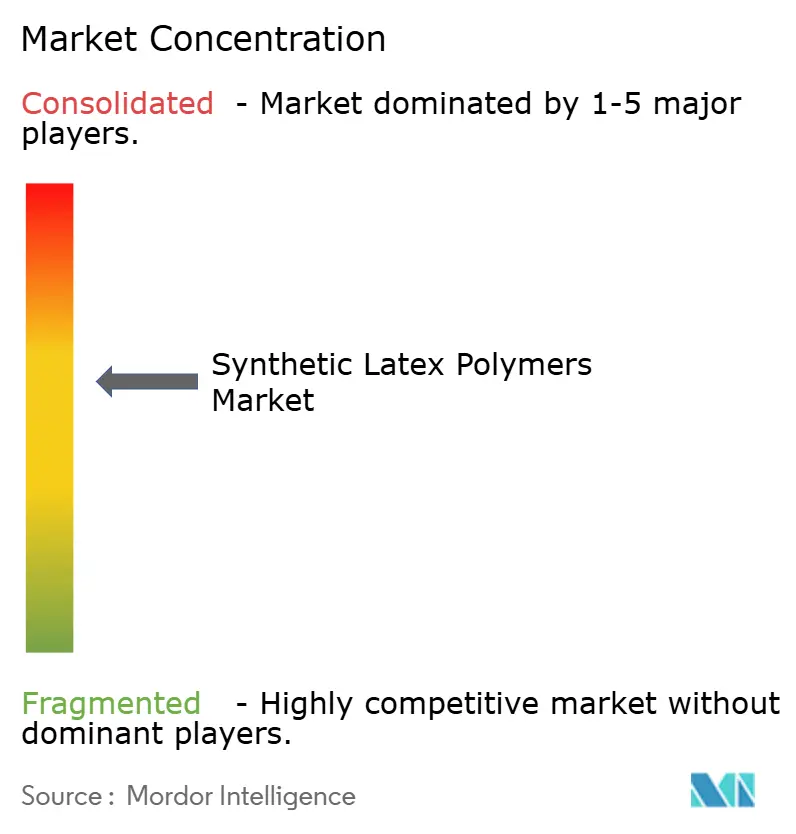

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Latex Polymers Market Analysis by Mordor Intelligence

The synthetic latex polymers market size in 2026 is estimated at USD 39.89 billion, growing from 2025 value of USD 38.71 billion with 2031 projections showing USD 46.34 billion, growing at 3.04% CAGR over 2026-2031. A mix of regulatory mandates and performance-driven reformulations underpins this growth, as end users pivot to water-based systems that align with volatile organic compound limits and emerging sustainability targets. Construction programs in emerging economies, rising demand for low-VOC architectural coatings, and incremental medical uptake keep volumes expanding, even as certain mature applications such as carpet backing plateau in North America and Europe. Competitive intensity now centers on sustainable feedstocks, circular economy credentials, and supply security, with global players pursuing bio-based chemistries and plant modernization to safeguard margins. At the same time, regional champions leverage integrated feedstocks and customer proximity to defend share in price-sensitive segments, preserving a dynamic yet increasingly compliance-oriented competitive landscape.

Key Report Takeaways

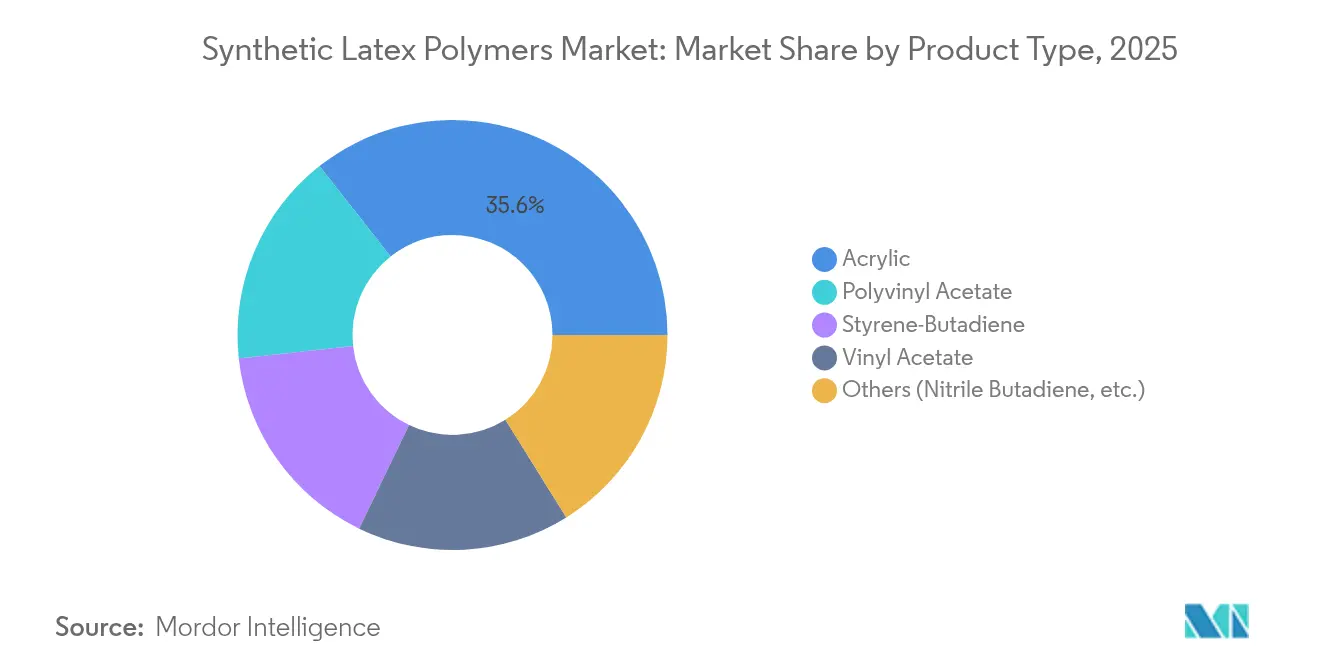

- By polymer type, acrylics captured 35.62% of the synthetic latex polymers market share in 2025; the same polymer group is set to register a 3.42% CAGR through 2031.

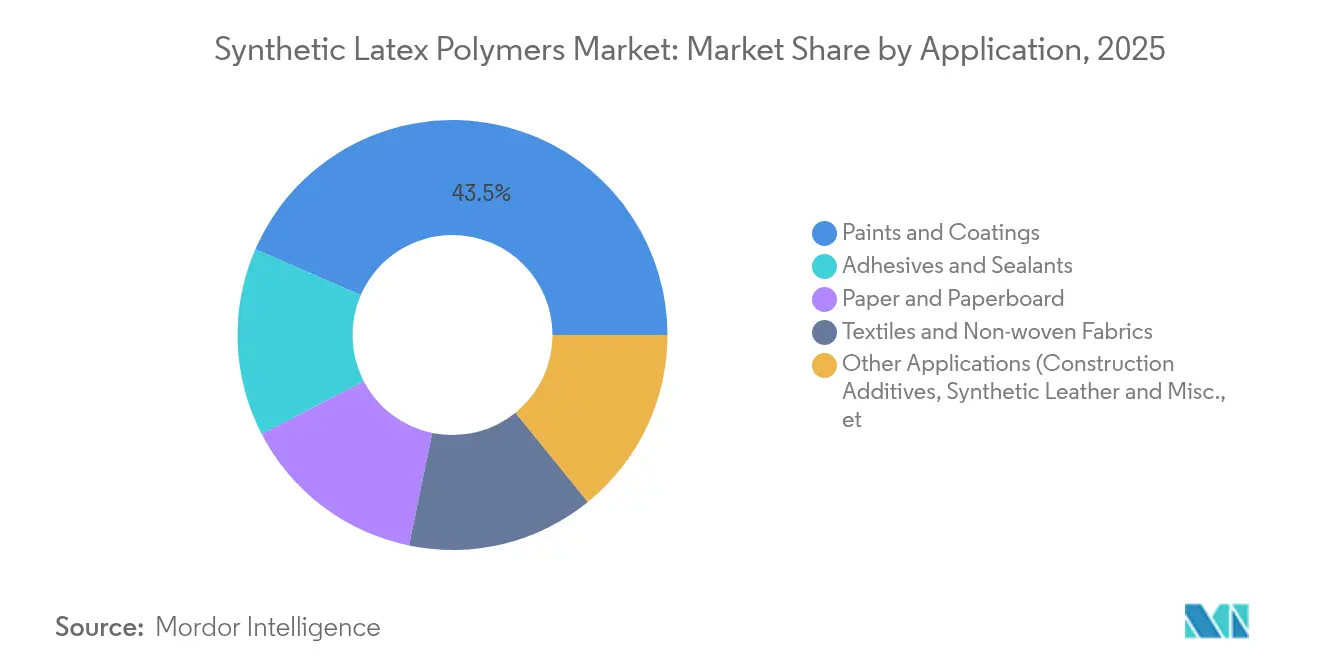

- By application, the paints and coatings application segment accounted for a significant revenue share of 43.47% in 2025. It is projected to grow at a CAGR of 3.88% through 2031, emerging as the fastest-growing segment in the industry.

- By geography, Asia-Pacific accounted for 48.10% of the synthetic latex polymers market size in 2025, whereas the Middle East and Africa region is advancing at a 4.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Synthetic Latex Polymers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from paints & coatings industry | +1.2% | Global, led by APAC & North America | Medium term (2-4 years) |

| Construction boom driving adhesives & sealants usage | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| VOC regulations favouring synthetic latex over solvent systems | +0.6% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Increasing utilization in medical and healthcare application | +0.3% | Global, led by North America & Europe | Long term (≥ 4 years) |

| 3-D printable concrete admixtures using latex for rheology | +0.1% | North America & Europe, pilot APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Paints & Coatings Industry

Architectural reformulations continue to accelerate uptake in the synthetic latex polymers market as coating makers align with VOC caps that now range from 50 g/L to 250 g/L in jurisdictions such as California’s South Coast AQMD Rule 1168[1]South Coast AQMD, “Rule 1168 Adhesive and Sealant Applications,” aqmd.gov. Global suppliers respond with next-generation acrylic dispersions, typified by BASF’s 2025 industrial portfolio, which eliminates reportable VOCs and integrates bio-based feedstock while retaining film strength and weatherability. A widening gap between solvent and water-based systems reinforces the long-term shift toward synthetic latex, particularly in interior architectural finishes where odor, drying time, and indoor-air benchmarks converge.

Construction Boom Driving Adhesives & Sealants Usage

Emerging-market infrastructure cycles sustain another pillar of growth for the synthetic latex polymers market. Saudi Arabia’s Vision 2030 blueprint, for example, doubles national petrochemical capacity to more than 140 million tons by 2030 and prioritizes specialty polymers geared to construction chemistry. Public procurement rules echo this direction: Washington State DOT 2024 specifications require latex-modified concrete overlays on critical bridge decks, guaranteeing baseline demand for styrene-butadiene dispersions.

VOC Regulations Favouring Synthetic Latex Over Solvent Systems

Rulemaking bodies worldwide continue to tighten the compliance vise on solvent emissions, further cementing the synthetic latex polymers market trajectory. The US EPA’s 2024 Hazardous Air Pollutant amendment alone removes 6,230 tons of HAPs per year at an industry cost of USD 193 million, accelerating substitution to water-based latex dispersions[2]US EPA, “Final Rule: Hazardous Organic NESHAP Revisions 2024,” epa.gov. Parallel initiatives in California’s Consumer Products Regulation and Maricopa County’s ozone plan demonstrate regulatory harmonization, while EPDLA’s position paper underscores five decades of solvent-free performance within European polymer dispersions[3]European Polymer Dispersion and Latex Association, “Position Paper on Synthetic Polymer Microparticles,” epdla.eu. Collectively, these mandates reduce formulation latitude for solvent chemistries and channel capital toward advanced latex plants.

Increasing Utilization in Medical and Healthcare Applications

Healthcare conversion gathers pace as device makers prioritize biocompatibility and traceability in glove, catheter, and film applications. Health Canada’s 2025 adoption of ISO 11193-1 for medical gloves formalizes performance rules that favor synthetic nitrile and polychloroprene latex over natural rubber for allergy risk mitigation. Research paths are widening as antimicrobial latex grades and biodegradable fillers enter the pipeline, positioning suppliers with regulatory expertise and specialty compounding capacity for incremental share capture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material (butadiene) cost volatility | -0.7% | Global, APAC & North America prominent | Short term (≤ 2 years) |

| Carpet demand decline in developed markets | -0.4% | North America & Europe | Medium term (2-4 years) |

| C4 refinery shutdowns limiting butadiene supply | -0.3% | Global supply chains, regional variations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material (Butadiene) Cost Volatility

Butadiene swings continue to squeeze latex margins. Q1 2025 spot prices reacted sharply to soft automotive tire demand and selective cracker turnarounds. The American Chemistry Council estimates styrene-butadiene latex consumes 8% of total butadiene, exposing producers to every upstream rally. Further pressure stems from LyondellBasell’s review of European olefin assets, which clouds forward supply visibility.

Carpet Demand Decline in Developed Markets

Residential carpet is losing floor share to resilient and hard-surface options. Mohawk Industries reports accelerated investment in recycled-content rigid core lines and PVC-free variants, signaling a structural reset that directly trims latex-backing volumes. Textile Exchange notes global polyester output climbed to 71 million t in 2023, but most incremental tonnage funnels into apparel and technical textiles rather than tufted carpet. North American and European latex suppliers must therefore pivot to higher-growth uses such as architectural coatings or technical non-wovens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Acrylic Leadership Anchored by Compliance Edge

Acrylics hold 35.62% of the synthetic latex polymers market share in 2025 and are expanding at a 3.42% CAGR, reinforced by excellent film-forming, weather resistance, and low-VOC compliance. Within the broader synthetic latex polymers market size, acrylic dispersions routinely serve as the default binder in premium zero-odor wall paints that meet indoor-air programs such as LEED and BREEAM. Suppliers also advance self-crosslinking technology that boosts scrub resistance without external coalescents. Styrene-butadiene grades remain competitive in paper, carpet, and cementitious admixtures because of favorable cost-performance ratios, yet the segment must navigate feedstock volatility. Vinyl acetate and polyvinyl acetate niches persist in woodworking and textile finishing where flexibility outweighs water-whitening concerns. Nitrile butadiene latex commands loyal demand in protective gloves due to chemical resistance and puncture strength. Government research grants, typified by the USD 51 million Sustainable Polymers Tech Hub in Akron, aim to commercialize bio-based butadiene, ultimately reshuffling cost structures and carbon metrics across polymer types.

Acrylic dominance looks durable, although incremental innovation will likely unfold along bio-acrylic monomers, recyclability, and circular feedstock sourcing. As regulations tighten microplastic release and carbon disclosure, the superior compliance record of acrylics positions them to preserve leadership, while producers of styrene-heavy chemistries may invest in hybrid formulations or mass-balance certification to stay relevant.

By Application: Paints & Coatings Sustain Outperformance

The paints & coatings segment commands 43.47% of the synthetic latex polymers market in 2025 and is set to climb at a 3.88% CAGR through 2031, outpacing overall market growth. That dominance arises from enduring construction activity, interior air-quality codes, and homeowner preference for quick-drying low-odor finishes. The segment also exemplifies tighter alignment between performance and sustainability: producers deploy high-solids latex, low surfactant residues, and biocide-optimized packages to curb lifecycle emissions. Adhesives & sealants usage mirrors infrastructure outlays, especially in Asia-Pacific roadways and Middle East megaprojects. Paper & paperboard coatings face substitution pressure from biolatex blends that can replace up to 75% of synthetic latex in certain gloss grades, yet the hybrid approach may still lock in a baseline binder demand. Technical textiles and non-wovens rise on back of single-use medical drapes and filtration media, both under scrutiny for recyclability. Emerging 3-D printing admixtures, though nascent, embody the next specialty frontier, capitalizing on latex capability to tune rheology for layered deposition in automated construction yards.

Geography Analysis

Asia-Pacific holds 48.10% of the synthetic latex polymers market size in 2025, reflecting its deep manufacturing base, abundant labor, and rapid urbanization. China drives a large portion of regional coating and adhesive consumption, even as plant rationalizations and ethane-based feedstock shifts redefine competitiveness in petrochemicals. India adds momentum through public housing schemes and expanding packaging demand for e-commerce. Still, the region’s growth curve is flattening as installed capacity catches up with prior surges and as ESG auditing gains traction among multinational buyers, favoring suppliers that can document low carbon intensity and circular practices.

The Middle East & Africa currently contributes a smaller volume but is the fastest mover, with a 4.05% CAGR anticipated to 2031. Gulf Cooperation Council economies bankroll mega-infrastructure under Vision 2030, underpinned by competitive feedstock and integrated refinery-to-polymer complexes. Saudi Arabia’s plan to more than double petrochemical output to 140 million t annually underscores commitment to downstream value capture, including synthetic latex raw materials Cross-border partnerships—such as the Sadara venture between Saudi Aramco and Dow—reinforce scale and market access.

North America and Europe represent mature demand centers where the synthetic latex polymers market is shaped more by regulation than volume spikes. The US Department of Energy calculates that the chemicals and refining segment requires USD 90-120 billion in decarbonization investment by 2030, prodding latex producers to green electricity, heat integration, and mass-balance certified feedstocks. Europe follows a similar path, embedding polymer taxation, extended producer responsibility, and zero-pollution roadmaps into industrial policy. Suppliers with legacy solvent footprints face the most significant transformation costs, while integrated players redirect R&D to bio-acrylics, mechanical recycling, and emission-free drying ovens.

Competitive Landscape

The synthetic latex polymers market exhibits moderate consolidation among the top 5 players. Prominent companies such as BASF, Dow, Arkema, and LyondellBasell are strategically aligning their operations by leveraging integrated production capabilities and making targeted investments. These actions are driven by the need to adapt to evolving regulations and shifting customer preferences. The nature of competition has transitioned, with a greater emphasis on technological advancements rather than cost leadership. Consequently, compliance with regulatory standards has become a fundamental prerequisite for market entry rather than a competitive differentiator. Simultaneously, regional participants like Kumho Petrochemical, LANXESS, and ZEON Corporation are establishing specialized niches by utilizing their technical expertise and fostering strong customer relationships within specific application areas or regions.

Synthetic Latex Polymers Industry Leaders

Dow

Matco Chemicals Group

Arkema

BASF

Kumho Petrochemical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zeon Corporation announced its plans to expand high-grade solution-polymerised styrene-butadiene rubber (S-SBR) production, crucial for fuel-efficient tyres, at its Singapore plant, Zeon Chemicals Singapore Pte Ltd (ZCS). The facility, now installed, will begin test production before full operations in 2026, raising combined annual capacity to 125,000 tonnes.

- March 2024: Arlanxeo announced plans to build a hydrogenated nitrile butadiene rubber (HNBR) plant in Changzhou, China. The facility will have a nameplate annual capacity of 5,000 tons, with the first phase enabling 2,500 tons of production annually. Operations are expected to begin in Q3 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the synthetic latex polymers market as the global sales value of water-borne polymer emulsions produced from petro-chemical monomers such as styrene, butadiene, acrylics, vinyl acetate, and related copolymers that act as binders in paints, adhesives, paper coatings, textiles, and construction additives. According to Mordor Intelligence, only virgin, factory-formulated latex shipped in bulk, drums, or tote packaging is counted at manufacturer selling price.

Scope Exclusion: We exclude natural rubber latex, silicone dispersions, and downstream compounded products like ready-mixed paint or adhesive pastes.

Segmentation Overview

- By Polymer Type

- Styrene-Butadiene

- Acrylic

- Vinyl Acetate

- Polyvinyl Acetate

- Others (Nitrile Butadiene, etc.)

- By Application

- Paints and Coatings

- Adhesives and Sealants

- Paper and Paperboard

- Textiles and Non-woven Fabrics

- Other Applications (Construction Additives, Synthetic Leather and Misc., etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Desk Research

We began with publicly available trade statistics, most notably UN Comtrade shipment values, USITC and Eurostat production tallies, and import duty filings that reveal cross-border flows of styrene-acrylic and SBR latexes. Sector insights from associations such as the European Council of the Paint, Printing Ink and Artist's Colours Industry and TAPPI provided demand indicators in coatings and paper. Company 10-Ks, investor decks, and environmental filings clarified capacity changes, while patent abstracts on Questel highlighted pipeline chemistries shaping future volumes.

Mordor analysts then drew on paid screens in D&B Hoovers and Dow Jones Factiva to benchmark revenue splits of key producers and to capture announcement-led demand spikes in construction and packaging. The sources listed here are illustrative; many additional references fed our evidence map, validation steps, and scope checks.

Primary Research

We spoke with procurement leads at coating formulators, regional distributors, and plant engineers across Asia-Pacific, North America, and Europe to verify price brackets, typical solid content, and substitution trends toward vinyl acetate ethylene grades. These interviews also helped us refine utilization rates and reconcile regional stock builds visible in customs data.

Market-Sizing & Forecasting

A top-down model converts polymer production and trade balances into net apparent consumption, which is then aligned with application-level spending pools. Selected bottom-up cross-checks, supplier roll-ups, and sampled average selling price times regional shipment volume anchor totals and flag variance. Key drivers in our equation include housing starts, architectural paint output, corrugated board tonnage, automotive build rates, raw-material spreads, and evolving VOC caps. Forecasts rely on multivariate regression mixed with scenario analysis for feedstock volatility; gaps in bottom-up detail are bridged using weighted regional penetration factors vetted during primary research.

Data Validation & Update Cycle

Mordor analysts pass each model through anomaly screens, benchmark outputs against independent polymer indices, and re-run variance checks before sign-off. Reports refresh every twelve months, with interim tweaks when material events, such as a major plant outage, shift supply or price baselines.

Why Mordor's Synthetic Latex Polymers Baseline Earns Trust

Published numbers often differ because firms select dissimilar polymer families, apply varying average prices, or freeze exchange rates at different points in the year. We declare our scope upfront and apply a disciplined refresh cadence, which curbs currency drift and ensures late-year capacity additions enter the base.

Key gap drivers versus other publishers include narrower grade baskets, reliance on shipment listings without domestic production reconciliation, and aggressive price escalation curves that inflate headline value.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 38.71 B (2025) | Mordor Intelligence | - |

| USD 40.6 B (2024) | Global Consultancy A | Uses constant 2023 FX rates and omits captive vinyl acetate volumes |

| USD 72.1 B (2025) | Industry Journal B | Blends synthetic latex with natural rubber and applies plant-gate volume x retail paint ASP |

These comparisons show that our balanced scope selection and dual-path validation deliver a dependable, decision-ready baseline, while more expansive or loosely priced approaches swing totals markedly higher or lower. Mordor's method therefore provides the transparent middle ground executives can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current Synthetic Latex Polymers Market size?

The market stands at USD 39.89 billion in 2026 and is forecast to climb to USD 46.34 billion by 2031 at a 3.04% CAGR.

Which application segment leads demand?

Paints & coatings dominate with 43.47% revenue share in 2025, driven by low-VOC architectural coatings and steady construction activity.

Which region grows the fastest over the forecast period?

The Middle East & Africa region advances at a 4.05% CAGR through 2031 on the back of Vision 2030 infrastructure and petrochemical capacity expansion.

How does regulation influence market growth?

Tightening VOC and hazardous pollutant standards worldwide accelerate the shift to water-based latex systems, adding roughly 0.6 percentage points to forecast CAGR.

Page last updated on: