Global Surgical Drills Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

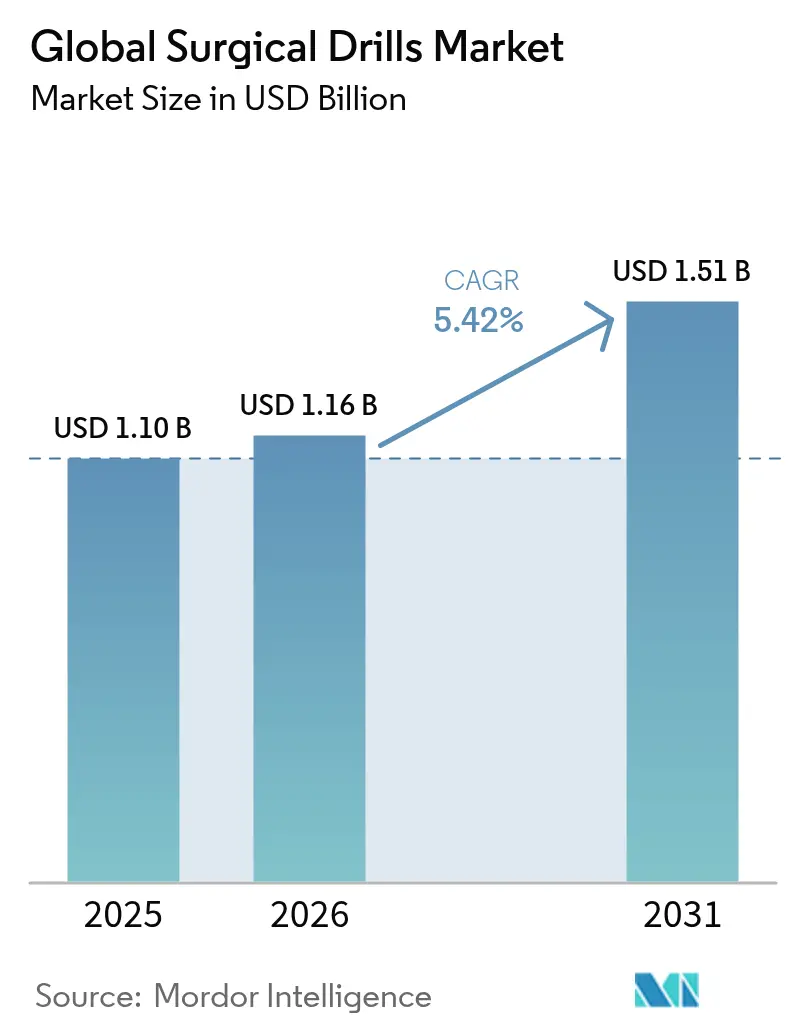

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

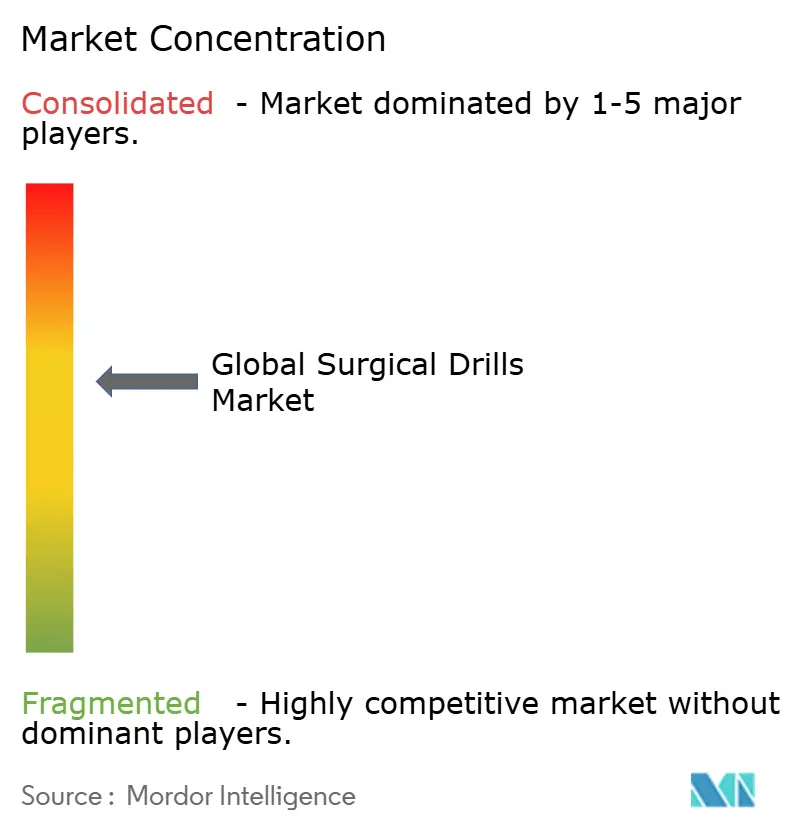

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Surgical Drills Market Analysis by Mordor Intelligence

The surgical drills market size is expected to grow from USD 1.10 billion in 2025 to USD 1.16 billion in 2026 and is forecast to reach USD 1.51 billion by 2031 at 5.42% CAGR over 2026-2031. Demand is powered by climbing surgical volumes, rapid improvements in battery chemistry, and the migration of procedures toward minimally invasive techniques that call for ever-tighter drilling tolerances. Hospitals are shifting capital budgets from pneumatic lines to cordless systems because smart batteries cut turnover time, while software-guided drill profiles give surgeons repeatable accuracy regardless of bone density. Rare-earth–efficient motors, lighter composite housings, and autoclavable lithium packs have pushed performance parity with corded gear, setting the stage for cordless dominance. Aging demographics and the steady rise of robotic and navigation platforms further tighten the link between drill performance and overall surgical workflow efficiency, elevating engineering quality over simple unit sales growth.

Key Report Takeaways

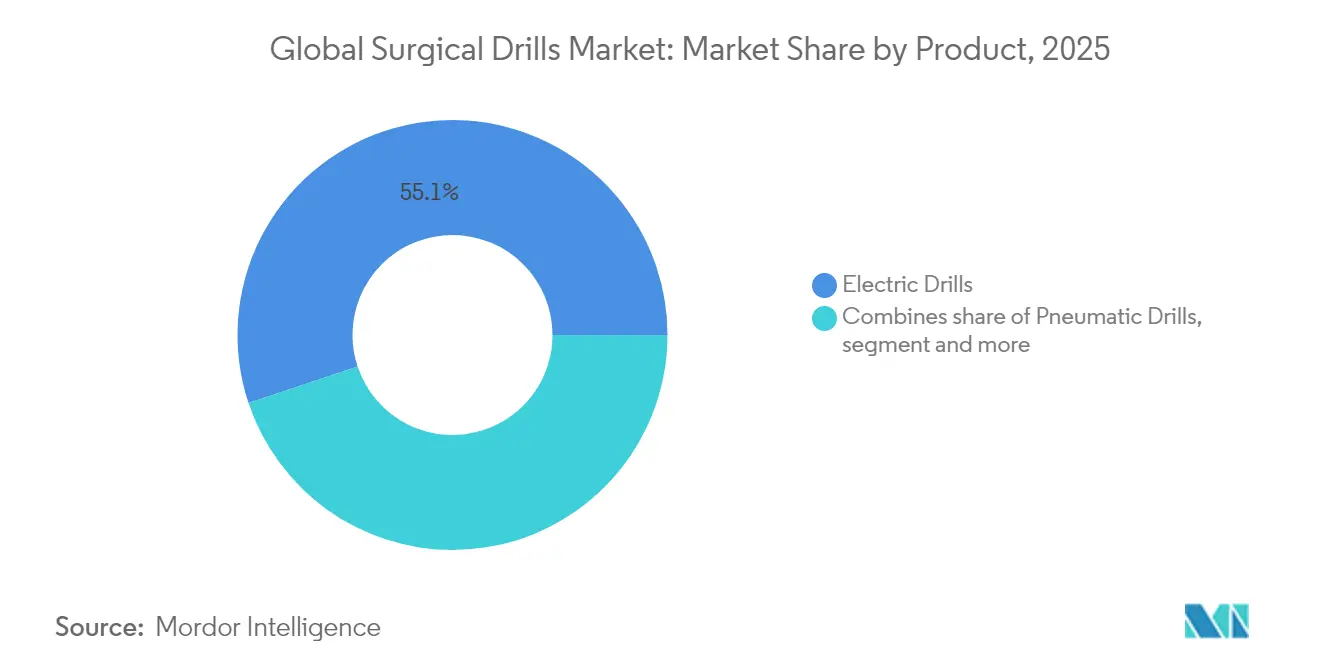

- By product, electric drills led with 55.12% revenue share in 2025; battery-powered drills are projected to expand at a 6.12% CAGR to 2031.

- By speed, high-speed (above 60,000 rpm) commanded 60.85% of the surgical drills market size in 2025, also high-speed (above 60,000 rpm) is forecast to post the fastest 5.98% CAGR to 2031.

- By application, orthopedic surgery accounted for 66.05% of the surgical drills market share in 2025, while dental surgery is advancing at a 6.48% CAGR through 2031.

- By end-user, hospitals and clinics commanded 69.05% of the surgical drills market size in 2025, whereas ambulatory surgery centers are growing quickest at 6.84% CAGR.

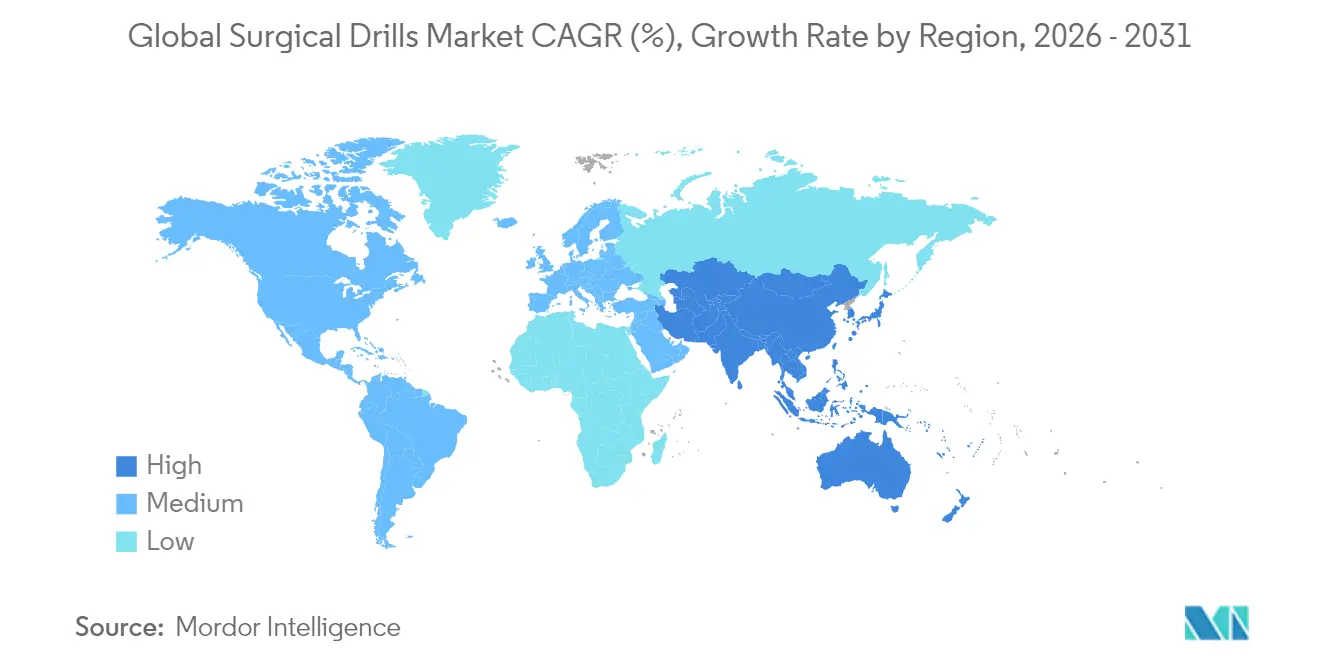

- By geography, North America held 40.20% of the surgical drills market share in 2025; Asia-Pacific is forecast to post the fastest 7.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Drills Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising orthopedic & trauma surgery volume | +1.2% | Global, strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Ergonomics & power-train innovation | +0.8% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Uptick in minimally invasive & robotic cases | +1.0% | North America & Europe core, expanding into Asia-Pacific | Medium term (2-4 years) |

| Growing geriatric musculoskeletal burden | +0.9% | Global, accelerated in developed economies | Long term (≥ 4 years) |

| Shift to single-use drills | +0.6% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| 3-D-printed custom drill guides | +0.4% | North America & Europe, selective uptake in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Orthopedic & Trauma Surgery Volume

Primary total knee arthroplasties in the United States alone are forecast to jump 673% by 2030, while hip replacements rise 174%, creating an unprecedented load for precision drilling systems. Similar trajectories play out in fast-urbanizing Asian economies where traffic-related trauma lifts fracture repairs. As cases migrate from inpatient theaters to outpatient suites, battery-powered platforms that bypass built-in compressor lines win favor, especially in ambulatory orthopedic centers posting double-digit growth. High procedure complexity in elderly bone drives torque-controlled drills that avoid micro-cracks, raising demand for programmable speed profiles. These factors combine to keep the surgical drills market on a sturdy upward arc.

Rapid Ergonomics & Power-Train Innovation

New generations of cordless drills match, and in some tasks exceed, pneumatic torque while eliminating hose drag that can contaminate sterile fields. CONMED’s Hall Lithium Battery system recharges in 30 minutes and withstands repeated autoclave cycles, solving the durability gap that once hampered lithium packs.[1]CONMED Corporation, “Hall Lithium Battery System,” conmed.com Stryker’s Signature 2 delivers 75,000 RPM from a slim handle that reduces surgeon fatigue, and its software lets teams preload speed-torque curves for specific bone types. Hospitals measure such gains in minutes saved per case, turning capital-equipment debates into workflow decisions rather than pure price comparisons. As AI overlays guide depth and angle, drills become data nodes in the wider digital OR ecosystem.

Surge in Minimally Invasive & Robot-Assisted Procedures

Robotic systems performed 17% more procedures in 2024, and robotic TKAs already make up 13% of all U.S. knee replacements. In Europe and Asia, AI-aided platforms such as Johnson & Johnson’s VELYS add real-time kinematic feedback that depends on drills capable of micron-level reproducibility. Force-sensing handpieces inside Intuitive’s da Vinci 5 reduce tissue force by 43%, proving the clinical value of embedded sensors. As robots spread from flag-ship centers to regional hospitals, sales of drills that integrate seamlessly with robotic arms will outpace those of stand-alone devices, expanding the surgical drills market.

Growing Geriatric Musculoskeletal Burden

In Germany, total hip arthroplasties could rise 29% from 2016 to 2040, with the steepest climb among patients aged 80-89 years. High-porosity bone in this cohort heightens the need for drills that modulate speed in real time to curb heat buildup. Health systems also push for shorter anesthesia windows, rewarding automated drilling modules that shave minutes from bone prep. Collectively, demographic pressure cements a steady baseline for the surgical drills market even when discretionary procedures plateau.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-surgery complications linked to drilling | -0.7% | Global, higher in emerging markets | Short term (≤ 2 years) |

| High acquisition & lifecycle cost | -0.5% | Global, pronounced in cost-sensitive markets | Medium term (2-4 years) |

| Sterilization waste & sustainability pressure | -0.3% | Europe & North America leading, expanding globally | Long term (≥ 4 years) |

| Rare-earth magnet supply bottlenecks | -0.4% | Global, highest impact on premium products | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Surgery Complications Linked to Drilling

Bone temperatures above 47 °C impair osteogenesis; conventional drills can exceed 100 °C in dense cortical bone, expanding osteonecrosis zones.[2]Paweł Chodzko-Zajko, “Thermal Risks in Bone Drilling,” MDPI Applied Sciences, mdpi.comStudies show even sequential reaming fails to eliminate heat trauma entirely, fueling legal and cost concerns for hospitals. Ultrasonic-assisted drilling lowers force and heat but costs more and requires surgeon retraining, slowing uptake. Until embedded cooling or smarter torque governors become mainstream, risk-averse buyers in emerging markets may postpone upgrades, restraining part of the surgical drills market.

High Acquisition & Lifecycle Cost of Power Systems

A top-tier cordless console, four handpieces, and two battery sets can exceed USD 50,000 over seven years once maintenance and cell replacements are tallied. Although pneumatics carry compressor upkeep, the upfront sticker shock of lithium systems challenges procurement teams in cost-controlled regions. Value-based payment models now dominate U.S. orthopedics, compelling administrators to prove tangible efficiency gains before approving new drills. Vendors counter with leasing, multi-year service bundles, and modular upgrades, but budget scrutiny still slows purchase cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Corded Reliability Meets Cordless Momentum

Electric drills currently generate 55.12% of revenue, reflecting decades of OR familiarity and steady performance. Yet cordless units are climbing at 6.12% CAGR as battery swaps under 30 seconds and autoclave-safe packs free teams from fixed power outlets. Pneumatic drills retain a niche in high-volume trauma centers that already own central air, but their share erodes as compressors age out. Accessory kits—sterile bits, backup batteries, docking carts—form a steady annuity stream, so vendors align channel programs to lock hospitals into platform ecosystems. The surgical drills market size for cordless platforms is forecast to eclipse corded revenue by the late 2020s, driven by procedure mobility in hybrid ORs.

Custom-tuned power management chips now stretch runtime past eight complex orthopedic cases per charge, erasing prior downtime criticism. Arthrex’s 2025 cordless launch paired a carbon-fiber shell with AI-based cell-health analytics, signaling a trend toward predictive maintenance that minimizes unplanned stoppages. Suppliers that retrofit compatibility sleeves for legacy shafts lower switching friction, accelerating fleet conversion within budget-sensitive systems.

By Speed: Precision Favors the Fast Lane

High-speed drills topping 60,000 RPM hold 60.85% share and still grow at 5.98% CAGR, underscoring surgeon preference for crisp cutting in minimally invasive corridors. These handpieces integrate micro-vent channels and ceramic bearings to dissipate friction heat and preserve bone viability. The surgical drills market size for high-speed models is projected to reach USD 954.6 million by 2031 as ENT and spine teams demand burrs that navigate tight anatomy without chatter. Standard-speed drills remain important in trauma units and revision arthroplasty where dense callus calls for controlled advancement.

Recent design shifts favor adaptive-speed controllers that drop rpm automatically when sensors detect thin cortical layers, protecting underlying tissue. Stryker’s servo loop caps overshoot within 50 microseconds, and firmware updates ship over secure Wi-Fi, linking handpieces to central device-management dashboards.

By Application: Orthopedic Dominance, Dental Acceleration

Orthopedics accounts for 66.05% of revenue thanks to joint replacements and fracture fixations, but dental indications clock the fastest 6.48% CAGR as implant volumes surge. Oral surgeons demand drills that limit thermal necrosis in narrow sockets; single-drill protocols validated in 2024 dropped peak bone temperature by 10 °C versus sequential reaming. The surgical drills market size in dentistry is forecast to double this decade, aided by chair-side 3-D workflows that rely on low-noise, high-speed bits.

Neurosurgery and ENT call for ultra-small collets and depth-stop algorithms; Northwestern Medicine’s adoption of an auto-stop brain drill in March 2025 cut ventriculostomy times and reduced drift risk. Such specialty wins highlight opportunities for niche manufacturers even as broad orthopedic spend dominates.

By End User: Hospital Bulk Buys vs ASC Agility

Hospitals and clinics still absorb 69.05% of sales, bundling drills into multi-year power-tool agreements that align with robotic acquisitions. Yet ambulatory surgery centers (ASCs) post a 6.84% CAGR, pulling procedures like total knees into outpatient suites.

The surgical drills market size captured by ASCs could top USD 427.4 million by 2031 if current migration persists. These centers value cordless sets that roll between theaters, quick-charge in 15 minutes, and require minimal biomedical tech oversight. Conversely, hospitals exploit purchasing clout to demand fleet-wide software licenses and predictive-service analytics, putting pricing pressure on vendors.

Geography Analysis

North America holds 40.20% of 2025 revenue, powered by early adoption of integrated digital ORs, solid reimbursement, and the world’s highest orthopedic caseload per capita. Leading U.S. centers embed cordless drills into robotic workstations, tightening vendor partnerships around ecosystem compatibility. Canada’s single-payer provinces purchase through group tenders that favor platform breadth over niche innovation, while Mexico’s private hospitals import premium U.S. gear to capture medical-tourism flows. Despite maturity, the region’s keen appetite for AI-enabled upgrades keeps the surgical drills market vibrant, though annual growth moderates below emerging-market pace.

Europe offers a stable but sustainability-sensitive landscape. Germany, France, and the United Kingdom remain the anchor buyers, yet environmental directives and post-Brexit regulatory divergence add compliance layers. Hospitals in Italy and Spain increasingly stipulate low-waste packaging and end-of-life recycling plans in tenders. Eastern European states, buoyed by EU structural funds, retrofit theaters with cordless drills to leapfrog aging pneumatic lines. With CE-plus-UKCA dual marking now standard, vendors streamline filings to avoid product-launch lags, keeping continental share competitive.

Asia-Pacific is set to grow at 7.15% CAGR, the fastest worldwide. China funnels public funding into trauma centers and invests in in-house robotic ecosystems, often pairing domestic drill makers with locally built arms to reduce import spend. Japan’s super-aged population continues to swell arthroplasty lists, compelling hospitals to adopt torque-controlled drills that minimize cortical burn in osteoporotic bone. India’s tier-I private chains equip new ASCs with battery suites, while government facilities still favor budget electric sets, carving a two-tier segment. Australia and South Korea, at technology frontiers, serve as regional reference sites for 75,000 RPM handpieces with cloud-based service logs. Collectively, this mix pushes the surgical drills market toward diversified, region-specific product roadmaps.

Competitive Landscape

The market tilts moderately consolidated, with the top players controlling significant revenue slice. They wield scale advantages in regulatory staffing, clinical-training hubs, and accessory ecosystems, deterring smaller entrants. Stryker deepened its moat via the 2024 launch of Spine Guidance 5 software, embedding drill telemetry into navigation consoles. Johnson & Johnson bundles its VELYS robotic knees with battery drills and multi-year analytics subscriptions, creating high switching costs for hospitals.

Specialist challengers attack niches. Hubly Surgical won early U.S. traction by proving its auto-stop cranial drill cuts complication-linked re-interventions, earning Northwestern Medicine’s fleet-wide adoption in March 2025. Paragon 28 tailors right-angle drills for ankle arthroplasty, a segment underserved by multi-specialty giants. Chinese vendors, buoyed by local capital and government procurement quotas, push competitively priced high-speed sets across Southeast Asia, nudging larger firms on price but lagging on global regulatory breadth.

Technology convergence is the new battleground. Vendors race to integrate AI-based force feedback, cloud-logged usage analytics, and self-diagnosing battery packs. Firms without in-house digital depth partner with software specialists to close gaps, as exemplified by Zimmer Biomet’s 2025 agreement with a U.S. surgical-navigation start-up. Simultaneously, rare-earth supply concerns spur collaborative R&D on alternative magnet pathways. The competitive tempo keeps the surgical drills market dynamic even as baseline growth steadies.

Global Surgical Drills Industry Leaders

Stryker Corporation

Zimmer Biomet Holdings Inc.

Medtronic plc

Portescap US Inc.

GMI Ilerimplant

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arthrex launched a battery-powered system designed for orthopedic applications, expanding the company’s cordless surgical instrument portfolio to address surgeon mobility requirements and infrastructure independence in modern operating environments.

- March 2025: Northwestern Medicine became the first healthcare system to utilize Hubly Surgical’s battery-powered brain drill featuring automatic stop mechanisms and single-handed operation, reducing ventriculostomy procedure times while improving safety in over 60,000 annual U.S. procedures.

- September 2024: Paragon 28 launched the Right-Angle Drill specifically designed for ankle replacement procedures, demonstrating continued innovation in specialized orthopedic drilling applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the surgical drills market as all powered, reusable or single-use drill handpieces and their core power modules that bore or mill human bone during orthopedic, dental, ENT, neuro, and trauma procedures. Disposable burs, navigation systems, and related saws are covered only when they ship bundled with a drill console for direct drilling use.

Scope Exclusions: Purely manual hand drills and general-purpose craft rotary tools sold outside the operating suite are not considered.

Segmentation Overview

- By Product

- Pneumatic Drills

- Electric Drills

- Battery-Powered Drills

- Accessories

- By Speed

- High-Speed (above 60,000 rpm)

- Standard Speed (below 60,000 rpm)

- By Application

- Orthopedic Surgeries

- Dental Surgeries

- ENT Surgeries

- Neurosurgery

- Other Applications

- By End User

- Hospitals and Clinics

- Ambulatory Surgery Centers

- Specialty Dental and ENT Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Qualitative interviews and structured surveys with orthopedic surgeons, neurosurgeons, sterile-processing managers, and biomedical engineers across North America, Europe, Asia-Pacific, and Latin America validated utilization rates, average selling prices, and emerging single-use adoption that secondary literature only hinted at. Follow-ups with procurement leads clarified warranty cycles and fleet renewal triggers.

Desk Research

We screened open data from tier-1 authorities such as the World Health Organization's Global Surgery indicators, the OECD Health Statistics, the United States FDA 510(k) database, Eurostat procedure counts, and orthopedic associations in Asia-Pacific. Company 10-K filings, hospital capex presentations, and peer-reviewed journals on powered instrumentation complemented these inputs. Subscription resources that Mordor analysts access, including D&B Hoovers for company revenues and Questel for patent activity, helped map supplier splits and technology flow. This list illustrates, not exhausts, the secondary sources consulted throughout data collection and verification.

Market-Sizing & Forecasting

We built a top-down model that begins with annual orthopedic, dental, ENT, and neuro procedure volumes per country; these are multiplied by drill penetration ratios and kit-per-procedure norms, then converted to value using region-specific ASPs. Supplier roll-ups from sampled public revenues and distributor channel checks serve as a bottom-up reasonableness screen, after which totals are reconciled. Key drivers, including elective surgery backlog clearance, aging population growth, hospital capital budgets, single-use drill uptake, and battery-density improvements, feed a multivariate regression that projects the market to 2030. Where bottom-up gaps surfaced, regional averages from comparable device segments bridged the shortfall.

Data Validation & Update Cycle

Outputs face automated variance flags, peer review, and senior analyst sign-off. We refresh every twelve months, and interim updates are triggered when regulatory approvals, supply shocks, or large M&A events alter baseline assumptions.

Why Mordor's Surgical Drills Baseline Stands Up to Scrutiny

Published figures often diverge because firms differ on scope, base year, and refresh speed. By anchoring estimates to verified procedure counts and tested ASP bands, Mordor Intelligence minimizes that spread.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.10 B (2025) | Mordor Intelligence | - |

| USD 1.33 B (2024) | Global Consultancy A | Bundles saw systems and accessories; shipment value used as proxy without ASP checks |

| USD 1.29 B (2023) | Industry Journal B | Includes disposable burs and applies pre-COVID growth curve; last refresh 2023 |

The comparison shows that when definitions stretch beyond true drill revenue or rest on outdated procedure data, estimates inflate. By keeping scope tight, validating with clinicians, and updating annually, we deliver a balanced, decision-ready baseline clients can rely on.

Key Questions Answered in the Report

What is the current value of the surgical drills market?

The surgical drills market is valued at USD 1.16 billion in 2026 and is forecast to reach USD 1.51 billion by 2031.

Which product segment is growing fastest?

Battery-powered drills form the quickest-expanding segment, registering a 6.12% CAGR as cordless mobility gains traction in modern operating rooms.

Why are ambulatory surgery centers important to market growth?

ASCs perform more outpatient joint and spine surgeries each year; their need for portable, infrastructure-free equipment pushes demand for battery drills, helping the segment grow at 6.84% CAGR.

What geographic region will post the highest growth through 2031?

Asia-Pacific leads with a 7.15% CAGR thanks to large procedure volumes, hospital construction, and rising adoption of advanced orthopedic technologies.

How are sustainability concerns affecting drill purchases?

European and North American tenders increasingly weigh single-use waste and battery recyclability, prompting vendors to design eco-friendly casings and recycling programs.

Page last updated on: