Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

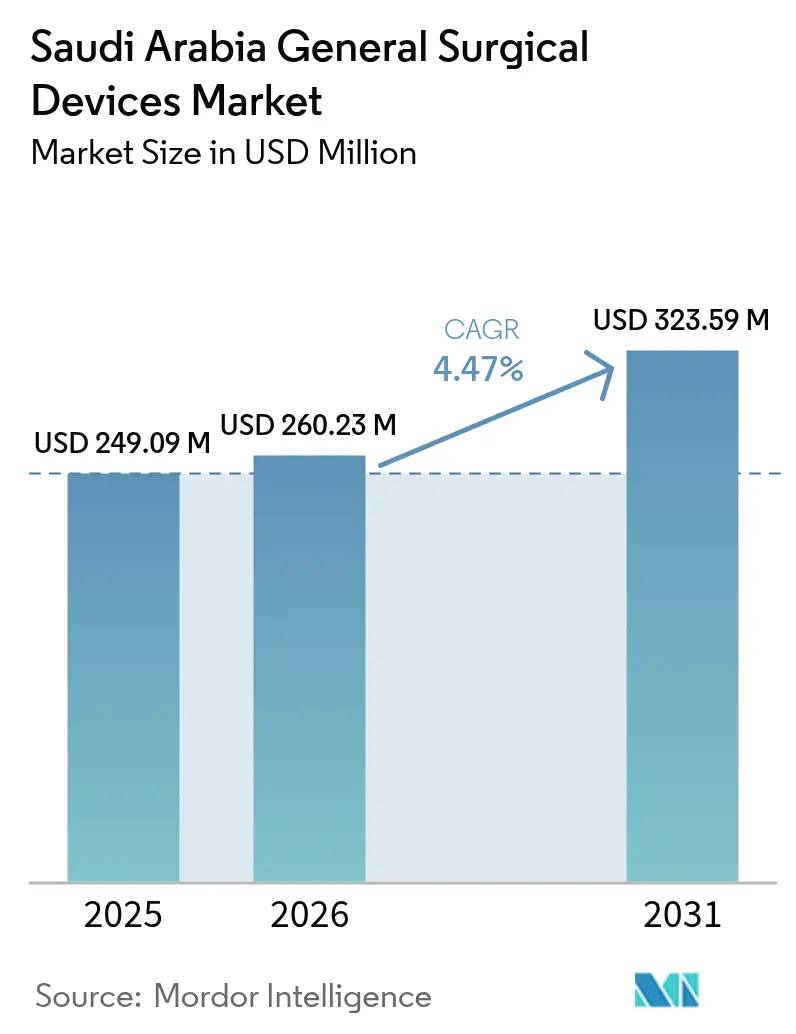

| Base Year Market Size (2025) | USD 249.09 Million |

| Market Size (2026) | USD 260.23 Million |

| Market Size (2031) | USD 323.59 Million |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

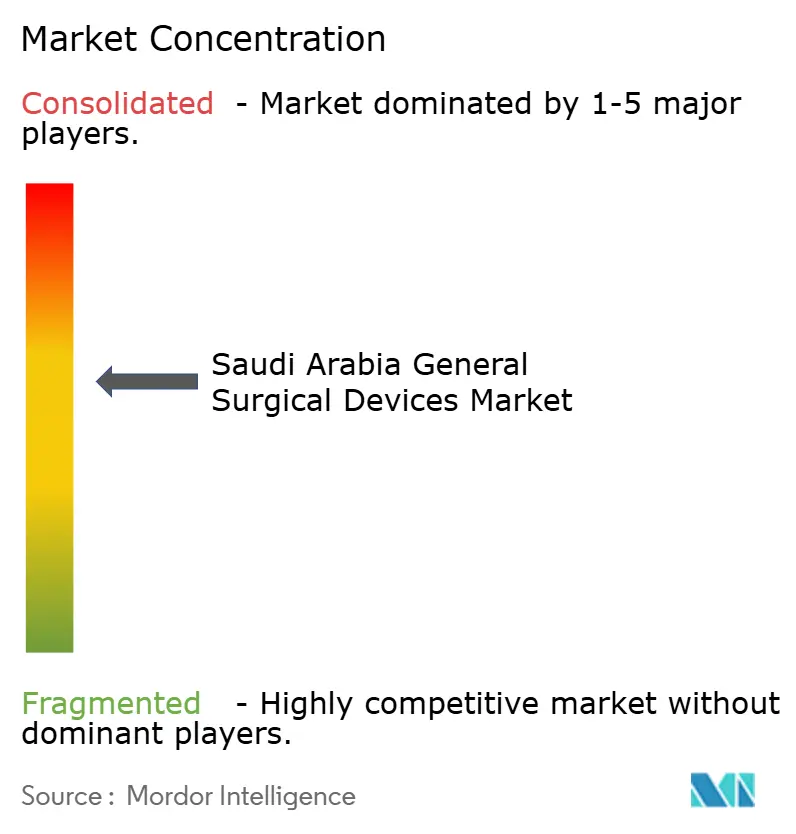

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia General Surgical Devices Market Analysis by Mordor Intelligence

The Saudi Arabia general surgical devices market size in 2026 is estimated at USD 260.23 million, growing from 2025 value of USD 249.09 million with 2031 projections showing USD 323.59 million, growing at 4.47% CAGR over 2026-2031. Steady capital deployment under Vision 2030, rising procedure volumes, and fast-growing adoption of minimally invasive and robotic technologies underpin this trajectory. More than USD 65 billion has been earmarked for healthcare infrastructure, and 65% of care delivery is set to transition to private operators, encouraging broad product uptake across public and private systems. Elective and emergency surgeries together gained scale in 2024 as surgery accounted for 24.7% of all medical referrals, keeping baseline demand resilient[1]Saudi Ministry of Health, “Statistical Yearbook 2024,” moh.gov.sa. Growing trauma caseloads, obesity-linked bariatric interventions, and sustained digital health investment are positioning suppliers for steady revenue growth even as import dependence continues to expose buyers to foreign-exchange swings.

Key Report Takeaways

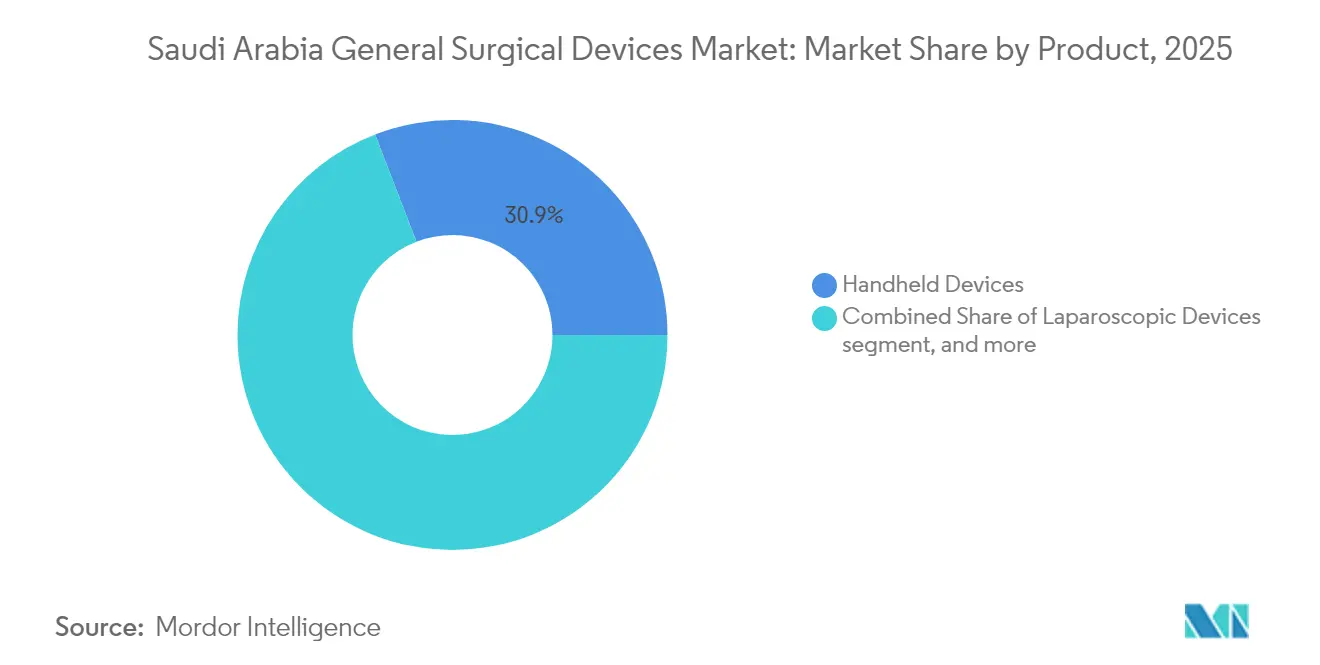

- By product category, handheld devices led with 30.86% of Saudi Arabia's general surgical devices market share in 2025. robotics & 3D-printed patient-specific Instruments posted the highest projected CAGR at 6.18% through 2031.

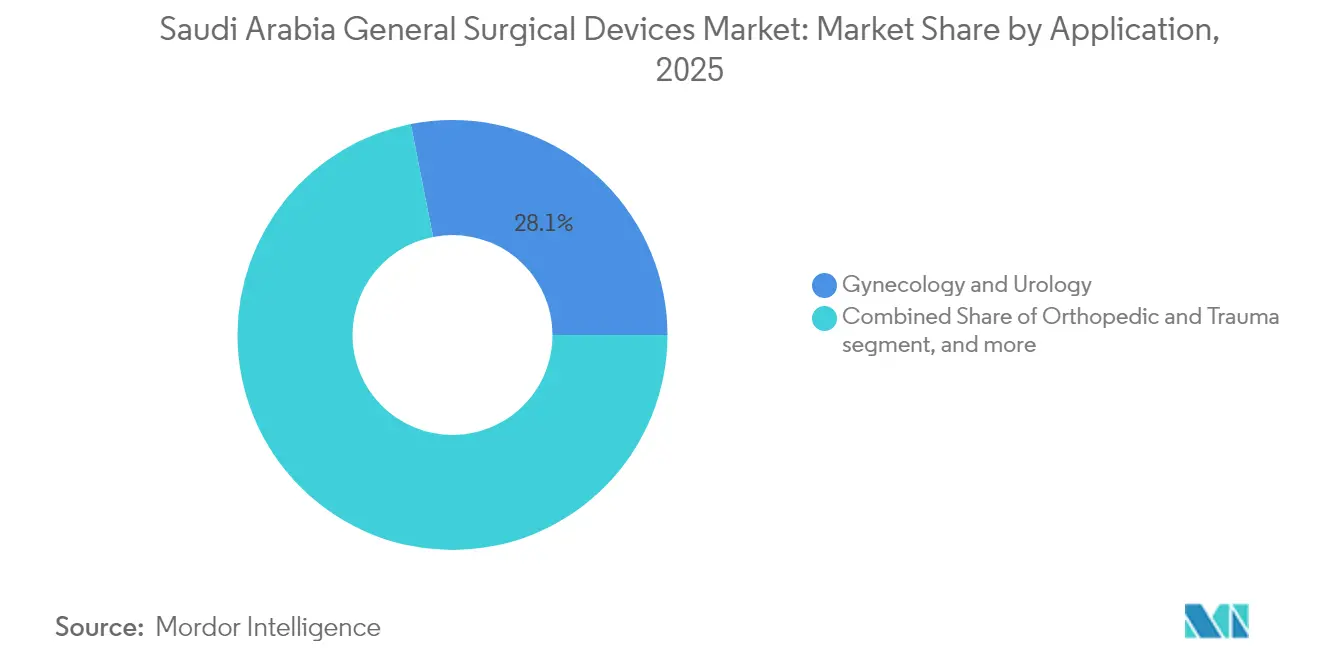

- By application, gynecology & urology held a 28.11% slice of Saudi Arabia general surgical devices market size in 2025. bariatric & general abdominal procedures are forecast to expand at a 6.55% CAGR to 2031.

- By end user, public hospitals & medical cities commanded 33.02% of Saudi Arabia general surgical devices market share in 2025 while ambulatory surgical centers record the highest projected CAGR at 6.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing trauma and road-traffic surgery volumes | +1.3% | Global, strongest in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Rising demand for minimally-invasive and laparoscopic procedures | +1.1% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Government Vision 2030 spending on surgical infrastructure | +0.9% | Gulf Cooperation Council economies | Short term (≤ 2 years) |

| Surge in 3D-printed, patient-specific surgical guides | +0.7% | North America, Europe, Japan | Long term (≥ 4 years) |

| Hospital point-of-care sterilization driving single-use devices | +0.5% | Urban tertiary centers worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Trauma & Road-Traffic Surgery Volumes

Saudi Arabia general surgical devices market demand continues to escalate as trauma centers confront persistent growth in accidents requiring complex interventions. Major facilities in Riyadh and Jeddah logged 15% to 20% annual increases in trauma surgeries in 2024, driven by vehicle density and expanding road networks. Eastern Province industrial incidents add further volume, and the state investment in helicopter emergency services drives uptake of portable, rapid-deploy instruments. Consistent spending on level 1 trauma centers keeps Handheld and Electrosurgical Devices in routine rotation, ensuring steady replacement cycles within the Saudi Arabia general surgical devices market.

Rising Demand for Minimally Invasive & Laparoscopic Procedures

A strong patient preference for shorter recovery, combined with hospital cost-containment goals, is pivoting device procurement toward laparoscopic and robotic systems. King Faisal Specialist Hospital completed 1,195 robotic procedures in 2023 with a 98% cardiac survival rate, reinforcing clinical confidence and fueling incremental capital requests[2]King Faisal Specialist Hospital & Research Centre, “Robotic Surgery Outcomes 2023,” kfshrc.edu.sa. Only 27.2% of surveyed patients are aware of robotic options and over half voice safety doubts, highlighting education opportunities for suppliers. Expanded laparoscopic training across 170 specialties continues to create a skilled workforce ready to operate advanced platforms, accelerating adoption within the Saudi Arabia general surgical devices market.

Government Vision 2030 Spend on Surgical Infrastructure

Vision 2030 revolves around public-private partnership funding that modernizes surgical suites and integrates hybrid operating rooms. The National Unified Procurement Company (NUPCO) secured SAR 2.5 billion to streamline equipment acquisition, and hospital expansions exceeding SAR 12 billion prioritize image-guided ORs. Private-sector delivery is targeted to hit 65% by 2030, assuring continuous device replacement cycles. These investments safeguard long-term growth prospects for the Saudi Arabia general surgical devices market, especially for integrated systems that enhance efficiency and clinical accuracy.

Surge in 3D-Printed, Patient-Specific Surgical Guides

Hospitals such as King Abdulaziz University Hospital now run in-house 3D printing labs that prepare personalized guides, cutting operating time by up to 30% while improving fit in orthopedic and cranial cases. The Saudi Food and Drug Authority issued targeted guidance in October 2024 that clarifies quality and traceability parameters, encouraging investments in on-site additive manufacturing. Partnerships with KAUST to embed AI in surgical planning further amplify interest, helping 3D-Printed Instruments achieve the swiftest CAGR within the Saudi Arabia general surgical devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SFDA reimbursement delays for novel surgical devices | -0.8% | Saudi Arabia and wider GCC | Short term (≤ 2 years) |

| High import dependence and FX-linked cost volatility | -0.7% | Emerging markets in Africa and South Asia | Medium term (2-4 years) |

| Shortage of laparo-robotic surgeons inflating OR idle time | -0.6% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Capital-intensive robotics and hybrid-OR gear | -0.5% | Global, strongest in mid-scale hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SFDA Reimbursement Delays for Novel Surgical Devices

Approval cycles of 12 to 18 months for breakthrough tools challenge liquidity for private hospitals and ambulatory centers that must purchase before reimbursement is confirmed[3]Saudi Food and Drug Authority, “Medical Device Registration Pathway,” sfda.gov.sa. The centralized NUPCO catalog can further slow adoption when items fall outside standard lists. As a result, companies developing AI-guided navigation systems or new energy sealing devices face delayed revenue realization in the Saudi Arabia general surgical devices market while evidence dossiers undergo local review.

High Import Dependence & FX-Linked Cost Volatility

Imports of USD 1.62 billion dwarf local output of USD 24 million, leaving buyers exposed to currency swings and potential geopolitical disruptions. Early localization programs, including ENAYAH consumable manufacturing, remain limited to basic disposables. While the SFDA outlines four production pathways, technology-transfer hurdles and high capital needs have limited domestic production of complex devices. Fluctuating exchange rates therefore weigh on procurement budgets and margin planning in the Saudi Arabia general surgical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Robust Core Demand and Rapid Robotic Upside

Handheld Devices maintained a 30.86% share in 2025, reflecting widespread utility and familiar training paths in every operating theater. Procurement teams rely on predictable price points to manage large volumes, allowing Handheld lines to anchor the Saudi Arabia general surgical devices market. Laparoscopic portfolios follow closely thanks to national emphasis on minimally invasive methods. Electrosurgical and energy sealing systems remain staples in high-throughput centers, whereas Wound-Closure Devices sustain demand across hospitalization levels.

Robotics & 3D-Printed Patient-Specific Instruments log the fastest 6.18% CAGR as clinicians chase precision and lower revisions. King Faisal Specialist Hospital’s 1,370 robotic cases in 2024 demonstrate high performance that justifies new capital spending. SFDA 3D printing guidance streamlines certification for patient-matched guides, raising interest in bespoke implants that bolster surgical confidence. As private systems scale, integrated navigation and imaging suites lift share for Trocars & Access Devices and Navigation Systems. The Saudi Arabia general surgical devices market size is projected to gain additional lift from bundled OR rebuilds that combine robotics, imaging, and advanced energy tools.

By Application: Stable Core Segments and Obesity-Driven Acceleration

Gynecology & Urology procedures held 28.11% of Saudi Arabia general surgical devices market size in 2025, supported by demographic demand for reproductive and prostate interventions. The segment benefits from entrenched clinical pathways and a broad hospital footprint that ensures recurrent replacement orders. Cardiac surgeries contribute sizable volumes through specialized centers, while Orthopedic & Trauma cases remain driven by motor-vehicle accidents.

Bariatric & General Abdominal surgeries expand at a brisk 6.55% CAGR to 2031, reflecting obesity prevalence exceeding 35% among adults. Growing insurance coverage for bariatric procedures, alongside the roll-out of dedicated obesity programs, unlocks incremental device opportunities from stapling to energy sealing. Rising medical tourism for cosmetic and elective cases also sharpens demand in Other Applications, adding depth to the Saudi Arabia general surgical devices market.

By End User: Established Hospital Hubs and Outpatient Momentum

Public Hospitals & Medical Cities captured 33.02% of Saudi Arabia general surgical devices market share in 2025, boosted by a SAR 86 billion budget and centralized purchasing leverage. These institutions acquire premium systems faster due to stable state funding and robust support infrastructure. Private Hospitals continue to increase absolute procurement as Vision 2030 pushes for 65% private-sector care, with Dallah Health and Fakeeh Care leading SAR 9 billion in OR upgrades.

Ambulatory Surgical Centers grow at 6.78% CAGR as payer pressure and patient preference drive day-surgery expansion. ASCs favor compact energy systems and modular visualization platforms that keep capital outlay manageable yet efficient. Specialty and Bariatric Clinics differentiate by adopting robotic or 3D-printed solutions that attract niche patient groups, thus reinforcing segment variety within the Saudi Arabia general surgical devices market.

Competitive Landscape

The Saudi Arabia general surgical devices market sits in a moderately concentrated tier where multinational firms dominate through tight distributor alliances. Johnson & Johnson, Medtronic, and Stryker leverage global evidence libraries to secure reference accounts and navigate SFDA documentation swiftly. Local agents who understand NUPCO tender protocols are essential for repeat success. Price competition has intensified under the single-buyer model, yet clinical outcome data and total cost-of-ownership metrics allow premium manufacturers to defend margins when they deliver integrated robotic or AI-navigation suites.

Technology differentiation is accelerating. Early adopters of 3D printing, such as hospitals partnered with Materialise or Stratasys channels, are reshaping preoperative planning workflows. AI-powered imaging overlays attract neurosurgery and orthopedics departments looking for precision advantages. Simultaneously, domestic firms supported by National Industrial Development Fund grants are exploring joint ventures for basic consumables to trim the import bill. This dual trend of high-end imports and early-stage localization keeps competition dynamic and propels innovation cycles within the Saudi Arabia general surgical devices market.

White-space gaps remain in ambulatory-center focused carts, compact visualization towers, and surgeon education platforms. Players able to combine modular equipment with on-site service and tailored training see higher win rates. As private hospital groups expand bed capacity and the SFDA continues to refine fast-track pathways for critical devices, differentiation will hinge on speed to market, clinical evidence, and bundled service propositions in the Saudi Arabia general surgical devices market.

Saudi Arabia General Surgical Devices Industry Leaders

Conmed Corporation

B. Braun SE

Johnson & Johnson Services, Inc.

Medtronic plc

Stryker Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: The Saudi Food and Drug Authority released new regulations covering diagnostic laboratory equipment and 3D printing for patient-specific devices, establishing a clear approval framework.

- October 2024: Becton Dickinson signed an MoU with the Saudi Patient Safety Center to advance device utilization training and reduce surgical site infections.

- September 2024: Global Health Exhibition 2024 in Riyadh featured USD 13.3 billion in announced healthcare investments, spotlighting robotic systems and AI-navigation launches.

Saudi Arabia General Surgical Devices Market Report Scope

As per the scope of this report, general surgical devices refer to a range of devices used to perform different kinds of surgical procedures.

The Saudi Arabia General Surgical Devices Market is Segmented by Product (Handheld Devices, Laparoscopic Devices, Electro Surgical Devices, Wound Closure Devices, Trocars, and Access Devices, Other Products) and Application (Gynecology and Urology, Cardiology, Orthopaedic, Neurology, Other Applications). The report offers the value (in USD million) for the above segments.

By Product

| Handheld Devices |

| Laparoscopic Devices |

| Electrosurgical & Energy-Sealing Devices |

| Wound-Closure Devices |

| Trocars & Access Devices |

| Surgical Navigation & Imaging Systems |

| Robotics & 3D-Printed Patient-Specific Instruments |

By Application

| Gynecology & Urology |

| Cardiology / Cardiothoracic |

| Orthopedic & Trauma |

| Neurology & Spine |

| Bariatric & General Abdominal |

| Other Applications |

By End User

| Public Hospitals & Medical Cities |

| Private Hospitals |

| Ambulatory Surgical Centres |

| Specialty & Bariatric Clinics |

| By Product | Handheld Devices |

| Laparoscopic Devices | |

| Electrosurgical & Energy-Sealing Devices | |

| Wound-Closure Devices | |

| Trocars & Access Devices | |

| Surgical Navigation & Imaging Systems | |

| Robotics & 3D-Printed Patient-Specific Instruments | |

| By Application | Gynecology & Urology |

| Cardiology / Cardiothoracic | |

| Orthopedic & Trauma | |

| Neurology & Spine | |

| Bariatric & General Abdominal | |

| Other Applications | |

| By End User | Public Hospitals & Medical Cities |

| Private Hospitals | |

| Ambulatory Surgical Centres | |

| Specialty & Bariatric Clinics |

Key Questions Answered in the Report

How large will the Saudi Arabia general surgical devices market be by 2031?

It is projected to reach USD 323.59 million by 2031, growing at a 4.47% CAGR between 2026 and 2031.

Which product category is expanding fastest in Saudi Arabia?

Robotics & 3D-Printed Patient-Specific Instruments are forecast to log the highest 6.18% CAGR through 2031 as hospitals invest in precision technologies.

What drives demand for bariatric surgical devices in Saudi Arabia?

Adult obesity prevalence above 35% is leading to rapid growth in bariatric and metabolic procedures that require specialized stapling, energy sealing, and imaging devices.

Why are ambulatory surgical centers gaining traction?

Outpatient facilities help lower costs and improve patient convenience, growing at 6.78% CAGR as payer policies and Vision 2030 reforms favor same-day surgery models.

How does import dependence affect procurement budgets?

With USD 1.62 billion in device imports against limited local output, providers face foreign-exchange risk and potential supply disruptions that can inflate lifecycle costs.

What role does Vision 2030 play in surgical device adoption?

The program commits more than USD 65 billion to health infrastructure and targets 65% private-sector care, driving sustained investment in modern operating rooms and advanced surgical technologies.

Page last updated on: