Internet Radio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

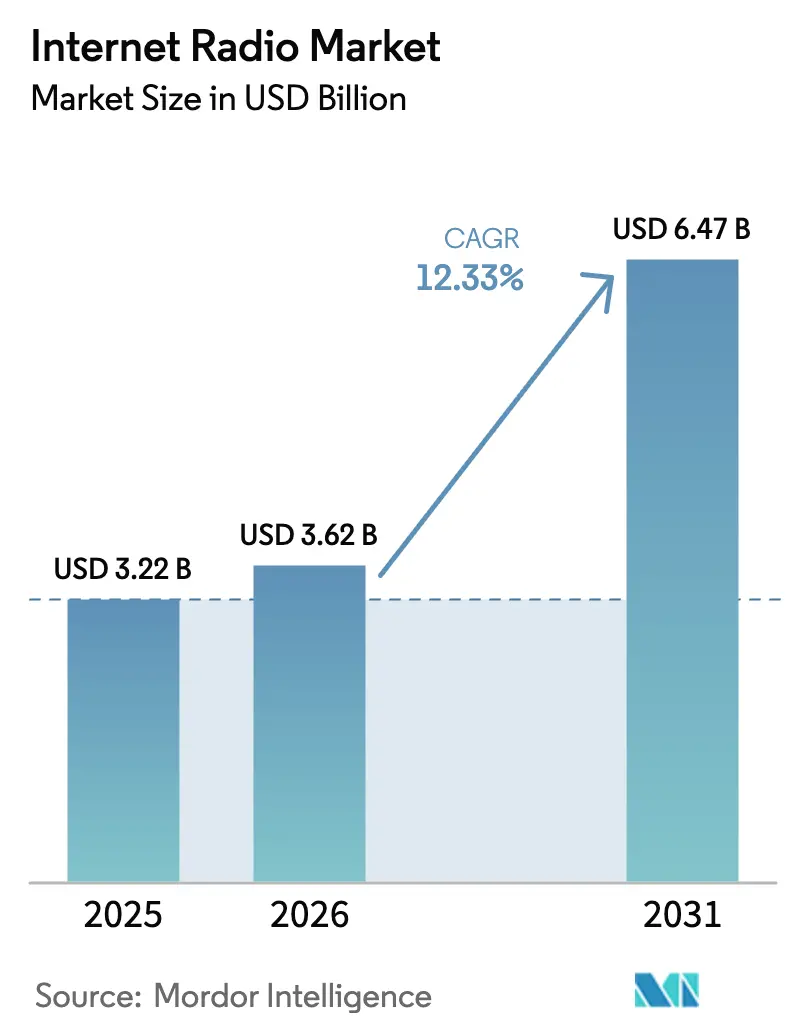

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 6.47 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

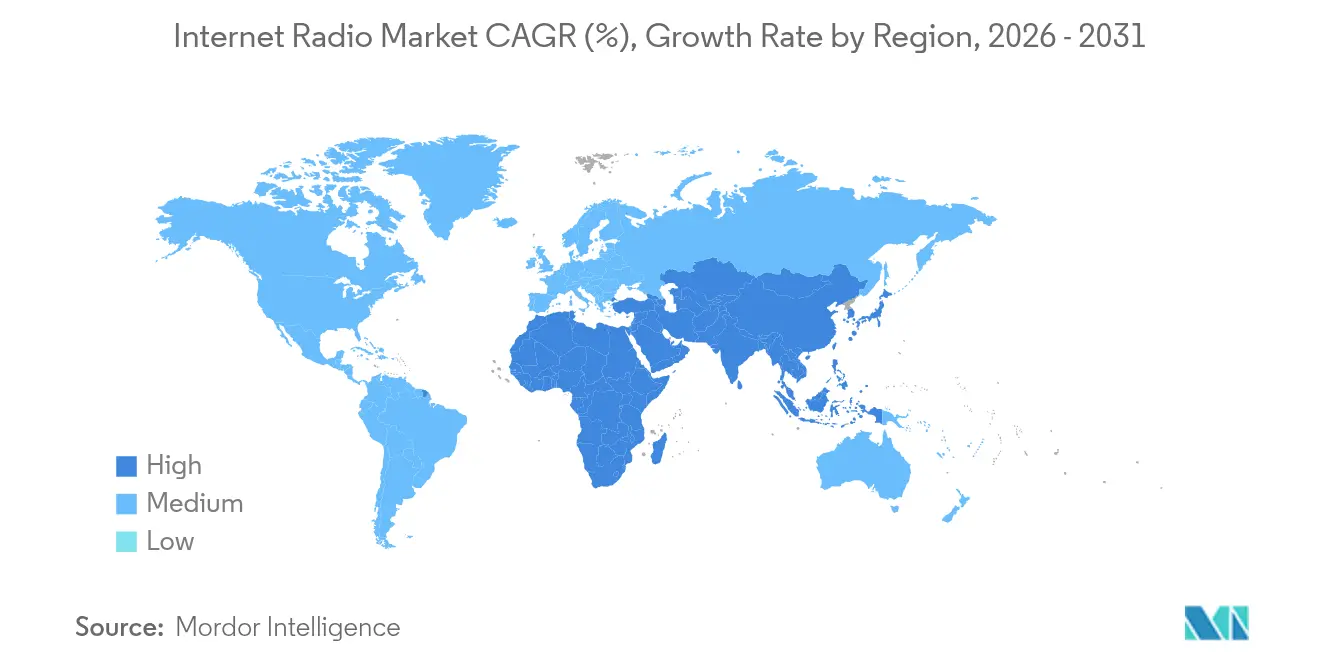

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internet Radio Market Analysis by Mordor Intelligence

The internet radio market size was valued at USD 3.22 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 6.47 billion by 2031, at a CAGR of 12.33% during the forecast period (2026-2031). Growth rests on wider broadband coverage, the rapid global adoption of smart speakers, and advertisers’ rising preference for programmatic audio. Nearly 4 billion monthly radio listeners worldwide drive USD 42 billion in radio advertising revenues that increasingly flow toward digital channels. North America continues to anchor demand, while Asia-Pacific opens the largest incremental opportunity as smartphone penetration climbs. Hyperlocal digital content, 5G-enabled high-bitrate mobile streams, and OEM integration in connected cars further strengthen the internet radio market’s long-term prospects. Intensifying competition is tempered by cloud-native automation that lowers entry barriers and sustains a pipeline of niche stations targeting underserved communities.

Key Report Takeaways

- By software media player, iTunes led with a 39.35% revenue share of the internet radio market in 2025, while the cloud/open-source “Others” category is projected to outpace peers at a 15.47% CAGR through 2031.

- By device, PCs commanded 33.25% of internet radio market share in 2025; smart devices are forecast to expand at a 19.62% CAGR to 2031.

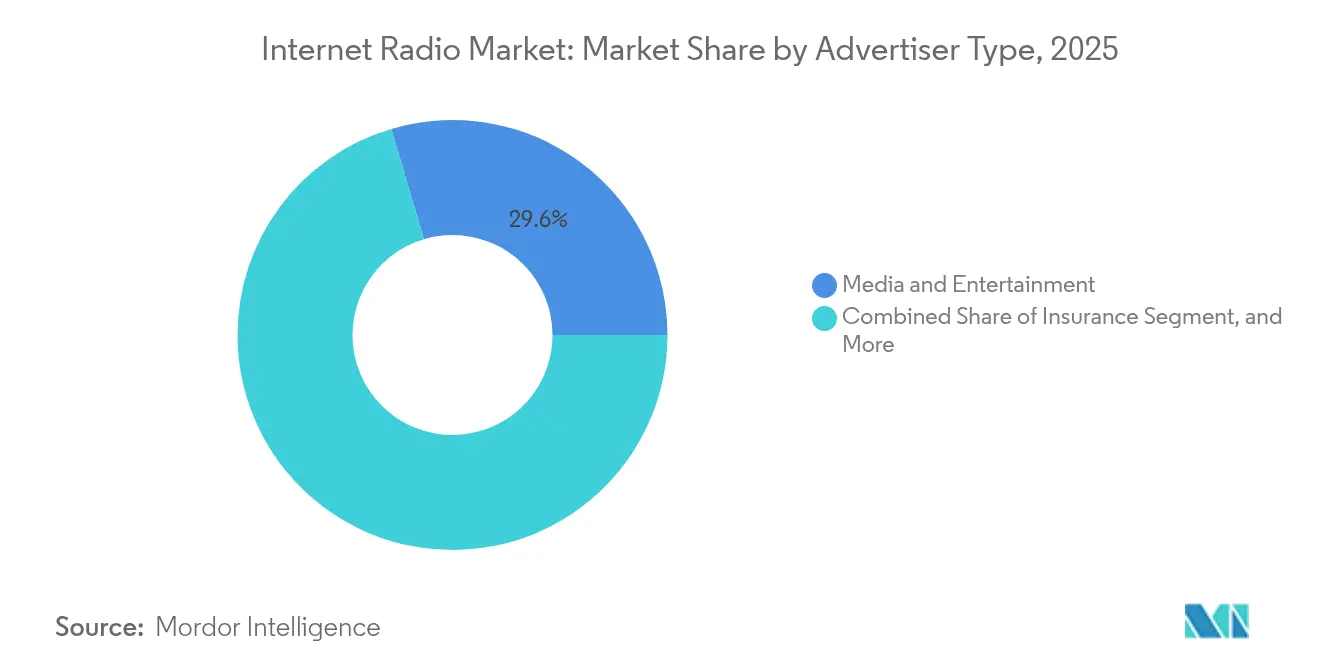

- By advertiser type, media & entertainment held 29.60% of 2025 spend, whereas consumer electronics is set to post the fastest 16.08% CAGR between 2026-2031.

- By geography, North America dominated with a 47.20% revenue share in 2025; Asia-Pacific is the fastest-growing region at an 17.65% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Internet Radio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperlocal content diversification | +3.1% | North America (spillover to Europe) | Medium term (2-4 years) |

| Smart-speaker adoption | +2.8% | Europe, North America | Short term (≤ 2 years) |

| Programmatic audio ROI | +2.3% | Asia-Pacific (global expansion) | Medium term (2-4 years) |

| 5G high-bitrate streams | +1.9% | South Korea, Japan, China | Medium term (2-4 years) |

| Connected-car OEM integration | +1.5% | Germany, US (developed markets) | Medium term (2-4 years) |

| Cloud-native broadcast automation | +1.3% | Global, focus on NA & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperlocal Content Diversification Driving Listener Stickiness in North America

Radio groups such as Townsquare Media operate 349 terrestrial stations while simultaneously running community-focused digital portals that serve local news, events, and classifieds. Only 0.5% of total page views in many U.S. markets go to local news sites.[1]Federal Communications Commission, “Less of the Same: The Lack of Local News on the Internet,” apps.fcc.gov The scarcity of localized information creates a moat for broadcasters that can curate hyperlocal feeds. As these stations shift live streams and podcasts onto digital channels, listener sessions lengthen and churn drops. Advertisers reward the deeper engagement with premium CPMs, lifting North American revenue yields even as global music streamers chase broader audiences.

Rapid Adoption of Smart Speakers Boosting Hands-Free Streaming in Europe

Voice-activated access is reshaping how households consume audio. Smart speakers are installed in 32% of Australian homes-a penetration rate mirrored in several European markets.[2]Department of Infrastructure, “Radio Prominence on Smart Speakers,” Australian Government, infrastructure.gov.au Voice search removes friction, so users explore a wider range of stations and retain them in daily routines. Regulators have drafted prominence rules that require platforms like Amazon Alexa and Google Assistant to surface local radio options alongside global services, preserving plurality. Broadcasters that invest early in voice skill optimization find their streams recommended more frequently, reinforcing brand recall and boosting the internet radio market within the region.

Programmatic Audio Advertising ROI Outperforming Display in Asia

Digital audio advertising revenue grew 18.9% in 2023 to USD 7 billion.[3]David Cohen, “Internet Advertising Revenue Report 2023,” Interactive Advertising Bureau and PwC, iab.com Brands in China, India, and Indonesia are reallocating spend from static banners to programmatic audio because mid-roll spots achieve completion rates above 96%. Curated marketplaces match listener mood, location, and device context with creative assets, raising click-through and conversion metrics. Even with heightened privacy rules, non-cookie identifiers-such as content, time-of-day, and first-party login data-maintain addressability, sustaining the internet radio market’s share of total media budgets.

5G Roll-outs Enabling High-Bitrate Mobile Streams in South Korea and Japan

5G Broadcast blends linear transmission efficiency with the unicast flexibility of IP networkse. Korean and Japanese operators now deliver 320 kbps streams without buffer delays, enabling lossless audio and immersive formats. Listeners use smartphones as primary receivers during commutes, cementing mobile as a substitute for fixed listening. While spectrum policy and handset availability still limit coverage in parts of China, early adopters demonstrate that low-latency, high-quality streams lift session duration and attract new premium subscribers

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising licensing fees | −1.9% | United States (global implications) | Long term (≥ 4 years) |

| Ad-blocking extensions | −1.5% | Global (higher in developed markets) | Medium term (2-4 years) |

| Data-usage regulations | −1.3% | Europe, California (expanding) | Medium term (2-4 years) |

| Spectrum re-allocation | −1.0% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Music Licensing Fees Compressing Margins of Pure-Play Streamers in the U.S.

Performance rights organizations continue to negotiate higher royalty rates, pushing operating costs upward. Streaming royalties account for 80% of music-industry income.[4]Investopedia Editors, “How Pandora and Spotify Pay Artists,” Investopedia, investopedia.com The National Association of Broadcasters argues that additional performance taxes threaten local jobs.[5]National Association of Broadcasters, “A Performance Tax Threatens Local Jobs,” nab.org Smaller webcasters with narrow playlists struggle to absorb increases, reducing catalog breadth or shifting to subscription models that dampen audience growth. The constraint persists over the forecast horizon, weighing on the internet radio market’s profitability in the United States.

Ad-Blocking Extensions Curtailing Monetization on Browser-Based Players

Ad-avoidance software suppresses impressions and undermines CPM-based revenue. Studies link ad fatigue and intrusive formats to higher blocker adoption. As desktop listening still accounts for a sizable share in developed economies, blocked inventory leads to under-monetized sessions. Platforms respond by adding server-side ad stitching, diversified commerce modules, and discounted subscription tiers that remove ads altogether. Execution success varies, leaving monetization gaps that slow revenue scaling for certain segments of the internet radio market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Media Player: iTunes Dominance Faces Cloud Challenge

iTunes controlled 39.35% of segment revenue in 2025, illustrating the power of closed-loop ecosystems where hardware, OS, and storefront converge. Tight integration across iPhone, iPad, and macOS keeps churn minimal among higher-income users. In contrast, the “Others” bucket-primarily cloud-based and open-source players-is set to climb at a 15.47% CAGR through 2031. Listeners value platform-agnostic access, modular plug-ins, and lower CPU footprints. Windows Media Player and Winamp retain niche followings for customizable skins and legacy library support, though both lag on cross-device cloud sync. The competitive narrative is shifting as leading streaming services embed proprietary players; Spotify reported 675 million monthly active users and 263 million premium subscribers in Q4 2024. Control over playback technology yields richer behavioral data, refining recommendation engines, and improving ad targeting precision that collectively reinforce the internet radio market’s revenue flywheel.

At the same time, media-player vendors pursue partnerships with independent stations to surface live feeds in content carousels, adding long-tail diversity. HTML5-based web players gain relevance for low-latency delivery and server-side ad-insertion support, shrinking reliance on desktop executables. Over the forecast period, vertical integration blurs the line between player and platform. Agile, open-API architectures will likely win share from legacy monoliths as the internet radio market rewards flexibility and speed to deploy new codecs, immersive formats, and AI-driven personalization.

By Device Support: Smart Devices Redefine Listening Habits

PCs remained the leading access point in 2025 with a 33.25% internet radio market share, buoyed by office-hour listening and multitasking convenience. However, smart devices-including smart speakers, smart displays, and wearables-are set to register a 19.62% CAGR from 2026-2031, the fastest across all hardware classes. Voice-first interactions shorten discovery time, boosting total listening hours and encouraging hands-free exploration. Regulatory proposals in Australia and Europe mandate equal prominence for licensed radio services on these devicest. Compliance unlocks wider distribution for broadcasters that optimize conversational UI cues and structured station metadata.

Tablets and laptops fill the mid-mobility gap, serving households that prefer visual cover art and interactive playlists. Smartphones benefit disproportionately from 5G bandwidth that supports lossless streams, reducing historical quality trade-offs. Automotive dashboards emerge as strategic battlegrounds as OEMs preload audio apps and extend voice assistants to steering-wheel controls. The internet radio market size for connected-vehicle listening is projected to expand rapidly as annual new-car shipments integrate infotainment systems with embedded eSIMs. Cross-device synchronization-maintaining a paused stream from kitchen smart display to in-car head unit-creates stickiness that traditional AM/FM cannot match.

By Advertiser Type: Entertainment Leads While Electronics Accelerates

Media and entertainment advertisers captured 29.60% of 2025 spend, aligning film, streaming-video, and gaming promotions with audio audiences exploring culture and leisure content. Category synergy results in superior brand recall, keeping CPMs resilient. Consumer electronics brands, however, are forecast to climb at a 16.08% CAGR through 2031. Device launches increasingly pair with voice-enabled campaigns that demonstrate product functionality in real time. Programmatic platforms optimize spots based on listener device, location, and previous shopping behavior, raising conversion odds.

Insurance, travel, and QSR (quick-service-restaurant) sectors broaden mix allocation as brand-safety controls, contextual segments, and third-party verification improve. UK commercial radio advertising grew 3.2% year-over-year in 2024, nearly recapturing its 2022 peak. In parallel, digital audio ad spend rose 12% to USD 176 million, powered by a 23% increase in podcast placements Ofcom. Diversified demand insulates publishers from cyclical shifts in any single industry, supporting sustainable CPMs across the broader internet radio market.

Geography Analysis

North America generated 47.20% of 2025 revenue, anchored by wide broadband coverage, mature digital advertising infrastructure, and a premium consumer base. Local radio ad spend stood at USD 13.6 billion in 2024 Radio Advertising Bureau. Hyperlocal content drives differentiation, as demonstrated by Townsquare Media’s dual terrestrial-digital model that captures both community audiences and national advertisers. Rising performance royalties and privacy legislation introduce cost and compliance complexity, yet investment in cloud-native automation cushions margins for independent stations. Programmatic audio’s data-rich inventory keeps the internet radio market resilient even as economic headwinds weigh on discretionary ad budgets.

Asia-Pacific is forecast to deliver an 17.65% CAGR from 2026-2031, the highest globally. Population scale, cheaper data plans, and smartphone ubiquity expand the listener base. Commercial 5G roll-outs underpin lossless mobile streams, while governments in India, China, and Malaysia trial 5G Broadcast for hybrid unicast-broadcast delivery. Advertisers are reallocating spend after witnessing audio outperform display on ROI metrics. The region’s relatively low historical penetration leaves ample headroom, positioning the internet radio market size in Asia-Pacific for outsized absolute dollar growth.

Europe demonstrates sophisticated consumption patterns shaped by stringent regulation and high smart-speaker uptake. Online listening surpassed AM/FM for the first time in 2024, taking 28% of live radio hours. Voice-assistant prominence rules aim to protect pluralism, giving public-service broadcasters and local stations guaranteed discoverability. German OEMs ship vehicles with native internet radio apps, deepening in-car listening. Although macroeconomic softness tempers ad-spend momentum, strong cultural affinity for audio content and widespread broadband keep upside intact. South America and the Middle East and Africa remain nascent but show accelerating adoption, supported by improved 4G/5G coverage and rising disposable income, adding diversity and incremental volume to the global internet radio market

Competitive Landscape

The internet radio market combines scaled platforms with a vibrant long-tail. Spotify, Apple Music, and Amazon Music collectively attract hundreds of millions of users, translating into formidable negotiating leverage with labels and advertisers. Spotify’s 675 million MAUs and 263 million premium subscribers in Q4 2024 underscore subscription momentum. Apple pushes exclusivity through Dolby Atmos spatial audio to differentiate from rivals, while Amazon leverages Prime bundling to lower acquisition cost. Mid-tier players such as iHeartMedia anchor hybrid ad-subscription models; digital audio revenue reached USD 339 million in Q4 2024, up 7% year-over-year.

Independent stations leverage cloud-native broadcast software to minimize capex and target micro-communities. Open-source encoders and SaaS playout solutions cut OPEX by 10-15%, fostering innovation in genre-specific channels. Voice-assistant gatekeeping shapes competitive access; algorithms that favor station engagement metrics encourage producers to optimize metadata and sonic branding. Automotive integrations represent the next frontier. Agreements between broadcasters and German OEMs embed apps in infotainment stacks, simplifying discovery during commutes and adding defensibility.

Consolidation remains selective. Platforms acquire podcast networks to secure exclusive talent and diversify revenue beyond music royalties. Warner Music Group’s 8.2% streaming-revenue growth in fiscal 2024, despite softer ad-supported streams, highlights the importance of subscription economics. The outlook favors firms with multidimensional revenue-ads, subscriptions, live-event tie-ins, and merchandising-over single-source models. Regulatory scrutiny on anticompetitive practices and data privacy remains a watchpoint but has yet to materially dampen innovation within the internet radio market.

Internet Radio Industry Leaders

CBS Corporation

Citadel Broadcasting Corporation

Chrysalis Group

Pandora Media Inc.

TuneIn Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Annenberg Inclusion Initiative highlighted only 13.2% women and 7.9% under-represented executives in music streaming leadership Annenberg Inclusion Initiative.

- March 2025: iHeartMedia posted a 7% rise in Q4 2024 digital audio revenue to USD 339 million; podcast sales grew 6% to USD 140 million iHeartMedia.

- February 2025: Spotify disclosed 675 million MAUs and 263 million premium subscribers for Q4 2024 Spotify Investor Relations.

- January 2025: Australian Government proposed smart-speaker prominence rules to secure consistent access to licensed radio services Australian Government.

Global Internet Radio Market Report Scope

Internet radio is an audio service that uses the Internet as a distribution medium of broadcasting instead of the traditional radio waves. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The internet radio market is segmented by software media player (Itunes, Windows Media Player, Winamp and Others), by device support (PC, Laptop, Tablet, Smart Device and Other Devices), by advertiser type (Insurance, Travel Airline, Restaurant, Consumer Electronics, Media & Entertainment and Others) and by geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| iTunes |

| Windows Media Player |

| Winamp |

| Others |

| PC |

| Laptop |

| Tablet |

| Smart Device |

| Other Devices |

| Insurance |

| Travel and Airlines |

| Restaurant |

| Consumer Electronics |

| Media and Entertainment |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Software Media Player | iTunes | |

| Windows Media Player | ||

| Winamp | ||

| Others | ||

| By Device Support | PC | |

| Laptop | ||

| Tablet | ||

| Smart Device | ||

| Other Devices | ||

| By Advertiser Type | Insurance | |

| Travel and Airlines | ||

| Restaurant | ||

| Consumer Electronics | ||

| Media and Entertainment | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the internet radio market?

The internet radio market stands at USD 3.62 billion in 2026 and is projected to reach USD 6.47 billion by 2031, supported by a 12.33% CAGR.

Which region leads internet radio revenues?

North America accounts for 47.20% of global revenue in 2025, thanks to high broadband penetration and strong advertiser dem

What is driving the rapid growth of internet radio in Asia-Pacific?

Asia-Pacific’s 17.65% forecast CAGR comes from rising smartphone adoption, expanding 5G networks that enable high-quality mobile streams, and superior ROI from programmatic audio advertising.

How are smart speakers influencing listening habits?

Smart-speaker penetration of roughly one-third of households in leading European markets enables voice-activated discovery, extending daily listening time and boosting the internet radio market’s monetization potential.

Why are music licensing fees a major restraint?

Escalating royalty rates raise operating expenses for pure-play streamers, pressuring margins and encouraging pivots toward subscription or hybrid business models to offset cost increases.

What strategic moves are market leaders making?

Spotify is scaling exclusive podcasts and proprietary playback tech; Apple leverages spatial audio to differentiate; Amazon integrates internet radio services into connected-home and automotive ecosystems, broadening distribution channels.

Page last updated on: