Global Interleukin Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

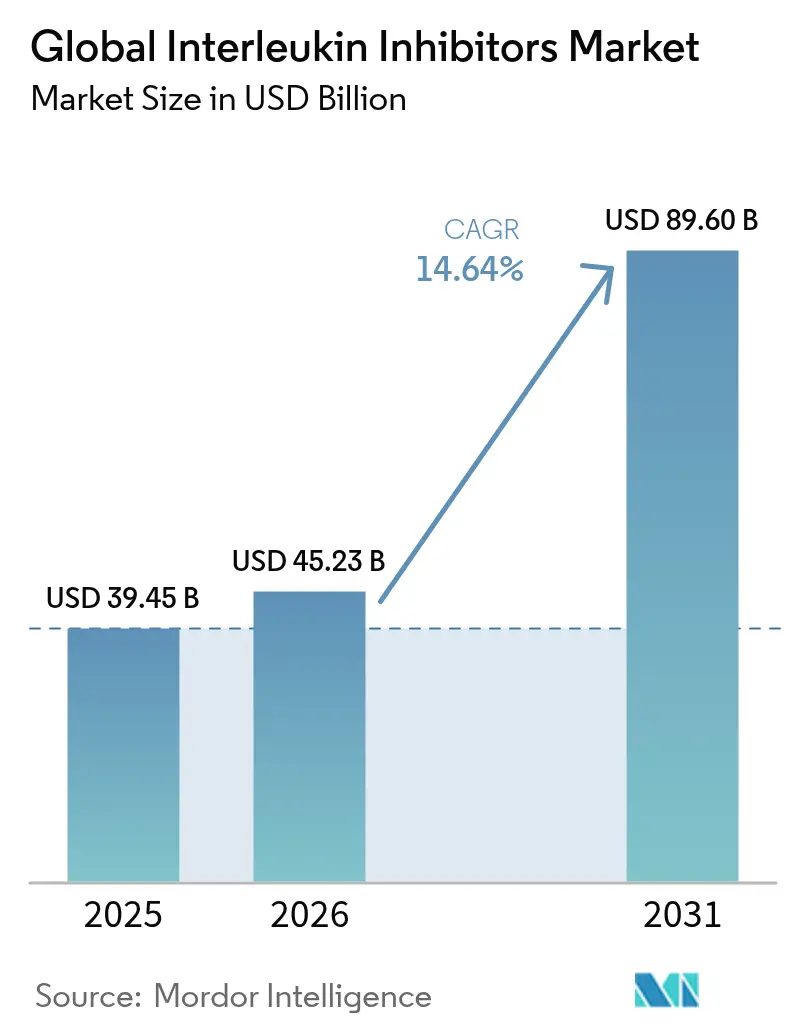

| Market Size (2026) | USD 45.23 Billion |

| Market Size (2031) | USD 89.6 Billion |

| Growth Rate (2026 - 2031) | 14.64% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Interleukin Inhibitors Market Analysis by Mordor Intelligence

The interleukin inhibitors market size in 2026 is estimated at USD 45.23 billion, growing from 2025 value of USD 39.45 billion with 2031 projections showing USD 89.6 billion, growing at 14.64% CAGR over 2026-2031. This rapid expansion anchors the interleukin inhibitors market size firmly within mainstream immunology as rising autoimmune prevalence, payer alignment for targeted biologics, and next-generation pipeline approvals reinforce demand worldwide. Demand is further supported by the global increase in autoimmune conditions recorded, while biosimilar penetration, AI-assisted drug discovery, and successful COVID-19 cytokine storm indications diversify revenue streams[1]Source: AbbVie Communications, “Three Ways AI Is Changing Drug Discovery at AbbVie,” AbbVie, abbvie.com . North America remains the primary revenue hub, yet the Asia-Pacific growth engine, strengthened by improved reimbursement and local manufacturing, is narrowing the gap. Subcutaneous delivery formats dominate prescribing habits and will continue gaining share as digital-enabled autoinjectors improve adherence. Competitive intensity is heightened by the patent expiry cycle, with ustekinumab biosimilars eroding originator share and setting the stage for a broader biosimilar wave through 2030.

Key Report Takeaways

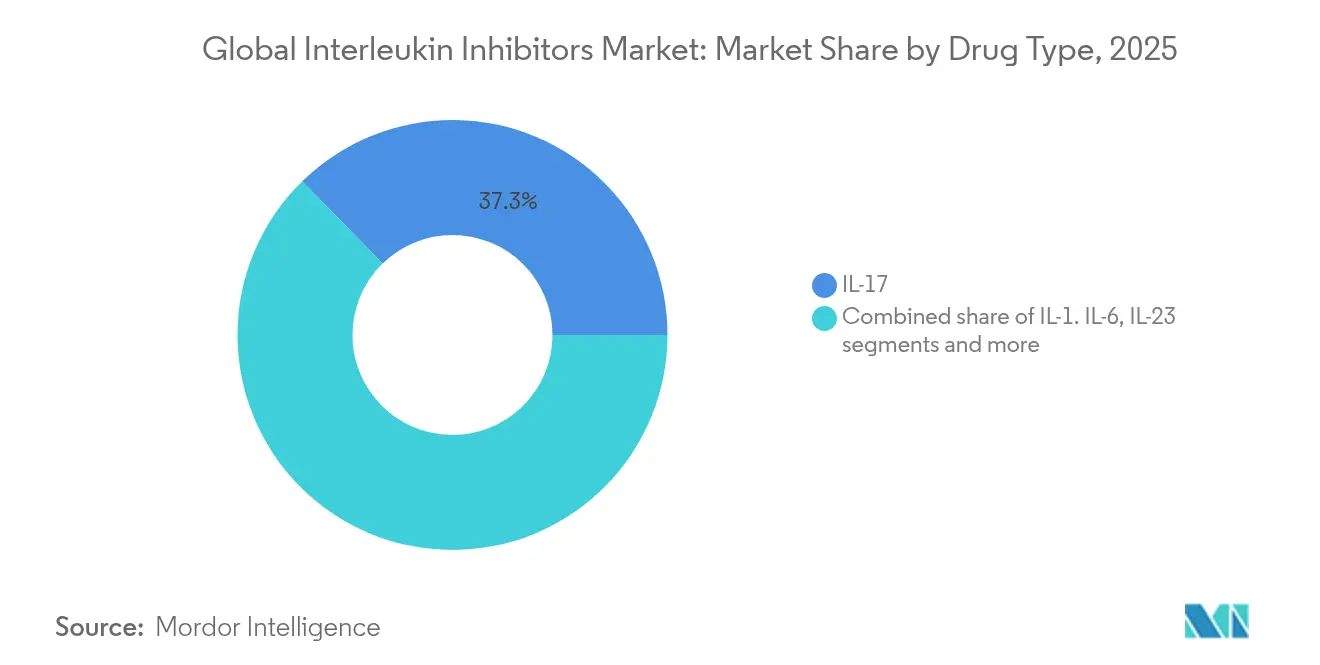

- By drug type, IL-17 inhibitors led with 37.32% revenue share in 2025; IL-23 inhibitors are forecast to expand at a 15.32% CAGR to 2031.

- By application, psoriasis captured 45.74% of the interleukin inhibitors market share in 2025, while ankylosing spondylitis is projected to advance at a 15.74% CAGR through 2031.

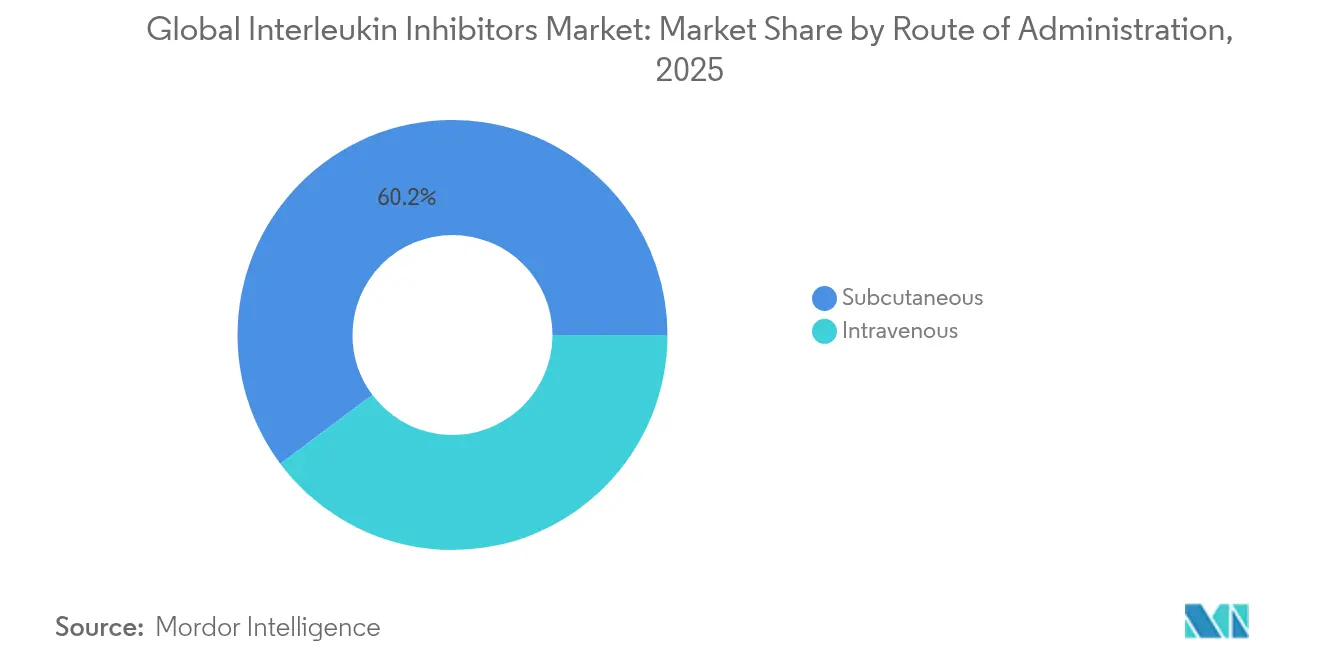

- By route of administration, subcutaneous delivery accounted for 60.21% of the interleukin inhibitors market size in 2025 and is expected to grow at a 16.05% CAGR during 2026-2031.

- By end-user, hospitals held 56.95% of 2025 revenue; home-care and self-administration programs are poised for the fastest 16.18% CAGR through 2031.

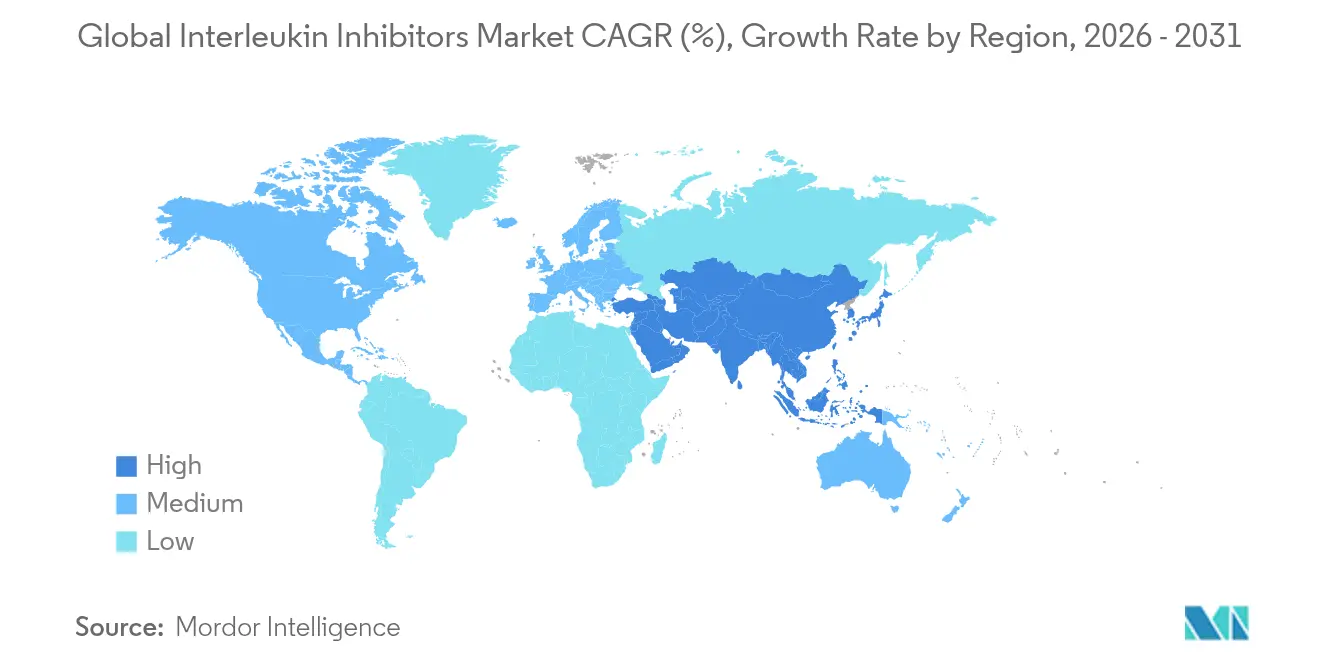

- By geography, North America commanded 41.78% of 2025 sales, while Asia-Pacific is projected to post the highest 16.42% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Interleukin Inhibitors Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prevalence of autoimmune & autoinflammatory diseases | +2.8% | Global, with higher concentration in North America & Europe | Long term (≥ 4 years) |

| Accelerated FDA & EMA approvals for next-gen IL-17/IL-23 biologics | +2.1% | Global, spill-over to emerging markets | Medium term (2-4 years) |

| Shift toward convenient self-injectable formulations | +1.9% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Expanding reimbursement in emerging Asian markets | +1.4% | APAC core, with early gains in China, India, Japan | Medium term (2-4 years) |

| AI-enabled target discovery for novel interleukin pathways | +0.8% | Global, concentrated in US & EU research hubs | Long term (≥ 4 years) |

| Clinical success of IL inhibitors in severe COVID-19 cytokine storm | +0.6% | Global, with institutional adoption patterns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Autoimmune & Autoinflammatory Diseases

Global autoimmune incidence has climbed, with conditions such as Graves’ disease accelerating most sharply . Higher prevalence in North America and Europe concentrates demand and drives premium pricing power. Multi-morbid presentations create complex treatment pathways that favor high-specificity biologics over broad immunosuppressants. Rheumatology and dermatology clinics report growing first-line use of interleukin inhibitors, reflecting guideline evolution. Sustained epidemiologic pressure therefore preserves the long-run revenue base of the interleukin inhibitors market.

Accelerated FDA & EMA Approvals for Next-Gen IL-17/IL-23 Biologics

Between 2024 and early 2025, regulators cleared several breakthrough assets, including bimekizumab for hidradenitis suppurativa and icotrokinra as the first oral IL-23 receptor inhibitor . Expedited review pathways shorten launch cycles and support premium introductory pricing. EMA endorsement of four ustekinumab biosimilars in 2024 demonstrates parallel confidence in class safety while intensifying price competition. Collectively, faster approvals lift physician willingness to switch within the same therapeutic class when superior convenience or efficacy is shown, boosting overall interleukin inhibitors market growth.

Shift Toward Convenient Self-Injectable Formulations

Seventy-two percent of prescriptions now specify self-administration, enabled by high-concentration autoinjectors that deliver >100 mg/mL with acceptable viscosity . Real-world adherence studies show superior persistence for subcutaneous over intravenous regimens. Digital sensors embedded in injectors generate dosing analytics that inform personalized titration and early flare detection. Payers increasingly favor home-based models because they lower infusion-center costs, fostering broader adoption and reinforcing the interleukin inhibitors market trajectory.

Expanding Reimbursement in Emerging Asian Markets

Japan, South Korea, and Taiwan cover 30-40% of Crohn’s disease patients for biologic therapy, whereas India remains under 1% due to limited insurance penetration. China’s domestic IL-17A inhibitor programs have progressed through later-stage trials, promising locally produced alternatives that will expand access while capping costs. National reimbursement extensions in Asia-Pacific therefore unlock volume gains despite price sensitivity, propelling the regional contribution to the interleukin inhibitors market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition cost versus small-molecule DMARDs | -1.8% | Global, with acute impact in emerging markets | Long term (≥ 4 years) |

| Looming biosimilar competition post-2026 | -1.5% | North America & EU core, expanding globally | Medium term (2-4 years) |

| Adverse infection-risk profile & black-box warnings | -1.2% | Global, with regulatory variation | Long term (≥ 4 years) |

| Payer preference shifting to step-therapy prior authorizations | -0.9% | North America core, expanding to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost Versus Small-Molecule DMARDs

Annual biologic therapy costs run from USD 14,000 to USD 91,609, far exceeding older disease-modifying antirheumatic drugs. Out-of-pocket ceilings in low-income markets remain prohibitive, restricting uptake. Payers demand real-world cost-offset evidence, forcing manufacturers to deliver head-to-head superiority data with hard endpoints such as hospitalization avoidance. The pricing premium therefore suppresses full-potential demand for the interleukin inhibitors market in cost-sensitive geographies.

Looming Biosimilar Competition Post-2026

Fourteen ustekinumab biosimilars have entered or are queued for launch, trimming Stelara revenue year-over-year and foreshadowing similar erosion for additional agents as patent cliffs loom . Aggressive list-price discounting similar to the adalimumab experience is expected, stressing originator margins. Nonetheless, lower prices may expand overall patient reach, partially offsetting revenue loss and altering the interleukin inhibitors market competitive equilibrium.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: IL-23 Inhibitors Drive Next-Generation Growth

IL-17 inhibitors anchored 37.32% of 2025 revenue, underpinned by durable efficacy in plaque psoriasis, psoriatic arthritis, and ankylosing spondylitis. Despite leadership, competitive breadth has intensified as bimekizumab expanded into hidradenitis suppurativa and axial spondyloarthritis. IL-23 inhibitors exhibit the fastest 15.32% CAGR because oral icotrokinra combines convenience with disease-modifying potential. Tocilizumab sustains IL-6 inhibitor relevance through COVID-19 and giant cell arteritis expansions. Niche IL-1 inhibitors cater to rare autoinflammatory syndromes, while dual-target regimens reflect a precision trend that widens addressable patient cohorts. Collectively, differentiated mechanisms diversify the interleukin inhibitors market size across drug classes, buffering against single-class risk.

The shift from parenteral to oral small-molecule IL-23 antagonists also enlarges eligible patient pools unwilling to self-inject. Pipeline innovation contains multiple multi-cytokine inhibitors aiming for broader suppression with fewer injections. Consequently, therapeutic class evolution ensures the interleukin inhibitors market retains a balanced assortment of established and emerging modalities through 2031.

By Application: Psoriasis Leadership Faces Ankylosing Spondylitis Challenge

Psoriasis delivered 45.74% of 2025 value, reinforced by clear superiority over systemic steroids and phototherapy. High skin-clearance rates such as PASI 90 attainment exceed 49.6% on oral icotrokinra, renewing enthusiasm for first-line biologic adoption. Meanwhile, ankylosing spondylitis shows 15.74% CAGR as improved MRI diagnostics broaden axial spondyloarthritis recognition. Rheumatoid arthritis remains a sizeable but slower-growth cohort because mature TNF inhibitors and JAKs compete aggressively on price. Inflammatory bowel disease advances on TREMFYA’s Crohn’s disease label expansion, while miscellaneous autoinflammatory conditions will benefit from AI-discovered interleukin pathways. These mixed dynamics keep the interleukin inhibitors market diversified across immune-mediated disorders.

Employing biomarker-guided treatment algorithms further optimizes positioning. Dermatologists and rheumatologists increasingly triage patients by cytokine profile, matching IL-23 blockers to skin-dominant disease and IL-17 blockers to axial manifestations. Precision matching enhances therapeutic outcomes and reinforces the interleukin inhibitors market share for optimized molecules.

By Route of Administration: Subcutaneous Dominance Accelerates

Subcutaneous formulations represented 60.21% of 2025 sales and outpace all routes at 16.05% CAGR. Autoinjectors deliver home-based doses that reduce infusion-center traffic and hospital cost. High-viscosity device engineering solved prior volume limits, enabling >100 mg/mL doses in under 15 seconds . Intravenous induction remains critical for acute Crohn’s disease flares and severe systemic presentations but is gradually relegated to complex cases. Market research shows that self-injection adherence rises when coupled with smartphone reminder apps and sensor-verified dose logging. These integrated platforms lend a digital overlay that preserves the competitive edge of subcutaneous therapies within the interleukin inhibitors market.

By End-User: Home-Care Programs Reshape Treatment Paradigms

Hospitals commanded 56.95% of 2025 consumption, reflecting initiation protocols, pharmacovigilance, and severe-case management. Yet home-care programs register the highest 16.18% CAGR as payers incentivize outpatient models to avoid facility fees. Specialty clinics build niche expertise that bridges full inpatient care and home administration, capturing complex but stable patients. Positive patient-reported outcomes underscore convenience, improved quality of life, and productivity gains, which amplify homecare pull. Device training modules and virtual nurse check-ins mitigate safety concerns, firmly rooting home settings in the evolving interleukin inhibitors market landscape.

Geography Analysis

North America generated 41.78% of 2025 revenue due to comprehensive insurance coverage and an early-adopter clinician culture. Biosimilar entry is expected to soften price points but widen access, balancing revenue shifts. Europe follows with entrenched national tender frameworks that negotiate volume-linked discounts, promoting class sustainability. Asia-Pacific posts the highest 16.42% CAGR, driven by China’s local production, India’s emerging private insurance products, and Japan’s expanding indications list. Growing disease recognition and guideline alignment push biologic initiation earlier in patient journeys, accelerating volume capture in the Asia-Pacific interleukin inhibitors market.

Latin American uptake is uneven; Brazil leads adoption through its Unified Health System, while other countries face procurement budget limits. Middle East & Africa show double-digit unit growth off a small base, with GCC reimbursement committees gradually incorporating biologics for psoriasis and rheumatoid arthritis. As tender wins propagate, regional visibility increases, supporting physician familiarity. Overall, geography diversity cushions macro-economic shocks and sustains the interleukin inhibitors market growth curve worldwide.

Competitive Landscape

The top five manufacturers control an majority of global revenue, yielding a moderately concentrated arena. Novartis leads on the strength of Cosentyx, which spans five major indications. Eli Lilly follows with via Taltz’s penetration into dermatology and rheumatology. Johnson & Johnson leverages TREMFYA and the oral icotrokinra program. AbbVie contributes with Skyrizi and strategic AI investments that compress discovery timelines, strengthening life-cycle management. Bimekizumab’s dual IL-17A/F profile has given UCB a rising presence.

Strategic emphasis centers on label expansions rather than de-novo targets, maximizing R&D productivity. Corporates also deepen digital companions that monitor dosing adherence, providing real-world evidence to payers. Biosimilar makers intensify price competition, but innovators counter with formulation upgrades and convenience features. Emerging AI-native firms such as Insilico are courting partnerships to plug pipeline gaps for larger players, reshaping the future dynamics of the interleukin inhibitors market.

Global Interleukin Inhibitors Industry Leaders

AbbVie, Inc

Johnson and Johnson

Novartis AG

Eli Lilly and Company

GlaxoSmithKline Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Johnson & Johnson reported Phase 3 oral icotrokinra results showing 64.7% IGA 0/1 and 49.6% PASI 90 in plaque psoriasis, heralding the first oral IL-23 inhibitor with high efficacy

- July 2025: Novartis announced the Phase III GCAptAIN study of Cosentyx in giant cell arteritis did not meet its primary endpoint but demonstrated steroid-sparing trends

Global Interleukin Inhibitors Market Report Scope

As per the scope of the report, Interleukin inhibitors are immunosuppressive agents which inhibit the action of interleukins which are synthesized by monocytes, macrophages, lymphocytes and certain other cells. The Interleukin Inhibitors Market is Segmented by Type (IL-1, IL-5, IL-6, IL-17, IL-23, and Other Types), Application (Psoriasis, Arthritis, Asthma, Inflammatory Bowel Disease, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| IL-1 Inhibitors |

| IL-6 Inhibitors |

| IL-17 Inhibitors |

| IL-23 Inhibitors |

| Multi-target / Others |

| Psoriasis & Psoriatic Arthritis |

| Rheumatoid Arthritis |

| Inflammatory Bowel Disease (Crohn’s & UC) |

| Ankylosing Spondylitis |

| Other Auto-Inflammatory Disorders |

| Subcutaneous |

| Intravenous |

| Hospitals |

| Specialty Clinics |

| Home-care / Self-administration Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Drug Type | IL-1 Inhibitors | |

| IL-6 Inhibitors | ||

| IL-17 Inhibitors | ||

| IL-23 Inhibitors | ||

| Multi-target / Others | ||

| By Application | Psoriasis & Psoriatic Arthritis | |

| Rheumatoid Arthritis | ||

| Inflammatory Bowel Disease (Crohn’s & UC) | ||

| Ankylosing Spondylitis | ||

| Other Auto-Inflammatory Disorders | ||

| By Route of Administration | Subcutaneous | |

| Intravenous | ||

| By End-user | Hospitals | |

| Specialty Clinics | ||

| Home-care / Self-administration Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current market size of the interleukin inhibitors market?

The interleukin inhibitors market size reached USD 45.23 billion in 2026 and is forecast to expand to USD 89.6 billion by 2031.

Which drug class leads the interleukin inhibitors market?

IL-17 inhibitors lead with 37.32% 2025 revenue share, driven by well-established agents covering multiple autoimmune indications.

Which region is growing fastest in the interleukin inhibitors market?

Asia-Pacific posts the highest 16.42% CAGR to 2031 due to expanding reimbursement, local manufacturing, and rising autoimmune diagnosis rates.

4 Why is subcutaneous delivery preferred for interleukin inhibitors?

High-concentration autoinjectors enable home-based dosing, improve adherence, and lower infusion-center costs, giving subcutaneous formats both the largest share and fastest growth.

Page last updated on: