Interferons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

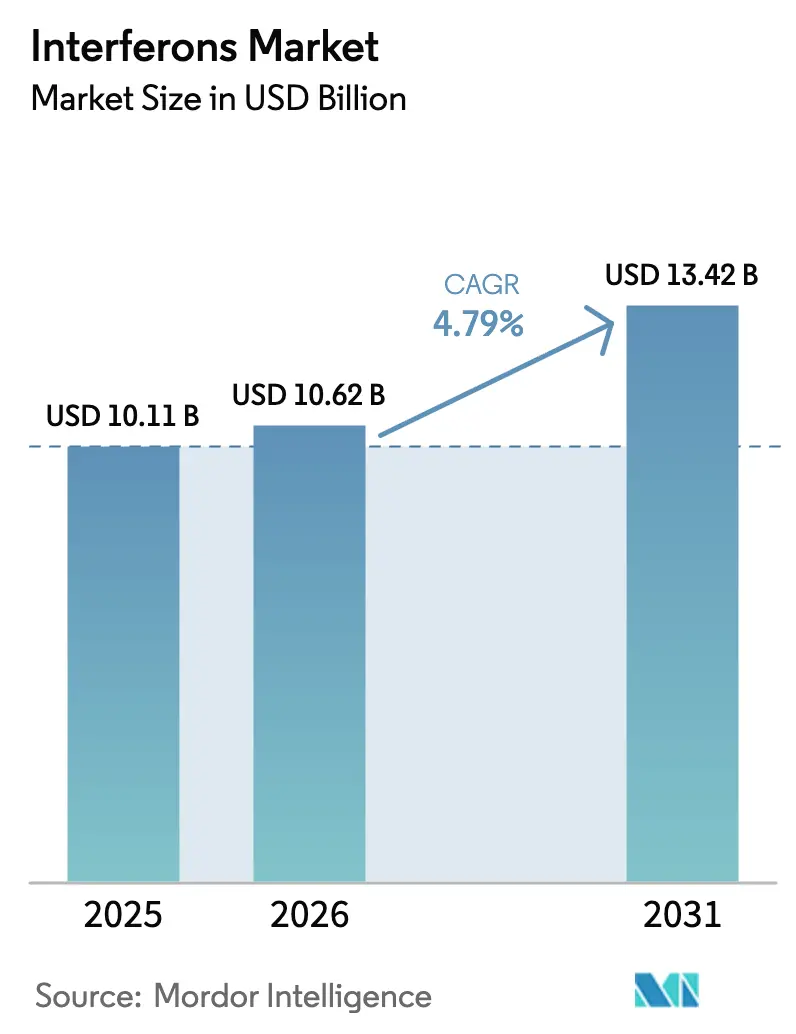

| Market Size (2026) | USD 10.62 Billion |

| Market Size (2031) | USD 13.42 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

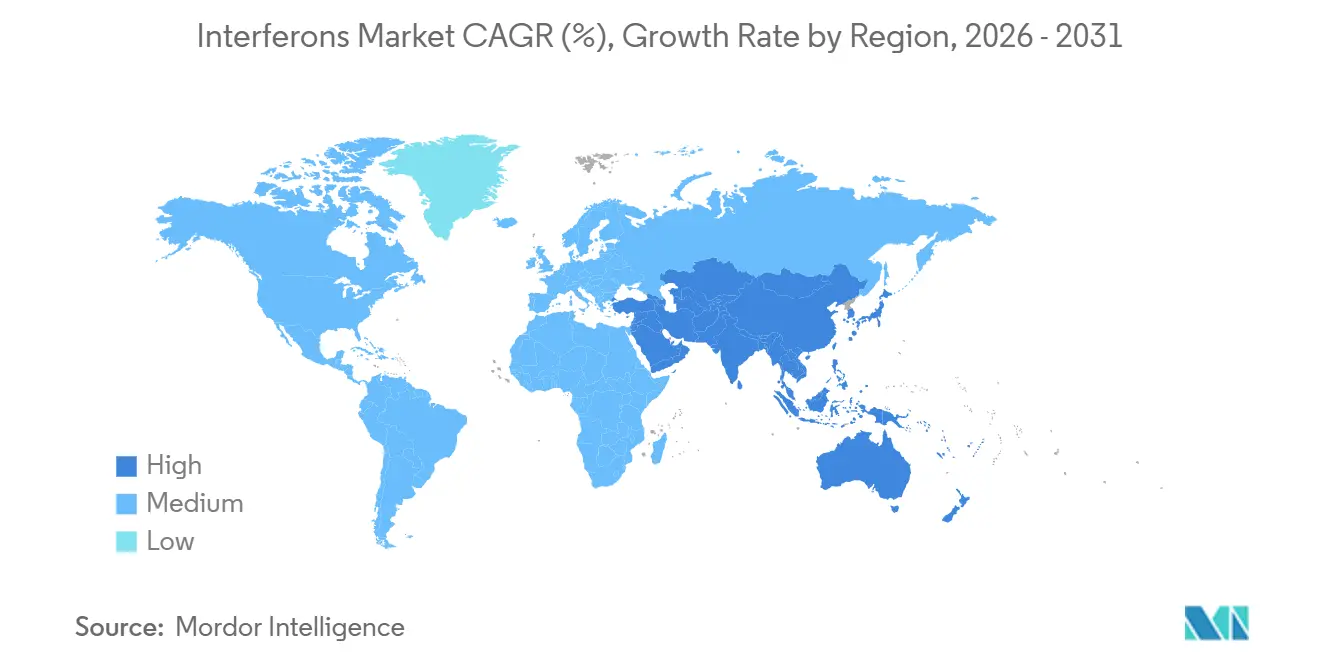

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

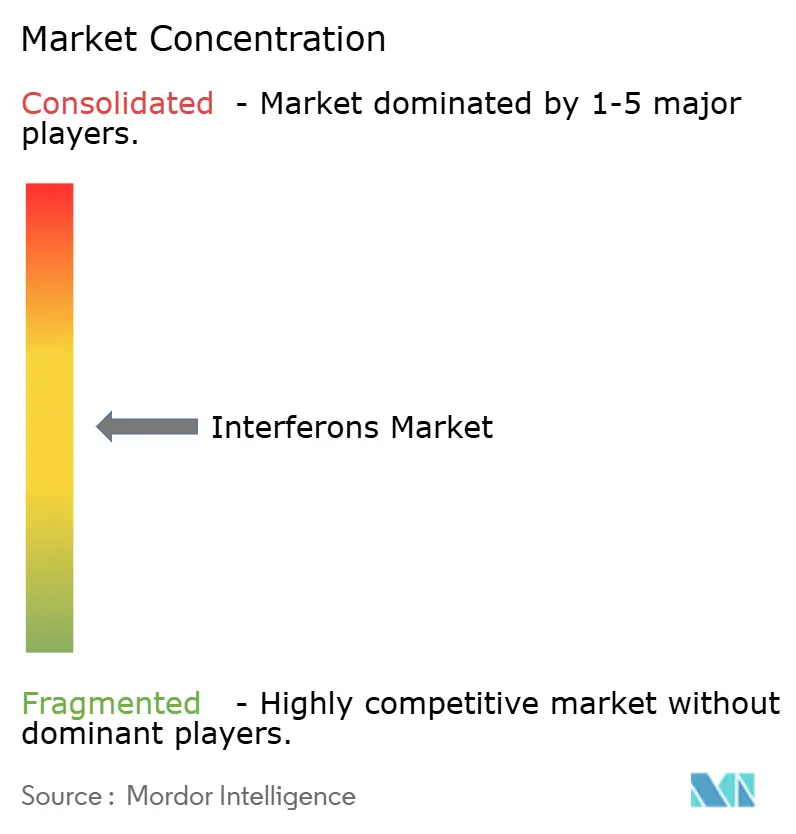

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interferons Market Analysis by Mordor Intelligence

The Interferons Market size is expected to increase from USD 10.11 billion in 2025 to USD 10.62 billion in 2026 and reach USD 13.42 billion by 2031, growing at a CAGR of 4.79% over 2026-2031.

The headline growth conceals a structural realignment: injectable interferon-α demand for hepatitis C has almost vanished, yet long-acting fusion proteins and intranasal prophylactics are opening new emergency-preparedness niches. Steady multiple-sclerosis prescribing of interferon-β, rising biosimilar penetration in price-sensitive regions, and fast-tracked oncology approvals for ropeginterferon alfa-2b underpin the market’s resilience. Meanwhile, cost-optimized manufacturing in India and China is expanding patient access, albeit at tighter margins, and government stockpiling of intranasal formulations for future respiratory outbreaks is emerging as a supplementary revenue stream.

Key Report Takeaways

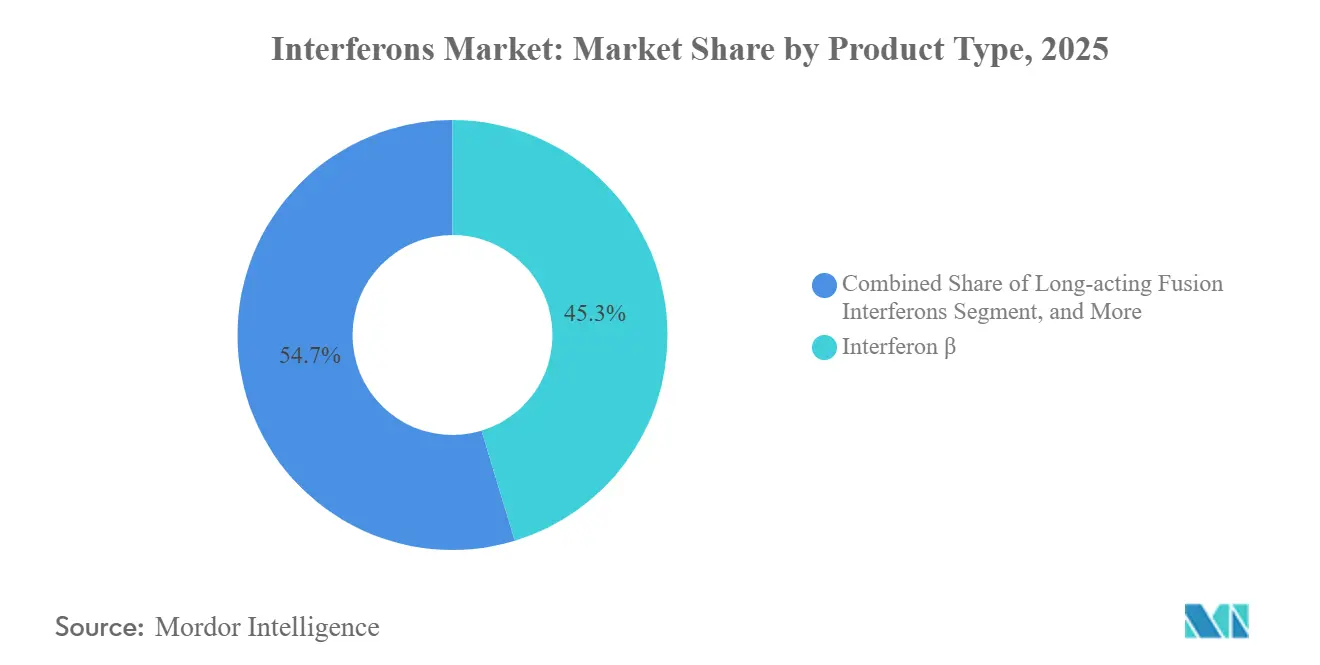

- By product type, interferon-β held 45.31% of the interferons market share in 2025, while long-acting fusion interferons are forecast to expand at a 7.02% CAGR through 2031.

- By application, multiple sclerosis accounted for 36.63% of the interferon market size in 2025, whereas emerging viral diseases are projected to advance at a 7.48% CAGR through 2031.

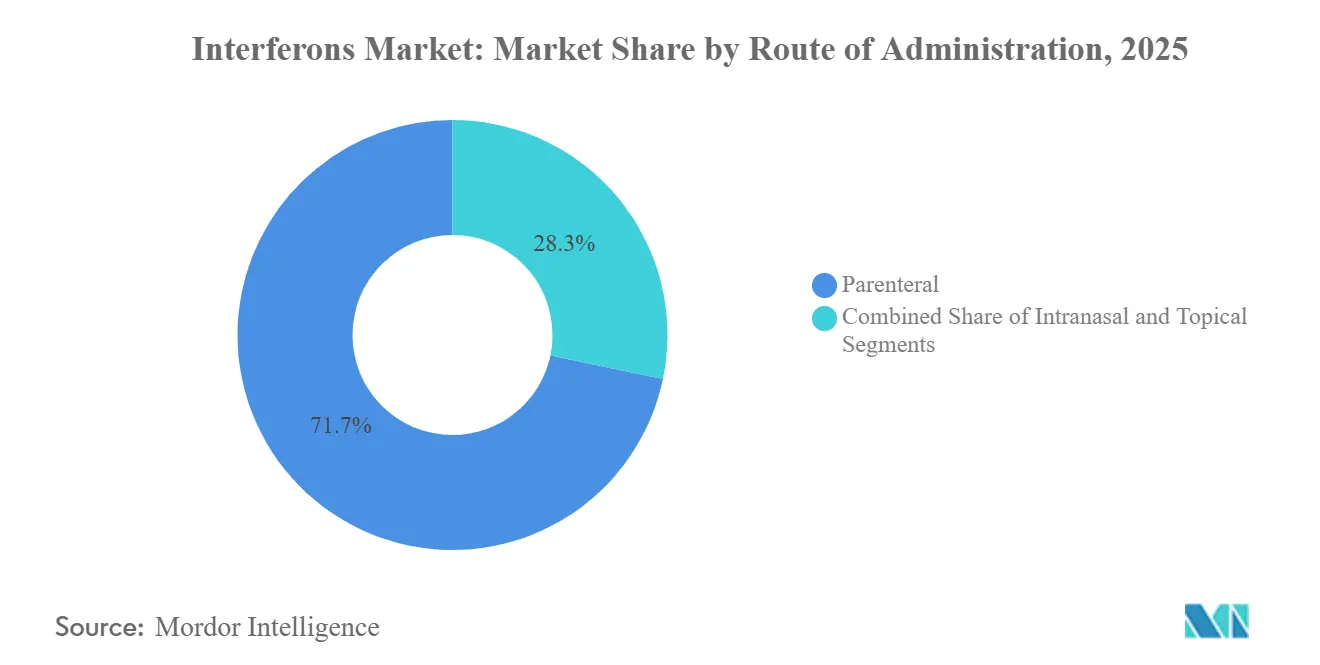

- By route of administration, parenteral products accounted for 71.72% of the interferon market size in 2025; intranasal delivery is projected to rise at a 6.13% CAGR.

- By end-user, hospitals generated 58.36% of 2025 revenue; home-care settings are posting the fastest 8.85% CAGR through 2031.

- By geography, North America led the interferon market share with 41.26% in 2025; however, the Asia-Pacific region is projected to grow at an 8.04% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Interferons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic viral infections | +0.8% | Asia-Pacific core, spill-over to Sub-Saharan Africa and Latin America | Long term (≥ 4 years) |

| Growing multiple-sclerosis patient pool using IFN-β first-line | +0.6% | North America & EU, emerging adoption in Middle East | Medium term (2-4 years) |

| Wider adoption of cost-saving biosimilar interferons | +1.2% | Global, concentrated in India, China, Brazil, CIS | Short term (≤ 2 years) |

| Expanding oncology pipeline using interferon-based immunotherapy | +0.5% | North America & EU, clinical trial activity in Japan and South Korea | Long term (≥ 4 years) |

| Intranasal interferon for pandemic respiratory threats | +0.7% | Global, early stockpiling in high-income countries | Medium term (2-4 years) |

| Long-acting fusion-protein interferons in late-stage R&D | +0.9% | North America & EU, licensing interest in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Viral Infections

Chronic hepatitis B affects an estimated 296 million carriers worldwide, with the highest burden concentrated in China and India.[1]World Health Organization, “Hepatitis B Fact Sheet,” WHO, who.intPeginterferon offers a finite 48-week regimen and achieves hepatitis B surface antigen loss in 3-7% of treatment-naive adults, outperforming the <1% rate associated with indefinite nucleos(t)ide analogue therapy. Combination trials pairing peginterferon with small-interfering RNA agents such as elebsiran achieved 21-33% antigen clearance, tripling monotherapy outcomes and renewing payer interest in interferon-based regimens. Domestic biosimilar producers in India and China undercut originator prices by up to 40%, enlarging eligible populations despite lower unit margins. Parallel research on dengue, mpox, and other expanding arboviruses highlights the broad antiviral utility of interferons, reinforcing their inclusion in national pandemic-preparedness stockpiles even before full commercial approval.

Growing Multiple-Sclerosis Patient Pool Using IFN-β First-Line

International guidelines continue to recommend interferon-β as a first-line option for patients with relapsing-remitting multiple sclerosis and low disease activity, or those with contraindications to higher-efficacy monoclonal antibodies. Although U.S. prescriptions declined as clinicians switched to ocrelizumab and BTK inhibitors, the global diagnosed MS population is expanding, particularly in the Middle East, where improved neurologic infrastructure is raising treatment rates. Pegylated interferon beta-1a (Plegridy), which extends injection intervals to every two weeks, preserves adherence in risk-averse cohorts until patent expiry in 2027, opening the door for biosimilars that will reset pricing across developed markets. Emerging MS centers in Saudi Arabia and Turkey are expected to leapfrog to these lower-cost alternatives, partly offsetting the erosion of North American revenue.

Wider Adoption of Cost-Saving Biosimilar Interferons

Price discounts of 15-35% in European tenders are enabling health ministries to treat 25-40% more patients within static budgets.[2]European Medicines Agency, “Biosimilar Medicines Overview,” ema.europa.euZydus Lifesciences’ acquisition of Agenus’s California biologics plants in 2025 signaled a strategic pivot toward FDA-compliant capacity that could introduce the first U.S. interferon biosimilar shortly after Plegridy’s patent cliff. Although pharmacy-benefit-manager rebate practices still favor originators, bipartisan pressure on drug costs is accelerating legislative proposals that would grant interchangeability designations to biosimilars with robust head-to-head data, a catalyst expected to compress North American prices by up to 30% over the next decade.

Expanding Oncology Pipeline Using Interferon-Based Immunotherapy

Ropeginterferon alfa-2b received FDA approval for the treatment of polycythemia vera, offering a once-monthly fusion protein that achieved significant reductions in JAK2V617F allele burden, an emerging molecular surrogate for event-free survival. Phase 3 enrollment in essential thrombocythemia reached 50% of target patients by mid-2024, buoyed by hematologists seeking non-cytotoxic cytoreduction strategies. Developers are now repurposing interferons for niche hematologic malignancies rather than competing head-on with checkpoint inhibitors in solid tumors. This focus promises modest but durable revenue streams under orphan-drug exclusivities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of DAAs displacing interferon in HCV | -1.4% | Global, complete displacement in high-income countries | Short term (≤ 2 years) |

| Flu-like adverse events lower treatment adherence | -0.6% | Worldwide, pronounced in oncology settings | Medium term (2-4 years) |

| Shortage of GMP-grade plasmid supply for recombinant IFN | -0.4% | North America & EU manufacturing hubs | Medium term (2-4 years) |

| Environmental concerns on pegylated IFN metabolites | -0.3% | EU & North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of DAAs Displacing Interferon in HCV

All-oral direct-acting antivirals achieve a sustained virologic response of greater than 95%, prompting the WHO and CDC to remove interferon-based regimens from their guidelines for hepatitis C.[3]Centers for Disease Control and Prevention, “Hepatitis C Treatment Guidelines,” cdc.gov The resulting USD 2–3 billion annual revenue loss between 2015 and 2023 shows how swiftly interferon sales can evaporate in the face of superior efficacy.

Flu-Like Adverse Events Lower Treatment Adherence

Injection-related fever, fatigue, and myalgia affect up to 60% of patients within 24 hours, driving discontinuation rates close to 20% in hepatitis B and multiple sclerosis cohorts. Pegylation reduces injection frequency, but not symptom severity, and even monthly ropeginterferon dosing leaves a tolerability gap relative to oral or targeted biologics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fusion Proteins Extend Dosing Intervals

Interferon-β dominated 2025 revenue with 45.31% interferon market share, but long-acting fusion proteins are accelerating at a 7.02% CAGR toward 2031. Ropeginterferon’s 78-hour half-life and monthly pen device support premium positioning for myeloproliferative neoplasms, while pegylated interferons remain the workhorse for finite-duration hepatitis B therapy. High-dose interferon-α in melanoma and renal cell carcinoma is being contracted, limited to centers that combine it with regional immunotherapies. Interferon-γ contributes negligible sales because its approved uses are restricted to rare pediatric immunodeficiencies.

Pipeline fusion constructs aim for half-lives exceeding 120 hours, potentially enabling quarterly maintenance dosing that repositions interferons as convenient options for chronic diseases. Developers pursuing albumin or hyFc scaffolds argue that reduced injection frequency will offset higher manufacturing costs. Whether HTA bodies will reimburse at premium price points hinges on real-world adherence gains and molecular-response surrogates proving long-term clinical benefit.

By Application: MS Dominance Erodes as Viral Preparedness Rises

Multiple sclerosis generated 36.63% of 2025 revenue, yet its share is inching downward as ocrelizumab and BTK inhibitors cannibalize first-line starts. In contrast, intranasal interferon stockpiling for future pandemics drives a 7.48% CAGR in the emerging-viral-disease segment. Hepatitis B remains a solid secondary pillar, thanks to peginterferon’s finite therapeutic window and superior functional cure probability.

Cancer indications are bifurcating: hematologists are embracing ropeginterferon for molecularly defined myeloproliferative neoplasms, while oncologists treating solid tumors continue to migrate to checkpoint inhibitors. The distinct trajectories illustrate how interferons retain relevance in niches where their broad immune activation complements targeted agents.

By Route of Administration: Mucosal Delivery Challenges Parenteral Dominance

Parenteral formats held 71.72% interferons market size in 2025, sustained by autoinjector upgrades that lowered injection-site-pain complaints by 30-40%. Nonetheless, intranasal candidates are attracting pandemic-preparedness funding and growing at 6.13% CAGR, propelled by once-daily prophylactic regimens that sidestep systemic cytokine toxicity. Topical and inhaled formats remain minor, with inhaled interferon-β failing to show clear survival benefits in mixed COVID-19 studies.

By End-User: Home-Care Gains as Autoinjectors Simplify Self-Administration

Hospitals represented 58.36% of 2025 sales, but payer site-of-care differentials, telemedicine onboarding, and improved pen-device usability are driving an 8.85% CAGR in home-care settings. Specialty clinics maintain a stable share by titrating doses and managing side effects, whereas academic centers contribute negligible direct revenue yet generate the clinical evidence needed for formulary adoption.

Geography Analysis

North America’s interferon market size, at 41.26%, remains the largest region in 2025, despite steady revenue contraction, with payer negotiations and impending biosimilar substitution expected to erode average selling prices by 20–25% after 2027. Europe follows a tender-driven procurement model that accelerates biosimilar turnover; originators maintain share primarily in Germany and Scandinavia, where physician loyalty and real-world evidence delay rapid switching. Asia-Pacific’s volume expansion, with a CAGR of 8.04% from 2026 to 2031, is driven by the hepatitis-B burden and cost-effective domestic manufacturing; however, fragmented provincial reimbursement in China moderates the pace of uptake. Emerging programs in Saudi Arabia, the United Arab Emirates, and Turkey are enhancing neurologic care infrastructure, increasing multiple sclerosis diagnosis rates, and providing a short-term boost to interferon-β uptake before next-generation oral therapies become dominant.

South America’s growth hinges on Brazil’s public tender cycles and Argentine biosimilar penetration. At the same time, Sub-Saharan Africa remains untapped mainly due to affordability constraints, although donor-funded procurement for viral outbreaks could catalyze sporadic spikes in demand. High-income Asia-Pacific markets, such as Japan and South Korea, enforce stringent biosimilar equivalence trials, which slow the introduction but ensure quality. Australia maintains niche use in hematology, with hospital groups favoring fusion proteins for myeloproliferative neoplasms under orphan-drug reimbursement pathways.

Competitive Landscape

Combined, Biogen, Roche, Merck, and AOP Orphan controlled a significant share of global revenue in 2025, signaling moderate concentration. Incumbents defend their share through patent-life extensions, such as Plegridy to 2027, and a Pegasys type-II variation in 2024, as well as by advancing long-acting fusion or intranasal formulations. Indian and Chinese manufacturers, including Zydus, Intas, and Anhui Anke, are expanding their FDA-ready facilities to challenge originators in regulated markets, a move expected to reduce U.S. interferon prices by up to one-third.

Strategic plays in 2025 included Zydus’s USD 75 million acquisition of Agenus’s California sites to accelerate biosimilar filings and CDMO contracts, as well as Merck’s purchase of Cidara Therapeutics to diversify its antiviral pipeline. Start-ups such as Kineta are advancing interferon-λ candidates that selectively activate epithelial immunity without systemic cytokine spikes; yet, these remain Phase 1 assets.

White-space opportunities lie in government procurement of intranasal interferons for respiratory-virus preparedness and in quarterly-dosing fusion constructs targeting chronic inflammatory diseases. Success in either avenue would shift technology differentiation from pegylation a commodity technique to advanced scaffold engineering, raising entry barriers for low-cost biosimilar producers.

Interferons Industry Leaders

Merck & Co.,Inc.

Biogen Inc

Bayer AG

Amega Biotech

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Merck agreed to acquire Cidara Therapeutics, adding a late-phase antiviral agent to its infectious-disease franchise.

- June 2025: Zydus Lifesciences purchased Agenus’s California biologics manufacturing sites for USD 75 million upfront and USD 50 million in milestones to pursue U.S. interferon biosimilar approvals.

- May 2024: Biogen announced the USD 1.15 billion acquisition of Human Immunology Biosciences, reallocating R&D capital from declining interferon revenue toward anti-CD38 immunology assets.

- August 2024: Pharmaand GmbH (pharma&) announced that the European Commission (EC) granted marketing authorization for a Type II variation of Pegasys (peginterferon alfa-2a). This authorization allows Pegasys to be used as a monotherapy treatment for adults diagnosed with polycythemia vera (PV) or essential thrombocythemia (ET).

Global Interferons Market Report Scope

As per the scope of the report, interferons are a class of proteins generated and released by the host cells against the presence of pathogenic microbes like bacteria, viruses, fungi, and tumor cells. Interferon proteins belong to a class of glycoproteins, namely cytokines, and are generally considered the first line of defense against microbial infections.

The interferons market is segmented by product type, application, and geography. By product type, the market is segmented as interferon alpha, interferon beta, and interferon gamma. By application, the market is segmented as hepatitis B, hepatitis C, melanoma, leukemia, multiple sclerosis, and renal cell carcinoma. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers market size and forecasts for the interferons market in value (USD) for the above segments.

| Interferon α |

| Interferon β |

| Interferon γ |

| Pegylated Interferons |

| Long-acting Fusion Interferons |

| Hepatitis B |

| Multiple Sclerosis |

| Melanoma |

| Leukemia |

| Renal Cell Carcinoma |

| Emerging Viral Diseases |

| Parenteral |

| Intranasal |

| Topical |

| Hospitals |

| Specialty Clinics |

| Home-care Settings |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Interferon α | |

| Interferon β | ||

| Interferon γ | ||

| Pegylated Interferons | ||

| Long-acting Fusion Interferons | ||

| By Application | Hepatitis B | |

| Multiple Sclerosis | ||

| Melanoma | ||

| Leukemia | ||

| Renal Cell Carcinoma | ||

| Emerging Viral Diseases | ||

| By Route of Administration | Parenteral | |

| Intranasal | ||

| Topical | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Home-care Settings | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What valuation and CAGR are forecast for global interferons through 2031?

Revenue is projected to rise from USD 10.62 billion in 2026 to USD 13.42 billion by 2031, implying a 4.79% CAGR.

Which therapy area currently contributes the most to interferon revenue?

Multiple sclerosis delivers the largest share, accounting for 36.63% of 2025 sales, owing to entrenched interferon-β first-line use.

How important is Asia-Pacific growth for interferon suppliers?

Asia-Pacific volumes are projected to expand at an 8.04% CAGR through 2031, driven by the prevalence of hepatitis B and cost-efficient biosimilar manufacturing in India and China.

Do long-acting fusion proteins meaningfully improve dosing schedules?

Yes, products such as ropeginterferon extend half-life to 78 hours, enabling once-monthly injections versus weekly or bi-weekly regimens for earlier pegylated versions.

How are intranasal interferons positioned for pandemic preparedness?

Phase 2 data showing 40% COVID-19 risk reduction in immunocompromised patients have spurred early government stockpiling, positioning nasal sprays as rapid-deploy prophylactics in future respiratory outbreaks.

Page last updated on: