Passive Electronic Components Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

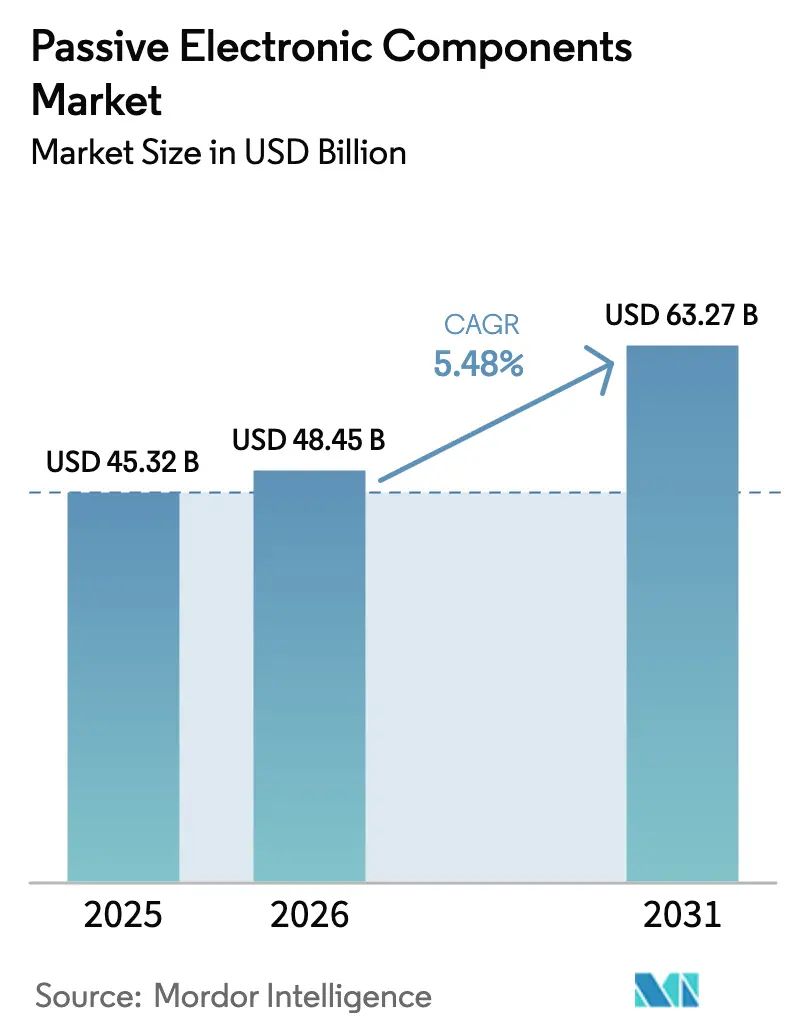

| Market Size (2026) | USD 48.45 Billion |

| Market Size (2031) | USD 63.27 Billion |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

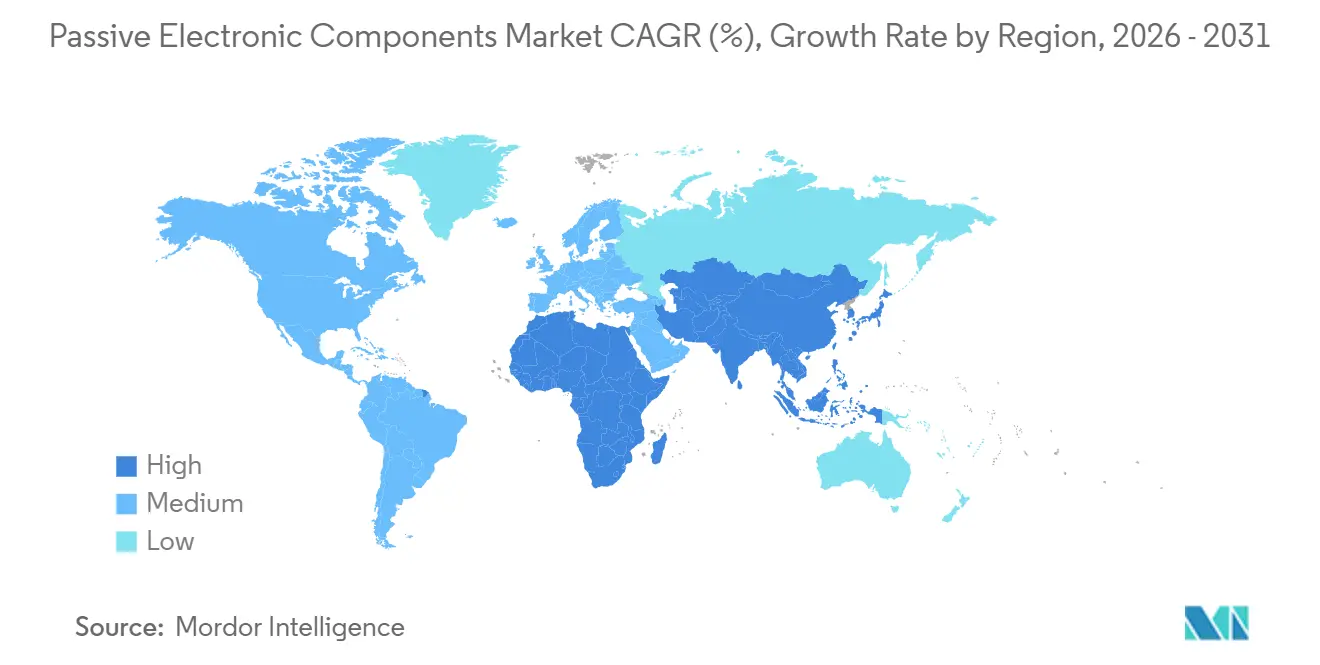

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passive Electronic Components Market Analysis by Mordor Intelligence

The passive electronic components market size was valued at USD 45.32 billion in 2025 and is estimated to grow from USD 48.45 billion in 2026 to reach USD 63.27 billion by 2031, at a CAGR of 5.48% during the forecast period (2026-2031). Expansion is led by electric-vehicle platforms that consume three to five times more capacitors, resistors, and inductors per unit than internal-combustion cars, while 5G and Wi-Fi 7 base-stations drive unprecedented demand for high-frequency filters. Equipment makers are embedding miniature passives in printed-circuit substrates to save board real estate, even as vertical integration into palladium and ruthenium supply dampens price shocks. Sovereign electronics programs in the Middle East, India, and Southeast Asia are regionalizing production, lowering logistics risk, and improving resiliency. Competitive focus has accordingly shifted from price wars to technology leadership, with leading suppliers patenting dielectrics that survive 260°C lead-free solder processes and integrating passives inside power-module packages for silicon-carbide inverters.

Key Report Takeaways

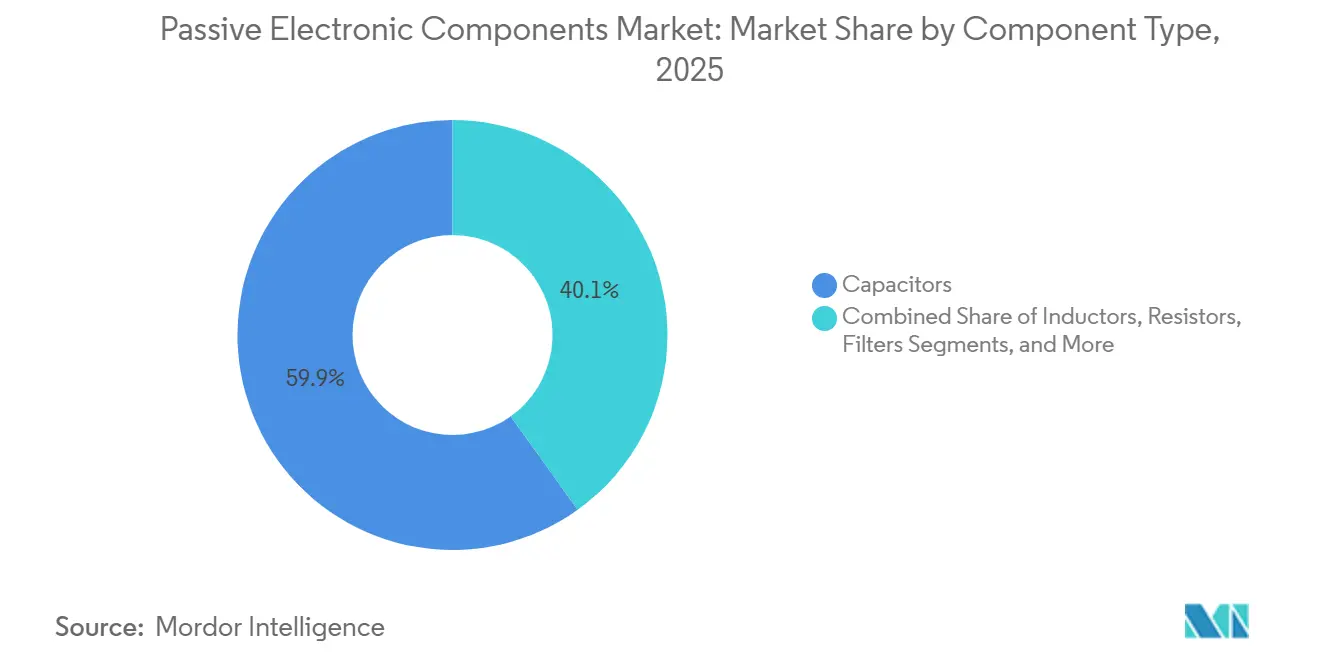

- By component type, capacitors accounted for 59.89% passive electronic components market share in 2025, while filters are expanding at an 8.23% CAGR through 2031.

- By capacitor product type, ceramic units led with 45.78% share of the passive electronic components market size in 2025; super capacitors are advancing at a 7.31% CAGR to 2031.

- By capacitor end-user industry, automotive captured 26.59% revenue share in 2025, yet energy applications are forecast to climb at a 7.02% CAGR.

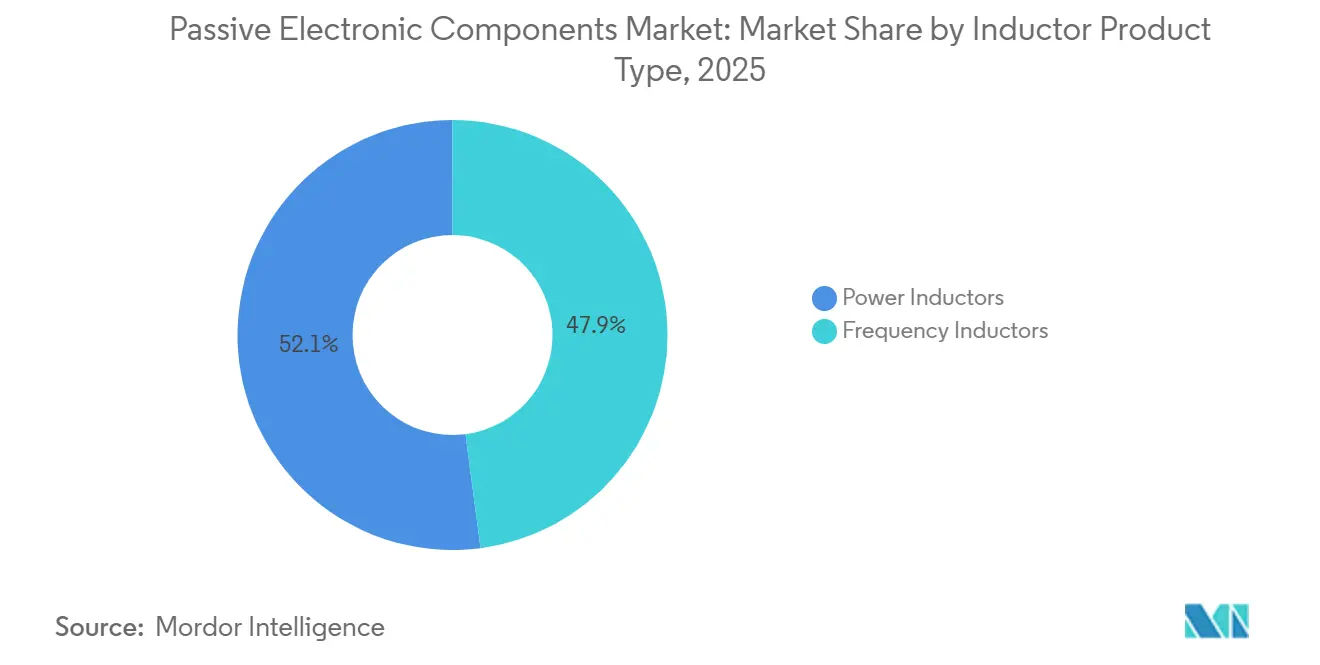

- By inductor product type, power inductors held 52.07% of revenue in 2025; RF inductors are set to record the quickest 6.82% CAGR by 2031.

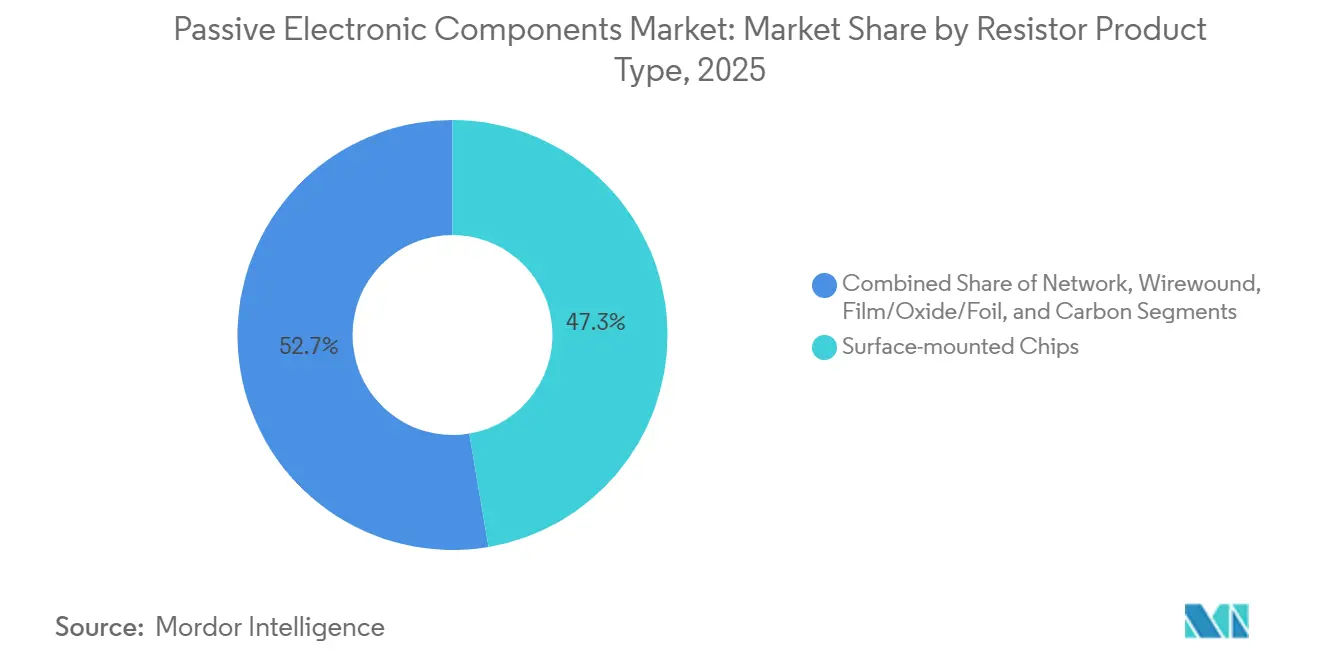

- By resistor product type, surface-mount chips commanded 47.32% share in 2025, whereas film, oxide, and foil devices are growing at a 6.03% CAGR.

- By geography, Asia Pacific contributed 36.12% of capacitor revenue in 2025, while the Middle East is expected to post a 6.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Passive Electronic Components Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in automotive electronics for electric and autonomous vehicles | +1.8% | China, Europe, North America | Medium term (2-4 years) |

| 5G rollout driving high-frequency passive component demand | +1.5% | Asia Pacific, North America | Short term (≤ 2 years) |

| Growing adoption of IoT devices requiring ultra-low-power passives | +1.2% | Asia Pacific, Europe | Medium term (2-4 years) |

| Vertical integration of materials supply to secure palladium and ruthenium | +0.7% | Japan, South Korea, Taiwan | Long term (≥ 4 years) |

| Emergence of embedded passive technology in PCB substrates | +0.9% | Asia Pacific, North America | Medium term (2-4 years) |

| Regionalization of electronics manufacturing to mitigate supply-chain risk | +1.0% | Southeast Asia, India, Mexico, Central Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Automotive Electronics for Electric and Autonomous Vehicles

Electric cars deploy up to 3,000 discrete passives, triple the count of legacy vehicles, because 800 V battery packs require high-ripple ceramic capacitors, current-sense resistors, and EMI filters. Battery-management systems alone integrate roughly 200 MLCCs per module, smoothing balancing currents to safeguard lithium-ion cells. Lidar and 77 GHz radar add inductors and temperature-stable capacitors that must meet minus-40 °C to plus-125 °C operating windows. Tesla reported an 18% rise in passive-component cost per vehicle in 2025, largely driven by these high-voltage upgrades.[1]Tesla Inc., “Annual Report 2025,” tesla.com Tier 1 suppliers are co-locating capacitor lines next to European and Chinese powertrain plants, cutting lead times from 12 to four weeks and freeing working capital.

5G Rollout Driving High-Frequency Passive Component Demand

Fifth-generation macro cells use spectrum above 3.5 GHz, where parasitics in conventional passives induce insertion loss. Massive-MIMO panels pack 64-256 radiators and need capacitors with self-resonant frequencies beyond 10 GHz. Global 5G standalone sites reached 1.2 million by end-2025, with China and South Korea hosting 60% of deployments.[2]GSMA, “Mobile Economy Report 2025,” gsma.com Each radio consumes roughly 400 passives, including RF inductors tuned for gigahertz operation. Ericsson documented a 25% weight cut in its mid-band radios by miniaturizing these passives, enabling lighter rooftop installs.[3]Ericsson, “Sustainability Report 2025,” ericsson.com Only a handful of vendors can sinter ferrite cores that keep permeability stable across temperature and humidity extremes.

Growing Adoption of IoT Devices Requiring Ultra-Low-Power Passives

Industrial sensors, smart agriculture nodes, and remote health monitors must survive years on coin cells, pushing vendors to design capacitors and inductors with leakage under 1 nA. Cellular IoT connections surpassed 3 billion in 2025, with agriculture and logistics the fastest adopters. Devices endure minus-40 °C to plus-85 °C swings and >90% humidity, which accelerates electromigration if terminations are not corrosion-proof. Manufacturers are applying conformal coatings to extend life beyond 10 years, a must for smart meters and pipeline monitors. Vishay noted that thin-film resistors originally tailored for engine-control units now appear in IoT gateways because they drift less than 0.1% over a decade.

Emergence of Embedded Passive Technology in PCB Substrates

Embedding resistors and capacitors inside PCB dielectric cuts board area 30% and shortens return paths, improving signal integrity. AT and S disclosed that embedded substrates represented 15% of 2025 HDI revenue, nearly double 2024 levels.[4]AT and S, “Annual Report 2025,” ats.net The method relies on sputter deposition and laser trimming, demanding USD 50 million per line in capital. Intel patented die-bump embedded decoupling capacitors that drop power-delivery impedance 40%, allowing clock speeds above 6 GHz without voltage droop. While cost-effective for sub-100 nF values, embedded passives lock customers to a single PCB supplier, raising switching costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in precious metal prices impacting capacitor costs | -0.9% | Japan, South Korea, Taiwan | Short term (≤ 2 years) |

| Miniaturization limits for high-capacitance components | -0.6% | Global, most binding in consumer electronics | Medium term (2-4 years) |

| Environmental regulations on tantalum and lead usage | -0.5% | Europe, North America, Asia Pacific | Long term (≥ 4 years) |

| Talent shortages in high-frequency RF design expertise | -0.4% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Precious Metal Prices Impacting Capacitor Costs

Palladium traded between USD 900 and USD 1,400 per troy ounce during 2025, making MLCC margins swing up to 5 percentage points for suppliers without hedging. Ruthenium spiked 40% in early-2025 as Russian export curbs tightened availability, forcing reformulation of electrode pastes that sacrifice capacitance density. TDK said precious-metal inflation trimmed its capacitor margin by 150 basis points in fiscal 2025 and triggered repricing with auto and industrial buyers. Small vendors lacking scale faced steeper hits, accelerating sector consolidation.

Miniaturization Limits for High-Capacitance Components

Dielectric thickness in MLCCs has shrunk to 0.5 µm, but going thinner triggers quantum tunneling and breakdown. Murata calculated that an 0201 package holding 22 µF would require 1,000 layers, a yield-killer that makes the part uneconomic. Designers are instead stacking lower-capacitance chips or adopting polymer hybrids for high bulk energy in slim footprints. Apple’s iPhone 16 combined ceramic and tantalum arrays to bypass this ceiling, albeit at higher bill-of-materials complexity.[5]Apple Inc., “Supplier Responsibility Report 2025,” apple.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Capacitors Anchor Market, Filters Surge on RF Demand

In 2025 capacitors commanded 59.89% revenue in the passive electronic components market, validating their universality for power conditioning across automotive, industrial, and consumer gear. Filters, although smaller in base, will expand at an 8.23% CAGR to 2031 as every 5G handset now integrates up to 40 acoustic filters to isolate Wi-Fi 6E, Bluetooth, ultra-wideband, and 5G signals. Inductors underpin power converters, while resistors set currents and divide voltages in all circuits.

Embedded technology is redrawing category boundaries. Substrates hosting thin-film resistors and capacitors trim z-height for smartphones, but values above 100 nF still mandate discrete devices for energy storage. As a result the passive electronic components market size for discrete capacitors in automotive and industrial domains is expected to remain dominant, even as signal-chain-centric filters continue to seize incremental share in handsets and base stations.

By Capacitor Product Type: Ceramic Dominance Meets Super Capacitor Momentum

Ceramic units delivered 45.78% of capacitor sales in 2025, benefiting from wide capacitance range, low ESR, and high frequency response. Super capacitors are set to post a 7.31% CAGR, supported by regenerative braking and grid-frequency regulation where their rapid charge-discharge cycles excel.

While tantalum and aluminum electrolytic devices continue in aerospace and industrial drives, suppliers are blending film and ceramic dielectrics to reach 1,000 V ratings in 800 V EV onboard chargers. This mix ensures the passive electronic components market size attached to high-voltage EV blocks keeps growing despite overall smartphone maturity.

By Capacitor End User Industry: Automotive Leads, Energy Accelerates

Automotive absorbed 26.59% of capacitor demand in 2025 in the passive electronic components market. Energy generation and storage will climb at a 7.02% CAGR through 2031 as photovoltaic inverters and wind turbines adopt film capacitors capable of enduring kilovolt surges.

Industrial machinery, aerospace, and medical devices keep requiring rugged or biocompatible units, yet consumer electronics continues to ship volume in the tens of billions of pieces. Segment focus is therefore tilting from pure volume to application diversity, preserving passive electronic components industry profitability.

By Inductor Product Type: Power Inductors Lead, RF Variants Gain

Power inductors contributed 52.07% of inductor revenue in 2025 thanks to buck and boost converters feeding CPUs and battery chargers. Frequency inductors, though only a quarter of segment value, are expected to expand at 6.82% CAGR as mid-band 5G and sat-com terminals proliferate.

Automotive 48 V mild hybrids and LED lighting require shielded inductors above 20 A saturation, whereas data-center AI accelerators need tight-tolerance RF coils for multi-gigahertz filters. Vendors refining ferrite powder to sustain permeability at these frequencies will capture the next wave of passive electronic components market growth.

By Inductor End User Industry: Automotive Dominates, Comms Surge

Automotive claimed 28.61% of inductor spend in 2025, driven by distributed DC-DC converters within EVs. Communications, servers, and storage will log a 6.47% CAGR to 2031 as AI clusters deploy hundreds of power stages per board.

Aerospace and defense need radiation-tolerant magnetics, while industrial motor drives rely on high-current chokes. Top players therefore pair automotive AEC-Q200 certification with customization services for rugged verticals, insulating margins even as smartphone volumes plateau.

By Resistor Product Type: Surface-Mount Chips Prevail, Film Variants Rise

Thick-film chip resistors held a 47.32% share in 2025, serving in everything from voltage dividers to pull-ups. Film, oxide, and foil parts will outpace at 6.03% CAGR because medical, aerospace, and instrumentation equipment demand temperature coefficients under 25 ppm/°C.

Wirewound units continue in dynamic braking and load banks, while resistor networks simplify LED backlighting. The passive electronic components market size devoted to precision film and foil devices therefore expands as analog-heavy applications seek sub-0.1% drift over life.

By Resistor End User Industry: Consumer Electronics Lead, Energy Grows

Smartphones, laptops, and consoles absorbed 27.47% of resistor revenue in 2025. Solar and wind inverters will be the quickest riser at 6.43% CAGR through 2031 as renovables install megawatt-scale power blocks.

Automotive EVs need current-sense chips up to 5 W in 2512 footprints, while medical imaging requires ultra-stable resistors in gradient amplifiers. These specialized niches reinforce the passive electronic components industry pivot from commoditized consumer volumes to high-value sectors.

Geography Analysis

Asia Pacific accounted for 36.12% of capacitor sales in 2025 and remains the anchor of the passive electronic components market thanks to deep manufacturing clusters in China, Japan, South Korea, and Taiwan. Regional governments subsidize next-generation dielectric research and provide tax incentives for capacity expansion, allowing suppliers to co-locate with smartphone, PC, and EV final-assembly hubs.

Middle East demand, although just mid-single-digit share, is expanding at 6.76% CAGR through 2031 under sovereign initiatives that fund semiconductor fabs, data centers, and solar farms. Abu Dhabi and Riyadh allocate multi-billion-dollar budgets to localize passive assembly, insulating critical telecom and power infrastructure from foreign supply disruptions.

North America and Europe represent mature yet resilient markets. Vehicle electrification, edge computing, and industrial automation sustain component pull, while environmental regulations push adoption of lead-free and tantalum-free designs. Mexico, the Czech Republic, and Poland capitalize on reshoring trends, attracting new MLCC and chip-resistor lines to shorten logistics for U.S. and German OEMs.

Regulatory Landscape

Environmental and materials-compliance rules continue to shape passive-component design and qualification, particularly for automotive and industrial electronics that must maintain high reliability under lead-free assembly. In the EU, the RoHS Directive remains a core constraint for solders, terminations, and legacy high-reliability use cases, with RoHS Annex III exemption updates and expiries moving through Commission delegated acts in 2025. These changes include time-bound allowances that affect lead content in specific component applications through the 2026 timeframe.

Trade and industrial policy adds further compliance work for globally distributed supply chains. In the United States, tariff policy changes under Section 232 altered how duties are calculated for covered electronics categories, shifting valuation mechanics to a full entered-value approach effective April 6, 2026. That raises the need for accurate HTS classification and supporting documentation for imported electronic parts and assemblies that embed passives.

Value Chain Analysis

The value chain starts upstream with mined and refined metals (notably palladium and ruthenium for electrodes and thick-film pastes, plus copper and aluminum for foils and terminations) and engineered materials such as dielectric powders and ferrite core materials. Material synthesis and specialized process know-how remain concentrated in established hubs, with Japan prominent in upstream materials and equipment ecosystems supporting multilayer ceramics, thin/thick films, and high-voltage capacitor constructions.

Midstream manufacturing covers high-volume MLCCs, chip resistors, and inductors, with production concentrated across Japan, Taiwan, China, and other Asia manufacturing bases, along with selected nearshoring capacity to serve North America and Europe. Downstream, authorized distributors and direct OEM/Tier-1 supply agreements manage allocation and lifecycle support, while lead-time and inventory swings keep showing up as recurring friction points. Industry monitoring flagged inventories for key passive categories at 12-month lows in February 2025, and companies responded through capacity additions and process upgrades, including Nichicon completing a JPY 7.6 billion fiscal-2025 investment to expand aluminum electrolytic and EV film capacitor capacity.

Competitive Landscape

The top five suppliers, Murata, TDK, Yageo, Samsung Electro-Mechanics, and Kyocera, command roughly 45% of 2025 revenue, yielding a moderately concentrated structure where scale and patent portfolios matter. These leaders pour capex into sintering furnaces that deposit sub-micron dielectrics, pushing capacitance density beyond rivals.

Murata filed 47 MLCC material patents in 2024 and will add 15% more capacity via a USD 670 million Fukui line that starts in 2026.[6]Murata Manufacturing, “Technical Symposium Presentation 2024,” murata.com TDK teams with Infineon to embed passives inside silicon-carbide modules, a move that elevates switching frequency to 100 kHz and erodes the value of discrete inductors. Yageo’s 2025 purchase of a Malaysian plant adds 8 billion MLCCs per month, diversifying production away from earthquake-prone Taiwan.[7]Yageo Corporation, “Annual Report 2025,” yageo.com

Disruptors like Fenghua and Torch edge into consumer applications through government subsidies, yet they struggle to secure AEC-Q200 qualification for automotive sockets. Raw-material volatility further narrows margins for second-tier players lacking long-term palladium contracts. Consolidation is thus expected to continue as niche capacitor and resistor makers seek scale or exit.

Passive Electronic Components Industry Leaders

Panasonic Corporation

TDK Corporation

Vishay Intertechnology Inc.

Murata Manufacturing Co. Ltd

Yageo Corporation (KEMET)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Demand for high-specification passives for AI servers, high-voltage power conversion, and embedded or miniaturized architectures is bringing targeted capacity and material investment, creating more room beyond commodity MLCCs and general-purpose chip resistors. Several 2026 programs reflect this shift: Holy Stone Enterprise announced a NT$3 billion (about USD 94 million) investment in March 2026 to add a production line at its Hokkaido R&D center and expand capacity at its Yilan Lize site in Taiwan for AI power-supply MLCCs. Kyocera also announced in July 2026 a JPY 100 billion multi-year investment plan (through fiscal year ending March 2031) to expand high-end MLCC capacity at its Kokubu site in Kagoshima, Japan.

Materials and package-level integration also create monetizable gaps where stability at high temperature, high ripple current, and high frequency is critical. In July 2026, Ishihara Sangyo disclosed plans to double titanium dioxide output at its Yokkaichi plant to support ceramic-capacitor demand tied to AI servers, which underscores scaling focused on MLCC dielectrics. In parallel, automotive-grade qualification (AEC-Q200) and embedded-passive adoption in PCB substrates are pushing suppliers toward application-specific offerings and more co-design engagement with OEMs and substrate manufacturers, supporting differentiated portfolios for high-reliability and high-density builds.

Recent Industry Developments

- June 2026: Murata introduced the GCJ21BD72A225KE02, a 2.2 uF/100Vdc soft-termination chip MLCC for automotive applications, expanding the company's high-voltage offering in compact 0805 case size. The soft-termination structure targets mechanical stress robustness on vehicle PCBs, supporting higher reliability in power and ADAS-related circuits.

- May 2025: TDK released a new passive-component product update through its news center, reflecting ongoing portfolio refresh cycles tied to miniaturization and performance upgrades for high-density electronics. The launch cadence supports faster design-in for OEMs dealing with tighter board area and higher switching frequencies across consumer and industrial platforms.

- February 2024: Panasonic announced a new capacitor-related product initiative via its global newsroom, reinforcing continued development of power-conditioning components used across computing, industrial electronics, and emerging fast-charging specifications. Product-line updates at major tier-1 suppliers help broaden sourcing options for OEMs managing qualification and lifecycle risks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated from passive electronic components used to control, store, or filter electrical signals in electronic circuits, across major end-use industries and regions.

Scope exclusions: We exclude active components and optoelectronics, and we also exclude pure assembly services that do not include a component sale.

Segmentation Overview

- By Component Type

- Capacitors

- Product Type

- Ceramic Capacitors

- Tantalum Capacitors

- Aluminum Electrolytic Capacitors

- Paper and Plastic Film Capacitors

- Super Capacitors

- By End User Industry

- Automotive

- Industrial

- Aerospace and Defense

- Consumer Electronics and Computing

- Communications/Servers/Data Storage

- Energy

- Medical

- By Geography

- North America

- Europe

- Asia-Pacific

- Rest of World

- Product Type

- Inductors

- By Product Type

- Power Inductors

- Frequency Inductors

- By End User Industry

- Automotive

- Aerospace and Defense

- Consumer Electronics and Computing

- Communications/Servers/Data Storage

- Other End User Industries

- By Geography

- North America

- Europe

- Asia-Pacific

- Rest of World

- By Product Type

- Resistors

- By Product Type

- Surface-mounted Chips

- Network

- Wirewound

- Film/Oxide/Foil

- Carbon

- By End User Industry

- Automotive

- Aerospace and Defense

- Consumer Electronics and Computing

- Communications/Servers/Data Storage

- Other End User Industries

- By Geography

- North America

- Europe

- Asia-Pacific

- Rest of World

- By Product Type

- Filters and Other Components

- By End User Industry

- Automotive

- Aerospace and Defense

- Consumer Electronics and Computing

- Communications/Servers/Data Storage

- Other End User Industries

- By Geography

- North America

- Europe

- Asia Pacific

- Rest of World

- By End User Industry

- Capacitors

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market context and to anchor the model to observable electronics demand indicators. We reviewed public technical and trade references such as IPC publications on PCB and electronics manufacturing trends, JEDEC standards references, IEEE journals for component technology shifts, and USITC trade data for related component flows. We also used government statistics and macro indicators (such as industrial production and electronics export series) to understand cycle timing.

On the supply side, we relied on company annual reports, investor presentations, and earnings call transcripts to interpret product mix changes, utilization commentary, and pricing language that influences average selling price paths. Patent databases were also used selectively to track where miniaturization, high-frequency filtering, and new dielectric materials were moving from R&D into commercial designs. The sources listed here are illustrative only, and we reviewed many other public documents and datasets to cross-check inputs and clarify where category boundaries could shift.

Primary Interviews and Surveys

Primary work focused on validating how demand is forming across core end markets, and on confirming how pricing and lead times are behaving for major passive categories. We spoke with a balanced mix of component ecosystem participants, including manufacturers, distributors, EMS firms, and large OEM buying teams, and we covered APAC, EMEA, and the Americas. Follow-up calls were then used to close gaps in assumptions that were not fully verifiable from public sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 41% |

| Mid tier: 50% | Functional/Unit leaders: 23% | EMEA: 36% |

| Smaller Players: 18% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where electronics production and end-market build plans were converted into a demand pool for passives, and then translated into value using category-level pricing logic. The model was subsequently checked using selective bottom-up approximations, such as sampled shipment volumes and price ranges for key categories, plus channel discussions on mix shifts, and then totals were adjusted when large gaps appeared.

A few practical inputs guided the model, including automotive and industrial electronics output trends, consumer device shipment cycles, data center and communications equipment build rates, and the typical content intensity of passives in high-frequency and power-management designs. We used lead-time direction and substitution patterns (for example, changes between capacitor types used in the same circuit function) as sanity checks for the volume and ASP curves. Forecasts were produced using scenario analysis, since the market is sensitive to macro cycles and inventory corrections, and the final path was selected after primary respondents aligned on the most likely demand normalization timeline. When bottom-up views were incomplete for niche filters or smaller subcategories, gaps were handled through ratio-based allocation tied to the better-tracked core groups and then rechecked against end-use demand signals.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final number is not driven by one data series or a single assumption. We compare model totals against independent signals such as end-market shipment trends, trade directionality, and company-reported revenue mix, and then review any unusual jumps in pricing or demand share before sign-off.

If a variance is large, analysts re-contact relevant respondents and revisit the driver that caused the movement, such as a sudden change in lead times or a revised end-market build plan. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is performed so clients receive the latest updated view.

Mordor Intelligence's Passive Electronic Components Market Size Measured Against Other Published Estimates

Published market values for passive electronic components can look far apart because not everyone counts the same component set, and the timing of the cycle can be captured differently. Differences also show up when pricing is treated as a flat assumption instead of being linked to mix shifts across capacitor types and other passives.

Some external figures focus only on the three core groups, or they anchor the base year to an earlier demand trough or peak, which changes the starting point even before forecast assumptions are applied. In the Mordor Intelligence model, the scope is expanded to include filters and other passive components alongside capacitors, inductors, and resistors, and the year-2026 value is tied to end-use demand signals that were rechecked through interviews and cycle indicators.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 48.45 B (2026) | |

| Industry Association A | USD 39.00 B (2023) | Covers only the three core passive groups (capacitors, resistors, and inductors) and is stated as a TAM for a fiscal-year view, which can exclude adjacent passive categories and shift timing versus a calendar-year market model. |

| Trade Journal B | USD 40.28 B (2025) | Uses a different base year and a longer-dated outlook, and the scope and pricing build are not transparent, which can understate the effect of mix-driven ASP changes and inventory-cycle normalization in the near term. |

Across the table, the spread is mainly explained by what is included in the component basket and which year is treated as the starting point of the cycle. When scope is clearly stated and demand signals are used to test pricing and volume direction, the resulting market value is easier to reproduce and to track over time for planning decisions.

Key Questions Answered in the Report

What is the current value of the passive electronic components market?

The passive electronic components market size is USD 48.45 billion in 2026 and is forecast to reach USD 63.27 billion by 2031.

Which component category dominates revenue today?

Capacitors command 59.89% of revenue in 2025, making them the largest component segment.

Which product type is growing fastest within capacitors?

Super capacitors are expanding at a 7.31% CAGR through 2031, fueled by regenerative braking and grid-frequency regulation.

How will 5G affect demand for passive parts?

Each 5G base station consumes about 400 passives, lifting high-frequency filter and inductor sales over the next two years.

Which region is the quickest-growing geography?

The Middle East is projected to post a 6.76% CAGR through 2031 thanks to sovereign investments in data centers and renewable energy.

Who are the leading suppliers?

Murata, TDK, Yageo, Samsung Electro-Mechanics, and Kyocera collectively hold around 45% of 2025 revenue.

Page last updated on: