USB Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

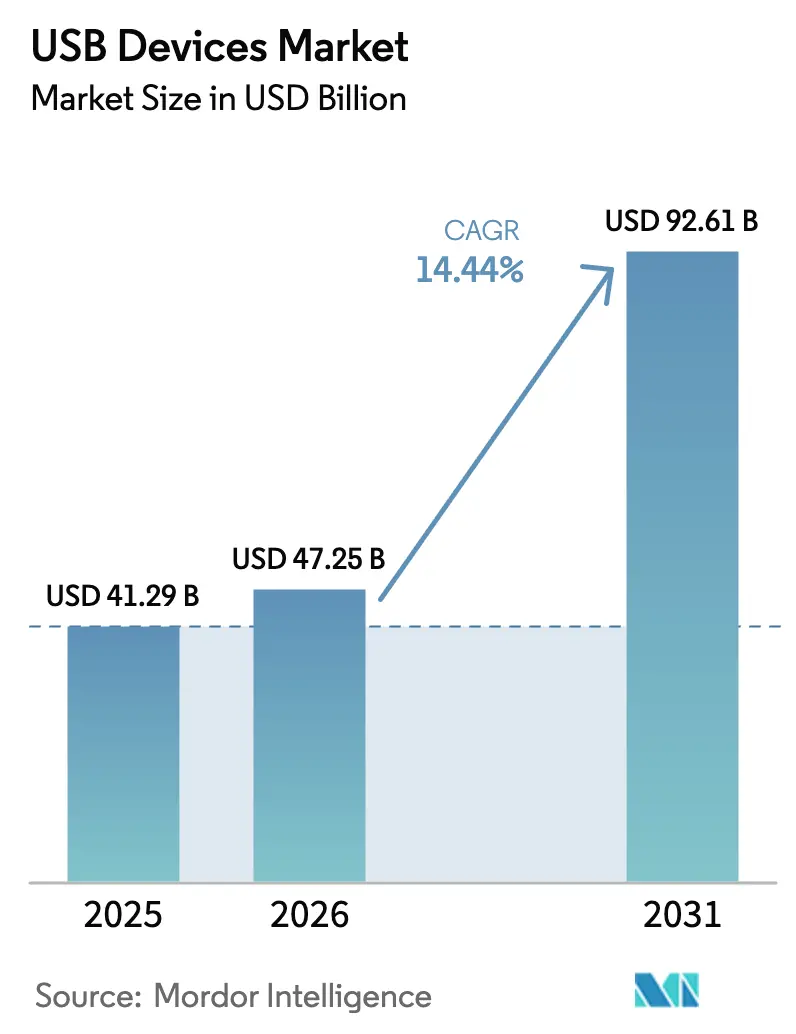

| Market Size (2026) | USD 47.25 Billion |

| Market Size (2031) | USD 92.61 Billion |

| Growth Rate (2026 - 2031) | 14.44% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

USB Devices Market Analysis by Mordor Intelligence

USB devices market size in 2026 is estimated at USD 47.25 billion, growing from 2025 value of USD 41.29 billion with 2031 projections showing USD 92.61 billion, growing at 14.44% CAGR over 2026-2031. Growth momentum reflects intertwined regulatory action, technology upgrades, and evolving usage patterns that favor the USB-C interface. Mandatory common-charger rules in the European Union and India accelerate connector consolidation, while the roll-out of USB4 enables single-cable solutions delivering 40 Gbps data and up to 240 W power. Automotive infotainment systems add further impetus as in-vehicle ports exceed 45 W to fast-charge tablets on road trips. Supply-side resilience is strengthening because memory and controller vendors are investing heavily in additional capacity, even as lingering shortages keep average selling prices firm. Competitive intensity remains moderate, giving scale players time to realign portfolios around high-speed, high-power products.

Key Report Takeaways

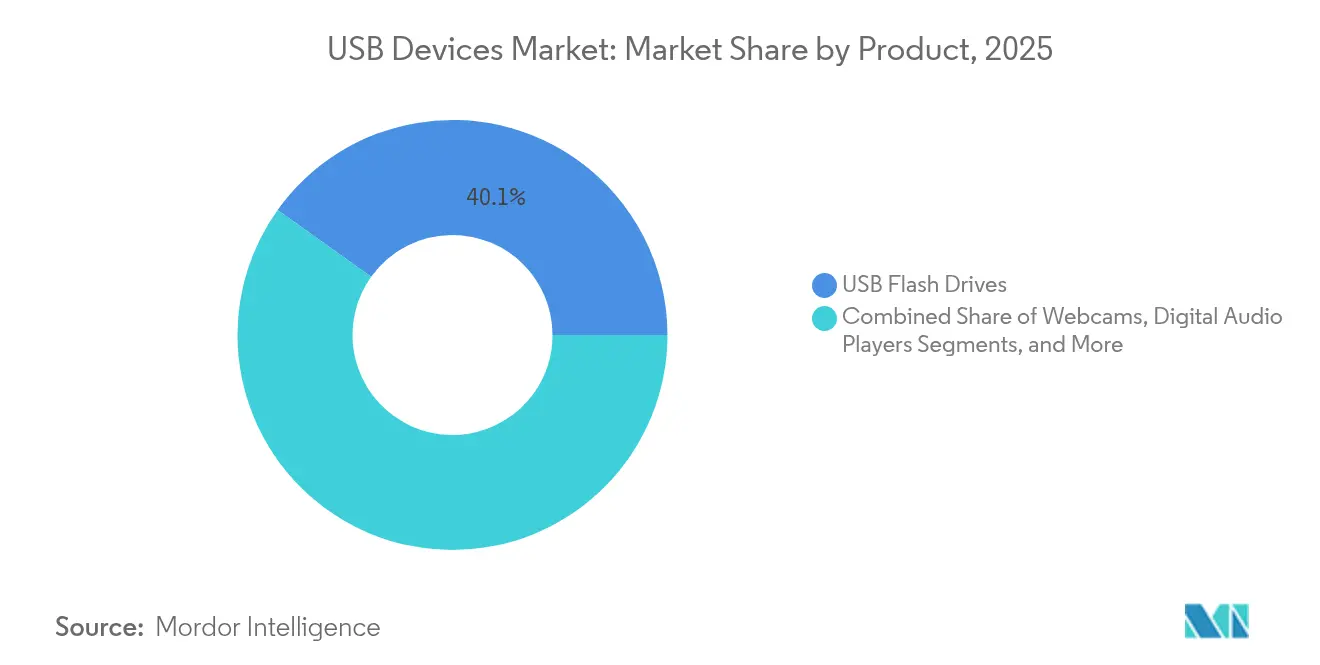

- By product category, USB flash drives led with 40.12% of USB devices market share in 2025, whereas hubs and docks are forecast to expand at a 15.08% CAGR to 2031.

- By device standard, USB 3.x held 54.35% revenue share in 2025; USB4 is expected to post the fastest growth at 15.72% through 2031.

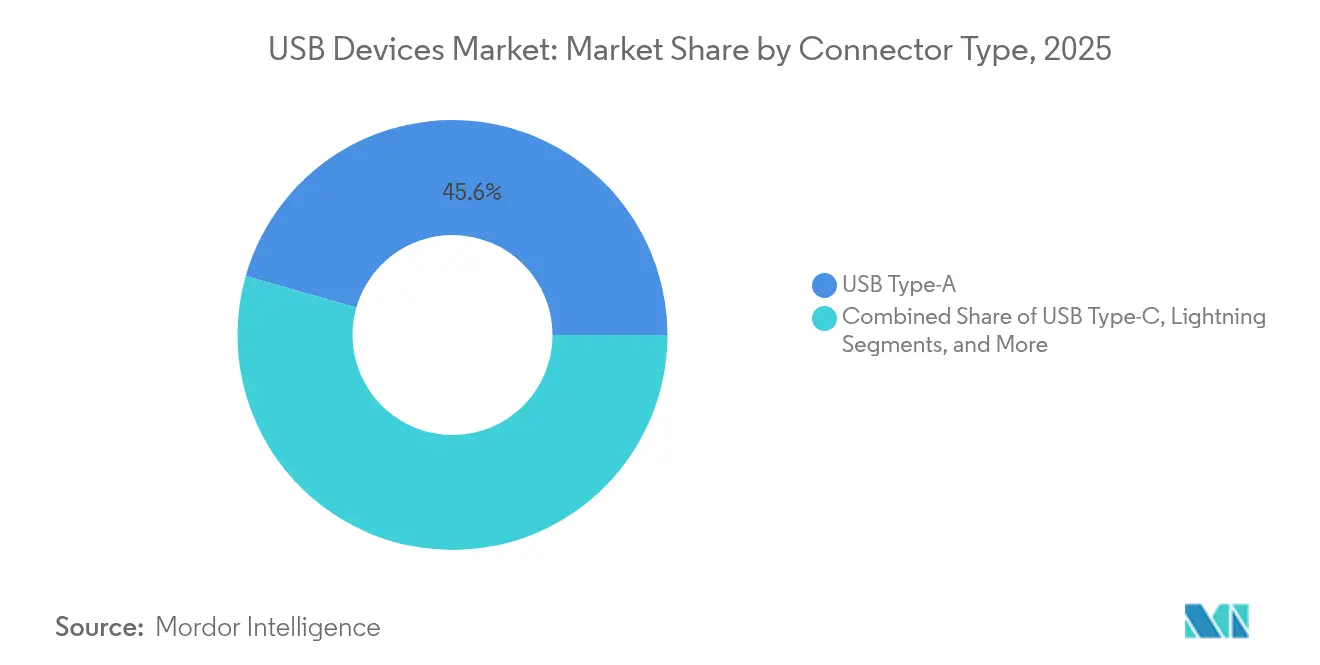

- By connector type, Type-A retained 45.58% share in 2025, while Type-C is advancing at a 14.45% CAGR through 2031.

- By application, automotive infotainment and charging accounted for the highest growth rate of 15.16% CAGR, though consumer electronics maintained 48.05% revenue share in 2025.

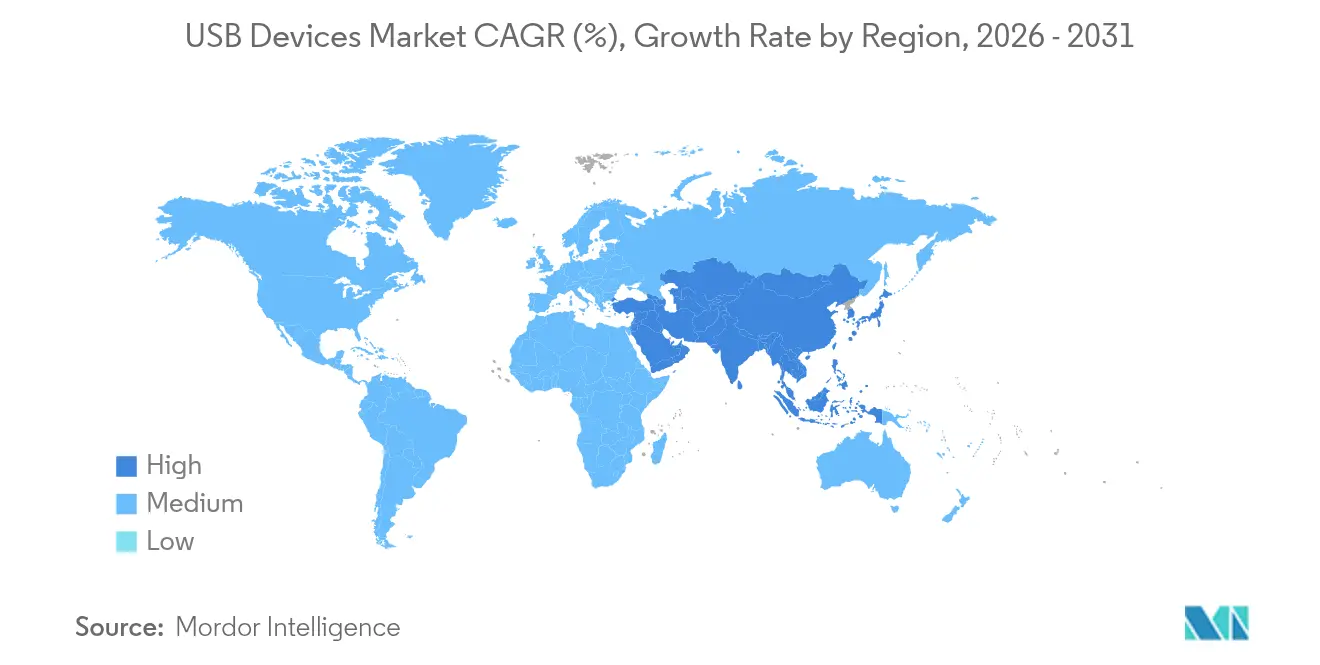

- By geography, Asia-Pacific commanded 52.12% share of the USB devices market in 2025; the Middle East and Africa region is poised for the fastest growth at 14.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global USB Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU and Indian mandates for USB-C | +2.3% | Europe, India, global | Short term (≤ 2 years) |

| In-vehicle fast-charge USB ports > 45 W | +1.8% | Global | Medium term (2-4 years) |

| Hybrid-work demand for webcams and hubs | +1.5% | Global, developed | Medium term (2-4 years) |

| Content-creator shift to USB4 SSD enclosures | +1.2% | North America, Europe, APAC cities | Medium term (2-4 years) |

| Gaming peripherals with low-latency polling | +0.9% | Global, gaming markets | Long term (≥ 4 years) |

| Point-of-care medical devices via USB-OTG | +0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of USB-C Mandated by EU and Indian Charger Regulations

The EU Common Charger Directive came into full effect in December 2024, obliging every portable electronic device to ship with a USB-C port and USB Power Delivery compatibility. Similar rules in India extend the unified charging standard to a consumer base exceeding 1.8 billion, harmonizing design roadmaps for global brands. Manufacturers can now rationalize SKUs, realize scale economies, and cut electronic waste, while users benefit from cables that handle up to 240 W charging and alternate-mode video output. Early evidence of the regulation’s ripple effect is Apple’s move from Lightning to USB-C on the iPhone 15 series.[1]European Commission, “EU Common Charger Rules: Power All Your Devices With a Single Charger,” commission.europa.eu

Growing In-vehicle USB Ports for Infotainment and Fast-Charge (Above 45 W)

Automakers are embedding multiple USB-C ports that deliver more than 45 W, letting passengers power laptops and stream 4K content through integrated entertainment systems. Premium models already employ USB4 controllers rated at 40 Gbps to synchronize media between personal devices and the vehicle’s head unit. Suppliers such as Microchip have introduced automotive-grade USB hubs and power ICs that withstand temperature extremes and electromagnetic interference.[2]Microchip Technology, “USB Products,” microchip.com Fleet operators view reliable charging as a productivity tool, creating steady aftermarket demand.

Remote-Work Video Collaboration Boosting USB Webcams and Hubs

Persistent hybrid-work patterns sustain enterprise spending on plug-and-play conference equipment. Logitech’s MeetUp 2 camera brings AI-driven framing and noise suppression to small rooms over a single USB-C link . Parallel improvements in docking stations support dual 4K monitors, 10 Gbps data, and 100 W power through one cable, shrinking desktop clutter. Corporate IT teams favor models with hardware encryption and remote-management firmware, marrying security with convenience.

Content-Creator Demand for High-Speed USB4 SSD Enclosures

Professional photographers and video editors are shifting workloads to portable SSDs that exploit USB4’s 40 Gbps pipe. Western Digital’s 2 TB and 4 TB offerings cater to 8K editing on location, while Micron’s ninth-generation NAND pushes sustained read speeds to 3.6 GB/s, closing the gap with internal NVMe drives.[3]Western Digital, “Western Digital Showcases New Super Speeds and Massive Capacities for M&E Workflows at NAB 2024,” westerndigital.com The combination of high throughput and compact form factors expands creative flexibility and shortens post-production cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise bans on removable flash drives | -1.4% | Global, regulated sectors | Short term (≤ 2 years) |

| Wireless charging & Wi-Fi 6E file transfer lower port counts | -1.1% | Developed, premium tiers | Medium term (2-4 years) |

| NAND controller & PMIC supply shortages inflate BOM | -0.8% | Global, APAC fabs | Short term (≤ 2 years) |

| Cloud-first endpoints shrink high-capacity thumb-drive demand | -0.6% | Global education, enterprise | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Bans on Removable Flash Drives for Data-Leak Risk

High-profile breaches have led defense agencies and financial institutions to outlaw unencrypted USB storage. Security suites such as Carbon Black Cloud now enable centralized blocking or whitelisting, curbing spontaneous file transfers.[4]Broadcom, “USB Device Blocking,” techdocs.broadcom.com While this policy depresses volumes for generic flash drives, it nudges procurement toward encrypted models with 256-bit AES and remote-wipe functions, partially offsetting the decline.

Shift to Wireless Charging and Wi-Fi File-Transfer Reducing Port Counts

Flagship smartphones now support 25 W MagSafe or Qi2 wireless charging, and Wi-Fi 6E achieves throughput rivaling USB 3.0, diminishing dependence on physical connectors. Device makers exploit the freed internal space to improve water resistance and battery capacity. The impact is concentrated in premium tiers, whereas industrial, medical, and gaming equipment still rely on wired interfaces for deterministic performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Flash Drives Hold Scale, Hubs Accelerate Connectivity

USB flash drives generated 40.12% of 2025 revenue, maintaining dominance because air-gapped transfers and offline backups remain everyday needs in education, media, and government. The segment benefits from low cost per gigabyte and the availability of encrypted models for regulated workflows. Portable solid-state drives with USB4 interfaces are encroaching on high-capacity tiers, yet thumb-drives remain unmatched for convenience. Conversely, hubs and docks are surging at 15.08% CAGR as knowledge workers equip single-cable workstations. These multi-function units combine power delivery, video, Ethernet, and card readers, placing them at the nexus of the USB devices market.

Gamers and content creators continue to lift demand for peripherals such as keyboards, mice, and headsets that leverage higher polling rates to minimize latency. Webcams, once a commodity, now embed AI chips for auto-framing and background blur, securing premium ASPs. Cable and charger units expand steadily because every USB-C device ships with at least one cable. Wireless adapters address niche environments that mandate cord-free setups, while digital audio players face a shrinking footprint as streaming dominates listening habits.

By Device Standard: USB4 Upshifts Performance Ceiling

USB 3.x accounted for 54.35% revenue in 2025, underpinning mainstream peripherals from printers to external drives. The standard will keep mass-market relevance due to favorable cost and broad chipset availability. However, USB4 is projected to outpace at 15.72% CAGR as professionals and gamers demand 40 Gbps bandwidth and 240 W power over a single connector. Early USB4 laptops pair with Thunderbolt 5 controllers to unlock daisy-chained 8K displays, spurring complementary sales of compliant cables and hubs.

USB2.0 endures in mouse, keyboard, and microcontroller applications where 480 Mbps suffices. Legacy USB1.1 holds niche industrial installs focused on validated reliability. Certification complexity for USB4 devices creates a services opportunity for test-equipment providers, while silicon vendors compete on power-efficiency metrics to manage thermal limits in thin-and-light devices.

By Connector Type: Type-C Takes Center Stage

Type-C ports are advancing at 14.45% CAGR, propelled by global charger mandates and inherent ease of use. The reversible plug, alternate-mode video, and high-power capability make it the default choice for phones, tablets, and laptops. In-vehicle infotainment, smart home hubs, and even power tools are migrating to ruggedized Type-C receptacles that survive vibration and dust. Despite the surge, Type-A still owns 45.58% of 2025 shipments, anchored by billions of legacy hosts and peripherals in homes, offices, and factories.

Type-B connectors remain present in niche equipment such as 3D printers and laboratory instruments that value mechanical robustness. Micro-B survives in cost-sensitive wearables and IoT sensors but is losing share steadily. Apple’s proprietary Lightning interface is in sunset mode as newer iPhone generations adopt Type-C to satisfy regulatory requirements.

By Application: Automotive Emerges as High-Growth Anchor

Consumer electronics delivered 48.05% of market demand in 2025, spanning smartphones, tablets, PCs, and wearables. The segment remains foundational but is maturing. Automotive infotainment and charging is forecast to climb at 15.16% CAGR, driven by electric vehicle adoption and passenger expectations for seamless connectivity. USB-C outlets in rear seats now power gaming handhelds and stream media directly to central displays.

IT and telecom infrastructure deploy USB ports for device configuration, firmware flashing, and out-of-band management. Healthcare equipment integrates USB-OTG to enable portable diagnostic probes and secure data offload in clinics. Industrial automation leverages ruggedized hubs to connect sensors on factory floors, while aerospace and defense specify hardened connectors resistant to vibration and temperature extremes. Each vertical demands tailored designs, broadening the total addressable USB devices market.

Geography Analysis

Asia-Pacific dominated with 52.12% revenue in 2025, underpinned by China’s manufacturing density, South Korea’s memory expertise, and Japan’s precision component base. Contract manufacturers in Vietnam and India are absorbing overflow orders as brands diversify supply chains for resilience. Gaming cafés and mobile-first consumers in the region exert steady pull for high-performance peripherals and chargers. Government mandates in India for USB-C reinforce the regional transition and align local ecosystems with global norms.

Europe’s regulatory stance makes it a bellwether for connector standardization and sustainability. The EU directive trimmed charger e-waste volumes and prompted vendors to develop durable, repairable cables. Germany’s Industry 4.0 initiatives anchor demand for industrial-grade USB components. Semiconductor expansion such as Nexperia’s USD 200 million wide-bandgap plant in Hamburg helps stabilize local component availability for next-generation hubs and power adapters.

North America exhibits premium demand characteristics. Content creators in the United States adopt USB4 SSDs to accelerate video workflows, while enterprises look for encrypted drives and remote-managed docks. Canada’s AI research community needs fast external storage, and Mexico’s electronics clusters gain momentum as near-shore assembly options. The Middle East and Africa region, although smaller, leads in relative growth at 14.88% CAGR through 2031. Smartphone penetration, smart-city projects, and edge computing roll-outs drive fresh installations of USB-enabled IoT gateways across Gulf Cooperation Council economies and South Africa’s metro areas.

Competitive Landscape

The USB devices market displays moderate fragmentation. Kingston, SanDisk, and Samsung capture the bulk of flash-drive and portable SSD revenue by harnessing vertically integrated NAND capacity. Micron’s ninth-generation NAND delivers 3.6 GB/s sustained reads, positioning the firm for high-performance USB4 enclosures. Logitech secures 35% share in computer mice and 42% in webcams through continuous innovation and a CHF 330.4 million annual R&D budget.

Peripheral specialists like Razer and Corsair carve premiums in gaming by marketing low-latency polling and customizable RGB lighting. Anker and UGREEN master the mid-price charging and hub niche, relying on e-commerce visibility and rapid refresh cycles. With USB4 and 240 W power delivery gaining ground, chipset providers such as Texas Instruments and Infineon expand reference designs, while cable vendors compete on e-marker reliability and bend durability. Automotive-grade connectors and industrial USB gateways remain lightly contested, presenting entry opportunities for firms with application-specific engineering depth.

USB Devices Industry Leaders

Kingston Technology

SanDisk

Transcend Information Inc.

Samsung Electronics Co

Toshiba Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Micron committed USD 200 billion to expand domestic memory manufacturing and R&D, targeting 40% of global DRAM production in the United States.

- May 2025: Micron introduced Crucial T710 PCIe Gen5 NVMe SSD and X10 Portable SSD, pushing external USB storage to 8 TB and 14,900 MB/s read speeds.

- February 2025: Micron shipped 1γ DRAM at 9,200 MT/s, cutting power use by 20% versus prior nodes.

- January 2025: Western Digital launched SanDisk Creator USB-C Flash Drive and related products at CES 2025.

- January 2025: Infineon broke ground on a backend fab in Thailand to boost supply of power modules vital for USB chargers.

Global USB Devices Market Report Scope

USB is a standard and widely used interface that enables easy connectivity between electronic devices, allowing efficient data transfer and power delivery. Its standardized design has improved device compatibility by providing a universal solution for connecting peripherals such as external storage devices, printers, and input tools like keyboards and mice. USB technology has advanced significantly, from its initial focus on basic connectivity to supporting high-speed data transfer, video output, and power delivery in modern versions like USB Type-C.

The USB devices markets is segmented by product (webcam, USB flash drives, digital audio players, computer peripherals, others), by device type (USB 2.0, USB 3.0, USB 4.0), by connector type (type b, type c, lightning connectors), by application (IT & telecommunication, automotive, consumer electronics, healthcare & medical devices, others), by geography (North America [United States, Canada, Mexico, and Rest of North America], Europe [Germany, United Kingdom, France, Spain, and Rest of Europe], Asia-Pacific [India, China, Japan, New Zealand, Australia and Rest of Asia-Pacific], Latin America [Brazil, Argentina, and Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, and Rest of Middle East and Africa]).

The report offers market forecasts and size in value (USD) for all the above segments.

| Webcams |

| USB Flash Drives |

| Digital Audio Players |

| Computer Peripherals (Keyboards, Mice, Headsets) |

| USB Hubs and Docks |

| USB Cables and Chargers |

| Wireless USB Adapters |

| Others |

| USB 1.1 |

| USB 2.0 |

| USB 3.0/3.1 Gen 1 |

| USB 3.2 Gen 2 |

| USB4 and Above |

| Type-A |

| Type-B |

| Micro-B |

| Type-C |

| Lightning |

| Consumer Electronics |

| IT and Telecommunication |

| Automotive Infotainment and Charging |

| Healthcare and Medical Devices |

| Industrial Automation and IIoT |

| Aerospace and Defense |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product | Webcams | ||

| USB Flash Drives | |||

| Digital Audio Players | |||

| Computer Peripherals (Keyboards, Mice, Headsets) | |||

| USB Hubs and Docks | |||

| USB Cables and Chargers | |||

| Wireless USB Adapters | |||

| Others | |||

| By Device Standard | USB 1.1 | ||

| USB 2.0 | |||

| USB 3.0/3.1 Gen 1 | |||

| USB 3.2 Gen 2 | |||

| USB4 and Above | |||

| By Connector Type | Type-A | ||

| Type-B | |||

| Micro-B | |||

| Type-C | |||

| Lightning | |||

| By Application | Consumer Electronics | ||

| IT and Telecommunication | |||

| Automotive Infotainment and Charging | |||

| Healthcare and Medical Devices | |||

| Industrial Automation and IIoT | |||

| Aerospace and Defense | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the USB devices market?

The USB devices market size is USD 47.25 billion in 2026.

How fast is the USB devices market expected to grow?

The market is forecast to expand at a 14.44% CAGR, reaching USD 92.61 billion by 2031.

Which product category leads the USB devices market share?

USB flash drives lead with 40.12% share in 2025.

Why is USB-C adoption accelerating worldwide?

Regulatory mandates in the EU and India plus technical advantages like reversible plugs and 240 W power delivery drive rapid USB-C adoption.

Which application segment is growing the fastest?

Automotive infotainment and charging leads growth with a projected 15.16% CAGR through 2031.

What regions show the highest growth potential?

The Middle East and Africa region is projected to grow at 14.88% CAGR through 2031 thanks to smartphone adoption and infrastructure investments.

Page last updated on: